Key Findings

- The waning pandemic and robust economic recovery have come with many benefits—plentiful jobs and fast-growing (nominal) incomes—but also serious challenges such as high and rising inflation.

- Rather than pushing for more fiscal stimulus or leaving it to the Federal Reserve to handle inflation through higher interest rates, policymakers should focus on boosting the productive capacity of the economy by reforming the tax code to prioritize economic growth and opportunity.

- In terms of business taxation, the tax code should be improved to encourage investment, innovation, dynamism, and competitiveness, leading to more and better jobs.

- In terms of individual taxation, streamlining benefits, cleaning up complicated provisions, and eliminating tax penalties on saving would help families enjoy financial security and the returns to their work and saving.

Table of Contents

- Introduction

- — Business Tax Reforms

- — Individual Income Tax Reforms

- Business Tax Reforms

- — Better cost recovery for capital investment

- — Better cost recovery for R&D and a simpler R&D tax credit

- — Maintain a competitive corporate tax system

- — Remove the double taxation of corporate income

- — Clean up the structure of the business tax code

- — Return to competitive free trade policies

- Individual Income Tax Reforms

- — Streamline social benefits

- — Remove tax barriers from personal saving

- — Clean up the structure of the individual income tax code

- — Inflation index structural features of the tax code not indexed for inflation

- Conclusion

- References

Introduction

After more than two years of a global pandemic, people are eager to not just get back to normal, but to thrive. The desire, coupled with major shifts in working and living arrangements, new technologies, and new policies, presents exciting opportunities—and serious challenges—for American families and businesses. Coming out of the pandemic, we envision an economy brimming with innovation, dynamism, plentiful jobs, and economic and social mobility, all of which will foster greater financial security for American families. As the American people step into a new economic landscape, policymakers must keep up, or they risk jeopardizing the growth and opportunity our changing economy can bring.

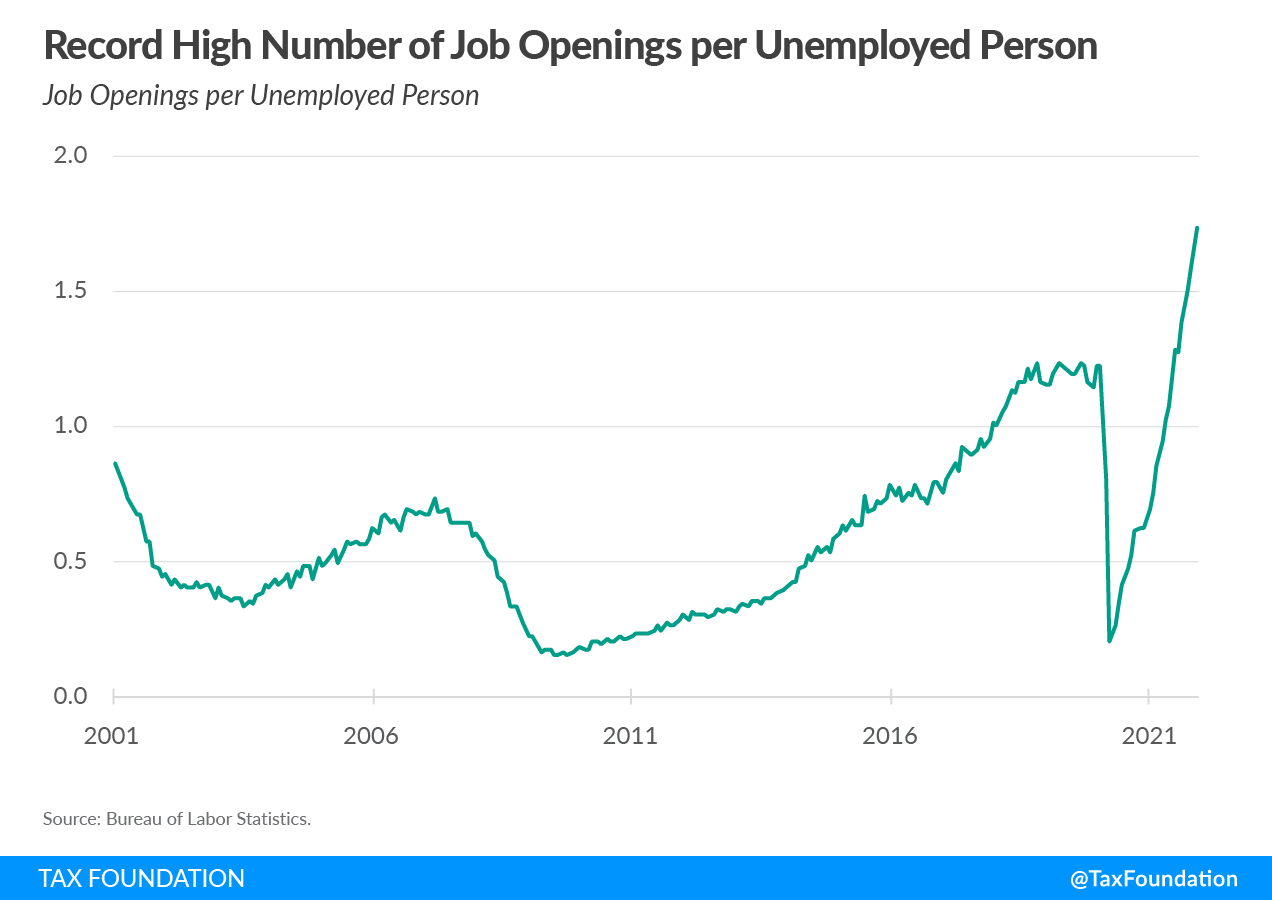

Increased geographic mobility combined with the “Great Resignation,”[1] in which millions of workers are pausing to reevaluate their careers, means for many Americans, opportunities are already on the rise. Since May of 2021, job openings have exceeded unemployment, an imbalance that continues to grow in favor of workers—currently about 1.7 job openings exist for every person unemployed, the highest on record.[2]

The increasingly tight labor market and extraordinary imbalance, however, are symptomatic of a more general mismatch in the economy in which demand (e.g., employer demand for labor and consumer demand for goods and services) far outstrips supply. Another symptom is inflation, which as of the latest reading hit 7.5 percent—the highest rate in 40 years—causing real (inflation-adjusted) earnings to fall 3.1 percent over the last year.[3] Inflation has been particularly hard on low-income households, as they spend a disproportionate share of their earnings on necessities such as food, energy, and housing, which have experienced relatively high rates of inflation.[4]

The return of high inflation after 40 years should cause policymakers to rethink their approach. In an effort to boost aggregate demand to offset the effects of the pandemic, policymakers pushed through an unprecedented $5 trillion of fiscal stimulus, including several rounds of economic impact payments and an expanded child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly., which far overshot the loss of earnings, leading to excess demand and inflation.[5] Rather than pushing for more stimulus, policymakers should now look for ways to relieve supply constraints and boost aggregate supply as much as possible to meet the demand.

Essentially, to the extent we can, we need to grow our way out of the problem by increasing the productive capacity of the economy; that is, increasing labor supply (hours worked and labor force participation) and capital investment in machines, factories, and research and development. As economist John Cochrane has noted, historical episodes of inflation, such as the 1970s, have ended only after some combination of monetary, fiscal, and microeconomic reforms improved incentives to work, save, and invest and raised the long-term growth trajectory of the economy.[6]

As such, the federal tax system is a key lever policymakers can use to improve incentives and long-run economic growth while containing inflation. Each of the reforms we consider here would help policymakers create a federal tax code that prioritizes economic growth and opportunity, creating the conditions for more investment, better jobs, higher real incomes, and improved standards of living.

They are reforms to ensure people can pursue new ideas and business ventures, create new opportunities for workers, realize upward mobility, and work toward greater financial security. Further, the tax reforms would simplify the tax code, create resilience against uncertainty and higher inflation, and increase the global competitiveness of the United States by attracting investment. Prioritizing economic growth and opportunity will lead to an environment where many of today’s challenges—from inflation and the national debt to the need for clean energy and affordable housing—can be addressed.

First, policymakers should aim to promote greater investment, innovation, dynamism, and competitiveness by improving the way the tax code treats private enterprise.

Business Tax Reforms:

- Better cost recoveryCost recovery refers to how the tax system permits businesses to recover the cost of investments through depreciation or amortization. Depreciation and amortization deductions affect taxable income, effective tax rates, and investment decisions. for capital investment: Implementing full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for short-lived capital investments and indexing the depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco schedules for buildings and factories (referred to as “neutral cost recovery”) would remove tax and inflation penalties from investments in physical assets, encouraging more investment to benefit workers and businesses.

- Better cost recovery and simpler treatment for Research & Development expenses: While the U.S. leads on many R&D fronts, our advantage is in jeopardy as tax and inflation penalties on R&D investments went into effect at the start of 2022. Reversing the penalties and simplifying the R&D tax credit so smaller businesses, start-ups, and entrepreneurs can effectively use the credit, will incentivize continued innovation.

- Maintain a competitive corporate tax system: The combined federal-state U.S. corporate tax rate of 25.8 percent ranks slightly above the OECD average of 22.7 percent—a substantial improvement made by the Tax Cuts and Jobs Act (TCJA) of 2017, prior to which the U.S. had the highest corporate tax rate in the developed world. As countries continue to compete for international investment, the U.S. should strive to maintain a competitive corporate tax rate. Similarly, the U.S. should reduce and simplify international tax rules to be consistent with rules found in other industrialized countries.

- Remove the double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. of corporate income: Shareholder taxes on capital gains and dividends are layered on top of corporate taxes. Many countries have reduced the double taxation of corporate income by more fully integrating the individual and corporate tax codes, which reduces distortions, lowers the cost of capital, and encourages investment.

- Clean up the structure of the business tax code: It is possible to raise large amounts of tax revenue while cleaning up the structure of the business tax code by eliminating unsound business tax expenditures. The additional revenue can offset the cost of other improvements to the business tax code while simplifying taxes for businesses.

- Return to competitive, free trade policies: Since 2018, the United States has embarked on a trade war to shield legacy industries from competitive pressures while failing to address trade practices of other nations. Removing the tariffs, which have created higher prices for U.S. consumers and businesses, is another way to ensure industries remain competitive and consumers and businesses do not face disadvantages compared to others around the globe.

Jump to detailed business tax reforms.

Second, policymakers should remove barriers to work and investment, aim to help individuals and families save for the future, and take the fear out of filing taxes.

Individual Income Tax Reforms:

- Streamline social benefits: The complicated nature of today’s tax credit system presents an opportunity for reforms to simplify the filing process for taxpayers and administrators by consolidating child-related benefits into one provision and work-related benefits into another.

- Remove tax barriers from personal saving: Just as Americans enjoy the benefits of saving for retirement through a 401(k) or Roth IRA, they should also be able to save for any purpose—e.g., to finance education, housing, a new business venture, or career transition—without getting penalized for it. Universal savings accounts (USAs) would apply the proper tax treatment to saving in general, with only one layer of taxation at the time of either contribution or withdrawal.

- Clean up the structure of the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source code: It is also possible to raise large amounts of revenue while cleaning up the structure of the individual tax code, resulting in a simpler, more neutral tax system across households. The revenue raised can be used to offset the cost of individual tax reforms, including permanent reductions of marginal tax rates.

- Inflation index features of the tax code not indexed for inflation: Several individual income tax parameters remain unindexed for inflation, meaning higher levels of inflation can artificially increase individual tax burdens. Better inflation indexingInflation indexing refers to automatic cost-of-living adjustments built into tax provisions to keep pace with inflation. Absent these adjustments, income taxes are subject to “bracket creep” and stealth increases on taxpayers, while excise taxes are vulnerable to erosion as taxes expressed in nominal dollars, rather than rates, slowly lose value. across the individual income tax code will ensure the tax code is structured to account for inflation, though the income tax system itself is inherently prone to inflation-related issues.

Jump to detailed individual income tax reforms.

Business Tax Reforms:

Better cost recovery for capital investment

If we aim to grow the workforce and become more productive, it requires thriving businesses investing in new equipment and technology, expanding facilities and locations, and hiring and training workers. Workers in particular are better off when investment increases. The tax code, however, creates an impediment to productivity-enhancing investments, as some opportunities for businesses and workers never occur because the tax code is standing in the way.

High corporate taxes in particular have been shown to depress investment and constrain economic prosperity.[7] For example, an OECD study examining data from 63 countries concluded corporate income taxes are the most economically damaging way to raise revenue, followed by individual income taxes, consumption taxes, and property taxes.[8]

Several studies demonstrate the corporate tax is borne by both workers and shareholders across the income spectrum.[9] For instance, a study of corporate taxes in Germany found workers bear about half of the tax burden in the form of lower wages, with low-skilled, young, and female employees disproportionately harmed.[10]

Improving the tax code’s capital cost recovery rules is crucial in the effort to increase business investment and create better opportunities for workers. Under the U.S. tax code, businesses can generally deduct their ordinary business costs, such as paying workers’ wages or utility bills, when calculating their income for tax purposes—and rightly so, as profit is defined as revenue less the cost of earning revenue.

Full deductions, however, are not always provided when businesses spend money on physical capital, such as a new facility. Typically, when businesses incur capital costs, they must deduct the costs over several years according to depreciation schedules set by lawmakers instead of deducting them immediately in the year the purchase occurs.

Delays mean the real value of the deduction, after adjustments for inflation and the time value of money, is less than the original cost—how much less valuable depends on the rate of inflation and the discount rate. Delays also increase the after-tax cost of making investments. A higher after-tax cost for investment leads to a lower level of investment, reduced productivity and output, and fewer opportunities for workers. High inflation makes the tax penalty for investments worse by further reducing the value of deductions over time.

Allowing a full and immediate deduction for all investment, i.e., full expensing, would go a long way toward simplifying the tax code and mitigating the effects of inflation, while ending the bias against investment created by the delay in depreciation deductions. Empirical evidence indicates accelerated depreciation policies increase employment opportunities[11] and can lead to higher wages.[12]

Through bonus depreciation, the current cost recovery system permits full and immediate deductions for investments in short-lived assets like machinery and equipment through 2022, after which the provision will phase down until it fully expires after 2026. Longer-lived assets do not qualify for the temporary bonus provision and face much harsher treatment. For example, when a business purchases a structure, it has to deduct the cost over a period of up to 27.5 years for a residential building or 39 years for a commercial building.

Making bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. a permanent part of the tax code would reduce the tax cost of investing in machinery and equipment, giving businesses a degree of certainty in their investment plans. For long-lived assets, which tend to be large and irregular investments, implementing a policy known as neutral cost recovery can provide better treatment.[13] Under neutral cost recovery, the current depreciation schedules for residential and nonresidential buildings would remain, and the deductions would be adjusted for inflation and the time value of money to compensate for delay.

Reducing the cost of making an investment in a new factory or better equipment by removing the tax hurdle standing in the way of such business decisions would create more employment opportunities for workers and lead to real wage growth. It would help put capital-intensive sectors, such as manufacturing and other heavy industry, on even footing with capital-light sectors, as both would get full deductions for their business expenses.

Better cost recovery for R&D and a simpler R&D tax credit

R&D investment is an important contributor to economic growth and technological innovation. The tax code, however, can make it difficult to engage in R&D because it delays deductions for R&D expenses and offers a complicated R&D tax credit.[14] R&D investment incentives can be improved by permitting R&D expenses to be fully expensed permanently and by simplifying the R&D tax credit’s design.

Just as it is important to provide full cost recovery for capital investment overall, R&D investment should also be provided a full and immediate deduction. Starting in 2022, R&D expenses must be deducted over five years, a policy established under the TCJA. Requiring R&D to be amortized is highly unusual, as R&D expenses have been immediately deductible in the U.S. since 1954.[15]

Fully expensing R&D investment would make the tax code simpler while increasing the incentive to invest in R&D. Ideally, full expensing of R&D investment would be restored on a permanent basis. Permanence would ensure that firms can innovate without uncertainty about the tax burden of their investments.[16]

The tax code also provides four separate R&D tax credits to encourage R&D investment by lowering a firm’s tax liability based on its spending on qualified research expenditures. In addition to the regular credit, the tax code provides an alternative simplified credit, a credit intended to encourage R&D in energy, and a credit in partnership with universities.

Firms, especially small and new firms, face several challenges when claiming the R&D tax credit, including difficulties defining what research qualifies for the credit. Up to 30 percent of the credit’s value is commonly unclaimed because of administrative hurdles.[17] Small businesses often are the most impacted: one study from the Small Business Administration (SBA) found less than 3 percent of the value of R&D tax credits went to small businesses.[18]

Another reason the R&D tax credit is less valuable for small businesses is because they often do not have tax liability to offset due to a lack of initial profitability. The credit can be made more valuable for smaller firms by carrying forward the value of the credit with an adjustment for the loss in value from deferring the credit.

The R&D tax credit could also be simplified by matching the R&D expenses eligible for the credit to the definition of R&D expenses eligible for expensing. Another option is to replace the four different credits with a simplified alternative to streamline the entire process.[19] The simplified approach would make the existing alternative simplified credit more generous by making the minimum credit value equal to 50 percent of a firm’s current-year research expenses while eliminating the regular credit altogether.[20] The Government Accountability Office (GAO) argues it would “reduce the revenue cost of the credit without affecting the average incentive it provides for research.”[21]

Maintain a competitive corporate tax system

Corporate taxes matter for competitiveness. In the global race to attract highly mobile corporate investment, the corporate tax is an important policy lever, as several studies have found a measurable effect on foreign direct investment.[22] In addition, a low and competitive corporate tax rate serves to reduce tax avoidance and profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens., bolstering the corporate tax base and stabilizing corporate tax revenue.[23]

As such, it is wise to keep the corporate tax rate as low and competitive as possible. The TCJA significantly reduced the corporate tax rate and brought it into closer alignment with peer nations, but at the same time added a new and complex tax applicable to the foreign income of U.S-based multinational enterprises (MNEs). Known as GILTI (Global Intangible Low-taxed Income), it uniquely applies to U.S. firms over and above corporate tax paid to foreign governments on earnings abroad.

While other countries currently have no such GILTI tax, approximately 140 countries have agreed to implement a global minimum tax of 15 percent applicable to domestic and foreign income on a country-by-country basis by 2023. To the extent foreign legislatures follow through with the agreement, U.S. companies may soon need to comply with minimum taxes implemented in each country in which they operate, in addition to GILTI. As such, policymakers in the U.S. should consider ways to simplify the U.S. tax code in a manner consistent with the global minimum tax agreement.

One option is to replace the GILTI regime with a simplified worldwide tax system, with one statutory tax rate for both domestic and foreign income. Such a reform would substantially trim or eliminate huge sections of the tax code relating to foreign income and base erosion, including the complex Subpart F rules that date to the 1960s. The worldwide system would have the following characteristics:

- A low tax rate consistent with the international agreement

- Full expensing for investment

- Full credit for foreign taxes against U.S. tax, to avoid or minimize double taxation

- No tax preferences that are not recognized by the global minimum tax[24]

In the event the global minimum tax agreement unravels, or is otherwise nonbinding or lacking in enforcement, the U.S. should reorient its international tax code to match rules found in other industrialized countries. In particular, the U.S. should consider replacing the GILTI regime with a more simplified territorial system, largely exempting foreign income from U.S. tax. Short of that, several incremental reforms to the GILTI regime would simplify the rules and improve U.S. competitiveness, including repeal of expense allocation rules and the haircut on foreign tax credits.[25]

Remove the double taxation of corporate income

The U.S. taxes businesses differently depending on their legal structure. Pass-through businesses, such as sole proprietorships, partnerships, and S corporations, pay only one layer of tax at the shareholder level through the individual income tax code. C corporations face two layers of tax: one at the entity level through the corporate income tax and a second at the shareholder level through capital gains and dividends taxes.

Double taxation of corporate income increases the cost of investment for corporations, encourages a shift from the traditional C corporate form to pass-through form, and incentivizes debt financing. Removing the double taxation of corporate income would level the playing field among different forms of businesses, reduce the tax burden on investment, and reduce distortions affecting business financing decisions. In other words, it would free up wasted resources and reduce tax barriers for investment, leading to more viable opportunities for both businesses and workers.

The U.S. currently reduces double taxation of corporate income by taxing long-term capital gains and qualified dividends at lower rates than ordinary income. Even when accounting for the lower shareholder-level rates, the U.S imposes an average federal-state combined tax rate of about 29 percent on capital gains and dividend income, higher than the OECD average of 23.9 percent on capital gains and 19.1 percent on dividend income.[26] [27]

Table 1 illustrates how the two layers of tax on corporate income combine to create a 47.4 percent integrated tax rate in the U.S., accounting for corporate and dividend taxes at the federal and state levels.[28] The U.S. integrated rate is higher than the OECD average of 40.1 percent.[29] The same double taxation occurs even when a corporation retains its after-tax earnings rather than distributing them as dividends. When corporate earnings are retained, the value of the stock rises to reflect an increase in assets held by the corporation. Shareholders who decide to sell their stock will realize a capital gain and pay a tax on it, facing a tax rate similar to the tax rate on dividends.

| Integrated Tax Rate Under Current Law | |

|---|---|

| A. Corporate Profits | $100.00 |

| B. Combined Corporate Income Tax | $25.75 |

| C. Distributed Dividend (A-B) | $74.25 |

| D. Combined Dividend Income Tax | $21.67 |

| E. Total After Tax Income (C-D) | $52.58 |

| Integrated Tax Rate (A-E) / A | 47.4% |

| Sources: State tax statues; Tax Foundation calculations. | |

Eliminating, or further reducing, the double taxation of corporate income can be accomplished by integrating the individual and corporate tax codes, as many other countries have done. For example:

- Australia integrates its corporate and individual income tax with a tax credit imputation. The corporation and the shareholder both pay part of the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax., but the shareholder is given a tax credit to offset the taxes already paid by the corporation. In the end, corporate income is taxed at the marginal income tax rate of shareholders. Including Australia, nine OECD countries have full or partial credit imputation systems.

- Estonia integrates its corporate and individual income tax by having a full dividend exemption at the shareholder level so only one layer of tax is applied at the corporate level on distributed corporate income. When an Estonian corporation makes a profit and distributes it to shareholders, it must pay the corporate income tax, but shareholders do not have to pay any additional taxes on the distributed dividends. The total tax on distributed profits between the corporation and the individual is therefore determined by the corporate tax rate. Including Estonia, six OECD countries have full or partial dividend exemptions.[31]

- Twelve countries either partially or fully exempt capital gains from individual-level taxation, which eliminates the double taxation of retained earnings. For example, Australia and Canada provide a 50 percent deduction (50 percent of a capital gain is tax-exempt) for capital gains, while New Zealand does not tax capital gains at all. Estonia, uniquely, exempts retained earnings at the corporate level but taxes capital gains at the individual level as ordinary income.

Although adopting such a system would have administrative challenges because the U.S. taxes corporations and pass-throughs differently, following other developed countries and integrating our corporate and individual tax codes would encourage more investment by reducing the tax burden on corporate income.

Clean up the structure of the business tax code

The Treasury Department releases an analysis of tax expenditures in the U.S. code each year.[32] Some provisions categorized as expenditures are important structural elements of the tax code, while others represent non-neutral or wasteful subsidies. Eliminating the latter can be a productive way to offset the cost of other business tax reforms.

Non-neutral tax expenditures can inhibit growth by reallocating investment to otherwise less productive areas, rather than increasing capital investment and growth across the whole economy. In 2021, we estimated eliminating various business tax expenditures (excluding structurally important provisions related to cost recovery, foreign income, or deferred income) would raise more than $900 billion over the next decade at minimal cost to economic growth.[33]

For example, the Low-Income Housing Tax Credit (LIHTC) is not particularly effective in generating new affordable housing investment because of its complex bureaucracy.[34] When it was created in 1986, the LIHTC was paired with worsening cost recovery for residential structures generally. Soon after, housing construction, particularly multifamily housing construction, collapsed.[35]

Improved cost recovery for investment in residential structures would be a simpler way to encourage new construction. A similar case could be made regarding certain clean energy subsidies, where better tax treatment of capital would sufficiently incentivize new, low-emissions technology.[36]

Table 2 suggests a list of tax subsidies lawmakers could consider repealing. Reducing the number of ineffective tax expenditures in the business tax code can free up revenue to put toward more effective policies such as full expensing. Doing so would increase investment and opportunity in the economy while minimizing the impact to the federal budget deficit.

| Expenditure | 10-Year Corporate Revenue Cost (2022-2031) | 10-Year Individual Revenue Cost (2022-2031) |

|---|---|---|

| Low-Income Housing Credit | $103.8 billion | $5.46 billion |

| Energy Production Credit* | $47.64 billion | $5.29 billion |

| Energy Investment Credit* | $55.04 billion | $4.94 billion |

| Credit Union Exemption | $25.33 billion | $0 billion |

| New Markets Tax Credit* | $11.21 billion | $0.23 billion |

| Enhanced Oil Recovery Credit | $9.50 billion | $0.52 billion |

| Tax Incentives for Preservation of Historic Structures | $7.31 billion | $1.86 billion |

| Exclusion for Municipal Bond Interest | $71.86 billion | $384.57 billion |

| Special Deduction for Blue Cross, Blue Shield Companies | $4.03 billion | $0 billion |

| Total | $335.72 billion | $402.87 billion |

|

* Temporary policies which are scheduled to expire in the budget window and would not be a source of long-term revenue. Note: Treasury Department tax expenditures estimates do not necessarily equal the increase in federal receipts that would result from repeal. Source: Author’s calculations; Office of Tax Analysis, “Tax Expenditures,” U.S. Department of the Treasury, December 2021, https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures. |

||

Return to competitive free trade policies

Since the end of World War II, the world has largely shifted from protectionist trade policies toward a rules-based, open trading system. Over time, increased trade has led to widespread benefits, including higher productivity in the United States and large increases in Americans’ standard of living.[38] While trade makes a nation wealthy, trade restrictions make a nation poorer.[39]

In 2018 the Trump administration reversed the trend and began imposing trade restrictions in the form of import taxes, or tariffs, on washing machines and solar panels, steel and aluminum, and a wide range of goods from China. Tariffs protect domestic industry from foreign competition, and proponents argue the protection provides time for domestic companies to regain their footing and competitiveness. Protection instead typically backfires; industries become stagnant without foreign companies competing with them for the domestic market. Tariffs on one good also raise costs for other domestic manufacturers as well as consumers and trigger retaliatory tariffs from other countries, further harming domestic production.

The Trump administration intended for the tariffs to revive the manufacturing sector, create jobs in the United States, and lead to fairer trading practices with China. The tariffs have not had the intended effect.

U.S. businesses have had to pay more than $140 billion in import taxes since the tariffs were imposed.[40] Rather than increase opportunities for workers, research shows the tariffs led to a net decrease in manufacturing employment. While employment in protected industries increased slightly, the increase was more than offset by decreases in employment in other industries, caused by higher prices and retaliatory tariffs.[41] Researchers concluded “tariffs have been a drag on employment and have failed to increase output.” Wide-ranging research also shows the tariffs led to higher prices for a variety of goods purchased by U.S. businesses and retail consumers.[42]

After four years, the tariffs have not resulted in employment gains or better prices for U.S. consumers. They have likewise failed to produce better trading conditions.[43] Instead of removing the tariffs entirely, the Biden administration has retained most tariffs with some modifications or exclusions and moved toward managed trade.[44] Fully removing the tariffs and restoring free trade practices is perhaps the most readily available, timely, and effective means to support U.S. industry and jobs while lowering costs for consumers.

Individual Income Tax Reforms

Streamline social benefits

The U.S. tax code currently provides two major support programs to working families: the Child Tax Credit (CTC) and the Earned Income Tax Credit (EITC). The CTC and the EITC are the two largest anti-poverty programs in the United States,[45] both by encouraging work and supplementing wages. The EITC contains strong work incentives demonstrated to increase employment, especially among low-income mothers, and it lifts about 5 million children out of poverty each year.[46] The CTC lifts about 1.7 million out of poverty each year.[47] The two credits are also costly. In 2022, the EITC is estimated to reduce federal revenue by $71.3 billion and the CTC by $115.6 billion.[48]

The credits are also unnecessarily complicated. Under current law, the EITC varies based on a household’s income and number of qualifying children. The credit for households without qualifying children is less than 1/6 the size of the credit offered to households with one child. The EITC contains significant marriage penalties, reducing or entirely eliminating benefits when a head of household filer marries a childless single filer. For example, the married filing jointly thresholds are not twice the size of the other thresholds but are instead only roughly $6,000 higher.[49]

The CTC reduces tax liability by up to $2,000 per qualifying child, with up to $1,500 refundable. The refundable portion phases in with earned income. Taxpayers may separately qualify for a $500 nonrefundable other dependent tax credit (ODTC). The CTC phases out for joint filers with incomes above $400,000 and single filers with incomes above $200,000.[50] After the end of 2025, the CTC will revert to a $1,000 credit, phasing out at $110,000 for joint filers and $75,000 for single filers.

The American Rescue Plan temporarily changed both credits for 2021. It expanded the EITC for workers without qualifying children by increasing the phase-in rate, raising the maximum credit from $530 to nearly $1,502, and raising the phaseout levels. It reduced the eligibility age from 25 to 19 for most workers and eliminated the upper age limit. It also expanded the CTC in three ways: for children under 6, the new max was $3,600 and for children ages 6 to 17 it was $3,000; the full amount of the credit was refundable and not subject to an income-based phase-in; and half the credit was distributed in advanced monthly payments. The EITC changes for taxpayers without qualifying children cost $11.8 billion, while the CTC changes cost more than $100 billion.[51] The changes have now expired.

The two credits depend on often-complicated family characteristics, leading to administrative challenges. For example, to qualify for the EITC, taxpayers must meet at least 20 requirements.[52] Partially as a result, the EITC suffers from a relatively high rate of incorrectly issued payments, including both overpayments and underpayments—mostly due to qualifying child errors.[53] The relationship, residency, and identification tests legally required to qualify for the CTC are likewise difficult for taxpayers to comply with and for the IRS to enforce, especially for families with complex living arrangements.[54]

One way to address the challenges would be to consolidate child-related benefits into one provision and work-related benefits into another.[55] Ideally, a child-related benefit would be moved out of the tax code and instead be administered by another agency, such as the Social Security Administration.

If designed carefully, reforms can be structured so changes in marginal rates boost work incentives and encourage more participation in the labor force, on net.[56] For example, as an alternative to the 2021 CTC changes, increasing the value of the EITC could significantly reduce poverty at a much lower cost while boosting, rather than reducing, employment.[57]

As another example, the Family Security Act[58] would eliminate the current CTC and replace it with a child allowance of $4,200 per child under age 6 ($350 per month) and $3,000 per child ages 6 to 17 ($250 per month), administered through the Social Security Administration.[59] The Act would reform the EITC by turning it into an earnings credit with a maximum amount of $1,000 per adult, no marriage penalties, and an extra $1,000 benefit for households with adult dependents. The Act proposes eliminating the State and Local Tax (SALT) deduction, Head of Household filing status, the Child and Dependent Care Tax Credit, and the Temporary Assistance for Needy Families program, and making eligibility changes to the Supplemental Nutrition Assistance Program (SNAP), to reduce the long-term fiscal impact.

Reforms to the CTC and EITC should also consider other household-related provisions, such as personal and dependent exemptions and standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. sizes as well as marriage and second-earner penalties.[60] If the CTC is moved outside the tax code, restoring dependent exemptions would be one way to continue adjustments for household size within the tax code.[61]

Reducing poverty is a key objective of reforms to the CTC and EITC. Simplifying and moving the CTC out of the tax code, while ensuring the tax code still accounts for household size, combined with a stronger and simpler earnings-based credit, would support a dynamic and open economy, helping ensure workers and families enjoy financial security by increasing the return to work.

Remove tax barriers from personal saving

Robust personal savings is an important part of financial security, enabling investment and economic opportunity in the United States. Unfortunately, the tax code creates many barriers for individuals who wish to put money away for the future with complicated rules and double taxation of saving, often incentivizing consumption over saving.[62]

The ideal tax code would ensure consumption and saving are treated neutrally. A tax-neutral approach to saving would also make it easier for Americans to build wealth and take advantage of opportunities requiring savings, such as buying a new home, supporting charitable causes, and helping their communities.

Instead, our tax code discourages saving with multiple levels of taxation: a dollar of income is taxed when earned under the income tax, again when it’s invested and earns additional profits, again when reinvested earnings are realized as a gain and face capital gains taxes, and potentially again when gifted to heirs through estate and gift taxes.[63]

Multiple layers of tax encourage immediate consumption over saving because the consumption is subject to only one layer of tax when the income is initially earned. It has negative economic impacts by reducing the amount of savings available for productive investment in the United States.[64] A smaller pool of domestic savings also means that foreign savers may fund domestic opportunities, reducing domestic investment returns accruing to domestic savers.

Currently, taxpayers can mitigate some of the tax penalty for saving by contributing to tax-neutral savings accounts dedicated to specific purposes, such as traditional or Roth retirement accounts and/or education savings accounts.

Allowing the saver to defer income taxes on the amount they save and only pay taxes on account distributions (known as a “traditional” account), or by taxing the earnings up front but exempting the returns to saving from additional income tax (known as a “Roth” account), removes the tax bias against saving. The treatment ensures saving done through such accounts is only taxed once, on par with income that is consumed.

Existing tax-neutral savings accounts have complicated and arbitrary rules and restrictions governing when distributions can be taken, how much can be deposited in each account, and how the savings can be used. While the limitations are intended to encourage savers to think ahead for retirement or their children’s education expenses, they also discourage saving by creating roadblocks and compliance costs for taxpayers.

Streamlining or removing complex rules to create universal savings accounts could encourage further saving and simplify the tax process. Rather than sitting down to plan what type of account can be used for what type of expense and when, what rules need to be followed, and whether one meets the requirements in a given year, universal savings accounts would allow individuals to set aside a given amount of money each year for any purpose, without worrying about tax penalties or restrictions on how to spend the money.

For example, other countries, such as the United Kingdom and Canada, provide universal savings accounts up to a maximum contribution threshold.[65] The programs are heavily utilized by taxpayers of all income levels, especially low-income taxpayers. The experience in other countries suggests universal savings accounts in the United States would broadly increase savings, improve financial security, and enhance opportunity for all Americans.[66]

Clean up the structure of the individual income tax code

True tax reform has traditionally been centered around the idea of lowering tax rates and broadening the tax base. Economists have long warned and well documented the economic damage of a high marginal income tax rate, as it reduces incentives to work, save, and invest. The budgetary cost of lowering marginal tax rates can be offset by eliminating certain deductions, exclusions, and credits.

After 2025, most of the changes made to the individual tax code under the TCJA will expire. Individual income tax rates were reduced from 10 percent, 15 percent, 25 percent, 28 percent, 33 percent, 35 percent, and 39.6 percent to 10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent, and 37 percent, respectively, and the widths of individual income tax brackets were adjusted. Making the TCJA rate and bracket changes permanent would increase long-run GDP by 0.9 percent and reduce federal revenue by $1.36 trillion from 2022 through 2031, when the tax cuts are scheduled to expire.[67] Other simplifying components of the TCJA, such as elimination of the Pease limitation and the Alternative Minimum Tax, should also be prioritized for permanence.

Other options to lower marginal rates include consolidating the current seven brackets into three with a top rate of 35 percent, which would increase long-run GDP by 1.3 percent at a budgetary cost of about $2.7 trillion over 10 years after accounting for economic growth.[68]

Offsetting the budgetary cost of lower marginal rates can be accomplished through many different base-broadening options. Under current law, health insurance provided by employers is not included as taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. , which leads employees to favor health insurance over regular wages as compensation. The distortion leads to more spending on overly comprehensive insurance plans than would otherwise occur, creating upward pressure on health-care costs. The exclusion for employer-provided health insurance is estimated by the Treasury Department to cost $3.0 trillion over 10 years, making it the single largest tax expenditureTax expenditures are departures from a “normal” tax code that lower the tax burden of individuals or businesses through an exemption, deduction, credit, or preferential rate. However, defining which tax expenditures grant special benefits to certain groups of people or types of economic activity is not always straightforward..[69] The exclusion also affects payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. receipts; the Treasury Department estimates it will reduce payroll tax receipts by $140 billion in 2022 and by more than $1.6 trillion from 2021 through 2030. As an alternative to revoking the entire exclusion, it could be capped so that health insurance benefits above the cap would be taxed as ordinary income.

A number of other exclusions narrow the income tax base and lead to significant distortions, such as the exclusion for municipal bond interest, which Treasury estimates costs nearly $291 billion for individuals over 10 years.

While much smaller, and scheduled to expire over the next decade, tax credits for energy-efficient home improvements and electric vehicles are disproportionately claimed by wealthier households[72] and are relatively inefficient ways to encourage the use of cleaner energy sources.

Other potential offsets would raise large amounts of revenue but would need to be weighed against substantial economic costs. For example, eliminating the deduction for state and local taxes would raise nearly $1.6 trillion over 10 years and reduce long-run GDP by 0.7 percent,[73] while eliminating the home mortgage interest deductionThe mortgage interest deduction is an itemized deduction for interest paid on home mortgages. It reduces households’ taxable incomes and, consequently, their total taxes paid. The Tax Cuts and Jobs Act (TCJA) reduced the amount of principal and limited the types of loans that qualify for the deduction. would raise nearly $1.0 trillion and reduce GDP by 0.7 percent.[74]

As Table 3 illustrates, many options are available to broaden the tax base and offset the cost of lower tax rates in a revenue neutral fashion to stabilize the federal budget and grow the economy.

| Expenditure | 10-Year Revenue from Individuals (2022-2031) |

|---|---|

| Exclusion of employer contributions for medical insurance premiums and medical care | $3.0 trillion |

| Exclusion of interest on public purpose state and local bonds | $290.8 billion |

| Credit for energy efficiency improvements to existing homes* | $120.0 million |

| Credit for residential energy-efficient property* | $4.5 billion |

| Tax credits for clean-fuel-burning vehicles and refueling property* | $2.9 billion |

| Deductibility of mortgage interest on owner-occupied homes^ | $798.4 billion |

| Deductibility of state and local property tax on owner-occupied homes^ | $384.4 billion |

| Deductibility of nonbusiness state and local taxes other than on owner-occupied homes^ | $760.9 billion |

| Total | $5.2 trillion |

|

* Temporary policies which are scheduled to expire in the budget window and would not be a source of long-term revenue. ^ Limits on policies are scheduled to expire in the budget window. Eliminating raises more revenue in the latter half of the budget window. Note: Treasury Department tax expenditures estimates do not necessarily equal the increase in federal receipts that would result from repeal. Source: Office of Tax Analysis, “Tax Expenditures,” December 2021, U.S. Department of the Treasury, https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures. |

|

Inflation index structural features of the tax code not indexed for inflation (where appropriate)

Inflation indexing some parts of the individual income tax code, namely structural elements like brackets, is relatively straightforward. Currently, ordinary income tax brackets are adjusted for inflation to help prevent bracket creepBracket creep occurs when inflation, or real income growth, pushes taxpayers into higher income tax brackets. Bracket creep results in an increase in income taxes without an increase in real income. Many tax provisions—both at the federal and state levels—are adjusted for inflation. Over time, bracket creep can increase how much income tax people owe as their income grows, either due to inflat–which occurs when inflation pushes taxpayers into higher tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. even though their income may not be higher in real terms. Several other provisions, like the standard deduction, EITC, and the refundable portion of the CTC, are also indexed for inflation.

Some structural provisions, however, are not indexed to inflation.

When measuring taxable income, it makes sense to subtract capital losses as capital losses offset capital gains. Having a limit on capital losses helps prevent abuse of the provision, but the limit should be increased from the current law of $3,000 to reflect the significant inflation that has occurred between 1978 and today, and adjusted going forward.[75]

The Net Investment Income Tax (NIIT) is a 3.8 percent tax on investment income for married tax filers earning over $250,000 in adjustable gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods and for single filers earning over $200,000 in adjustable gross income. Its thresholds have not been adjusted since the law was introduced a decade ago, so more taxpayers will be pushed into paying the NIIT although it initially targeted the very rich alone.

Outside of the structural elements, the income tax base itself is inherently prone to complex issues related to inflation. For instance, under current law, taxpayers pay capital gains tax on the difference between the purchase price of an asset (also known as the basis) and the price when sold. The basis, however, is not adjusted for inflation, so while on paper it may look like someone earned income, after accounting for inflation it is possible they may have lost money. Adopting a system of universal savings accounts, to the extent it broadly applies, would effectively address the problem of taxing nominal capital gains.

In combination, inflation indexing the structural elements of the code currently not indexed and adopting universal savings accounts would better account for inflation in the tax code, providing more certainty for taxpayers, reducing penalties on saving, and strengthening financial security.

Conclusion

As the American people step into the post-pandemic era, policymakers must keep up, or they risk jeopardizing the economic growth and opportunity our changing economy can offer. Implementing the business and individual tax reforms outlined here would align the tax code to greater economic growth and opportunity for American businesses and people. By reducing the tax code’s current barriers to investment and saving and simplifying its complex rules, lawmakers would greatly enhance the ability of Americans to pursue new ideas, create more opportunities, and build financial security for themselves and their families.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] Shawn Baldwin, “The Great Resignation: Why millions of workers are quitting their jobs,” CNBC, Oct. 19, 2021, https://www.cnbc.com/2021/10/19/the-great-resignation-why-people-are-quitting-their-jobs.html.

[2] Paul Davidson, “Great Resignation: Job openings rose, quitting dropped modestly from record high in December, JOLTS report shows,” USA TODAY, Feb. 1, 2022, https://www.usatoday.com/story/money/2022/02/01/great-resignation-continues-americans-quit-jobs-near-record-pace/9293122002/.

[3] U.S. Bureau of Labor Statistics, “Real Earnings Summary,” Feb. 10, 2022, https://www.bls.gov/news.release/realer.nr0.htm.

[4] Rachel Siegel and Andrew Van Dam, “‘Survival Mode’: Inflation Falls Hardest on Low-Income Americans,” The Washington Post, Feb. 13, 2022, https://www.washingtonpost.com/business/2022/02/13/low-income-high-inflation-inequality/.

[5] Lawrence H. Summers, “The Biden Stimulus is Admirably Ambitious. But It Brings Some Big Risks, Too,” The Washington Post, Feb. 4, 2021, https://www.washingtonpost.com/opinions/2021/02/04/larry-summers-biden-covid-stimulus/.

[6] Cochrane argues that tax and regulatory reforms in the 1980s improved long-run economic growth leading to budget surpluses in the late 1990s. See John H. Cochrane, “The Fiscal Theory of the Price Level: An Introduction and Overview,” forthcoming in the Journal of Economic Perspectives, https://static1.squarespace.com/static/5e6033a4ea02d801f37e15bb/t/61b79f3e95fc6559bce8ed34/1639423807095/Fiscal_theory_JEP.pdf.

[7] William McBride, “What is the Evidence on Taxes and Growth,” Tax Foundation, Dec. 18, 2012, https://www.taxfoundation.org/what-evidence-taxes-and-growth/; see also Alex Durante, “Reviewing Recent Evidence of the Effect of Taxes on Economic Growth,” Tax Foundation, May 21, 2021, https://www.taxfoundation.org/reviewing-recent-evidence-effect-taxes-economic-growth/.

[8] Åsa Johansson, Christopher Heady, Jens Matthias Arnold, Bert Brys, and Laura Vartia, “Taxation and Economic Growth,” Organisation for Economic Co-Operation and Development Working Paper No. 620, July 3, 2008, https://www.oecd-ilibrary.org/economics/taxation-and-economic-growth_241216205486.

[9] Stephen J. Entin, “Labor Bears Much of the Cost of the Corporate Tax,” Tax Foundation, Oct. 24, 2017, https://www.taxfoundation.org/labor-bears-corporate-tax/; Alex Durante, “Who Bears the Burden of Corporate Taxation? A Review of Recent Evidence,” June 10, 2021, https://www.taxfoundation.org/who-bears-burden-corporate-tax/; and William McBride, “Testimony: Joint Economic Committee Hearing on the Revenue Provisions of the Build Back Better Act,” Oct. 6, 2021, https://taxfoundation.org/build-back-better-revenue-joint-economic-committee-tax/.

[10] Clemens Fuest, Andreas Peichl, and Sebastian Siegloch, “Do Higher Corporate Taxes Reduce Wages? Micro Evidence from Germany,” American Economic Review 108:2 (February 2018): 393–418, https://www.doi.org/10.1257/aer.20130570.

[11] E. Mark Curtis, Daniel G. Garrett, Eric C. Ohrn, Kevin A. Roberts & Juan Carlos Suárez Serrato, “Capital Investment and Labor Demand,” National Bureau of Economic Research, November 2021, https://www.nber.org/papers/w29485.

[12] Eric Ohrn, “The Effect of Tax Incentives on U.S. Manufacturing: Evidence from State Accelerated Depreciation Policies,” Journal of Public Economics 108 (December 2019), https://www.sciencedirect.com/science/article/abs/pii/S0047272719301458.

[13] Erica York, Alex Muresianu, and Garrett Watson, “FAQ on Neutral Cost Recovery and Expensing,” Tax Foundation, July 10, 2020, https://www.taxfoundation.org/neutral-cost-recovery-full-expensing-faq/.

[14] Alex Muresianu and Garrett Watson, “Reviewing the Federal Tax Treatment of Research & Development Expenses,” Tax Foundation, Apr. 13, 2021, https://www.taxfoundation.org/research-and-development-tax/.

[15] Gary Guenther, “Research Tax Credit: Current Law and Policy Issues for the 114th Congress,” Congressional Research Service, June 18, 2016, https://www.everycrsreport.com/files/20160618_RL31181_ac919b4772ff5f454f8cedd2dd7aa8b290950a41.pdf.

[16] Garrett Watson, “Delaying R&D Amortization Costs Less but Generates Little Economic Benefit Compared to Full Cancellation,” Tax Foundation, July 29, 2021, https://www.taxfoundation.org/r-d-amortization-changes/.

[17] Pamela Sommers, “The Ripple Effects of an R&D Tax Credit Study’s Real Costs,” Thomson Reuters, accessed Feb. 10, 2022, https://www.silo.tips/download/the-ripple-effect-of-an-rd-tax-credit-study-s-real-costs.

[18] John O’Hare, Mary Schmitt, and Judy Xanthopoulos, “Measuring the Benefit of Federal Tax Expenditures Used by Small Business,” Small Business Administration, Office of Advocacy, November 2013, https://www.novoco.com/sites/default/files/atoms/files/measuring_tax_expenditures_111113.pdf; see also Garrett Watson, “Tax Expenditures Taken by Small Businesses in the Federal Tax Code,” Tax Foundation, Aug. 5, 2019, https://www.www.taxfoundation.org/small-business-tax-expenditures/.

[19] Government Accountability Office, “The Research Tax Credit’s Design and Administration Can Be Improved,” Nov. 6, 2009, https://www.gao.gov/products/gao-10-136.

[20] Ibid.

[21] Ibid.

[22] See, for instance, Ronald B. Davies, Iulia Siedschlag, and Zuzanna Studnicka, “The Impact of Taxes on the Extensive and Intensive Margins of FDI,” International Tax and Public Finance 28 (April 2021): 434–464, https://link.springer.com/article/10.1007/s10797-020-09640-3.

[23] Elke Asen, “What We Know: Reviewing the Academic Literature on Profit Shifting,” Tax Foundation, June 22, 2021, https://www.taxfoundation.org/international-tax-avoidance/.

[24] Daniel Bunn, “U.S. Tax Incentives Could be Caught in the Global Minimum Tax Crossfire,” Tax Foundation, Jan. 28, 2022, https://www.taxfoundation.org/us-global-minimum-tax-build-back-better/.

[25] Cody Kallen, “Expense Allocation: A Hidden Tax on Domestic Activities and Foreign Profits,” Tax Foundation, Aug. 26, 2021, https://www.taxfoundation.org/expense-allocation-rules-hidden-tax-foreign-profits/.

[26] Erica York, “Proposed Top Combined Marginal Capital Gains TaxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. Rate Would Be Third-Highest in OECD,” Tax Foundation,” Oct. 29, 2021, https://www.taxfoundation.org/reconciliation-bill-capital-gains-tax.

[27] Taylor LaJoie and Elke Asen, “Double Taxation of Corporate Income in the United States and the OECD,” Tax Foundation, Jan. 13, 2021, https://www.taxfoundation.org/double-taxation-of-corporate-income/.

[28] Alex Durante, “Higher Taxes Under House Ways and Means Plan Emphasize Need for Corporate Integration,” Tax Foundation, Oct. 13, 2021, https://www.taxfoundation.org/corporate-integration-tax-reform/.

[29] Elke Asen, “Integrated Tax Rates on Corporate Income in Europe,” Tax Foundation, Jan. 14, 2021, https://www.taxfoundation.org/integrated-tax-rates-on-corporate-income-in-europe/.

[30] OECD Tax Database, Table II.4. “Overall Statutory Tax Rates on Dividend Income,” https://stats.oecd.org/index.aspx?DataSetCode=Table_II1.

[31] Ibid.

[32] Office of Tax Analysis, “Tax Expenditures,” U.S. Department of the Treasury, December 2021, https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures.

[33] Tax Foundation, Options for Reforming America’s Tax Code 2.0, Apr. 19, 2021, https://www.taxfoundation.org/publications/options-for-reforming-americas-tax-code/?option=67.

[34] Everett Stamm and Taylor LaJoie, “Overview of the Low-Income Housing Tax Credit,” Tax Foundation, Aug. 11, 2020, https://www.taxfoundation.org/low-income-housing-tax-credit-lihtc/.

[35] Alex Muresianu, “1980s Tax Reform, Cost Recovery, and the Real Estate Industry: Lessons for Today,” Tax Foundation, July 23, 2020, https://www.taxfoundation.org/1980s-tax-reform-cost-recovery-and-the-real-estate-industry-lessons-for-today/; see also Thomas Davidoff, “Tax Reform and Sprawl,” Joint Center for Housing Studies at Harvard University, September 2013, https://www.jchs.harvard.edu/sites/default/files/hbtl-05.pdf.

[36] Alex Muresianu, “How Expensing for Capital Investment Can Accelerate the Transition to a Cleaner Economy,” Tax Foundation, Jan. 12, 2021, https://www.taxfoundation.org/energy-efficiency-climate-change-tax-policy/.

[37] Alex Muresianu, “Carbon TaxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them.: Weighing the Options for Financing Reconciliation,” Tax Foundation, Sept. 29, 2021, https://www.taxfoundation.org/carbon-tax-reconciliation/.

[38] Council of Economic Advisers, “Chapter 4: The Benefits of Open Trade and Investment Policies,” Economic Report of the President (Washington, D.C.: U.S. Government Printing Office, January 2009), https://georgewbush-whitehouse.archives.gov/cea/ERP_2009_Ch4.pdf.

[39] James K. Glassman, “The Blessings of Free Trade,” Cato Institute, May 1, 1998, https://www.cato.org/publications/trade-briefing-paper/blessings-free-trade.

[40] U.S. Customs and Border Patrol, “Trade Statistics,” https://www.cbp.gov/newsroom/stats/trade.

[41] Aaron Flaaen and Justin Pierce, “Disentangling the Effects of the 2018-2019 Tariffs on a Globally Connected U.S. Manufacturing Sector,” Federal Reserve Board, 2019, https://www.federalreserve.gov/econres/feds/files/2019086pap.pdf.

[42] Alex Durante and Alex Muresianu, “Who Really Pays the Tariffs? U.S. Firms and Consumers, Through Higher Prices,” Tax Foundation, Dec. 15, 2021, https://www.taxfoundation.org/who-really-pays-tariffs/.

[43] Chad P. Bown, “Anatomy of a flop: Why Trump’s US-China phase one trade deal fell short,” Peterson Institute for International Economics, Feb. 8, 2021, https://www.piie.com/blogs/trade-and-investment-policy-watch/anatomy-flop-why-trumps-us-china-phase-one-trade-deal-fell.

[44] See Zack Budryk, “Biden extends solar panel tariffs with modifications,” The Hill, Feb. 4, 2022, https://thehill.com/policy/energy-environment/592829-biden-extends-solar-panel-tariffs-with-modifications?rl=1; and Jenny Leonard, Eric Martin, and Isabel Reynolds, “U.S., Japan Set to Announce Pact to End Trump Steel Tariffs,” Bloomberg, Feb. 7, 2022, https://www.bloomberg.com/news/articles/2022-02-07/u-s-japan-set-to-announce-pact-to-end-trump-era-steel-tariffs?utm_source=google&utm_medium=bd&cmpId=google.

[45] Tara O’Neill Hayes, “Child Poverty and the Effects of Anti-Poverty Programs,” American Action Forum, June 17, 2021, https://www.americanactionforum.org/research/child-poverty-and-the-effects-of-anti-poverty-programs/.

[46] Diane Whitemore Schanzenbach and Michael R. Strain, “Employment Effects of the Earned Income Tax Credit: Taking the Long View,” National Bureau of Economic Research, November 2020, https://www.aei.org/wp-content/uploads/2020/11/w28041.pdf?x91208.

[47] Tara O’Neill Hayes, “Child Poverty and the Effects of Anti-Poverty Programs.”

[48] The Joint Committee on Taxation, “Estimates Of Federal Tax Expenditures For Fiscal Years 2020-2024,” Nov. 5, 2020, https://www.jct.gov/publications/2020/jcx-23-20/.

[49] Erica York, “2022 Tax Brackets,” Tax Foundation, Nov. 10, 2021, https://www.taxfoundation.org/2022-tax-brackets/.

[50] Note the current CTC levels were set in conjunction with changes to other family-related tax provisions, including the personal and dependent exemptions and standard deduction, all modified by the 2017 Tax Cuts and Jobs Act.

[51] The Joint Committee on Taxation, “Estimated Revenue Effects Of H.R. 1319, The ‘American Rescue Plan Act Of 2021,’” Mar. 9, 2021, https://www.jct.gov/publications/2021/jcx-14-21/.

[52] Amir El-Sibaie, “Illustrating the Earned Income Tax Credit’s Complexity,” Tax Foundation, July 14, 2016, https://www.taxfoundation.org/illustrating-earned-income-tax-credit-s-complexity/.

[53] Congressional Research Service, “The Earned Income Tax Credit (EITC): Administrative and Compliance Challenges,” Apr. 23, 2018, https://crsreports.congress.gov/product/pdf/R/R43873.

[54] Congressional Research Service, “Child Tax Benefits and Children with Complex or Dynamic Living Arrangements,” Mar. 12, 2021, https://crsreports.congress.gov/product/pdf/IN/IN11634.

[55] See Taxpayer Advocate Service, “2008 Annual Report to Congress, Volume One,” Dec. 31, 2008, 367, https://www.irs.gov/pub/tas/08_tas_arc_legrec.pdf.

[56] Tax Foundation, Options for Reforming America’s Tax Code 2.0.

[57] See Tara O’Neill Hayes, “Child Poverty and The Effects of Anti-Poverty Programs.”

[58] The Family Security Act, https://www.romney.senate.gov/wp-content/uploads/2021/02/family-security-act_one-pager.pdf.

[59] Erica York and Garrett Watson, “Sen. Romney’s Child Tax Reform Proposal Aims to Expand the Social Safety Net and Simplify Tax Credits,” Tax Foundation, Feb. 5, 2021, https://www.taxfoundation.org/child-allowance-romney-tax-proposal/.

[60] Taylor LaJoie, “When Marriage Doesn’t Pay: Analysis and Options for Addressing Marriage and Second-Earner Penalties,” Tax Foundation, June 23, 2020, https://www.taxfoundation.org/marriage-penalty-marriage-tax-penalty/.

[61] See Jane G. Gravelle, “Federal Income Tax Treatment of the Family Under the 2017 Tax Revisions,” Congressional Research Service, Jan. 24, 2020, https://www.everycrsreport.com/files/20200124_R46193_885e7ee54e8118ed77c158b7b09992b4ce929d0f.pdf: “The 2017 tax revision effectively eliminated personal exemptions claimed for the taxpayer, their spouse (if married), and any dependent (often referred to as the dependent exemption). However, the increased standard deduction more than offset these losses for taxpayers (and their spouses, if married).”

[62] Robert Bellafiore, “The Case for Universal Savings Accounts,” Tax Foundation, Feb. 26, 2019, https://www.taxfoundation.org/case-for-universal-savings-accounts/.

[63] Erica York, “What are Universal Savings Accounts and Why Are They Important?,” Tax Foundation, Sept. 11, 2018, https://www.taxfoundation.org/universal-savings-accounts-important/.

[64] Alan Cole, “Losing the Future: The Decline of U.S. Saving and Investment,” Oct. 1, 2014, https://www.taxfoundation.org/losing-future-decline-us-saving-and-investment.

[65] Robert Bellafiore, “The Case for Universal Savings Accounts.” https://taxfoundation.org/case-for-universal-savings-accounts/

[66] Ibid.

[67] Tax Foundation, “General Equilibrium Model,” February 2022.

[68] Tax Foundation, Options for Reforming America’s Tax Code 2.0.

[69] Ibid.

[70] Office of Management and Budget, ”Tax Expenditures” in Analytical Perspectives-Budget of the U.S. Government, FY 2022, https://www.whitehouse.gov/wp-content/uploads/2021/05/ap_10_expenditures_fy22.pdf.

[71] Office of Tax Analysis, “Tax Expenditures,” December 2021, U.S. Department of the Treasury, https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures.

[72] Scott Greenberg, “Clean Energy Credits Mostly Benefit the Wealthy, New Study Shows,” Tax Foundation, Aug. 21, 2015, https://www.taxfoundation.org/clean-energy-credits-mostly-benefit-wealthy-new-study-shows/.

[73] Tax Foundation, Options for Reforming America’s Tax Code 2.0.

[74] Ibid.

[75] Sidney Kess, “Deep Dive on the Tax Cuts and Jobs Act: Changes for Securities Investors,” The CPA Journal, October 2018, https://www.cpajournal.com/2018/10/19/deep-dive-on-the-tax-cuts-and-jobs-act-2/.

Share this article