Key Findings

- The tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. is shrinking for traditional excise taxes, including tobacco, alcohol, and motor fuels. These sources of revenue are unstable and work poorly as a source to fund growing expenditure programs.

- Newer excise taxes—including those on carbon, cannabis, alternative tobacco products, ride-sharing, and plastics—have the potential to significantly affect global trade and increase the percent of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue generated by excise taxes.

- For most excise taxes, the best choice of tax base is the externalityAn externality, in economics terms, is a side effect or consequence of an activity that is not reflected in the cost of that activity, and not primarily borne by those directly involved in said activity. Externalities can be caused by either production or consumption of a good or service and can be positive or negative. -causing agent, as that provides the best target for external costs.

- Excise taxes should ideally be levied early in the value chain. Limiting the number of taxpayers lowers the cost of enforcement and improves compliance, making tax implementation less costly and more efficient.

- Revenues from excise taxes should be spent on those social expenses (e.g., infrastructure costs associated with driving, and enforcement costs related to alcohol). Excise taxes should not be levied to raise general fund revenue because the tax bases are typically narrow and unstable.

- Excise taxes should take harm reduction into account to minimize the costs of excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. policy and maximize well-being.

Introduction

Excise taxes are a well-established component of global tax policy. Excise taxes are used to generate government revenue while providing incentives for market participants to consume and produce less harmful products. With proper design and implementation, excise taxes can improve overall well-being and fund public programs to improve market outcomes. Poor implementation of excise tax policy, however, can create an environment in which people are worse off than if no policy had been implemented in the first place.

Excise taxes are selective consumption taxes levied on targeted products or activities. The excise tax is added on top of other broad-based taxes like value-added taxes (VATs) or sales taxes. The selective nature of the excise taxes provides a narrow tax base. That narrow base must be justified by unique costs or considerations related to the taxed activity.

Excise taxes are sometimes referred to as “sin taxes” because they are often levied on products whose consumption is considered socially undesirable. Today, targets for selective excise taxes include products that are unhealthy for the user, create negative outcomes for third-party bystanders (negative externalities), generate burdens on public expenditures (which I will call “governalities”), or act as a user fee for accessing publicly funded goods or services. Many products slated for excise taxes trigger more than one of the motivations for selective taxation.

A variety of tax structures are used as excise taxes. Excise taxes can be applied per unit—selectively or ad quantum—or as a percentage of the price or value—ad valorem. The taxes can be levied at different points in the production process, including at the point of sale to the consumer, during wholesale transactions between businesses, or at the manufacturer when production is complete. Specific taxes can target different parts of the product, including raw materials, product ingredients, the weight of a product, the quantity of a product, or combinations of the above. In this paper, we explore existing tax structures and evaluate the best practices for using excise taxes on a range of products.

Traditional targets of excise taxes, including alcohol, tobacco, and fuel, have well-established tax rates and policies. Recent years have seen a pronounced shrinking of the tax base for these products.

Meanwhile, new excise taxes, such as those on carbon, cannabis, alternative tobacco products, ride-sharing, and plastics have the potential to significantly affect global trade and increase global excise tax revenues. Within each country, the revenues from a carbon taxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them. alone could exceed the revenues from all other excise taxes.[1]

This paper details a principled approach to selective excise taxation and explores recent trends and applications of global excise taxation. The first section describes excise taxes and how they are used. The second section describes what goes into designing effective and efficient excise taxes. The third section describes taxes on traditional excise products, while the fourth section details emerging and growing excise tax categories. Finally, the paper concludes with a summary and outline of best practices for excise taxes.

Table of Contents

- Excise Taxes Are Ubiquitous

- Excise Tax Design and Considerations

- — Textbook Taxation to Practical Policy

- — Simplicity, Transparency, Neutrality, and Stability

- — Tax Base

- — Tax Rate

- — Revenue Allocation

- — Regressivity

- — Harm Reduction and Well-Being

- Traditional Excise Categories

- — Alcohol

- — Tobacco

- — Fuel

- New Excise Taxes and Trends

- — Carbon

- — Cannabis

- — Alternative Tobacco Products

- — Sugar-Sweetened Beverages

- — Ride and Car-Sharing

- — Plastic and Extended Producer Responsibility

- Summary and Principles for Excise Tax Design

Excise Taxes Are Ubiquitous

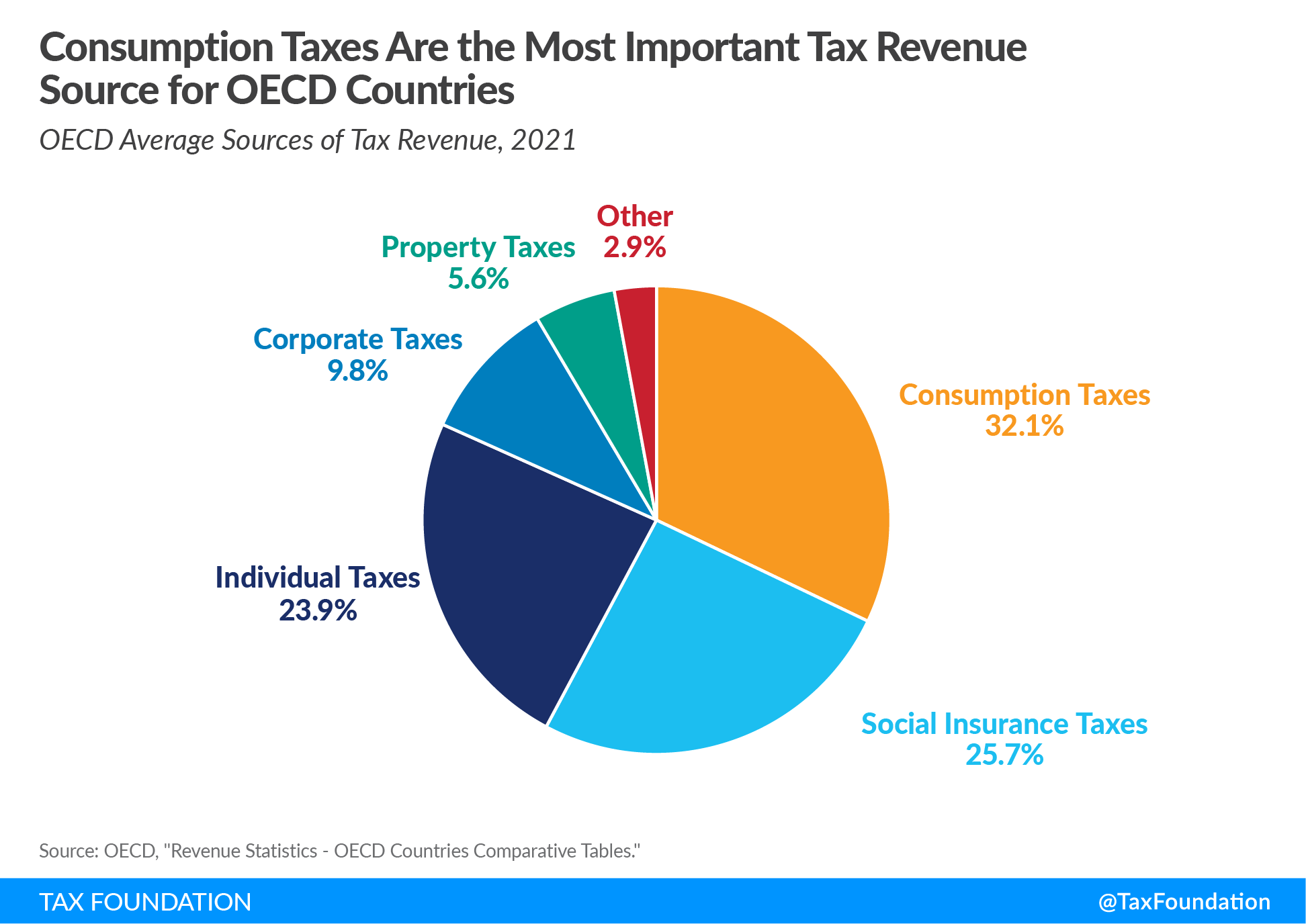

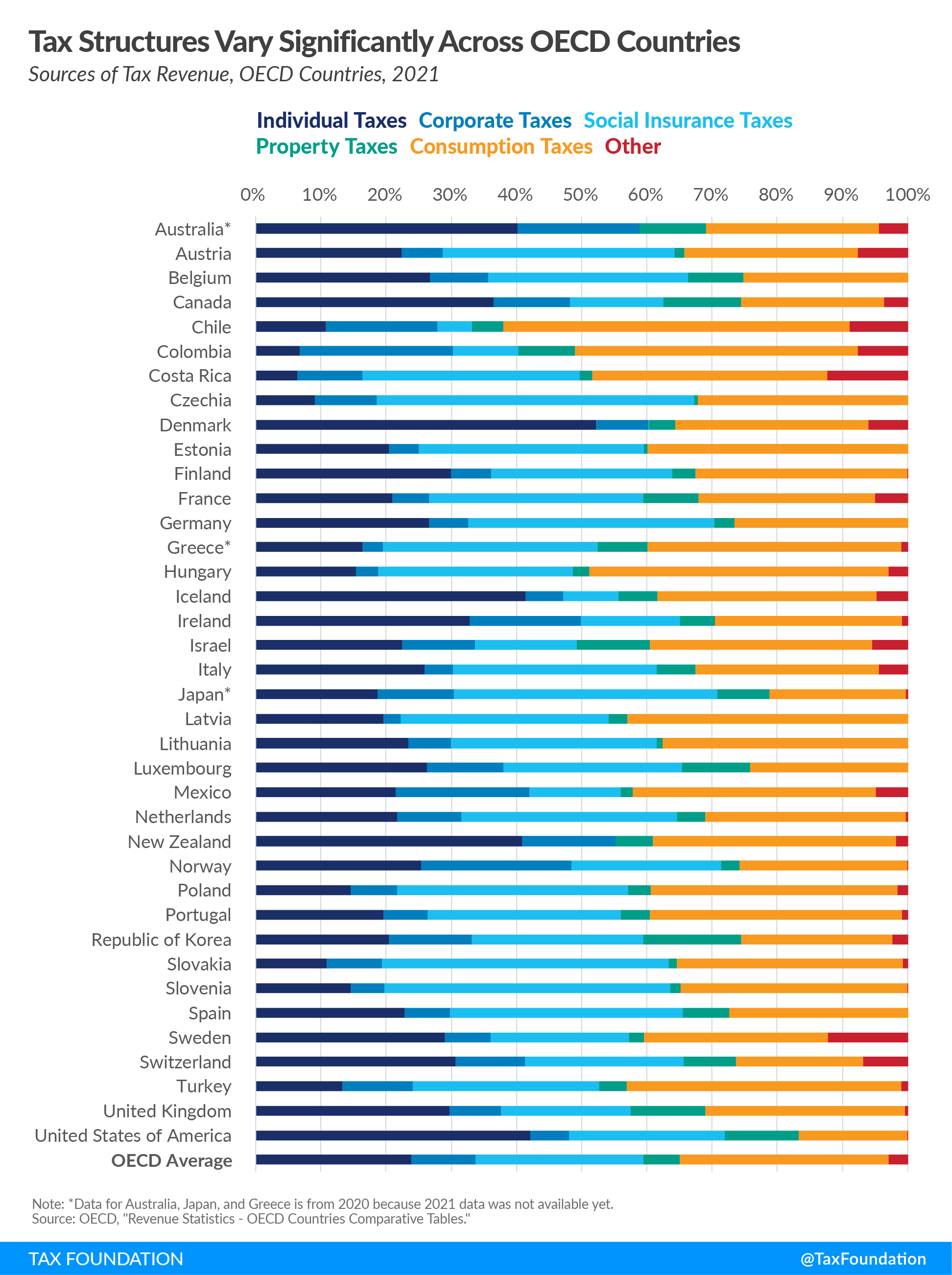

Excise taxes are a type of consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible. used around the globe. Across the Organization for Economic Co-operation and Development (OECD), consumption taxes are the largest source of government revenue.

Each country in the OECD uses consumption taxes, but reliance on consumption taxes varies. Consumption taxes account for more than half of government revenue in Chile, at 53.1 percent. They account for less than 20 percent of revenues in Switzerland—19.6 percent—and the United States—16.6 percent.

Most consumption tax revenue is generated by broad-based taxes such as VATs. Excise taxes are a major component of consumption taxes in many countries, however. At least 170 countries across the globe levy some sort of excise tax. Modern excise taxes come in a variety of forms, but excise taxes are one of the oldest kinds of taxes on record.

History’s first documented tax is from ancient Egypt around 3000 B.C. The focal point of Egyptian tax collection was an excise tax on the quantity of grain produced, but taxes were also levied on heads of cattle and liquid measures of oil and beer. Excise taxes first appeared in western Europe in the early 17th century and the first national excise tax in the United States was levied in 1791 on whiskey.

Historically, the primary motivation for excise taxes was the raising of government revenue. Governments needed tangible items that could be taxed. Non-necessities made relatively attractive targets. In the book that launched the modern field of economics in 1776, An Inquiry into the Nature and Causes of the Wealth of Nations, Adam Smith wrote, “Sugar, rum, and tobacco are commodities which are nowhere necessaries of life, which [have] become objects of almost universal consumption, and which are therefore extremely proper subjects of taxation.”[2]

Smith emphasizes that these products are ideal for taxation partly because they are of almost universal consumption. Of course, at the time the book was written, the British Empire relied on land taxes, stamp duties, customs duties, and excise taxes—not income taxes, general sales taxes, or many of the other broad-based taxes we are familiar with today.

Today, these goods are not universally consumed, and we have far broader bases and easier collection methods for tax revenue. Modern excise taxes thus rely on Smith’s point that these products are nowhere necessaries of life. Many of the products may even be harmful to users and bystanders. Thus, modern excise taxes are often implemented to try to deter the consumption of certain goods.

Basic economics dictates that as (tax-induced) prices go up, (legal) consumption falls. What follows this fundamental law of demand are questions and considerations that form the foundation for tax design: By how much will consumption fall? How much revenue will the tax generate? Who is consuming less? Who is bearing the burden of the tax? To what will people switch if they stop consuming? Will a tax create illicit markets? Are the net effects of the tax better than if no tax were put in place at all?

Excise Tax Design and Considerations

Excise tax design faces trade-offs like all tax and public policy. An underlying goal of tax policy is revenue generation. Unlike broad consumption and incomes taxes, where the disincentivized taxed activity results in societal loss—income taxes, for example, penalize working and the decrease in work caused by income taxes results in less production and an overall decline in well-being—the targets of many excise taxes have negative external effects, meaning that a reduction in market output could improve overall well-being. Poorly designed excise taxes, by contrast, may penalize certain classes of consumption arbitrarily, or even discourage consumers from shifting to products with fewer harms or externalities.

The design of excise tax systems is important. Well-designed taxes generate revenue with far less societal impact than poorly designed taxes.

The outcome of excise taxation should be to improve the lives of taxpayers and non-taxpayers alike. The best design for excise taxes is often simple in theory, but in a world with imperfect information and challenging implementation, several rules can guide tax policy to a point where, even if not perfect, tax policy still delivers reliable tax revenue and reduces harm.

Textbook Taxation to Practical Policy

The on-paper public policy solution for products that create an externality can be found in almost every introductory economics textbook. Pigouvian taxes and subsidies are named after economist Arthur Pigou, who penned the policy prescription in 1920. Pigou concluded that if a product produced some external harm/benefit, the market could move to an optimal output by the addition of a tax or subsidy in the amount of the harm/benefit. If a gallon of gasoline creates $1 of external harm, adding a $1 tax to each gallon would decrease the market quantity to an optimal, lesser amount. A subsidy would likewise increase the production and consumption of products with positive external benefits.

The general framework based on Pigouvian principles is still the premise for government’s use of excise taxes today, apart from governalities, as many the government programs responsible for goernalities didn’t exist in 1920. Examples of products taxed for Pigouvian purposes include alcohol taxes due to the external harms of alcohol consumption (e.g., drunk driving, domestic violence, and property damage), carbon taxes due to climate change, and plastic taxes due to environmental harms.

The textbook solution to negative externalities via Pigouvian taxes assumes information not necessarily available to policymakers and unfortunately ignores certain key features of practical tax policy. First, Pigouvian taxes assume the knowledge of the exact amount of social costs. Even for products where there is a general consensus that a social cost exists, estimates of the precise magnitude of those costs often vary widely. We present a wide range of estimates for the social costs per ton of carbon emissions later in this paper, for example.

In other cases, such as the development of new products or a product with a wide array of social effects, there may be few or no estimates of social costs available. The academic literature on cannabis is very young, without a consensus on the external harms of cannabis consumption. The resulting tax landscape is chaotic, absent an academically-supported universal foundation for tax policy.

Pigouvian solutions are also static in a world of constant change. Innovations and consumer preference shifts can completely alter the markets and change the social costs of the product. This would suggest that ideal Pigouvian taxes would change instantly in response to market fluctuations.

Similarly, Pigouvian taxes make no reference to the political economy involved in fiscal policy. Constantly changing tax rates would be infeasible. Political factors including the distributional effects of the tax burden and the ways in which the revenue from these taxes is spent further create a disconnect from the policy on paper to the real world.

Imperfect information and political barriers create enormous barriers to the practical implementation of Pigouvian taxes. As such, we can build off the foundation laid from Pigouvian insights, but we must extend those insights to provide both a robust set of guiding principles for tax policy and then specially cater tax design based on the characteristics of each product

Simplicity, Transparency, Neutrality, and Stability

All tax policy should be guided by the principles of simplicity, transparency, neutrality, and stability. Tax policies that are simple, transparent, neutral, and stable are easier to understand for taxpayers and governments. They are not wildly distortive, and they provide consistent, predictable, and equitable sources of revenue to fund public expenditures over time.

For simplicity, excise taxes should ideally be levied early in the value chain because this generally results in a smaller number of taxpayers. Limiting the number of taxpayers reduces the cost of enforcement and lowers the barriers to tax compliance, making the tax relatively efficient. This is easiest for excise taxes that are levied at a specific rate (e.g., $1.00 per pack of 20 cigarettes). The tax bill can be applied based on quantity and remitted by the limited number of manufacturers, as opposed to needing to be remitted by every consumer or every point-of-sale vendor.

Ad valorem rates (a percentage of value or sales price) should also be levied early in the production process to limit the number of taxpayers. The challenge to applying ad valorem taxes early in the production chain is that true market values may not be established until the final point of sale retailer. Market power at the wholesale or retail level, or vertical integration in a supply chain, can distort transaction prices prior to market sales. Market value is best reflected in the final sales price to customers, but levying a retail excise tax multiplies the number of taxpayers significantly. This will increase the cost of tax enforcement and is one reason that many federal governments do not levy excise taxes at the retail level.

For internationally traded products, simplicity means taxing at the port of arrival, levied at the same time as any tariffs. Taxes should be based on the destination jurisdiction’s rate and should match the rates of that country’s domestically manufactured goods.

For tax transparency, specific taxes tend to be more transparent than ad valorem, as the taxpayer more easily can identify the tax burden. The posted retail sales price will also be better-reflective of the final purchase price and incorporate the tax burden if taxes are levied early in the supply chain, allowing consumers to price in the tax as part of their purchasing decision and face fewer tax-induced surprised at checkout.

To increase the transparency of taxes levied prior to the point of sale, vendors can report out aggregate tax levied on the transaction on a receipt for consumers to review after purchase. Like simple taxes, transparent taxes are easier to comply with for taxpayers and tax administrators.

While excise taxes can be simple and transparent, they are not neutral. Neutral taxes, often with broad bases and low rates, minimize market distortions and facilitate decisions based on economic merits and not tax reasons. Excise taxes are targeted and designed specifically to impact decisions made by consumers.

Nevertheless, excise tax design should strive to be as neutral as possible within the taxed category. This is achieved by levying the tax on the best available proxy for the externality or cost. Doing this ensures that, for instance, two beers with the same alcohol content will have the same tax burden and two different brands of combustible cigarettes will have the same tax burden. By designing the tax to capture the externality, lawmakers guarantee that separate, non-problematic product design qualities will not affect tax levels.

The final design principle is stability. Given their narrow and often shrinking tax base, revenue from excise taxes lack long-term stability. Consider tobacco taxes. Tobacco consumption has been declining for decades, leading to a gradual decrease in revenues. Most countries and subnational governments have continued to ratchet up rates, which increase revenue immediately, but then revenues continue their downward trend. The result is a volatile source of revenue.[3]

Because excise taxes are non-neutral and provide an unstable source of revenue, they should be limited to cases where they can capture some externality or create a “user pays” system—not relied upon for general revenue.

Tax Base

The first question to ask in tax design is what will be taxed. The total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation is called the tax base.

In cases where an excise tax is levied as a user feeA user fee is a charge imposed by the government for the primary purpose of covering the cost of providing a service, directly raising funds from the people who benefit from the particular public good or service being provided. A user fee is not a tax, though some taxes may be labeled as user fees or closely resemble them. , the tax base should be the best available proxy for use. For instance, consumption of motor fuel acts as a proxy for drivers’ use of public roads.[4] In the future, some other proxy may prove superior; a vehicle miles traveled (VMT) tax has certain advantages as a proxy, for instance, though it raises legitimate privacy concerns. Nevertheless, motor fuel is a far better proxy for contributions to road use than simply taxing vehicle registration.

For excise taxes that target harm-generating products, the tax base should target the harm or external cost-causing element. Targeting the harm-causing element best allows market participants to “internalize the externality” or incorporate any external effects into their decision-making. For example, a tax placed on carbon emissions can price in external damages from pollution and climate change into energy consumption and production decisions.

Quantity-based specific taxes also help better align the tax base to the tax’s purpose than do ad valorem taxes for both user fees and externalities. The number of gallons of gasoline used better approximates road usage and emissions produced than the price paid per gallon. Similarly, the number of cigarettes smoked or the amount of alcohol consumed has a much clearer connection to any harm caused by this consumption than the retail sales price of the products.

Specific taxation is often simpler because the tax can be calculated based on weight, volume, or amount instead of an estimated value. This is especially true as products often flow between different layers of a vertically integrated company (for instance a beer brewer that also operates as a wholesaler) and as such does not have a clear market value to tax. If a tax is levied on value, the taxpayer or taxing entity must compute an artificial value to tax if the tax is not levied at the retail level (which few federal excise taxes are due to the number of taxpayers this would involve). Although rules exist for making this computation, it can create problems or perverse incentives—some of which are known as transfer pricing.[5]

Ad valorem taxes are more appropriate in certain circumstances, however. In sports betting, for example, the potential harm of betting is best expressed by the size of the bet. In other cases, the harm-causing agent can be difficult to quantify. Based on current technology, the amount of tetrahydrocannabinol (THC) in raw cannabis products is difficult and expensive to measure and can vary from plant to plant. Thus, a THC-based tax is difficult to apply and administer. In these cases, either a weight-based ad quantum tax or an ad valorem tax may be more effective (despite inherent limitations), or a hybrid model can be used until harm measurement can be more easily quantified.

Naturally, consumption alternatives that do not create negative externalities should not be included in the tax base. Coal-generated electricity emits carbon dioxide, making it an appropriate target for a carbon tax, whereas wind-generated electricity produces no carbon emissions and should be excluded from a carbon tax. There is a clear distinction between a tax on carbon and a tax on electricity. Identifying the proper tax base is essential if excise taxes are to be efficient and improve upon non-tax market outcomes.

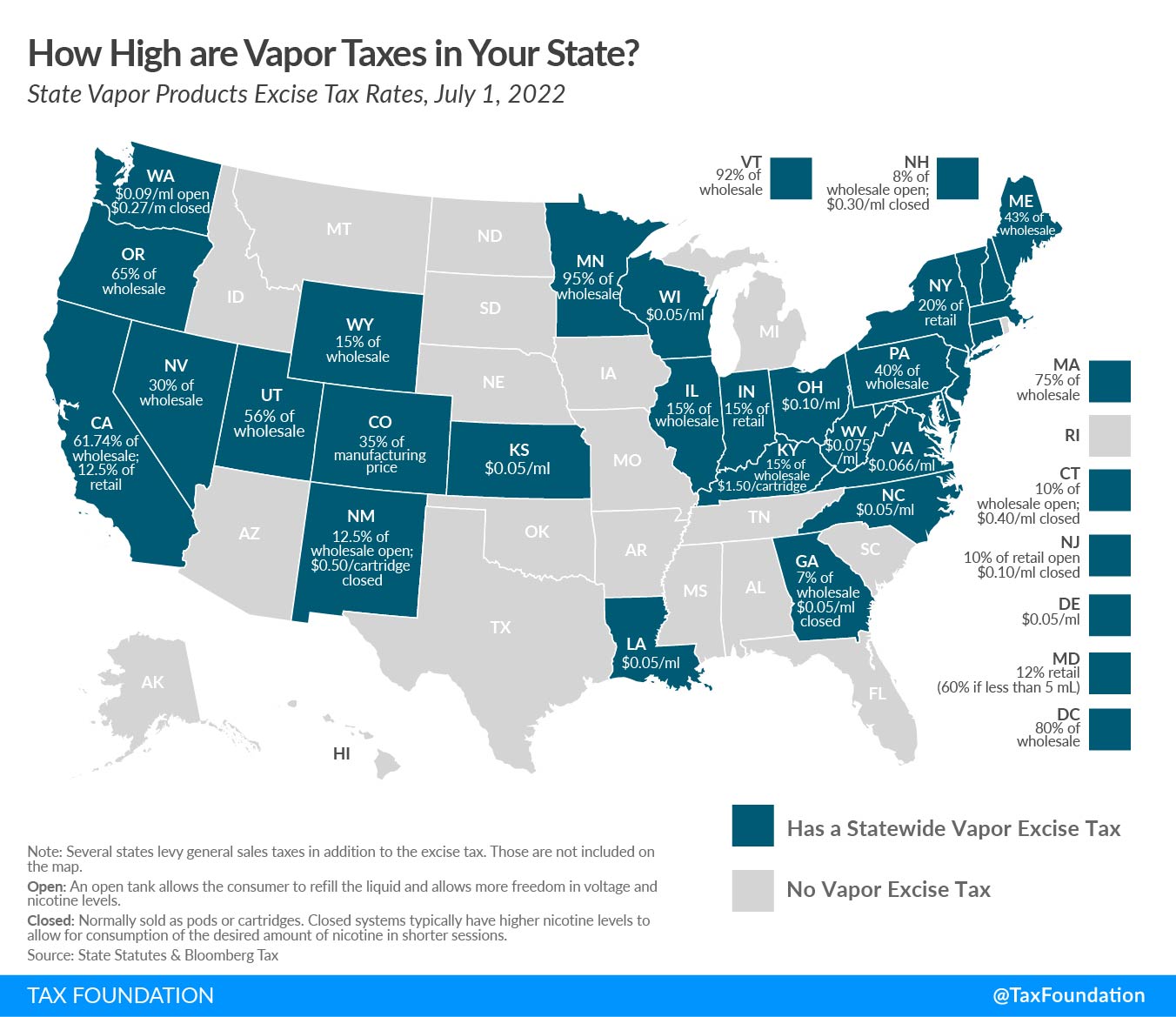

Including substitute goods in the tax base can discourage desirable substitutions from more harmful goods to less harmful ones. Two examples, discussed in more detail later, are taxes on vapor products and on other cigarette alternatives. Despite their significantly lower harm profile, these products are too often taxed as tobacco products. To encourage harm-reducing behavior, tax burdens should reflect differences in harm.

Directly targeting the externality also helps promote tax neutrality. France used to apply one excise tax rate on grain-based alcohol products like gin and whiskey and another lower rate on grape-based alcohol products like cognac. This practice, which favored domestically produced products over imports, was stopped by the European Court of Justice. The simpler, neutral approach would have been to levy a tax on alcohol content by volume, making the rates similar on cognac and gin.[6]

For practical implementation of excise taxes, a clear, well-defined tax base is essential. Poorly written tax base definitions can lead to the disproportionate treatment of similar products. In a recent example from the United States, in the state of Wisconsin, a “vapor product” was defined as a “noncombustible product that produces vapor or aerosol for inhalation from the application of a heating element to a liquid or other substance that is depleted as the product is used, regardless of whether the liquid or other substance contains nicotine.” Lawmakers in the state applied a tax where the tax rate was determined by milliliter of liquid, but the definition of a vapor product clearly referred to vaping equipment. As a result, a tax is only levied on products where vapor liquid and equipment were bundled together.[7]

Tax Rate

When a suitable tax base has been established, the next element of tax design is selecting the tax rate. The excise tax rate should be determined by several factors, first and foremost being the negative externalities or costs the tax is serving to internalize or recoup. Precise individual-specific estimates of social costs are difficult, so we often resort to using estimates of average social costs.

These calculations are relatively straightforward for some excise categories (e.g., the average cost of a mile driven by an average car on an average road). And because most roads are built with public funds, the costs incurred for road construction and maintenance are well-documented. (Even here, of course, the selected measure—motor fuel—cannot account for relevant factors like curb weight and number of axles.)

Other products taxed by excises are more difficult to quantify and assign costs. For instance, society is very unlikely to incur costs from a person drinking a glass of wine a week. Not until that person becomes a heavy user does she impose costs on society, and yet the excise rate is the same for the first glass as it is for the 10th. While using average costs to help set rates does overcharge responsible drinkers, heavy drinkers will still face a greater tax burden and disincentive to drinking.

Ad valorem rates have built-in inflation adjustments. As prices increase, so do tax collections. Specific taxes don’t have this mechanism. Consequently, specific taxes should be indexed for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. , but only if the costs associated with the product’s consumption increase over time. Road maintenance costs tend to increase with inflation, so specific fuel taxes should logically be indexed to inflation. The incredible decline in alcohol-related driving fatalities in certain countries—due in large part to the availability of ride-share technology—may have decreased the overall social costs of alcohol consumption, suggesting rates could actually decrease.

Other considerations that should go into establishing excise tax rates are market conditions, available economic substitutes, and the general tax burden. Market conditions play a particularly important role for products that compete with the illicit market. For example, recreational marijuana retailers not only compete with each other, but also with illegal operators. The same is true for both sports betting services and tobacco retailers.

Considering economic substitutes is important because a tax that is too narrow will not be neutral and simple consumer substitution may negate intended benefits from a tax. Consider excise taxes applied only to soda with the intention of decreasing total caloric consumption and reducing public health expenditures related to obesity. Academic studies find that after a soda taxA soda tax is an excise tax on sugary drinks. Most soda taxes apply a flat rate per ounce of a sugar-sweetened beverage. people drink less soda, but they substitute elsewhere and do not decrease their overall caloric consumption. Bans can have similar effects: in one specific instance, soda was banned from a public school and children switched to drinking more chocolate milk.[8]

Finally, as lawmakers decide on tax rates, they should consider the overall tax burden for their citizens. Excise taxes are typically imposed in addition to general sales taxes, individual and corporate income taxes, property taxes, and other kinds of taxes. Because of the narrow base, excise taxes make poor tools for funding broad government expenditures. Even where an excise tax is economically rationalized, excessive taxes on businesses can impair economic growth, job creation, and wages.

Revenue Allocation

Revenue from excise taxes should be allocated to cover societal costs related to the consumption of the taxed products. Some examples include funding health costs related to smoking, infrastructure costs associated with driving, anti-addiction programs, and enforcing bans on alcohol-impaired driving. Allocating revenue to cover the cost associated with the consumption of excised goods increases the taxpayers’ understanding of the tax and may be able to decrease social costs over time.

The fraction of revenue dedicated or “earmarked” to an expenditure category varies widely by tax type and jurisdiction. In Europe, many environmental taxes are earmarked for environmental expenditures. The Dutch water pollution tax, for example, is used to finance the sanitization and purification of water.[9]

Globally, the World Bank reports that at least 80 countries earmark some portion of their revenue to health spending. The most common earmarks are income or payroll taxes to fund health care or pensions. The next most popular sources of earmarks are revenues from tobacco, alcohol, and unhealthy foods.[10]

In the United States, only about half of all tobacco tax revenue is earmarked for an expenditure purpose. The expenditures to which the revenues are earmarked range from the obvious—health care (60.8 percent of all earmarked tobacco revenue) and social services (18.4 percent)—to the less theoretically connected—capital projects (4.4 percent) and debt payments (1.5 percent). Tobacco control receives less than 1 percent of earmarked tobacco revenues.[11] Lawmakers in 25 U.S. states divert a significant amount of revenue raised from motor fuel taxes to unrelated spending programs like education (Kansas and Texas), tourism (Utah), or wildlife conservation (Florida).[12]

Improper alignment of expenditure programs that grow over time with excise tax revenue sources creates a problem. Well-designed excise taxes discourage use (e.g., less smoking, fewer carbon emissions, etc.), resulting in a shrinking tax base over time.

In the UK, for example, as fewer consumers smoke and drink, tobacco and alcohol collections have declined. The several-decade trend of shrinking tax bases means that tobacco now makes up just 1 percent of total public sector receipts, down from 1.9 percent two decades ago, and alcohol revenues make up 1.3 percent of receipts, down from 1.7 percent.[13]

If the revenues are dedicated directly to expenditure programs to help alleviate the social costs of consumption, there should be no problem with a shrinking tax base. Less consumption would mean fewer social costs and less need for tax-funded expenditures.

Often, however, governments use these revenues for general expenses or special projects unrelated to the tax. In the United States, the state of Colorado earmarks funds from an excise tax on online sports gaming to be spent on its Water Plan. When volatile gaming revenue missed projections in 2022, the state had difficulty funding water infrastructure projects. The state then followed up with a redesign of its gaming tax, with a higher effective tax rate.

A common response is for political calls to increase the tax rate to offset revenue loss from a shrinking or volatile excise tax base. Unless the social costs of the activity increased, such calls are economically unfounded. Shrinking tax bases only present a major problem for expenditure programs that are poorly connected to an excise revenue source.

In Europe, serious fiscal questions loom as the EU pursues a 55 percent reduction in carbon emissions by 2030. Energy taxes are the primary tool currently proposed for pursuing reduced carbon emissions. However, the more successful the transition away from carbon fuels becomes, the more the carbon fuel tax base will shrink, generating lower revenues to pursue technologies and alternative energy investments. To the extent that this is a mark of success, that may not be a problem—but if lawmakers come to count on the resources for broader expenditures, success at decarbonization can generate revenue shortfalls.

Regressivity

Excise taxes are regressive because the tax comprises a larger percentage of lower-income households’ budgets than higher-income households’ budgets. Regressive taxes disproportionally impact the poor.

Simply because a tax is regressive, however, doesn’t mean it shouldn’t be used. Most consumption taxes are regressive, but they still have a role in a broader system of tax and transfers that is almost invariably highly progressive.

Consumption doesn’t keep pace with income growth because savings increases as incomes grow. Progressive taxes—those that increase in burden as incomes grow—enjoy substantial popularity. Relying only on progressive taxes, however, would be problematic, as would carving up consumption tax bases exclusively in service to progressivity, in part because of the narrow number of taxable items would create a narrow, volatile tax base whose non-neutrality could introduce sizable economic distortions and disincentivize important economic activities like earning income, saving, and investing in property. Best practices for tax policy, therefore, usually include a mix of both progressive and regressive taxes that provide a stable source of revenue but minimize market distortions and the tax burden on the poor.

While excise taxes are regressive, they vary in extent. Table 1 illustrates the tax burden in the U.S. from select federal excise taxes and income by quintile. One way to measure the degree to which a tax is regressive is by subtracting the tax burden for a product in the lowest quintile from the share of income earned by that same quintile. The lowest quintile of Americans shoulders 15.9 percent of the tax burden on tobacco, while earning only 3.1 percent of the income.

| Motor Fuel | Air Travel | Alcohol | Tobacco | Income Distribution | |

|---|---|---|---|---|---|

| Lowest quintile | 4.20% | 4.50% | 3.50% | 15.90% | 3.10% |

| Second quintile | 10.50% | 7.00% | 8.60% | 18.30% | 8.30% |

| Middle quintile | 17.10% | 14.10% | 17.20% | 18.10% | 14.10% |

| Fourth quintile | 23.40% | 21.60% | 23.90% | 20.10% | 22.70% |

| Top quintile | 44.40% | 52.40% | 46.70% | 27.30% | 51.90% |

| Total | 100% | 100% | 100% | 100% | 100% |

|

Note: aggregates may not equal 100% due to rounding. Sources: Urban Brookings Tax Policy Center, “Who bears the burden of federal excise taxes?” https://www. taxpolicycenter.org/briefing-book/who-bears-burden-federal-excise-taxes; and U.S. Census Bureau, “Income and Poverty in the United States: 2019,” https://www.census.gov/library/publications/2020/demo/p60-270.html. |

|||||

The excise tax burdens on motor fuels, air travel,[14] and alcohol generally mirror the income distribution by income group. This is truer for taxes on air travel but less so for highway and alcohol taxes. Tobacco taxes have a far greater burden on the poorest income earners than taxes on motor fuels, air travel, or alcohol.

For comparison, an income tax is highly progressive. Using data from U.S. federal income taxes, one study finds that the bottom 50 percent of earners paid only 3.1 percent of all federal income taxes in 2019.[15] That is a far smaller tax burden on income than the tax burden on tobacco, alcohol, or fuel for the bottom half of income earners.

Another way to explore the regressive effect of excise taxes is to calculate how a tax increase would affect after-tax income. Table 2 presents the results of a 50 percent increase in the U.S. federal tobacco excise tax, as estimated by the Tax Foundation’s General Equilibrium Model. A 50 percent increase in the U.S. tax rate on tobacco products would negatively impact the lowest quintile’s after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. by 0.2 percent whereas the top quintile would only see a 0.02 percent decline—one-tenth of the impact.

| Income distribution | Impact on after tax income | Additional tax burden | |

|---|---|---|---|

| Lowest quintile | 3.10% | -0.20% | $5.3 billion |

| Top quintile | 51.90% | -0.02% | $9.2 billion |

|

Sources: Tax Foundation Tax and Growth Model, October 2019; U.S. Census Bureau |

|||

The model also estimates that the 50 percent tax increase on tobacco would raise an additional $33.6 billion in federal revenue over 10 years.[16] If that additional burden is distributed like the existing burden, the lowest quintile would pay $5.3 billion more in taxes on tobacco and the top quintile would pay $9.2 billion more in taxes on tobacco. While the top quintile pays more actual tax, they also earn 51.9 percent of total income, whereas Americans in the lowest quintile earn 3.1 percent of total income.

It is worth noting that most tax burdens are represented as average effects for the entire quintile. Not everyone in those groups consumes tobacco products; most do not. Therefore, the tax increase will be substantially greater for the tobacco consumers in each group.

By itself, having a regressive effect should not dissuade policymakers from levying a tax. User-pay systems and internalizing externalities are positive motivations for excise tax policy. However, the disproportionate effect of regressive taxes on the poor is reason to limit the application of excise taxes to those uses. Excise taxes should not be a tool for revenue maximization or used as a method to fund general government expenses.

Harm Reduction and Well-Being

The overall goal of excise taxation should be to improve well-being. Individual well-being is notoriously difficult to measure and often impossible to quantify. When studying well-being, economists can use revealed preference as a baseline against which to judge relative ranking and preferences. These are informative, but not very helpful in comparing across individuals or aggregating across a population. Even in the absence of robust quantifiable data, though, accounting for personal preferences and individual well-being is essential to any discussion about how taxes impact people.

Taxes, almost exclusively, decrease well-being. In an ideal setting, government expenditures enabled by tax revenues should broadly offset that decrease. But in this framework, taxes are costs that should be minimized. The exception to this is when a product or activity has a social cost. In this case, well-being increases for bystanders when consumption falls, but market participants are made worse off by the tax.

Consider a tax increase on beer. If a person wants to have a drink at home in the evening, they must pay more (tax) for that drink and are thus worse off. The brewer also faces costs in the form of lower sales and smaller margins. They lose. The person who used to buy a beer to drink at home in the evening but now switches to a different drink because beer is more expensive post-tax is worse off: no matter what they drink instead, revealed preference tells us that they would rather have had a beer. So even those that get priced out of the market are made worse off. Obviously, if there are societal gains because a higher beer tax means fewer people become inebriated and then drive a vehicle, there are also winners. Similarly, some people may never form an alcohol addiction if taxes are higher (though for others, alcohol dependency will yield inelastic demand even as taxes rise). But it is essential to highlight that most market participants are made worse off by a tax.

A thorough discussion of the reasons why individuals choose to consume products that inebriate or yield short-term satisfaction at the cost of long-run health is beyond the scope of this paper. But recognizing that individuals make these choices in pursuit of their own happiness is paramount to crafting policy that promotes well-being.

These issues are at the forefront of the discussion about harm reduction products. For example, smoking is addictive and causes long-run health problems. Because smokers primarily smoke to consume the stimulant nicotine, producers have responded by creating a wide array of products that allow people to consume nicotine without smoking. These alternative tobacco products—including vapes, heat-not-burn tobacco, and several others—are markedly less harmful to users.

Policies that encourage consumers to move from smoking to an alternative form of nicotine consumption yield many of the benefits of smoking cessation without the heavy-handedness of, say, a prohibition on nicotine products. They would also avoid withdrawal symptoms and driving people to illicit markets. Alternative tobacco products alleviate most of the external harms of tobacco use (e.g., secondhand smoke), the internal harms (e.g., long-run health problems), and still allow individuals to consume nicotine. These products are socially beneficial in the real world where addictions cannot simply be willed away and consumers’ preferences may not align with policymakers’. Taxing harm reduction products as intensely as more harmful ones may discourage—and certainly does nothing to encourage—switching.

Harm reduction is a key approach to excise tax policy to maximize well-being. The well-being of individuals participating in markets targeted by excise taxes is often overlooked when researchers don’t have quantifiable data on post-tax happiness or well-being.

Traditional Excise Categories

Alcohol

Alcohol taxes are among the oldest taxes on record. Beer was included as a taxable item in ancient Egyptian tax records. British excise taxes on table beer and brewing hops date back to 1643, where the tax on beer was particularly striking because these policies were a direct reversal of statutory price controls in the earlier medieval and early modern periods.[17] The United States can trace its beer taxes back to colonial days when New Amsterdam (now New York) governors began to collect taxes on beer. In 1644, the tax amounted to two guilders (80 cents) on each half barrel of beer tapped; half was paid by the brewer and half by the retailer.[18]

Today, all OECD countries tax alcohol. Alcohol by volume (abv) is the standard measure of alcohol content contained in an alcoholic beverage.[19] To compare across products and across countries, we convert the tax rates into common currency and standard container sizes.

Alcohol can be produced from a wide range of products and processes. The Customs Combined Nomenclature Code (CN) separates alcoholic beverages into six categories:[20] (1) beer made from malt (code 22.03); (2) wine made from grapes (code 22.04); (3) vermouth and other wine of fresh grapes flavored with plants or aromatic substances (code 22.05); (4) cider, mead and other fermented beverages (code 22.06); (5) undenatured ethyl alcohol of an alcoholic strength of 80 percent pure abv or higher (code 22.07 and code 22.08); (6) and undenatured ethyl alcohol of an alcoholic strength of less than 80 percent abv (code 22.08). We focus our discussion on the most popular consumer products in the alcohol space: beer, wine, and spirits (ethyl alcohol products).

Beer

Beer tax rates vary considerably across countries. The Czech Republic, Germany, Luxembourg, the Slovak Republic, and Turkey levy a rate less than $5 per hectoliter per abv, while Finland ($44.76) and Israel ($74.30) apply rates that are as much as 3,200 percent higher than the rates applied in lower tax countries.

Table 3 presents the beer tax rates for all OECD countries. Many countries apply intricate tax rates that can vary by alcohol content of the beer sold or size of the producer, while others apply an ad valorem excise tax. The rates presented in Table 3 are summaries for presentation and comparison. More details on the countries’ tax rates can be found in the Notes Tables.

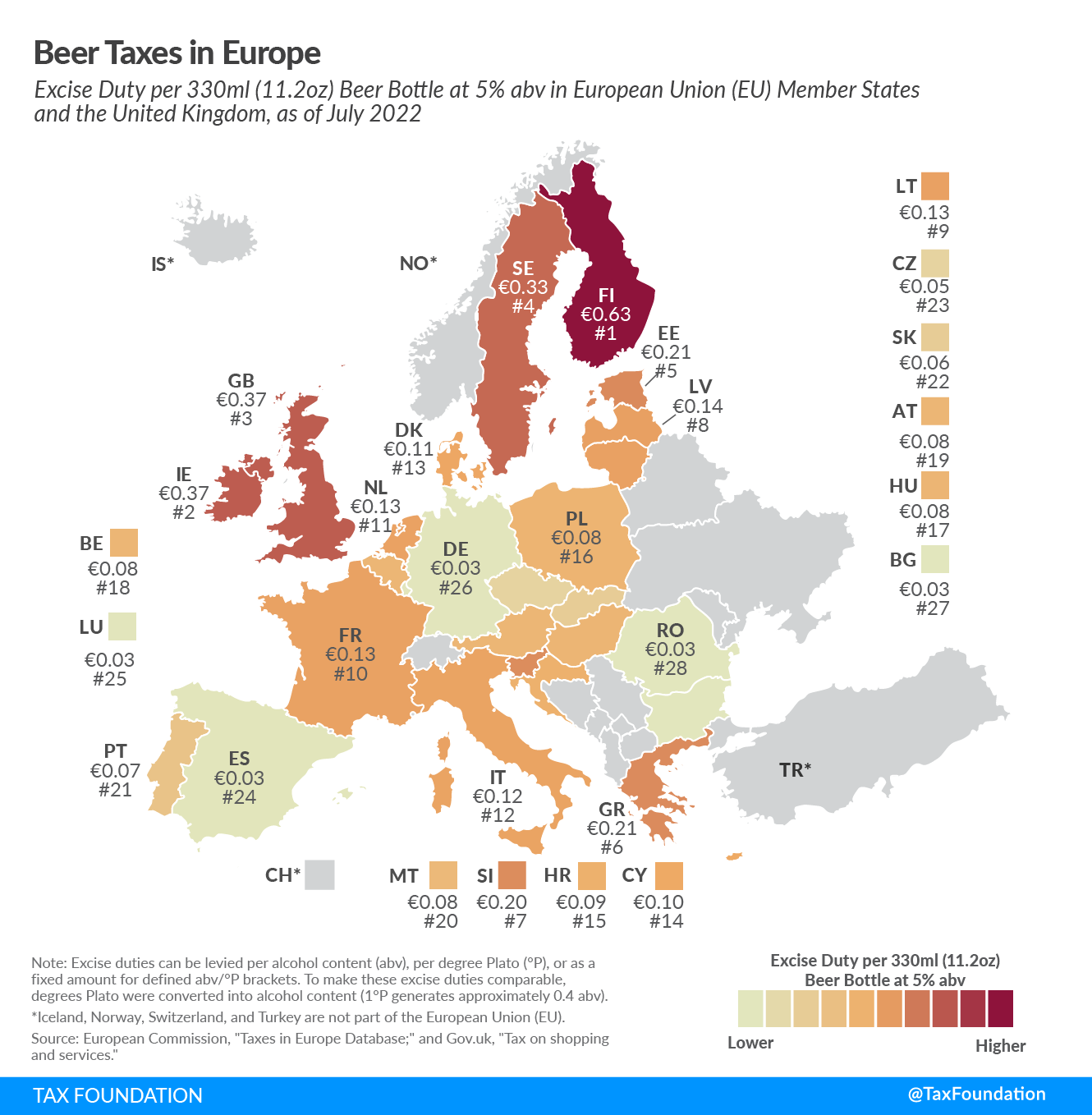

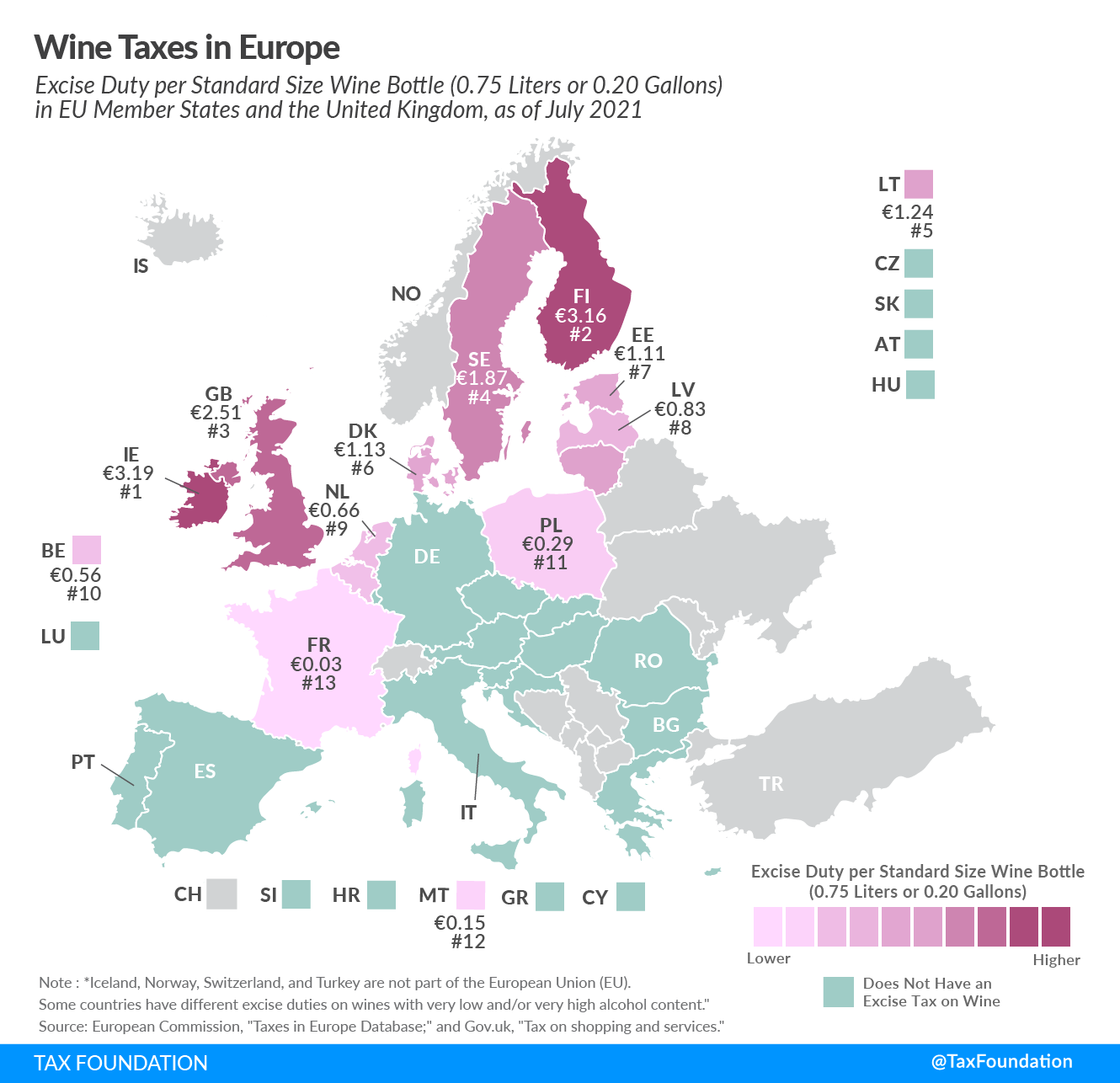

Many countries have multinational agreements on tax policy. EU law, for example, requires every EU country to levy an excise duty on beer of at least €1.87 per 100 liters (26.4 gal) and degree of alcohol content.[21]

Converting that rate to a typical 330ml (11.2 oz) beer bottle with 5 percent alcohol content, the rate amounts to a minimum tax of €0.03 ($0.04). As this map illustrates, only a few EU countries stick close to the minimum rate; most levy much higher excise duties.

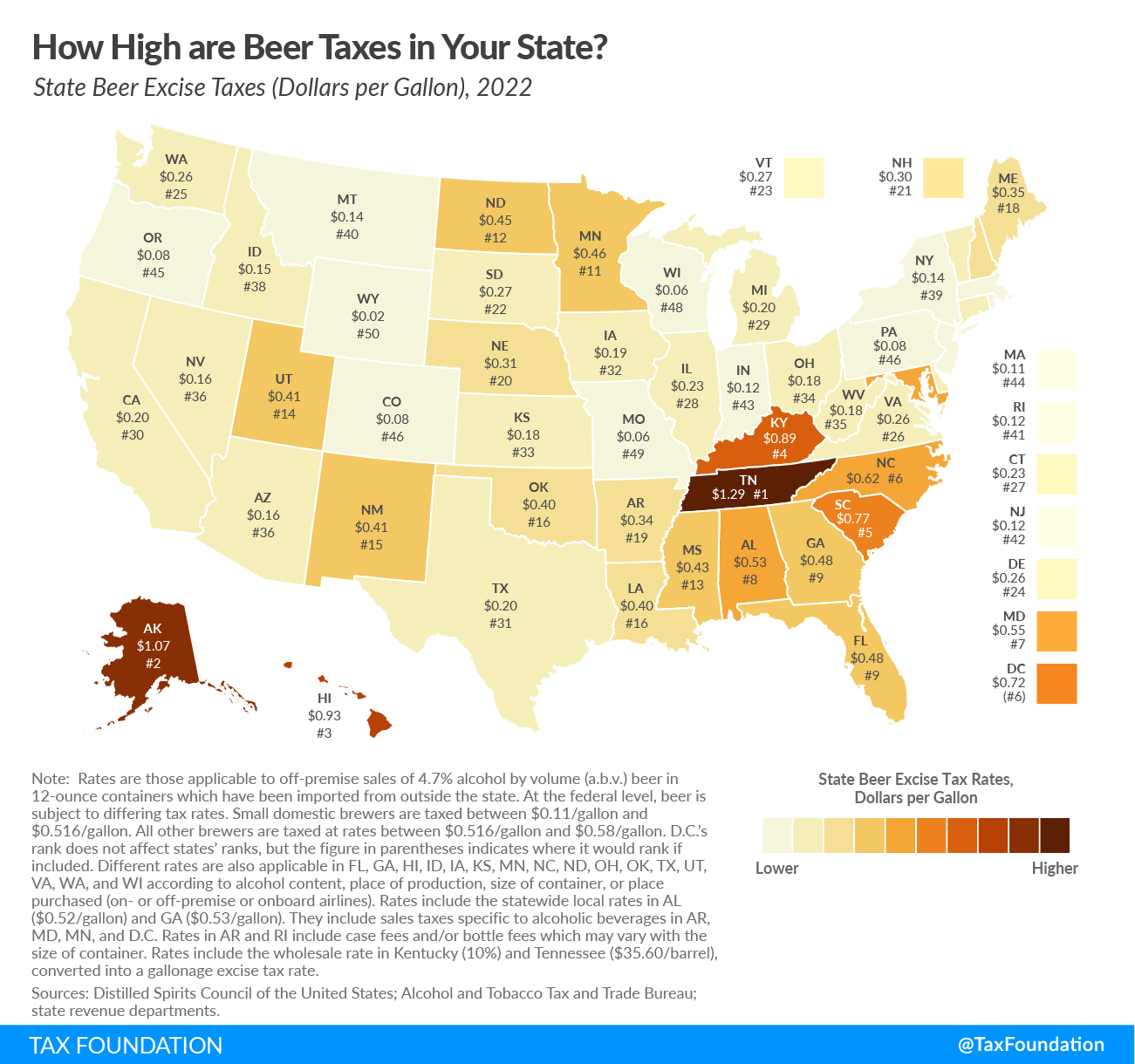

Subnational governments can levy taxes on alcohol as well. In the United States, the federal excise tax ranges from $0.11 to $0.58 per gallon based on production, location, and quantity. All 50 U.S. states and the District of Columbia also levy additional taxes on fermented malt beverages, illustrated in Figure 5. Rates vary from $0.02 per gallon in Wyoming to $1.29 per gallon in Tennessee.

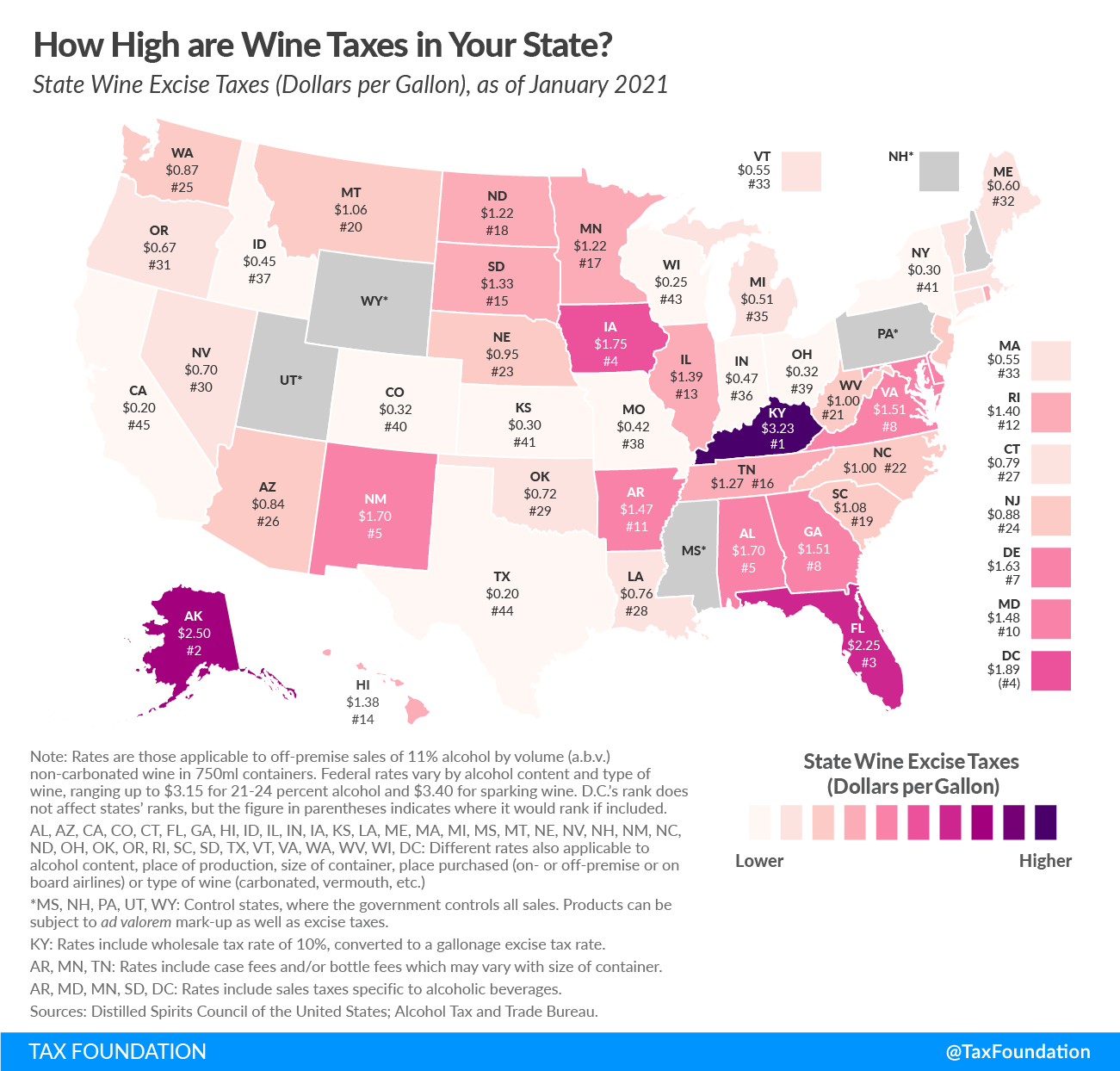

Wine

Wine is a unique product in the alcohol category in that many countries levy no excise tax on it. Thirteen OECD countries apply no excise tax to wine (Austria, Czech Republic, Germany, Greece, Hungary, Israel, Italy, Luxembourg, Portugal, Slovak Republic, Slovenia, Spain, and Switzerland). Luxembourg goes so far as to offer a lower VAT rate (14 percent instead of the standard 17 percent) for wine with alcohol content less than or equal to 13 percent.

On the other end of the spectrum, Norway has the highest wine tax among OECD countries at $6.73 per liter, followed by Ireland and Finland at nearly $5 per liter. Table 4 displays the wine tax rates for all OECD countries.

Australia, Chile, Korea, and Mexico apply ad valorem taxes in lieu of ad quantum or specific excise taxes. The United States has many subnational state taxes in addition to the federal excise tax. The two maps below show the wine tax rates, adjusted for currency and measuring unit, across the European Union and the United States.

Spirits

Consumption of distilled spirits has increased significantly in recent years. Due in part to new product developments and innovations like ready-to-drink (RTD) cocktails, consumers can purchase spirits that are easier to consume and with less bulk. Long considered a secondary beverage of choice in many countries, spirits sales overtook beer sales in the United States in 2022.[22]

Spirits consumption and tax revenues have experienced significant fluctuations based on currency rate swings and changing international tastes over the past few years as well. All types of alcohol have various geographic production clusters, based largely on agricultural yields (grapes, grain, potatoes, rice, etc.). Recent changes have been particularly fruitful for certain products. The market for Mexican tequila has seen sizable growth and exports of Japanese liquor—mostly sake and whiskey—have grown sixfold over the past decade.[23]

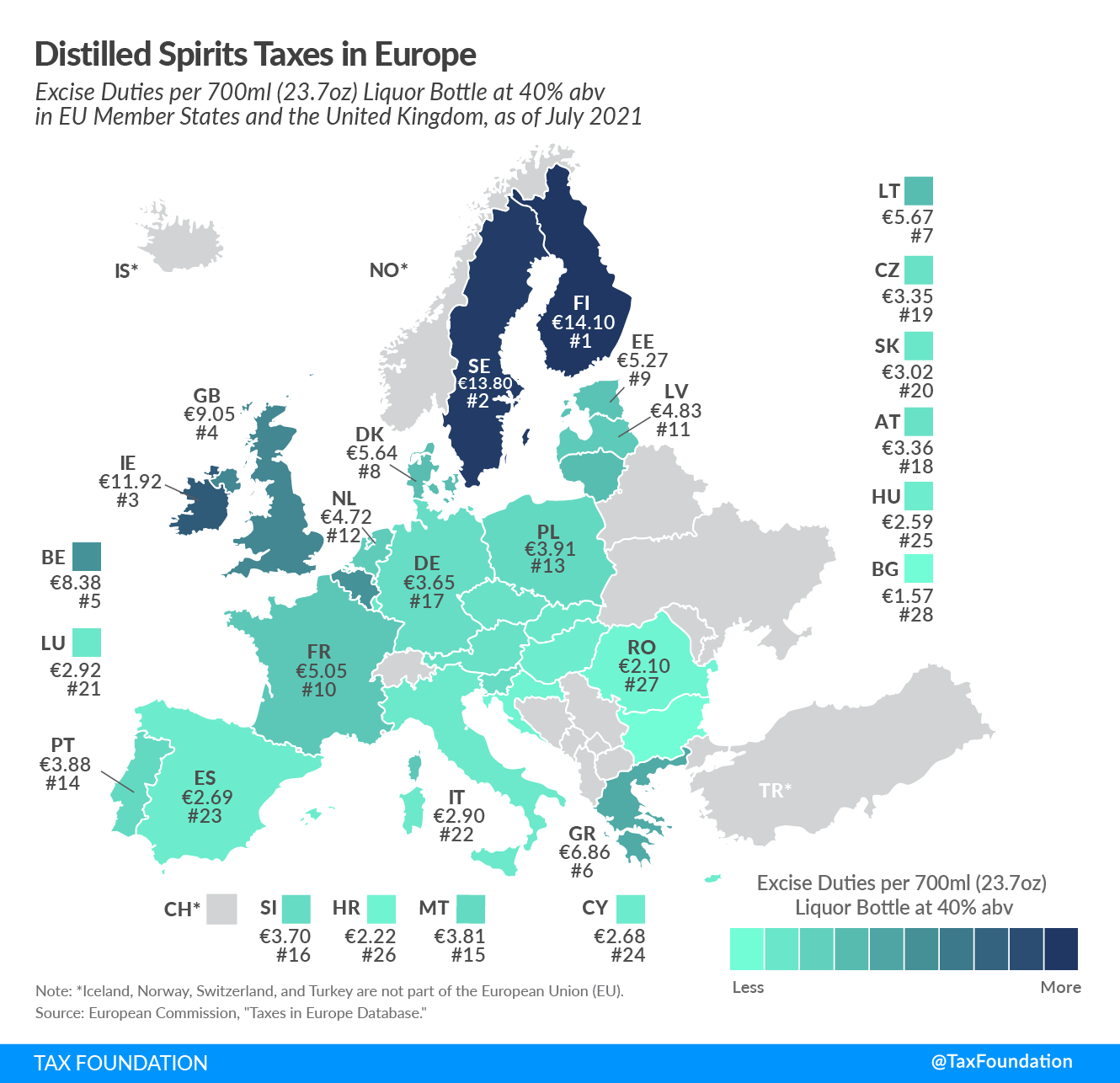

Spirits are generally taxed per proof per volume. The higher the alcohol content, the greater the tax. Like other kinds of alcohol taxes, spirits excise taxes vary widely. Table 5 shows that the tax on a hectoliter of absolute alcohol ranges from less than $1,000 in the United States to more than $12,000 in Iceland.

Even adjusting for higher alcohol content, distilled spirits generally carry a greater tax per alcohol content than either beer or wine. Nowhere is that more evident than in countries that apply taxes to spirits and no tax to wine. A glass of wine with 13 percent alcohol content could go tax-free, while a 13 percent alcohol content rum and coke will carry the full weight of a country’s spirits taxes.

Across the EU, spirits are the most heavily taxed alcohol. Taxes range from $6.41 per liter in Bulgaria to more than $57 per liter in Finland.

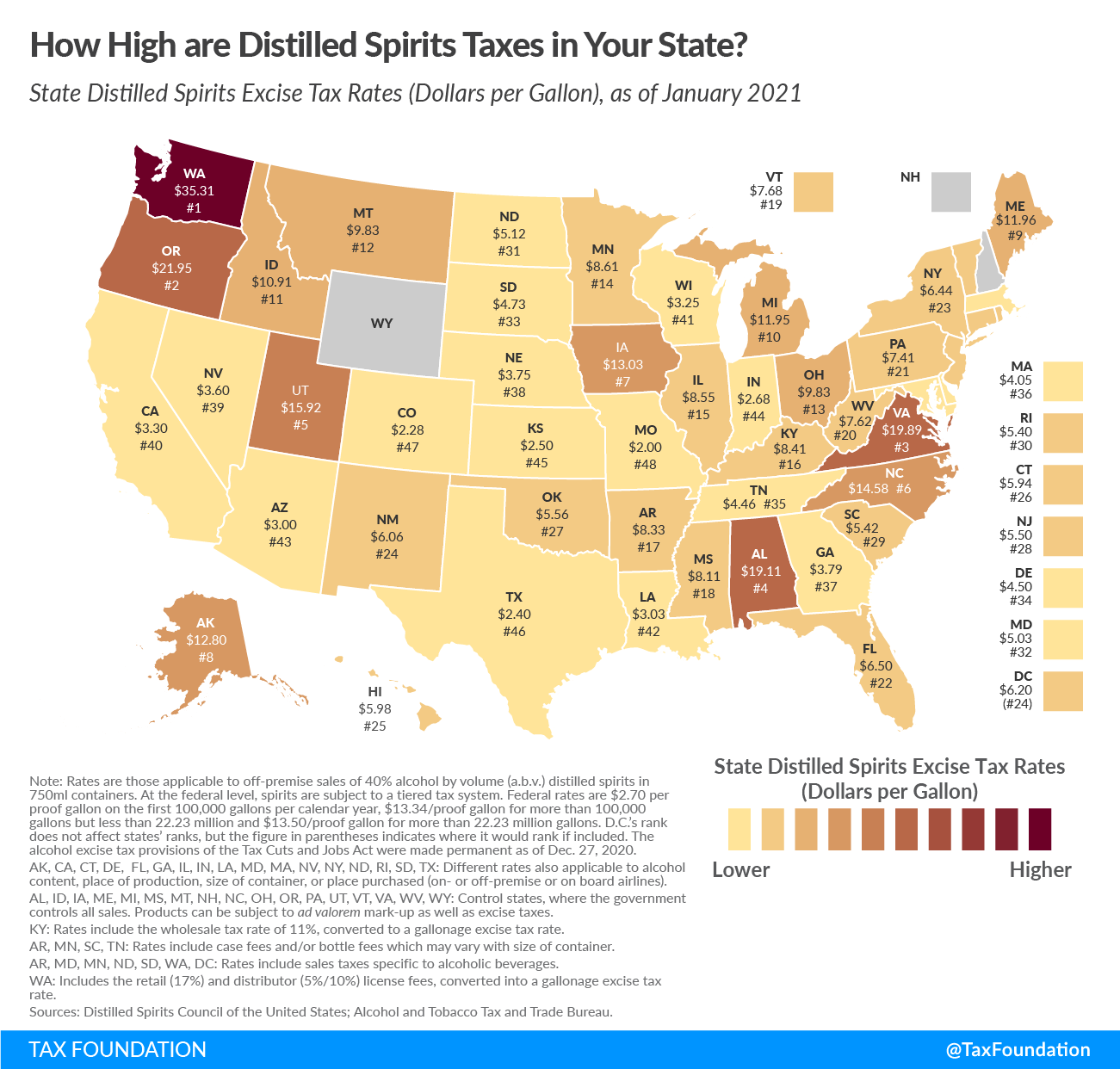

In the United States, the state of Washington taxes distilled spirits more than any other state, at $35.31 per gallon, followed by Oregon ($21.95) and Virginia ($19.89). Distilled spirits are taxed the least in Wyoming and New Hampshire. However, in these states (and others), the state maintains a monopoly on the sale of spirits. This allows the state government to manipulate prices to (dis)incentivize the purchase of distilled spirits through non-tax measures including price adjustments and retail availability, and to generate revenue through “markup” rather than taxes.

Tobacco

All OECD countries tax tobacco. As with alcohol, combustible tobacco products are subdivided into multiple categories for tax purposes, including cigarettes, cigars, cigarette rolling tobacco, and pipe tobacco. Unlike excises on alcoholic beverages, which are almost exclusively ad quantum, most countries levy a combination of ad quantum and ad valorem taxes on tobacco products.

Table 6 shows the excise tax rates for OECD countries on cigarettes and Table 7 shows the tax rates for cigars and rolling tobacco. Once again, a wide range of taxes are levied on tobacco products. Specific taxes range from $0.84 per cigarette in Australia to $0.02 per cigarette in Luxembourg. Several countries don’t levy an ad valorem tax, but for countries that do, rates range from 1 percent of the retail sales price (RSP) in Sweden and Denmark to more than 60 percent in Turkey (63 percent) and South Korea (64.76 percent).

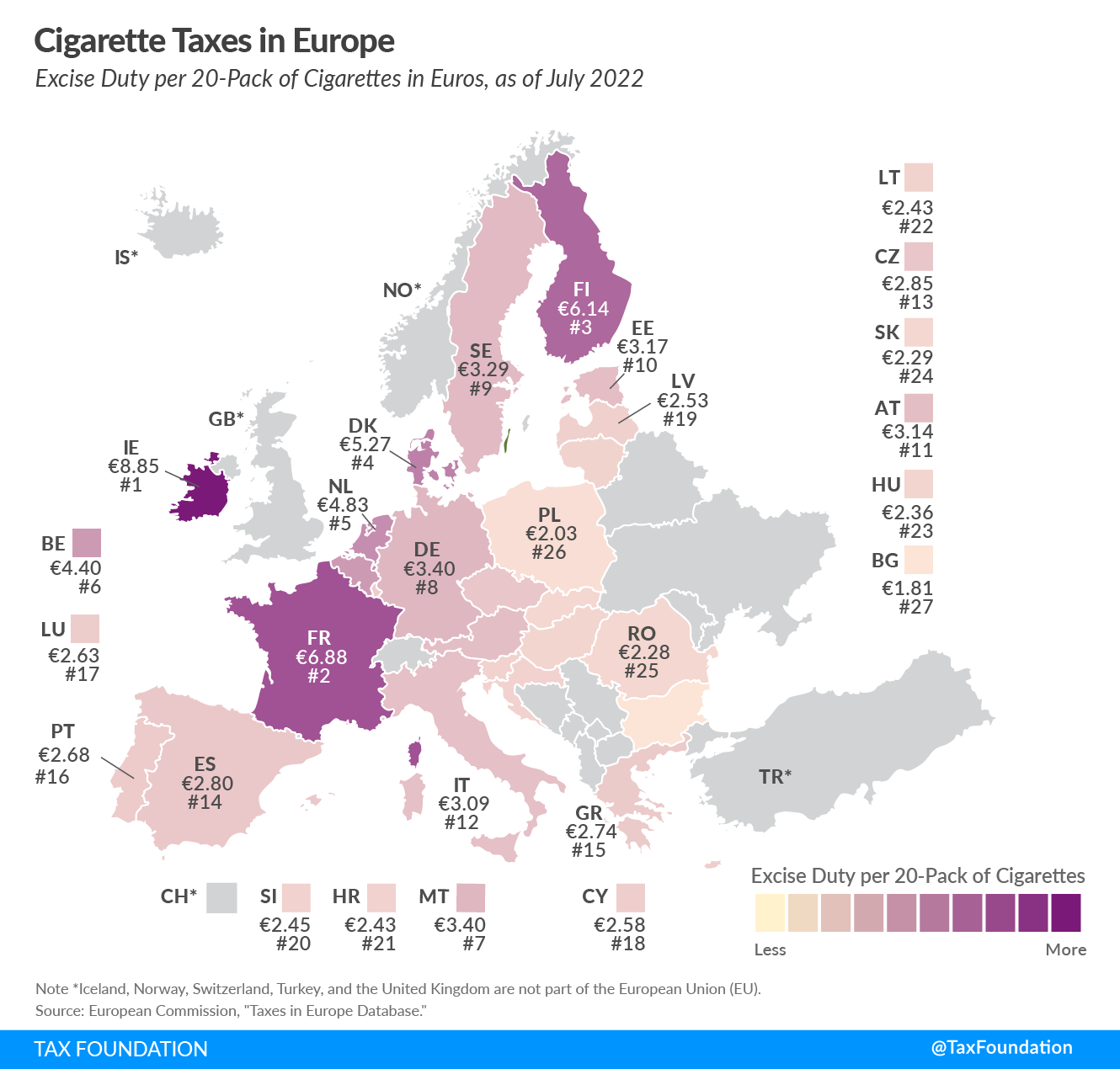

Across the EU, the Tobacco Tax Directive requires Member States to levy a minimum excise tax rate on cigarettes and other tobacco products. EU cigarette taxes include both a specific cigarette tax (a fixed euro amount per pack of cigarettes) and an ad valorem tax (an added percentage of the RSP).[24]

In total, the current minimum cigarette excise taxes in the EU are €1.80 ($1.89) per 20-cigarette pack and the total excise duty must be at least 60 percent of an EU country’s weighted average RSP (certain exceptions apply). These tobacco excise taxes come in addition to the broad consumption value-added taxes (VATs). EU legislation only establishes minimum rates. Several countries levy higher rates, illustrated in Figure 10.

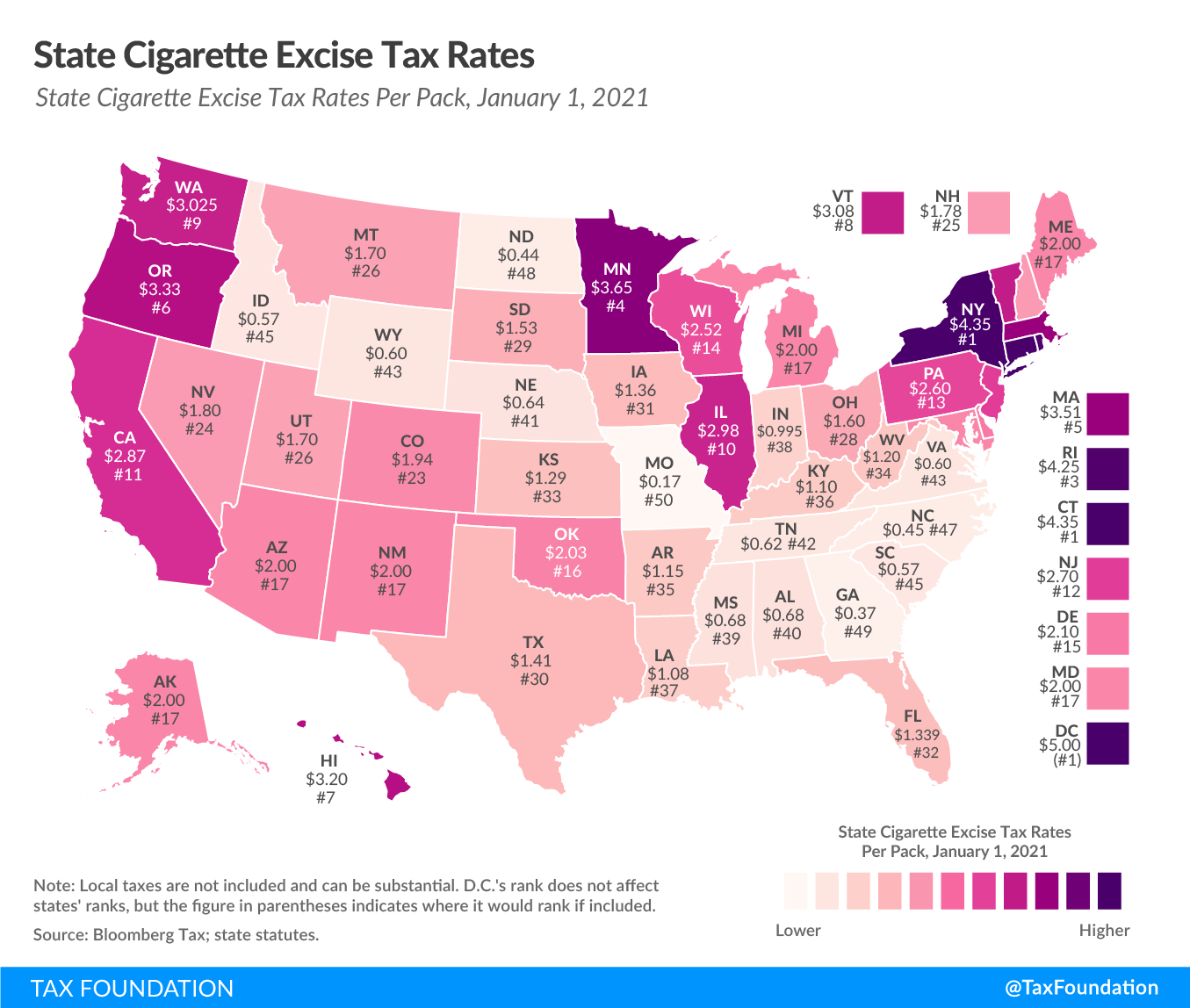

Tax rates can vary significantly at the subnational level as well. In the United States, for instance, local excise rates on cigarettes (on top of the federal tax) range from $0.17 per pack of 20 cigarettes in Missouri to $4.50 in Washington, D.C., and $4.35 in New York and Connecticut. Several counties and cities also add their own taxes to tobacco. These rates are applied in addition to the $1.01 tax applied per pack of 20 cigarettes at the national level.

Tax Burden on Tobacco

To assess the total tax burden on tobacco products, we need to combine all the multiple kinds of taxes (ad valorem excise, ad quantum excise, VAT, sales taxes, import duties, etc.) from each level of government, along with any minimum tax, markup, or pricing controls. To estimate the total tax burden, we calculate the difference between the pre-tax price for cigarettes and the aggregate amount of taxes paid for that product using average RSP as reported by OECD member representatives.

Table 8 shows the average RSP and tax burden as a share of the total price of cigarettes for OECD countries. Both the RSP and the pre-tax prices vary widely based on economic conditions, geographic production capabilities, and the structure of the market.

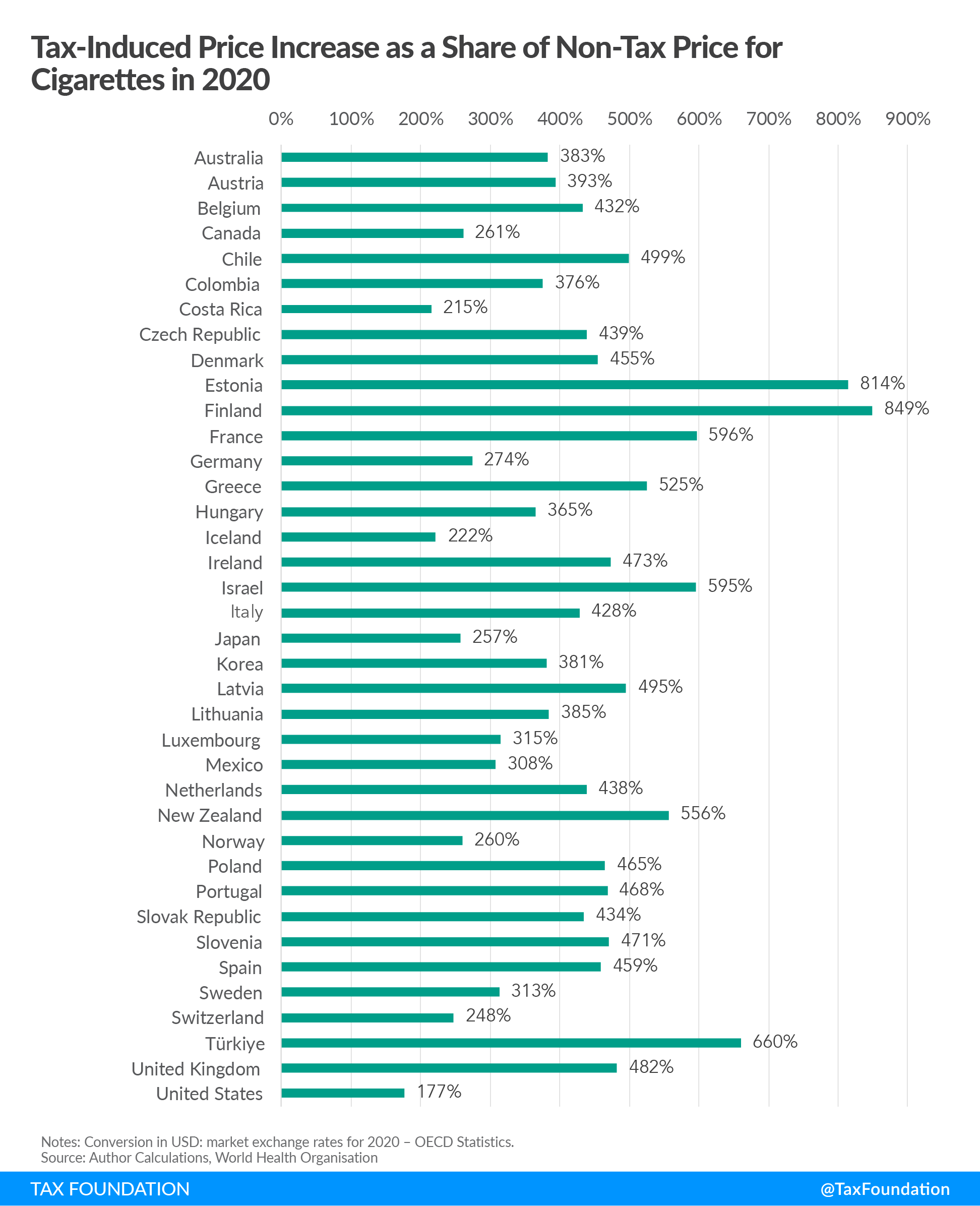

Figure 12 illustrates the tax-induced markup for cigarettes. The lowest levels of tobacco tax burden are in the United States and Costa Rica, where the RSP is 177 percent and 215 percent of the pre-tax price for a package of 20 cigarettes, respectively. In Estonia and Finland, the RSP is more than 800 percent of the pre-tax price for cigarettes.

Cigarette Smuggling

Sizable price markups for legal cigarettes create incentives for tax avoidance. Tax avoidance can take two different forms, each with different policy implications. Customers can shop across borders to purchase cigarettes legally in lower-tax jurisdictions, or illicit actors can establish a marketplace in which cigarettes are sold with little or no tax paid whatsoever.

Cross-border shopping or tax arbitrage is mostly a zero-sum activity from a cost perspective, and smugglers may even facilitate an increase in total economic activity by decreasing the market tax burden, albeit at high costs (not to mention the innate criminal nature of the activity). A smuggler who legally purchases cigarettes in a lower-tax region like Portugal and then sells the cigarettes in a high-tax area, like Ireland, still pays tax and buys European products—even if the tax loss for Ireland exceeds the tax gain for Portugal and tax-based attempts of discouraging consumption are partially thwarted.

Some criminals, however, avoid legal markets altogether. Rather than pay market prices and lower taxes on cigarettes, criminal organizations produce counterfeit cigarettes with the look and feel of legitimate brands and sell them with counterfeit tax stamps, paying no tax at all. In 2020, three men were arrested in the United States for transporting internationally produced illicit cigarettes. They admitted intentions to smuggle over 400 million cigarettes.[25]

The counterfeit cigarette capital of the world is China. Estimates put the Chinese counterfeit production as high as 400 billion cigarettes per year.[26] Because of the enormous volume of product that ships into global ports from China, it may be easier and cheaper to smuggle Chinese cigarettes through ports than transport products across continental territories.

“Cheap whites” or “illicit whites” are a staple of the international counterfeit market. These generic-looking white cigarettes are produced legally in low-tax jurisdictions but are often intended for smuggling.[27] Reports indicate that the Chinese tobacco monopoly is playing a significant role in the “illicit whites” tobacco markets across North, Central, and South America.[28]

There are real social costs associated with the tax arbitrage in legally purchased manufactured cigarettes, but they pale in comparison to the dangers posed by this counterfeit market.

Internationally smuggled and counterfeit cigarettes are dangerous products as they do not live up to the quality control standards imposed on legitimate brand cigarettes. Researchers have found that counterfeit cigarettes can have as much as seven times the lead of authentic brands and close to three times as much thallium, a toxic heavy metal.[29] Other sources report finding insect eggs, dead flies, mold, and human feces in counterfeit cigarettes.[30]

In June 2019, Canadian authorities arrested nine people who reportedly smuggled over one million pounds of tobacco (valued at CAD 110 million). According to police, the group was involved in both theft and arms trafficking.[31] That same year, European authorities arrested 22 people across five countries representing an organized crime ring suspected of large-scale cigarette trafficking, drug trafficking, assassinations, and money laundering which had netted an estimated $750 million over two years.[32] In Spain in 2020, authorities busted an underground illegal cigarette factory. The organized crime network behind the operation is suspected of large-scale cigarette trafficking with profits estimated at $647,000 per week.[33]

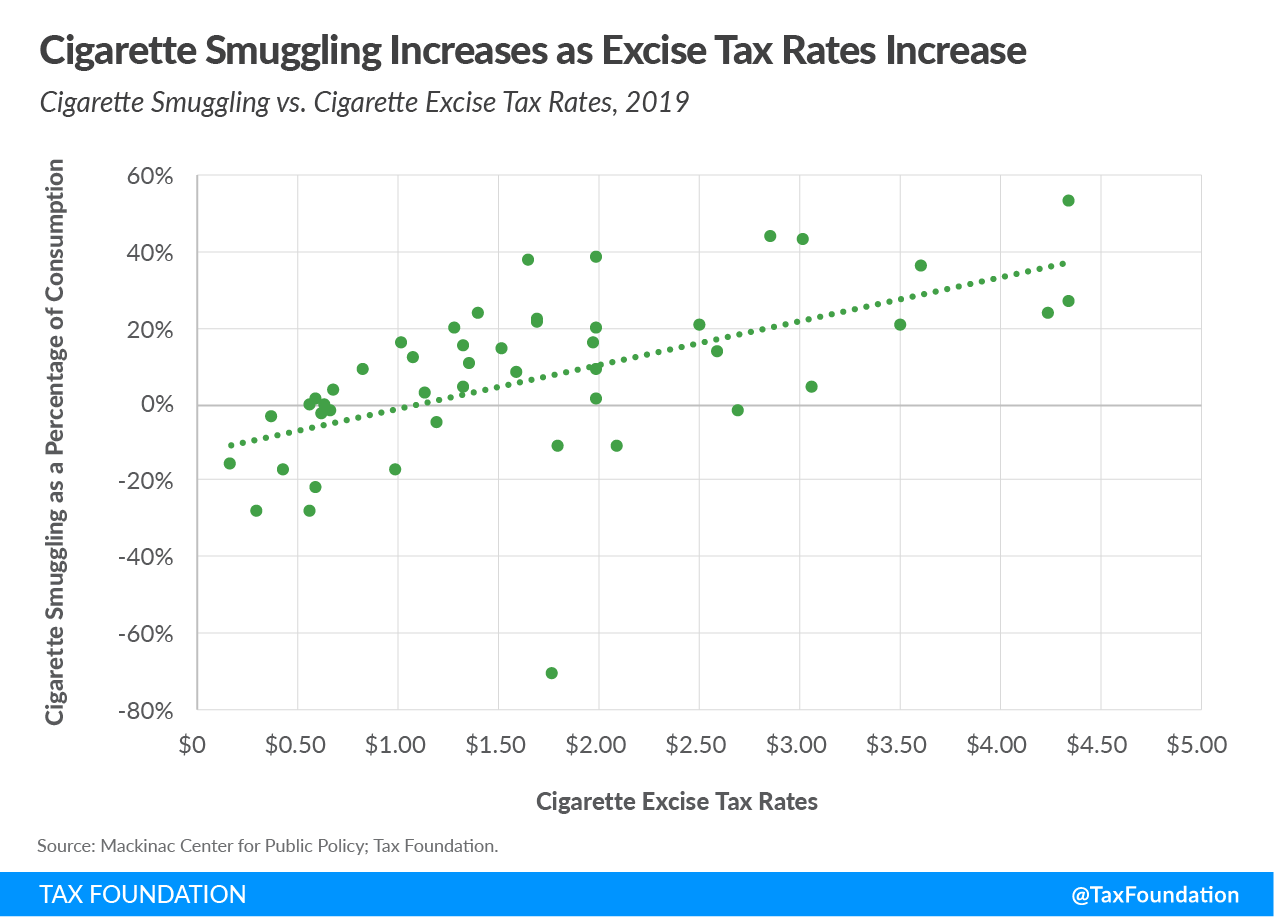

Empirical studies consistently show a positive relationship between cigarette tax rates and smuggling. Figure 13 shows a strong positive relationship between cigarette tax rates and smuggling rates in U.S. States.

Academic studies of European smuggling reach the same conclusion. A 2018 study concluded that a €1 increase in tax per pack of cigarettes would increase illicit market share by 5 to 12 percentage points and increase illicit cigarette sales by 29 percent to 95 percent.[34]

Global illicit trade in tobacco is a growing problem. Cigarette smuggling is low-risk and high-reward; billions of dollars are made each year through smuggling. To make matters worse, smuggling operations involve corruption, money laundering, and terrorism.[35] According to the Financial Action Task Force (FATF), “Large-scale organized smuggling likely accounts for the vast majority of cigarettes smuggled globally.”[36] These operations hurt consumers, because the products often fail to adhere to health standards; governments, because of lost revenue; legal businesses, because they cannot compete with illicit products; and bystanders, because they endure the effects of a more financially solvent black market.

Fuel

Fuels are subdivided into categories based on the material specifications and product uses. The main categories for excise purposes are unleaded gasoline, diesel oil, and light fuel for home heating. Many OECD countries also tax other energy products such as natural gas and electricity. Others directly levy carbon taxes or implement caps on carbon emissions as part of a tradable permit system. In this section, we discuss excise taxes on motor fuels and heating fuels. We discuss carbon taxes in the Trends section.

Motor Fuel

Transportation fuel taxes have existed since the early 20th century. Initially designed as a targeted revenue-raising tool, modern fuel taxes serve several purposes. Fuel taxes act as a user fee for road usage, fund road construction and maintenance, discourage traffic congestion, incentivize the use of public transportation, and incorporate environmental concerns.

The motor fuel tax is relatively well designed to capture many of the negative externalities caused by driving petroleum-powered vehicles. From the Pigouvian perspective, the motor fuel tax is one of the best policy options to internalize the externalities associated with automotive transportation.[37]

Across all OECD countries, the tax burden for premium unleaded gasoline is nearly half of the retail sales price. Table 9 shows that the United States is an outlier, with a tax burden of 14.2 percent, less than half of the next lowest OECD country, Turkey, at 29 percent. The tax burden in Ireland and Israel exceeds 60 percent of the price at the pump.

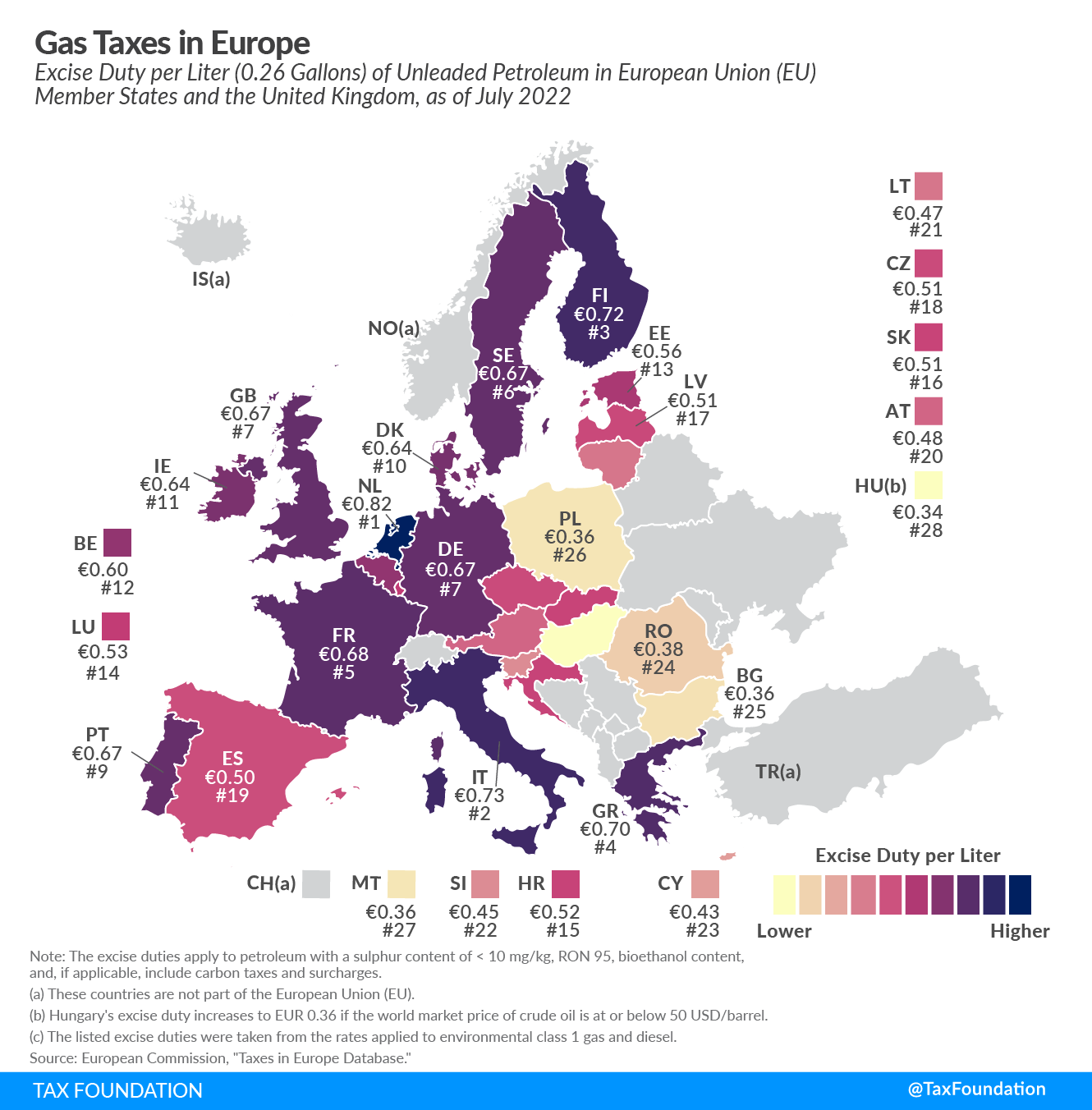

The EU Energy Taxation Directive (2003/96/EC) sets common rules for the taxation of energy products in Member States, including fuel. The minimum rates on road fuels are €0.359/l for unleaded gasoline; €0.330/l for diesel fuel and €0.125/kg for liquified petroleum gas. The map below highlights that only Bulgaria, Hungary, and Poland stick to the minimum fuel tax rate, while all other EU countries opt to levy higher excise duties on gas.

The Netherlands has the highest gas tax in the European Union, at €0.82 per liter ($3.69 per gallon). Italy applies the second highest rate at €0.73 per liter ($3.26 per gallon), followed by Finland at €0.72 per liter ($3.24 per gallon).

Roughly 30 percent of new passenger vehicles in the European Union are diesel vehicles.[38] Therefore, many European consumers face excise duties on diesel instead of gasoline. The EU sets a slightly lower minimum excise duty of €0.33 per liter ($1.48 per gallon) on diesel.[39]

Excise tax rates for diesel fuel are lower than the rates for gasoline in all OECD countries except Australia, Belgium, and the United Kingdom where the rates are the same, and in Switzerland and the United States where the tax rate for diesel exceeds the rate for gasoline. This is peculiar from an environmental tax perspective, as diesel consumption has a greater environmental impact than unleaded gasoline, largely due to the significant differences in nitrogen oxides (NOx) and particulate emissions.[40] In Finland, Norway, Slovenia, and Sweden, the environmental concerns of fuel consumption are sufficient that the excise rate explicitly includes a CO2 component for both unleaded gasoline and diesel fuel.

Gas taxes also differ across the United States. State tax rates range from $0.6698 per gallon in California and $0.5956 in Illinois to $0.1498 in Alaska and $0.1742 in Missouri.

The aggregate tax burden on transportation is larger than the excise tax on fuel. Vehicles are subject to registration (and recurrent circulation) fees and taxes, purchase fees and taxes, distance-and-weight-based taxes, parking fees, and road usage tolls.

While motor fuel taxes have served as a highly effective tool for more than a century, significant changes are likely underway to transportation taxes. Growing environmental concerns about carbon dioxide emissions have created upward pressure on fuel rates. At the same time, electric vehicles that consume no motor fuel, but still use the roadways, have a growing market share; and new individual-level tracking technology can more precisely identify the amount of road usage per vehicle. The motor fuels tax may soon become obsolete, as governments are able to levy a combination of vehicle registration fees and precise user fees via vehicle miles traveled taxes (VMTs).

Heating Fuel

Heating oil is taxed at lower rates than motor fuels in most OECD countries, illustrated in Table 10. In the European Union (EU), the Energy Tax Directive’s (ETD) minimum tax for heating fuel (€0.021/l) is much lower than the minimum tax rate for motor fuel (€0.3/l of diesel). Only a few EU Member States (Czech Republic, Hungary, and the Netherlands) apply a similar tax rate for heating and diesel oil. No countries apply reduced VAT rates for diesel or gasoline, but Ireland, Luxembourg, and the UK apply a reduced VAT rate for heating oil.

For countries that tax heating fuels, the taxes range from $0.05 in the United States to $1.22 in Israel. Taxes make up more than 40 percent of the total price of heating fuels in Denmark, Greece, Israel, Italy, the Netherlands, and Portugal. Taxes comprise less than 5 percent of the price of home heating oil in the United States.

New Excise Taxes and Trends

New excise tax categories arise constantly. Most of these taxes have limited geographic applicability and generate relatively small amounts of revenue. Relatively niche excise taxes are levied on decks of playing cards, fur clothing, blueberries, admission to entertainment shows, parking spots, candy, ice cream, and sales of products at establishments related to the sex industry.[41] In 2022, the United States even added a 1 percent tax to publicly traded company stock buybacks.[42]

Other trends in excise taxes could completely change the landscape of excise taxation. Growth in excise taxes on cannabis, alternative tobacco products, sugar-sweetened beverages, ride-sharing, and plastics have the potential for a global tax base and major implications for global consumption. Carbon taxes would also have global implementation, ideally, and the revenue from carbon taxes has the potential to exceed annual tax collections from all other forms of excise taxes combined.

Carbon

Climate change has become an increasingly pressing global issue. Policy solutions to address climate change are increasingly muddled, from an all-encompassing agenda that expands government control over the whole economy to a status quo of patchwork of subsidies and regulatory regimes.

The patchwork policy approach has produced, not surprisingly, mixed results. Many policies, including tax credits for alternative fossil fuels, green energy subsidies, and energy efficiency standards for appliances and automobiles, help reduce carbon emissions, but often at a high cost for a small environmental gain.

One policy that could internalize the social costs in a neutral manner would be to impose a price on carbon. In 2019, more than 3,500 U.S. economists signed the Economists’ Statement on Carbon Dividends.[43] The statement offered five policy recommendations:

- Implement a carbon tax because it is the most cost-effective method of reducing carbon emissions at the necessary scale and speed.

- A carbon tax should increase every year until emissions reduction goals are met and be revenue neutral to avoid debates over the size of government.

- A sufficiently robust and gradually rising carbon tax will replace the need for various carbon regulations that are less efficient.

- A border carbon adjustment system can prevent carbon leakage and enhance the competitiveness of firms that are more energy efficient.

- To maximize the fairness and political viability of a rising carbon tax, all the revenue should be returned directly to citizens through equal lump-sum rebates. Most families, including the most vulnerable, will benefit financially by receiving more in “carbon dividends” than they pay in increased energy prices.

The foundation of a carbon tax is simple. Executing and implementing a global carbon tax is more challenging.

First, to apply an appropriate tax on carbon, we need to have an approximate measure of the social costs of carbon emissions. What are the social costs of carbon emissions? There are a range of answers. Within just the United States, the Trump administration estimated the social cost of carbon to be $8 per ton,[44] while the Biden administration currently uses a social cost of carbon of $51 per ton. High-end estimates of the social cost of carbon can reach well above $100 per ton—as an example, the state of New York arrived at the social cost of carbon of $125 per ton.[45] The number of assumptions required for an estimate of the social cost of carbon leads to a wide variety of dollar figures, but $50 per ton is an estimate near the median.[46]

When applying a carbon tax, the earlier in the production process the better. According to a 2009 study, it would be possible to collect a carbon tax on 80 percent of U.S. carbon emissions while only directly taxing 3,000 businesses, illustrating the relative simplicity of an upstream point of collection.[47]

Across the globe, existing carbon taxes have a range of coverage. British Columbia’s carbon tax covers 78 percent of the province’s emissions, but Poland’s carbon tax covers less than 5 percent of the country’s emissions.[48] Spain’s carbon tax only applies to fluorinated gases, taxing only 3 percent of the country’s total greenhouse gas emissions. Norway, by contrast, recently abolished most exemptions and now covers more than 60 percent of its greenhouse gas emissions. Ideally, a carbon tax base should be broad enough to cover most carbon emissions.

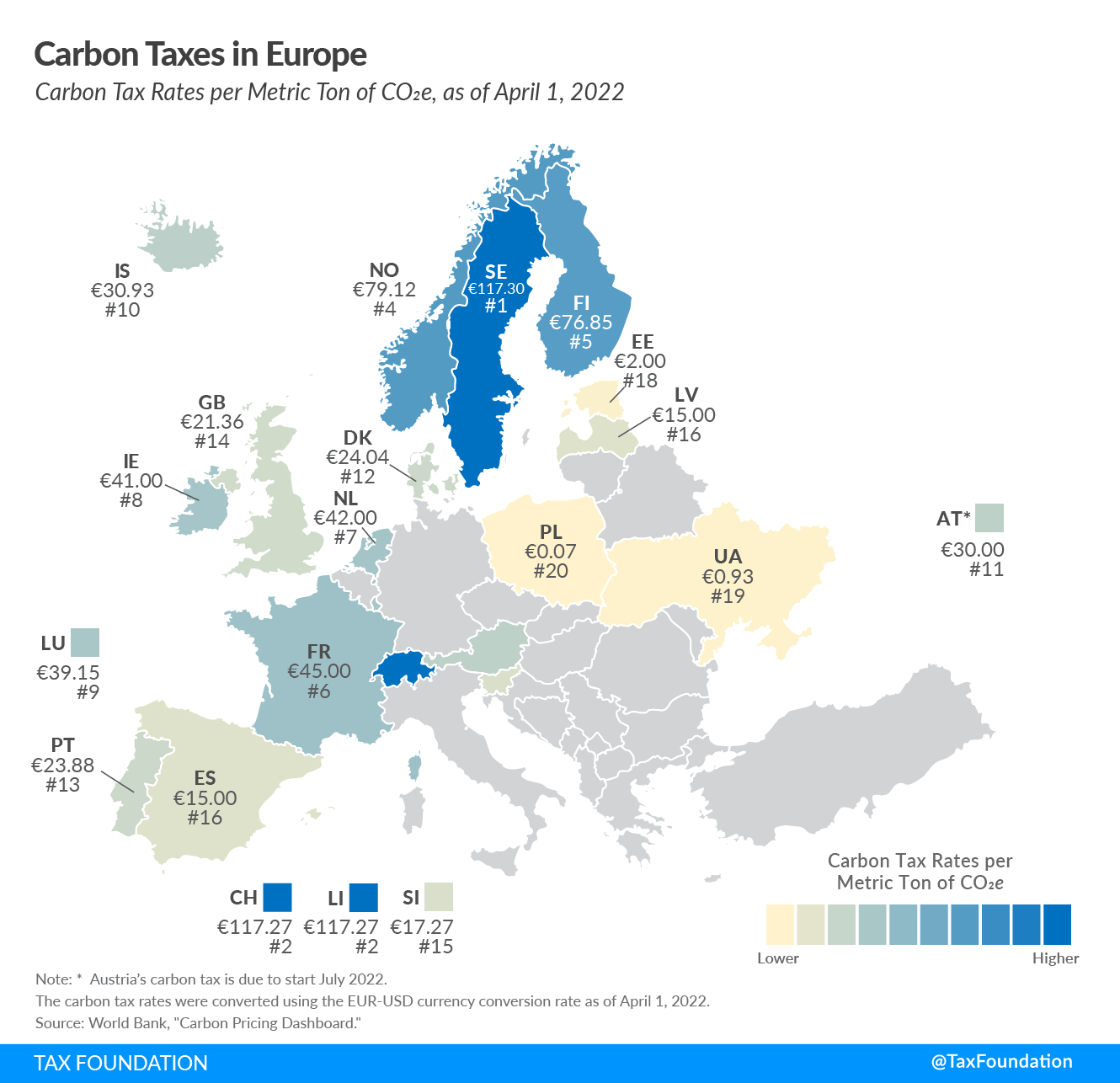

Finland was the first country to introduce a carbon tax in 1990. Eighteen European countries have followed suit, implementing carbon taxes that range from less than €1 per metric ton of carbon to more than €100.

Figure 16 shows that in Europe, Sweden levies the highest carbon tax rate at €117.30 ($129.89) per ton of carbon emissions, followed by Switzerland, Liechtenstein, and Finland. The lowest carbon tax rates in Europe are in Poland (€0.07, $0.08), Ukraine (€0.93, $1.03), and Estonia (€2, $2.21).

All Member States of the EU, plus Iceland, Liechtenstein, and Norway, are part of the EU Emissions Trading System (EU ETS). The EU ETS is a market created to trade a capped number of greenhouse gas emission allowances. European Economic Area countries also levy a carbon tax that is also part of the EU ETS. Separate European emissions trading systems include Switzerland’s system, which is tied to the EU ETS, and the UK’s ETS post-Brexit system established in 2021. A separate ETS for buildings and transport (ETS II) is expected to launch in 2027.

Lastly, in December 2022, the European Union entered the final stage of negotiations on the world’s first carbon border adjustment mechanism (CBAM). The transitional phase of CBAM will begin in October 2023, with the permanent system in place in January 2026.[49]

While the EU finalizes its laws and policies on CBAM, it may have succeeded in another, potentially equally important objective abroad. Its approach to CBAM emphasized “encouraging partner countries to establish carbon pricing policies to fight climate change.” The CBAM is a tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. that will be imposed on all imported products within CBAM’s product scope. Producers can offset this tariff if they can demonstrate that the producer already paid a carbon tax on the product in their home country. Thus, by implementing CBAM as a tariff, the EU encouraged foreign policymakers—particularly in the United States—to engage in climate negotiations more seriously.

As policymakers across the globe debate the way forward on carbon taxes and CBAM, the fundamentals of good tax policy are paramount to keep in mind. A broad-based carbon tax could allow governments to raise stable revenue, incentivize greenhouse gas emission reductions, and potentially avoid a harmful trade war over climate tax measures.

Cannabis

Globally, cannabis is the most widely used illicit drug, and its usage has increased over the past two decades.[50] The UN Office on Drugs and Crime’s (UNODC) World Drug Report estimates that in 2020, more than 4 percent of the global population aged 15–64 (209 million people) had used cannabis in the past year.[51] Marijuana use, cultivation, and global traffic are all on upward trajectories.

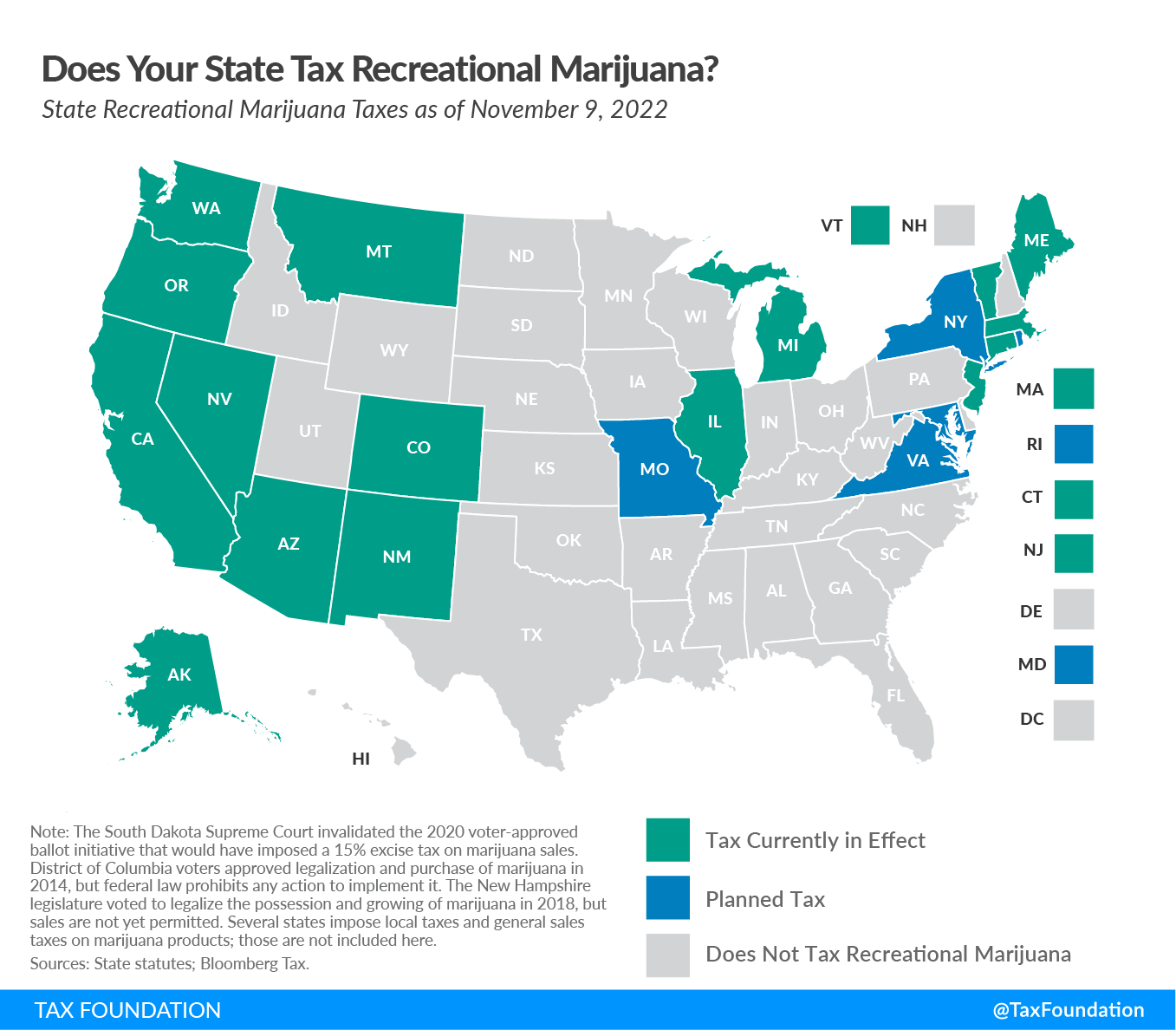

Uruguay was the first country to legalize recreational use of cannabis in 2014. A handful of countries have followed suit, with much of the growth in the global cannabis market generated from the legalization of medical and recreational use in North America. Canada legalized recreational marijuana use in 2018; legal reforms started in Mexico but have stalled; and while no policy has been adopted at the national level in the United States, 21 states, illustrated below, have implemented legislation to legalize and tax recreational marijuana sales.

The unusual situation surrounding the legality of cannabis, along with the novelty of legalization, has resulted in a wide variety of tax designs.[52] Table 11 below highlights the variety of tax policies implemented across the U.S. states. Certain states apply specific taxes, others apply ad valorem taxes, and some states apply a hybrid approach that uses both. The ad valorem rates are applied at the wholesale and retail levels and range from 10 percent in Michigan and Rhode Island (as a standalone tax, though rates go as low as 3 percent in Connecticut, which applies a hybrid tax) to 37 percent in Washington. Specific taxes are levied separately on cannabis seeds, flower (mature and immature), leaves, trim, clones, whole plants, concentrates, and edibles, and can vary by THC content in the product.

| State | Tax Rate |

|---|---|

| Alaska | $50/oz. mature flowers; |

| $25/oz. immature flowers; | |

| $15/oz. trim, $1 per clone | |

| Arizona | 16% excise tax (retail price) |

| California | 15% excise tax (levied on wholesale at average market rate); |

| $9.65/oz. flowers & $2.87/oz. leaves cultivation tax; | |

| $1.35/oz fresh cannabis plant | |

| Colorado | 15% excise tax (levied on wholesale at average market rate); |

| 15% excise tax (retail price) | |

| Connecticut | 3% excise tax (retail price) |

| $0.00625 per milligram of THC in plant material | |

| $0.0275 per milligram of THC in edibles | |

| $0.09 per milligram of THC in non-edible products | |

| Illnois | 7% excise tax of value at wholesale level; |

| 10% tax on cannabis flower or products with less than 35% THC; | |

| 20% tax on products infused with cannabis, such as edible products; | |

| 25% tax on any product with a THC concentration higher than 35% | |

| Maine | 10% excise tax (retail price); |

| $335/lb. flower; | |

| $94/lb. trim; | |

| $1.5 per immature plant or seedling; | |

| $0.3 per seed | |

| Massuchetts | 10.75% excise tax (retail price) |

| Maryland (a) | TDB |

| Michigan | 10% excise tax (retail price) |

| Missouri (a) | 6% excise tax (retail price) |

| Montana | 20% excise tax (retail price) |

| Nevada | 15% excise tax (fair market value at wholesale); |

| 10% excise tax (retail price) | |

| New Jersey | Up to $10 per ounce, if the average retail price of an ounce of usable cannabis was $350 or more; |

| up to $30 per ounce, if the average retail price of an ounce of usable cannabis was less than $350 but at least $250; | |

| up to $40 per ounce, if the average retail price of an ounce of usable cannabis was less than $250 but at least $200; | |

| up to $60 per ounce, if the average retail price of an ounce of usable cannabis was less than $200 | |

| New Mexico | 12% excise tax (retail price) |

| New York | $0.005 per milligram of THC in flower |

| $0.008 per milligram of THC in concentrates | |

| $0.03 per milligram of THC in edibles | |

| 9% excise tax (retail price) | |

| Oregon | 17% excise tax (retail price) |

| Rhode Island | 10% excise tax (retail price) |

| Virginia | 21% excise tax (retail price) |

| Vermont | 14% excise tax (retail price) |

| Washington | 37% excise tax (retail price) |

|

(a) As of July 2022, retail sale of recreational marijuana has not yet started. Note: District of Columbia voters approved legalization and purchase of marijuana in 2014 but federal law prohibits any action to implement it. In 2018, the New Hampshire legislature voted to legalize the possession and growing of marijuana, but sales are not permitted. Alabama, Georgia, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Minnesota, Nebraska, North Carolina, South Carolina, Oklahoma, Rhode Island, and Tennessee impose a controlled substance tax on the purchase of illegal products. Several states impose local taxes as well as general sales taxes on marijuana products. Those are not included here. Sources: State statutes; Bloomberg Tax. |

|

Several important lessons emerged from the rollout of marijuana laws and the adoption of legal markets. First, the revenue potential from legal marijuana markets is significant. These revenues may take years to materialize after legalization, however, and revenues will be volatile, particularly if taxes are levied ad valorem instead of ad quantum. Table 12 projects the excise tax potential for all 50 U.S. states and the District of Columbia using average revenue from early adopting states, $220 per marijuana-using resident.[53]

| State | Marijuana Excise Tax Revenue Potential |

|---|---|

| Alabama | $92,217,856 |

| Alaska | $28,258,632 |

| Arizona | $183,169,705 |

| Arkansas | $59,314,764 |

| California | $1,086,253,401 |

| Colorado | $230,239,177 |

| Connecticut | $97,696,550 |

| Delaware | $24,566,974 |

| District of Columbia | $26,605,996 |

| Florida | $448,740,070 |

| Georgia | $198,400,771 |

| Hawaii | $28,453,985 |

| Idaho | $33,295,445 |

| Illinois | $277,576,356 |

| Indiana | $157,009,061 |

| Iowa | $50,183,462 |

| Kansas | $42,058,743 |

| Kentucky | $83,008,154 |

| Louisiana | $81,616,779 |

| Maine | $50,685,850 |

| Maryland | $135,837,117 |

| Massachusetts | $214,347,227 |

| Michigan | $288,183,493 |

| Minnesota | $122,072,389 |

| Mississippi | $47,304,242 |

| Missouri | $119,222,374 |

| Montana | $35,142,502 |

| Nebraska | $35,975,930 |

| Nevada | $106,255,348 |

| New Hampshire | $44,163,575 |

| New Jersey | $158,974,353 |

| New Mexico | $61,692,434 |

| New York | $431,141,823 |

| North Carolina | $182,947,622 |

| North Dakota | $13,231,599 |

| Ohio | $220,827,478 |

| Oklahoma | $67,680,000 |

| Oregon | $182,845,089 |

| Pennsylvania | $244,553,615 |

| Rhode Island | $35,455,500 |

| South Carolina | $96,680,914 |

| South Dakota | $14,270,281 |

| Tennessee | $132,509,552 |

| Texas | $397,424,206 |

| Utah | $44,428,908 |

| Vermont | $27,313,974 |

| Virginia | $139,977,848 |

| Washington | $285,674,135 |

| West Virginia | $38,327,540 |

| Wisconsin | $117,791,078 |

| Wyoming | $10,054,045 |

|

Note: Calculation is based on average recreational marijuana excise tax paid per marijuana-using resident in Alaska, Colorado, California, Nevada, Oregon, and Washington ($220 in FY 2020) and number of marijuana-using residents in every state. The $220 is likely an underestimation of the amount paid per legal user, as the total number of users include 18-21-year-olds who do not Sources: Colorado Department of Revenue; SAMHSA; U.S. Census Bureau; author’s calculations. |

|

When designing the tax, rates should be low enough to allow legal markets to undercut, or at least gain price parity with, the illicit market. Revenue targets should aim to raise enough revenue to fund marijuana-related spending priorities and cover societal costs related to consumption.

Identifying the social costs of marijuana consumption is difficult because the academic literature on the topic is very young and some costs would be reduced by legalization. In 2018, the Canadian Substance Use Costs and Harm Scientific Working Group estimated the annual external costs of several drugs, including cannabis. Their estimates of the national social costs of cannabis were $2.8 billion. That included $0.2 billion in health-care costs, $0.4 billion in lost productivity, $1.8 billion in criminal justice costs, and $0.5 billion in other costs.

A 2019 academic study merged these costs with legal and illegal cannabis price data to calculate separate externalities based on legal and illegal sales.[54] They arrive at estimates of illicit market externalities of CAD 4.36 per gram (CAD 123.60 per ounce) and legal market externalities of CAD 1.62 per gram (CAD 46.41 per ounce).

The researchers conclude that current taxation and pricing policies in Canada overprice legally sold cannabis. Recent data show that Canadians buying cannabis from legal sources pay about CAD 10 per gram, while those utilizing the grey market pay CAD 6.37 per gram.[55] This overpricing causes users who would otherwise prefer legal cannabis to continue to purchase illicit market cannabis. Because every gram of illicit cannabis purchased as a substitute for a gram of legal cannabis imposes an additional cost to society of CAD 2.74 policymakers should carefully design pricing strategies to encourage customers to move from illicit markets to legal markets.