Note: The following is the testimony of Dr. William McBride, Tax Foundation Vice President of Federal Tax and Economic Policy, prepared for a Joint Economic Committee hearing on October 6, 2021, titled, “Building Back Better: Raising Revenue to Invest in Shared Prosperity.”

Chairman Beyer, Ranking Member Lee, and members of the Joint Economic Committee, thank you for inviting me to testify today.

I am Dr. William McBride, Vice President of Federal Tax and Economic Policy at the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation, and today I will share the key findings of our analysis of the most recent iteration of the President’s Build Back Better Agenda.

There are three primary takeaways from our analysis. The first is that the corporate tax is not just paid by corporate shareholders: raising the corporate tax rate will reduce investment and productivity growth, ultimately leading to lower wages across the board.

The second is that further increasing the progressivity of the tax code by raising individual income taxes for high-income earners comes with a cost: it will reduce incentives to work, save, and invest, broadly reducing employment opportunities throughout the economy.

And lastly, the tax code is not an effective tool for social policy: optimal tax policy raises the amount of revenue needed while creating minimal economic costs, and other goals are better addressed through proper spending programs.

Table of Contents

- Raising Corporate Income Taxes Will Reduce Investment in America

- — Overall Impact of the Ways and Means Package

- — Impact of Selected Corporate Provisions from the Ways and Means Package

- — Impact of International Policies

- Increasing the Progressivity of the Tax Code Comes with a Cost

- — Impact on Pass-through Business Income

- — Impact of Selected Individual Income Tax Provisions from the Ways and Means Package

- — Current Progressivity of the U.S. Tax Code

- Adding More Complexity to the Tax Code Is Problematic

- Conclusion

Point 1: Raising Corporate Income Taxes Will Reduce Investment in America

Raising corporate income taxes has a large negative impact on the U.S. economy, because it reduces the after-tax return on corporate investment, reducing incentives to invest. As investment shrinks, worker productivity declines along with wages and hiring.

Our modeling of the Ways and Means CommitteeThe Committee on Ways and Means, more commonly referred to as the House Ways and Means Committee, is the chief tax-writing committee in the US. The House Ways and Means Committee has jurisdiction over all bills relating to taxes and other revenue generation, as well as spending programs like Social Security, Medicare, and unemployment insurance, among others.’s latest Build Back Better proposal found that the plan would reduce the size of the economy by about 1 percent in the long run, shrink the capital stock by 1.8 percent, cut wages by 0.7 percent, and cost more than 300,000 jobs.[1] While the proposal would increase tax revenue by about $1.06 trillion over 10 years, conventionally estimated, in the long run it would reduce GDP by more than $2 for every $1 raised.[2]

The revenue and economic impacts are largely driven by the plan’s increase of the corporate tax rate to 26.5 percent, which would reduce long-run GDP by 0.6 percent, the capital stock by 1.1 percent, wages by 0.5 percent, and cost over 100,000 jobs.

| Long-Run Gross Domestic Product | -0.98% |

| Long-Run Gross National Product | -1.01% |

| Capital Stock | -1.84% |

| Wage Rate | -0.68% |

| Full-Time Equivalent Jobs | -303,000 |

| Conventional Revenue (10-Year) | $1.06 trillion |

| Dynamic Revenue (10-Year) | $804 billion |

|

Source: Tax Foundation General Equilibrium Model, September 2021. |

|

| Raise the Corporate Tax Rate to 26.5 Percent | International Provisions (combined) | |

|---|---|---|

| Long-Run Gross Domestic Product | -0.6% | -0.1% |

| Long-Run Gross National Product | -0.5% | -0.1% |

| Capital Stock | -1.1% | -0.2% |

| Wage Rate | -0.5% | -0.1% |

| Full-Time Equivalent Jobs | -107,000 | -12,000 |

| Conventional Revenue (10-Year) | $704 billion | $136 billion |

|

Source: Tax Foundation General Equilibrium Model, September 2021. |

||

The international tax increases on U.S. multinationals (MNEs), including higher taxes on Global Intangible Low-taxed Income (GILTI) and a new limit on interest expense, further reduce the size of the economy by about 0.1 percent, the capital stock by 0.2 percent, wages by 0.1 percent, and jobs by 12,000. Higher GILTI taxes reduce the incentive of U.S. MNEs to invest in research and development (R&D) in the U.S. due to reduced after-tax income from intellectual property (IP) that has been located abroad. There is an additional effect of higher international taxes that we have not modeled (due to a lack of data): the reduction in American incomes arising from the incentive of U.S. MNEs to avoid the international tax increases by selling foreign assets to foreign competitors.

The international tax increases are intended to reduce profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens., i.e., the ability of U.S. MNEs to shift profits abroad where taxes are lower. However, we find that profit shifting would be made worse by the bill, as it would increase taxes on domestic income more than it would on foreign income. Specifically, the bill raises the statutory corporate tax rate 5.5 percentage points and raises the tax rate on Foreign Derived Intangible Income (FDII), while raising the effective tax rate on foreign income by between 2.4 and 5.1 percentage points over the budget window. On net, we estimate increased profit shifting by U.S. MNEs reduces revenue by $57.9 billion over a decade.[3]

These estimates do not include the benefits of infrastructure, since that is not included in the House reconciliation bill. However, in our modeling of the American Jobs Plan, which included about $1.7 trillion in infrastructure spending as well as a higher corporate tax rate of 28 percent among other tax increases, we found that plan would on net reduce GDP by 0.5 percent and cost more than 100,000 jobs.[4]

The negative impact of corporate taxes on economic growth is well-documented.[5] An OECD study examining data from 63 countries concluded that corporate income taxes are the most economically damaging way to raise revenue, followed by individual income taxes, consumption taxes, and property taxes.[6] A study on taxes in the United Kingdom found that taxes on consumption are less economically damaging than taxes on corporate and individual income.[7] A study of U.S. tax changes since World War II found that a 1 percentage point cut in the average corporate tax rate raises real GDP per capita by 0.6 percent after one year, a somewhat larger impact than a similarly sized cut in individual income taxes.[8] Based on U.S. state taxes, a study found that a 1 percentage point cut in the corporate tax rate leads to a 0.2 percent increase in employment and a 0.3 percent increase in wages.[9]

Furthermore, several studies demonstrate that the corporate tax is borne in part by workers.[10] For instance, a study of corporate taxes in Germany found that workers bear about half of the tax burden in the form of lower wages, with low-skilled, young, and female employees disproportionately harmed.[11]

The corporate tax is also borne by owners of shares, including retirees earning considerably less than $400,000. In the short run, the Joint Committee on Taxation (JCT) assumes owners of capital bear all of the corporate tax, yet that includes more than 90 million tax filers earning less than $200,000. In the long run, JCT assumes workers bear a portion of the corporate tax, such that the burden falls on more than 150 million tax filers earning less than $200,000.[12]

In its distributional analysis of the House bill, including the corporate taxes, the JCT finds that 34.8 percent of filers earning between $100,000 and $200,000 will see a tax hike of more than $100 in 2023, and by 2027 that figure grows to 85.8 percent.[13]

Another downside to raising corporate taxes is it would reduce the competitiveness of U.S. companies. In a global economy in which firms based in countries all over the world compete to reach customers globally, corporate taxes are an important factor. As it stands, the U.S. corporate tax rate is competitive, but the GILTI tax is not, as it is a unique tax burden that only applies to U.S. firms over and above corporate tax paid to foreign governments on earnings abroad.

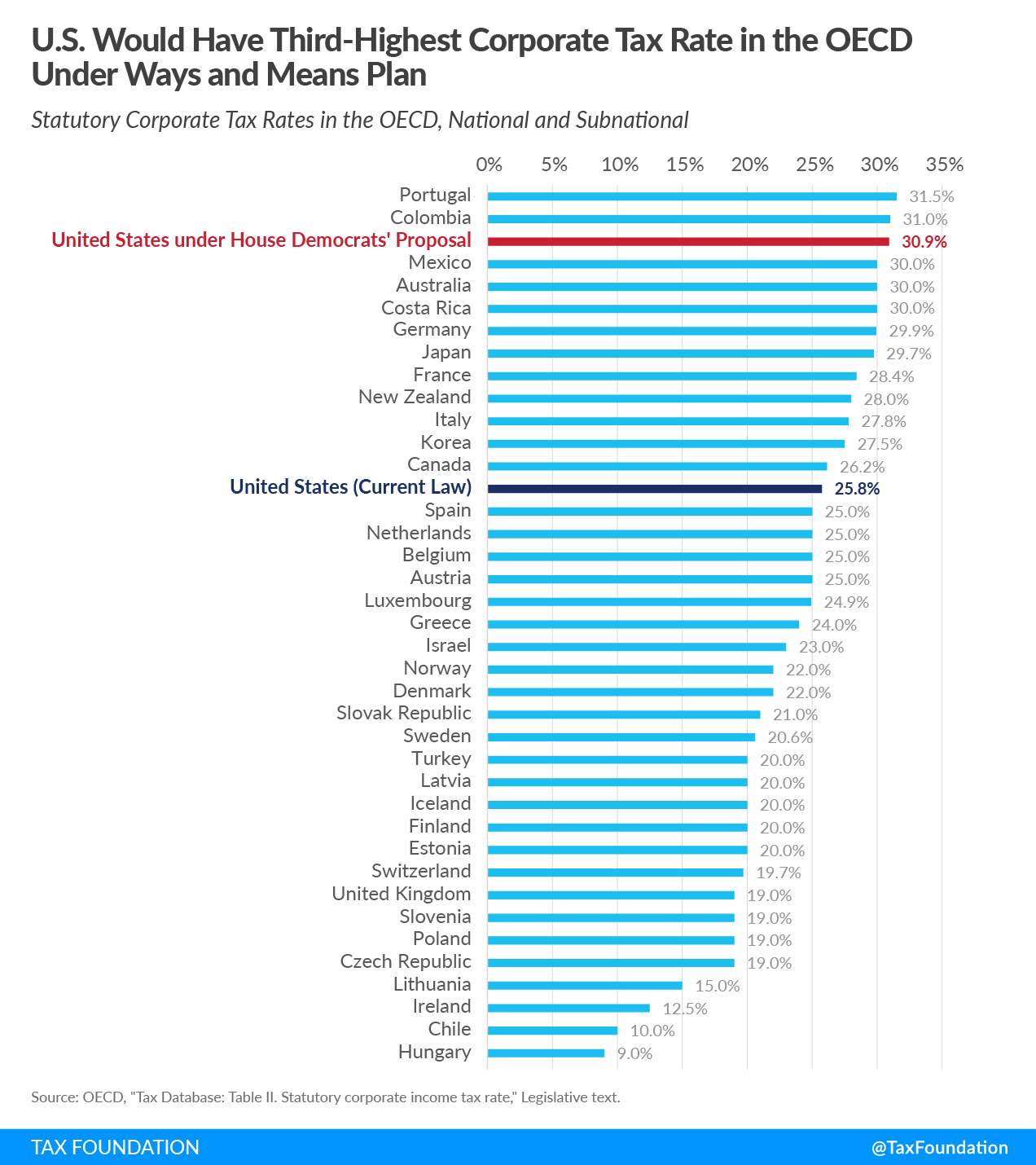

Regarding the corporate tax rate, at 25.8 percent inclusive of the average state corporate tax rate, the U.S. ranks slightly above the OECD average of 22.7 percent. The House bill would raise the federal corporate rate from 21 percent to 26.5 percent, which results in a combined federal-state corporate tax rate of 30.9 percent—the third highest corporate tax rate in the OECD, behind only Colombia and Portugal.[14] A similar result holds when accounting for various deductions and other tax preferences, i.e., U.S. effective corporate tax rates would rise to among the highest in the OECD under the House plan.[15]

Regarding the U.S. international tax system, we estimate that GILTI and other features of the current international tax system, including expense allocation, add about 5 or 6 percentage points of U.S. residual tax to the foreign earnings of U.S. MNEs, i.e., on top of foreign taxes. The international tax changes proposed in the House bill would increase the U.S. residual tax to about 10 percentage points or more, an increase of more than 70 percent in 2022.[16] That sort of tax increase on an already high U.S. residual tax could invite U.S. MNEs to engage in a variety of maneuvers to avoid it, including tax inversions and other mergers and acquisitions, along the lines of what we observed prior to the Tax Cuts and Jobs Act (TCJA), in which several major U.S. companies moved their headquarters abroad to low-tax countries.[17]

Point 2: Increasing the Progressivity of the Tax Code Comes with a Cost

On its own, the appeal of living in a society where incomes are more evenly distributed is understandable, and potentially desirable to many Americans. However, doing so by raising taxes on high earners, as the House bill proposes, comes with serious economic costs. Namely, it reduces incentives to work, save, and invest, negatively impacting the broader economy, particularly entrepreneurs who are starting and growing the next generation of businesses, including pass-through businesses such as partnerships and S corporations.

The pass-through sector is large, representing more than half of U.S. private sector employment.[18] These firms “pass through” earnings to owners who report them on individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source returns. The House bill levies several tax increases on pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. income, including:

- Raising the top marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. on ordinary income to 39.6 percent,

- Adding a 3 percent surcharge on modified adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods over $5 million,

- Capping the Section 199A pass-through business deduction at $500,000 for joint filers,

- Applying the 3.8 percent net investment income tax (NIIT) to active pass-through business income in excess of $500,000 for joint filers, and

- Limiting losses for pass-through businesses.

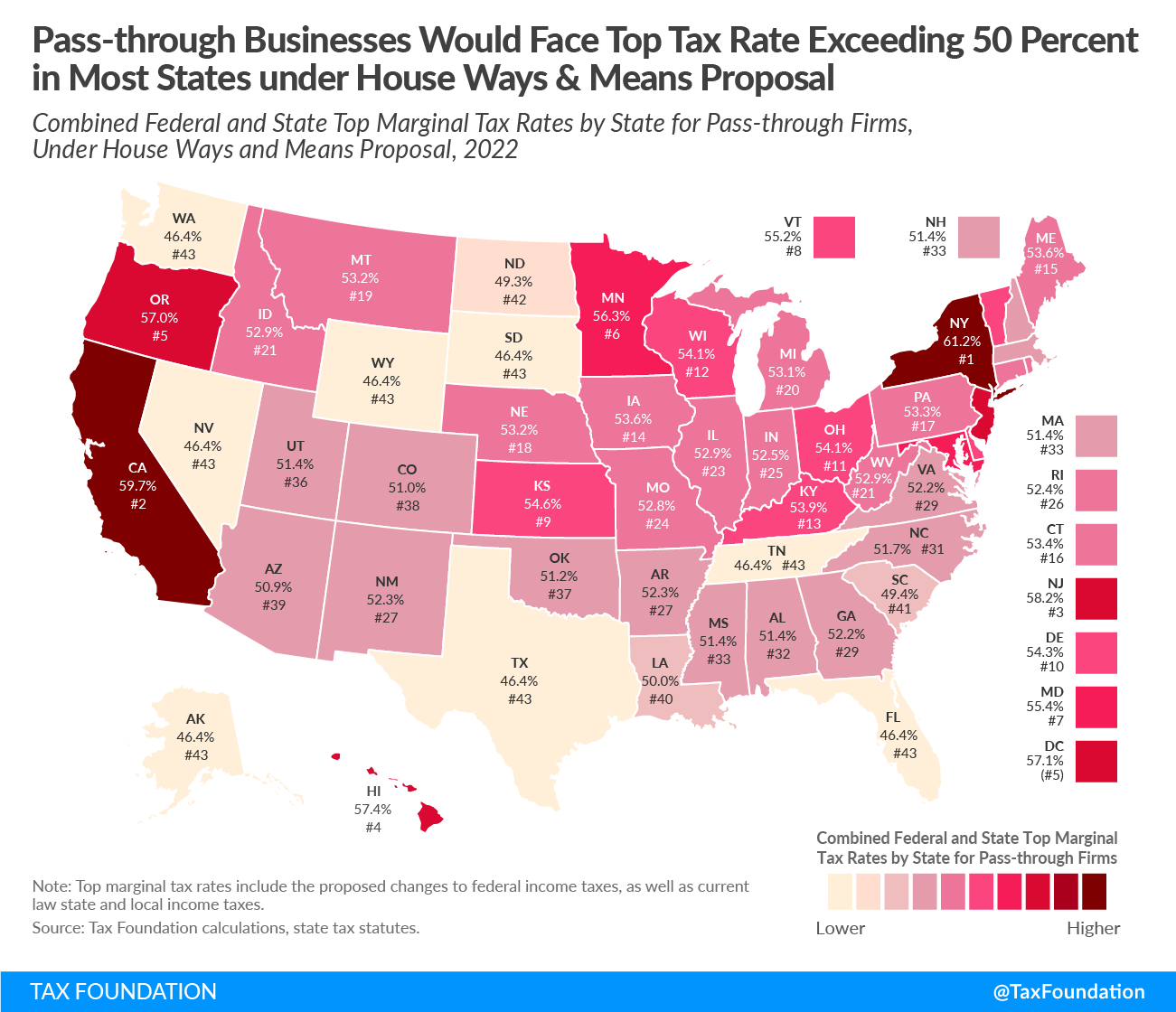

As a result of these tax increases, the top federal tax rate on pass-through business income, as well as ordinary income, would reach 46.4 percent—the highest since 1986. Including state-level income taxes, the combined top marginal tax rate would exceed 50 percent in 41 states.[19]

It may be claimed that the proposed tax increases only impact a small percent of firms, but economically it is more important to consider the share of business income that is affected. Our estimates indicate that more than half of pass-through business income would face a tax increase under these proposals.[20]

Our modeling of the House bill indicates the individual income tax increases would reduce the size of the economy by about 0.3 percent in the long run, shrink the capital stock by 0.6 percent, cut wages by 0.1 percent, and cost more than 140,000 jobs.[21] Most of the economic impact results from the five major tax increases on pass-through businesses listed above.

| Increase Income Tax Rate to 39.6 Percent and Apply to More Income | Apply a 3 Percent Surcharge to Modified Adjusted Gross Income | Other Pass-through Business Provisions (Combined) | |

|---|---|---|---|

| Long-Run Gross Domestic Product | -0.1% | Less than -0.05% | -0.1% |

| Long-Run Gross National Product | -0.1% | Less than -0.05% | -0.1% |

| Capital Stock | -0.1% | Less than -0.05% | -0.4% |

| Wage Rate | Less than -0.05% | Less than -0.05% | -0.1% |

| Full-Time Equivalent Jobs | -64,000 | -32,000 | -24,000 |

| Conventional Revenue (10-Year) | $157 billion | $131 billion | $396 billion |

|

Source: Tax Foundation General Equilibrium Model, September 2021. |

|||

The bill also raises the top long-term federal capital gains and qualified dividends tax rate 8 percentage points to 31.8 percent inclusive of the 3.8 percent NIIT and 3 percent surcharge. This would be the highest federal tax rate on capital gains since the 1970s. When considering state-level policies, the average top marginal combined tax rate on capital gains and qualified dividends would be about 37 percent.[22]

Because the capital gains and qualified dividends tax increases reduce the after-tax return to saving for U.S. residents, U.S. saving would fall, and to some extent be replaced by foreign saving. As a result, we find that the share of U.S. investment financed by foreign savers would increase, with the returns to that investment accruing to foreigners rather than Americans, causing U.S. incomes, as measured by GNP, to decline about 0.1 percent in the long run.[23]

There are several studies pointing to the economic costs of raising individual income taxes, particularly on high earners.[24] A study based on postwar tax reforms in the United States found that reducing marginal tax rates for the top 1 percent of earners leads to increases in real GDP and declines in unemployment, with a 1 percentage point cut in the tax rate increasing real GDP by 0.78 percent by the third year after the tax change.[25]

In looking at the experience of developed countries over the period 1971 to 2004, OECD researchers concluded that “a reduction in the top marginal [individual] tax rate is found to raise productivity in industries with potentially high rates of enterprise creation. Thus, reducing top marginal tax rates may help to enhance economy-wide productivity in OECD countries with a large share of such industries. …”[26]

The Congressional Budget Office (CBO) recently modeled three types of tax increases to fund a permanent increase in government spending of 10 percent of GDP annually: a flat labor tax, a flat income tax, and a progressive income tax. The CBO found that a progressive income tax is the most economically damaging, reducing GDP by 10 percent after 10 years, and reducing lifetime consumption and hours worked especially for younger households.[27]

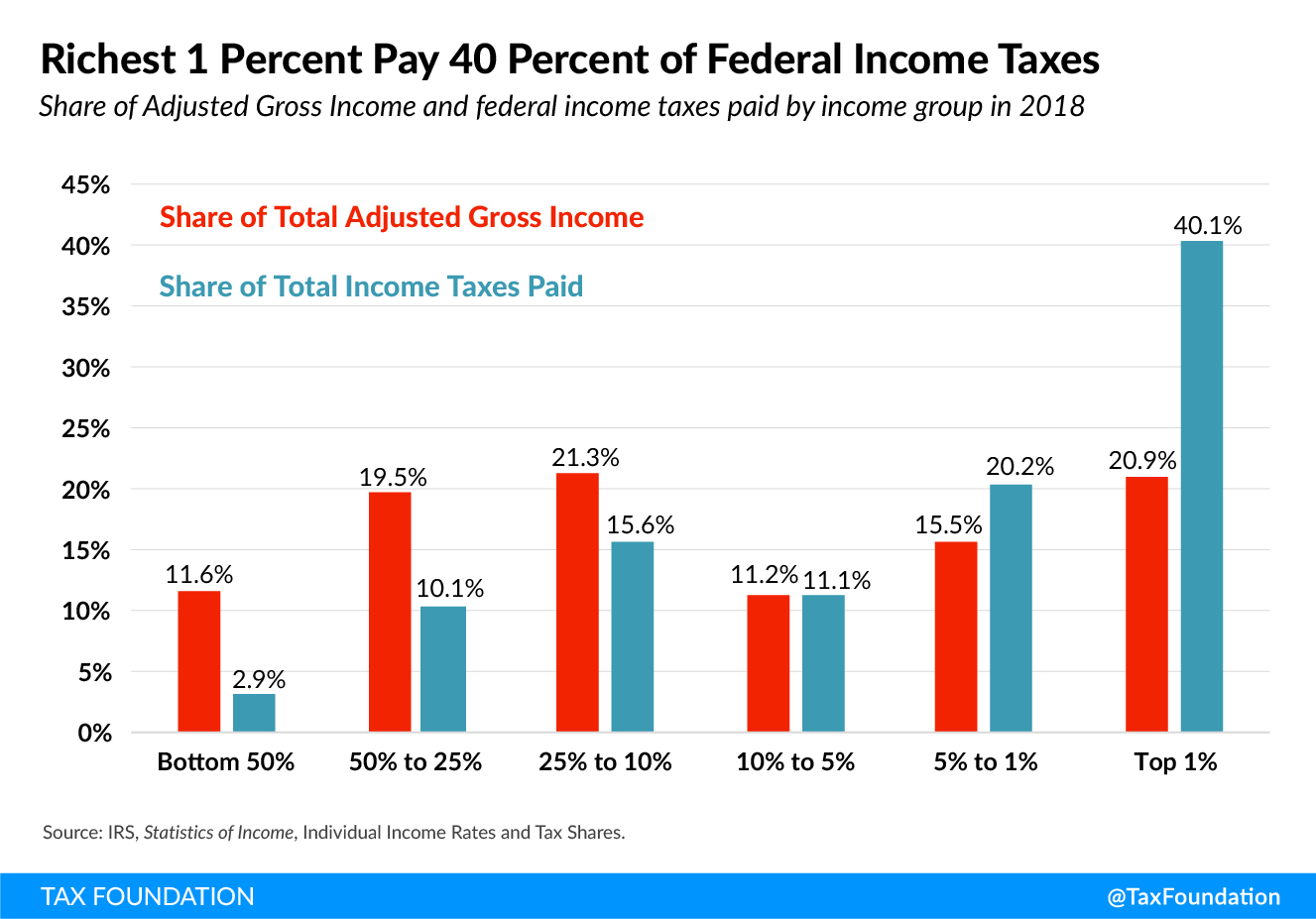

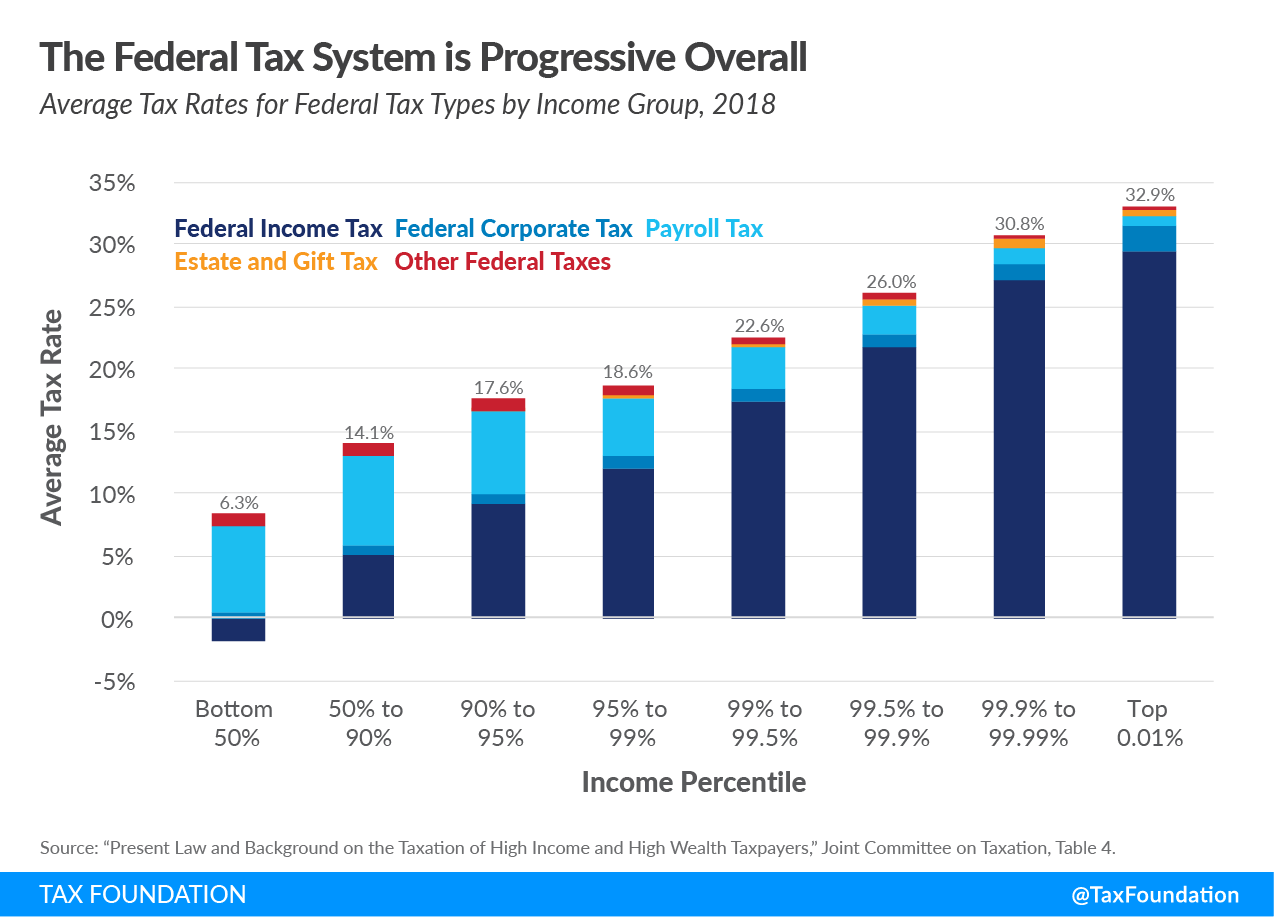

Finally, it should be noted that the goal of increasing the progressivity of the tax code has been accomplished several times over, generally as part of every major tax reform of the last 40 years. As a result, according to the latest IRS data for 2018, the top 1 percent of income earners paid 40.1 percent of federal individual income taxes—the highest share since 1980—while earning 20.9 percent of income.[28] Accounting for all federal taxes, data from the CBO and Treasury Department confirm that the tax code is progressive overall. For instance, Treasury finds that the highest earners pay the highest average effective tax rates when considering all federal taxes—the top 0.01 percent will pay an average federal ETR of 32.9 percent under current law in 2022.[29]

Point 3: Adding More Complexity to the Tax Code Is Problematic

Another economic downside of the plan is additional complexity and uncertainty. It adds 22 new tax credits and expands several existing ones, at a budgetary cost of more than $1 trillion over the next 10 years. This approach has several problems, in addition to the budgetary cost. First, while recognizing that tax cuts are effective incentives, this approach picks winners and losers through the political process rather than letting the market process determine the most valuable use of resources. Do we really think lawmakers have taken the time to do any sort of cost-benefit analysis on these proposals, and will they find time to effectively monitor and respond to the changing costs and benefits over time?

Second, the approach adds complexity and compliance costs for taxpayers and administrative burdens for the IRS. Third, many of the policies are temporary, which creates uncertainty for taxpayers. Fourth, the bewildering array of tax credits and other tax preferences contributes to a dysfunctional federal budgeting process that generates chronic deficits.

By far the largest tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. in the plan is the extension and modification of the Child Tax Credit (CTC), which as part of the American Rescue Plan Act (ARPA) was expanded temporarily for 2021 to include full refundability, an advanced monthly payment, and a maximum annual benefit of $3,600 per child.[30] The plan would extend the ARPA CTC through 2025 and permanently extend full refundability (allowing the maximum benefit regardless of income), which would have a budgetary cost of more than $100 billion per year through 2025, more than double the cost of the current law CTC. That is, more than $200 billion per year will be spent on the CTC, which is about 10 percent of all individual income tax revenue or more than half of all corporate tax revenue forecast under current law.

Because of this huge budgetary cost, both the expanded CTC and the current law CTC are temporary, and yet likely to be extended beyond their planned expiration in 2025, thus obscuring the full budgetary cost over the 10-year budget window. We estimate that extending the ARPA CTC permanently would cost about $1.6 trillion over the budget window, far exceeding all of the individual income tax pay-fors specified in the House bill.[31]

The refundable aspect of the CTC makes the budgeting and oversight process all the more arcane and difficult to track for voters, taxpayers, lawmakers, and the IRS. The expanded CTC is being sold as a tax cut, but it is in fact largely an outlay effect, i.e., spending, due to refundability.[32] The history of refundability with the CTC goes back to its introduction in 2001 when the maximum benefit was $1,000 per child, and it has expanded under every administration since. During that time, the refundable CTC has been plagued with improper payments, e.g., the Treasury Department found that nearly one-third of refundable CTC payments in tax years 2009 through 2011 were made in error.[33] Over its entire history the refundable CTC has contributed to a worsening budgetary outcome of chronic and escalating deficits.[34]

In addition to its budgetary impacts, the complicated design and implementation of the CTC, as well as its temporary nature, creates confusion for taxpayers, especially low-income earners. For example, a recent survey found that while most parents (88 percent) are aware of the expanded CTC, households with incomes below $25,000 are least likely to have heard about the credit.[35]

One thing they probably have not heard about is that the new monthly CTC contains a new definition of a child. Whereas the current CTC determines eligibility based on where the child lives for more than six months of the year, eligibility for the new monthly CTC is based on a five-factor “care” test specific to each month, including “involvement by the taxpayer in, and financial and other support by the taxpayer for, education or similar activities of the individual.” For families with multiple caregivers, e.g., split custody arrangements where the child spends part of the month with one or another parent, a grandparent, aunt, etc., this is a recipe for confusion, conflict, and administrative uncertainty.[36]

There is another question about how the expanded CTC impacts work incentives. Economists have long understood the concept of an “income effect” in which the incentive to work is diminished because of having more income, including government benefits. A recent literature review indicates that a 10 percent increase in income from government benefits reduces hours worked by 1.5 to 1.6 percent.[37] Partly out of these concerns, as well as concerns about budgetary costs, the CTC has historically been designed to phase in with income, effectively reducing marginal tax rates and increasing incentives to work for low-income households. The expanded CTC in the House bill eliminates the phase-in by making the CTC fully refundable, thus leaving only the work disincentive of the income effect for low-income households. In addition, the CTC phases out for higher income households, effectively raising marginal tax rates and reducing incentives to work for those households.[38]

Extending the CTC would provide relief for families, but it could be delivered in a less complex way that ideally would minimize work disincentives. Tax policy should be focused on how to raise revenue in the least economically harmful manner, and other goals should be handled as public spending subject to the appropriations process.[39] Transforming the CTC into a spending program, delivered through, for instance, the Social Security Administration, would make the tax code more focused on its primary purpose, and make the budget process more transparent. This idea has supporters from both sides of the aisle.

The bill would also spend more than $20 billion per year on expansions of the Child and Dependent Care Tax Credit (CDCTC), Earned Income Tax Credit (EITC), and Premium Tax Credit, which come with their own compliance and administrative challenges. For example, the Treasury Department has routinely found that a large share of refundable EITC payments is made in error—25 percent in tax year 2018 according to a recent report.[40]

In addition, the bill provides or expands numerous smaller tax credits for specific economic activities, whether for certain types of clean energy investment, housing construction, or broadband development, among others. These credits have a mixed track record at addressing their core concerns. For instance, the Low-Income Housing Tax Credit has become increasingly ineffective as a means to stimulate affordable housing.[41] Clean energy tax credits have been found to primarily benefit the wealthy.[42]

Instead of these targeted incentives, lawmakers could address underlying biases against investment more generally, stimulating new projects in these specific areas in the process. As an example, by not allowing companies to fully deduct investments in structures, the tax code discourages new, more energy-efficient construction.[43] Expensing for all capital investment would be a powerful pro-growth policy, while simplifying the tax code and helping solve many of these specific issues.[44]

Indeed, the best provision in the bill is postponing the amortization of R&D expenses.[45] Continuing to allow companies to fully deduct the cost of R&D is important for a wide range of crucial industries and issues, from pharmaceutical development to heavy manufacturing to green energy. However, the bill would not make full deductibility of R&D permanent, instead allowing it to expire after 2025 as opposed to after this year. Ideally, expensing of R&D would be permanent, providing companies with stable, long-term incentives to invest.[46]

Conclusion

There are a couple of broad takeaways from this. When you tax something, you get less of it. This is why governments tax tobacco (and the House bill increases those taxes), because it reduces tobacco use. That, and it generates tax revenue. The costs of the higher taxes should be weighed against the benefits, e.g., more tax revenue, improved public health, etc. Likewise, taxing income will reduce the generation of income. That means a smaller economy, less prosperity, and less opportunity. The economic costs can exceed the benefits in terms of tax revenue, and that is what we find with the House bill.

The other takeaway is that the IRS can only do so much, and taxpayers are getting confused. The tax code is already excessively complex and the IRS is overwhelmed in its ability to administer and enforce the tax laws. There is a limit beyond which adding more complex provisions to the tax code no longer benefits taxpayers, the government, or the country as a whole. Rather than pushing the limit, we should seriously consider simplification.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] William McBride et. al., “Build Back Better Act: Details & Analysis of the $3.5 Trillion Budget Reconciliation Bill,” Sept. 16, 2021, https://www.taxfoundation.org/build-back-better-plan-reconciliation-bill-tax/.

[2] Garrett Watson, “Economy Loses More than Revenue Gains in Ways and Means Build Back Better Act,” Tax Foundation, Sept. 22, 2021, https://www.taxfoundation.org/house-tax-plan-impact/.

[3] Cody Kallen, “How Heavily Taxed Are U.S. Multinationals?” Tax Foundation, Sept. 29, 2021, https://www.taxfoundation.org/us-multinational-corporations-tax/.

[4] Alex Durante, Cody Kallen, Huaqun Li, and William McBride, “Details and Analysis of President Biden’s American Jobs Plan,” June 4, 2021, https://www.taxfoundation.org/american-jobs-plan/.

[5] William McBride, “What is the Evidence on Taxes and Growth,” Tax Foundation, Dec. 18, 2012, https://www.taxfoundation.org/what-evidence-taxes-and-growth/; see also Alex Durante, “Reviewing Recent Evidence of the Effect of Taxes on Economic Growth,” Tax Foundation, May 21, 2021, https://taxfoundation.org/reviewing-recent-evidence-effect-taxes-economic-growth/.

[6] Åsa Johansson, Christopher Heady, Jens Matthias Arnold, Bert Brys, and Laura Vartia, “Taxation and Economic Growth,” Organisation for Economic Co-Operation and Development Working Paper No. 620, July 3, 2008, https://www.oecd-ilibrary.org/economics/taxation-and-economic-growth_241216205486.

[7] Ahn D. M. Nguyen, Luisanna Onnis, and Raffaelle Rossi, “The Macroeconomic Effects of Income and Consumption TaxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or income taxes where all savings are tax-deductible. Changes,” American Economic Journal: Economic Policy 13:2 (May 2021), https://www.aeaweb.org/articles?id=10.1257/pol.20170241&&from=f.

[8] Karel Mertens and Morten O. Ravn, “The Dynamic Effects of Personal and Corporate Income TaxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. Changes in the Unites States,” American Economic Review 103:4 (June 2013), https://www.aeaweb.org/articles?id=10.1257/aer.103.4.1212.

[9] Alexander Ljungqvist and Michael Smolyansky, “To Cut or Not to Cut? On the Impact of Corporate Taxes on Employment and Income,” National Bureau of Economic Research Working Paper No. 20753 (October 2018), https://www.nber.org/system/files/working_papers/w20753/w20753.pdf.

[10] Stephen J. Entin, “Labor Bears Much of the Cost of the Corporate Tax,” Tax Foundation, Oct. 24, 2017, https://www.taxfoundation.org/labor-bears-corporate-tax/; and Alex Durante, “Who Bears the Burden of Corporate Taxation? A Review of Recent Evidence,” June 10, 2021, https://www.taxfoundation.org/who-bears-burden-corporate-tax/.

[11] Clemens Fuest, Andreas Peichl, and Sebastian Siegloch, “Do Higher Corporate Taxes Reduce Wages? Micro Evidence from Germany,” American Economic Review 108:2 (February 2018): 393–418, https://www.doi.org/10.1257/aer.20130570.

[12] Joint Committee on Taxation, “Revenue Estimates and Distributional Analyses,” Aug. 3, 2021, https://www.finance.senate.gov/imo/media/doc/jct_analysis_on_corporate_tax_increase.pdf.

[13] Joint Committee on Taxation, “A Distribution of Returns by the Size of the Tax Change for Estimated Budgetary Effects of Subtitle B and an Amendment in the Nature of a Substitute of the Budget Reconciliation Legislative Recommendations by the Committee on Ways And Means” (D-02-21), Sept. 22, 2021, https://www.finance.senate.gov/imo/media/doc/jct_analysis_on_house_wm_bill.pdf.

[14] Alex Muresianu and Erica York, “U.S. Would Have Third-Highest Corporate Tax Rate in OECD Under Ways and Means Plan,” Sept. 15, 2021, https://www.taxfoundation.org/house-democrats-us-corporate-tax-third-highest/.

[15] Kyle Pomerleau and Grant M. Seiter, “How Would the US Corporate Tax Burden Compare with Those of Other Developed Nations?,” American Enterprise Institute, September 28, 2021, https://www.aei.org/economics/how-would-the-us-corporate-tax-burden-compare-with-those-of-other-developed-nations/.

[16] Cody Kallen, “How Heavily Taxed Are U.S. Multinationals?” see also, Penn Wharton Budget Model, “Effective Tax Rates on U.S. Multinationals’ Foreign Income under Proposed Changes by House Ways and Means and the OECD,” Sept. 28, 2021, https://budgetmodel.wharton.upenn.edu/issues/2021/9/28/effective-tax-rates-multinationals-ways-and-means-and-oecd.

[17] Andrew B. Lyon, “Insights on Trends in U.S. Cross-Border M&A Transactions After the Tax Cuts and Jobs Act,” Tax Notes International 100:4, (Oct. 26, 2020), https://ssrn.com/abstract=3735054; and Zachary Mider, “Tax Inversion,” Mar. 2, 2017, https://www.bloomberg.com/quicktake/tax-inversion.

[18] Scott Eastman, “Corporate and Pass-through Business Income and Returns Since 1980,” Apr. 23, 2019, https://www.taxfoundation.org/pass-through-business-income-since-1980/.

[19] William McBride and Alex Durante, “Top Tax Rate on Pass-through Business Income Would Exceed 50 Percent in Most States Under House Dems’ Plan,” Tax Foundation, Sept. 17, 2021, https://www.taxfoundation.org/house-democrats-pass-through-business-tax/.

[20] Alex Durante and Erica York, “Claiming 97 Percent of Small Businesses Exempt from Biden Taxes is Misleading,” Tax Foundation, Aug. 20, 2021, https://www.taxfoundation.org/97-percent-small-businesses-wont-pay-more-income-taxes-under-biden-tax-plan/.

[21] William McBride et. al., “Build Back Better Act: Details & Analysis of the $3.5 Trillion Budget Reconciliation Bill.”

[22] Erica York and Alex Muresianu, “Top Combined Capital Gains TaxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. Rates Would Average Nearly 37 Percent Under House Dems’ Plan,” Sept. 14, 2021, https://www.taxfoundation.org/house-democrats-capital-gains-tax-rates/.

[23] William McBride et. al., “Build Back Better Act: Details & Analysis of the $3.5 Trillion Budget Reconciliation Bill.”

[24] William McBride, “What Is the Evidence on Taxes and Growth,” Tax Foundation, Dec. 18, 2012, https://www.taxfoundation.org/what-evidence-taxes-and-growth/; see also Alex Durante, “Reviewing Recent Evidence of the Effect of Taxes on Economic Growth.”

[25] Karel Mertens and José Luis Montiel Olea, “Marginal Tax Rates and Income: New Time Series Evidence,” The Quarterly Journal of Economics 133:4 (November 2018), https://academic.oup.com/qje/article-abstract/133/4/1803/4880451?redirectedFrom=fulltext.

[26] Åsa Johansson, Christopher Heady, Jens Arnold, Bert Brys, Cyrille Schwellnus, & Laura Vartia, “Taxation and Economic Growth.”

[27] Congressional Budget Office, “The Economics of Financing a Large and Permanent Increase in Government Spending: Working Paper 2021-03,” Mar. 22, 2021, https://www.cbo.gov/publication/57021; see also Garrett Watson, “Congressional Budget Office and Tax Foundation Modeling Show That Some Tax Hikes Are More Damaging Than Others,” Tax Foundation, Mar. 26, 2021, https://www.taxfoundation.org/tax-hikes-are-more-damaging-than-others-analysis/.

[28] Scott Hodge, “Tax Fairness, Economic Growth, and Funding Government Investments,” Testimony Before the Subcommittee on Fiscal Responsibility and Economic Growth of the Committee on Finance, Apr. 27, 2021, https://www.taxfoundation.org/tax-fairness-funding-government-investments/.

[29] Alex Muresianu, “Yes, the U.S. Tax Code is Progressive,” Sept. 17, 2021, https://www.taxfoundation.org/us-tax-system-progressive/.

[30] Erica York, “Unanswered Questions about Upcoming Advance Child Tax Credit Payments,” Tax Foundation, July 7, 2021, https://www.taxfoundation.org/advance-child-tax-credit-payments/#:~:text=The%20federal%20child%20tax%20credit,single%20filers%20or%20joint%20filers.

[31] Erica York, Garrett Watson, Huaqun Li, “Temporary Policies Complicate the Child Tax Credit’s Future,” Tax Foundation, Sept. 3, 2021, https://www.taxfoundation.org/child-tax-credit-changes-reform/.

[32] For example, the Joint Committee on Taxation estimates that about $84 billion of the approximately $105 billion APRA CTC expansion is an outlay effect. See Joint Committee on Taxation, “Estimated Revenue Effects of H.R. 1319,” JCX-14-21, Mar. 9, 2021, https://www.jct.gov/CMSPages/GetFile.aspx?guid=52961732-5521-49ea-8443-59a539b71b62.

[33] Treasury Inspector General for Tax Administration, “Authorities Provided by the Internal Revenue Code Are Not Effectively Used to Address Erroneous Refundable Credit and WithholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount the employee requests. Credit Claims,” Feb. 26, 2020, https://www.treasury.gov/tigta/auditreports/2020reports/202040008fr.pdf.

[34] The last year the federal government ran a budget surplus was 2001.

[35] Leah Hamilton, Stephen Roll, Mathieu Despard, Elaine Maag, and Yung Chun, “Employment, Financial and Well-being Effects of the 2021 Expanded Child Tax Credit: Wave 1 Executive Summary,” Social Policy Institute Research (September 2021), https://socialpolicyinstitute.wustl.edu/employment-financial-wellbeing-effects-2021-ctc-report/.

[36] Janet Holtzblatt, “Whose Child Is It Anyway? The Ways & Means Definition Makes It Harder for The IRS To Know,” Tax Policy Center, Sept. 27, 2021, https://www.taxpolicycenter.org/taxvox/whose-child-it-anyway-ways-means-definition-makes-it-harder-irs-know.

[37] Scott Winship, “The Conservative Case Against Child Allowances,” American Enterprise Institute, March 2021, https://www.aei.org/wp-content/uploads/2021/03/The-conservative-case-against-child-allowances.pdf?x91208.

[38] Erica York, Garrett Watson, Huaqun Li, “Temporary Policies Complicate the Child Tax Credit’s Future.”

[39] Scott Hodge, “Distribution and Efficiency of Spending in the Tax Code,” Hearing Before the U.S. Senate Budget Committee, Mar. 9, 2011, /wp-content/uploads/2011/03/testimony_hodge_senate_budget_committee_2011-03-09.pdf.

[40] Treasury Inspector General for Tax Administration, “Authorities Provided by the Internal Revenue Code Are Not Effectively Used to Address Erroneous Refundable Credit and Withholding Credit Claims.”

[41] Michael D. Eriksen, “The Market Price of Low-Income Housing Tax Credits,” Journal of Urban Economics 66:2 (September 2009), https://ideas.repec.org/a/eee/juecon/v66y2009i2p141-149.html; see also Everett Stamm, “An Overview of the Low-Income Housing Tax Credit,” Tax Foundation, Aug. 11, 2020, https://www.taxfoundation.org/low-income-housing-tax-credit-lihtc/.

[42] David Roberts, “Clean Energy Tax Credits Mostly Go to the Affluent. Is There a Better Way?” Nov. 24, 2015, https://www.vox.com/2015/11/24/9792474/energy-tax-credits-inequitable.

[43] Alex Muresianu, “How Expensing for Capital Investment Can Accelerate the Transition to a Cleaner Economy,” Tax Foundation, Jan. 12, 2021, https://www.taxfoundation.org/energy-efficiency-climate-change-tax-policy/.

[44] Tax Foundation, “Option 65: Enact Full ExpensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for All Capital Investment,” in Options for Reforming America’s Tax Code 2.0 (Washington, D.C.: Tax Foundation, Apr. 19, 2021), https://www.taxfoundation.org/tax-reform-options/?option=65; see also Alex Muresianu, “Expensing Is Infrastructure, Too,” Tax Foundation, June 15, 2021, https://www.taxfoundation.org/expensing-infrastructure/.

[45] Alex Muresianu, Erica York, William McBride, and Garrett Watson, “The Good, the Bad, and the Ugly of the House Ways and Means Plan,” Tax Foundation, Sept. 20, 2021, https://www.taxfoundation.org/ways-and-means-plan-the-good-the-bad-and-the-ugly/.

[46] Garrett Watson, “Delaying R&D Amortization Costs Less but Generates Little Economic Benefit Compared to Full Cancellation,” Tax Foundation, July 29, 2021, https://www.taxfoundation.org/r-d-amortization-changes/.