Taxes are on the ballot this November—not just in the sense that candidates at all levels are offering their visions for taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policy, but also in the literal sense that voters in some states will get to decide important questions about how their states raise revenue. North Dakotans will decide whether to abolish the property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.; Washingtonians will determine the fate of the state’s relatively new tax on capital gains income; Oregonians will rule on whether to implement the nation’s highest gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. rate; South Dakotans will choose whether to exempt groceries from the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. —and on it goes.

Some measures are modest; others are monumental. Below, we highlight eight of the most significant measures (often with links to further analysis), then briefly summarize all 21 tax-related measures on state ballots this fall. On Election Day, this page will be updated regularly with live results for the eight featured measures.

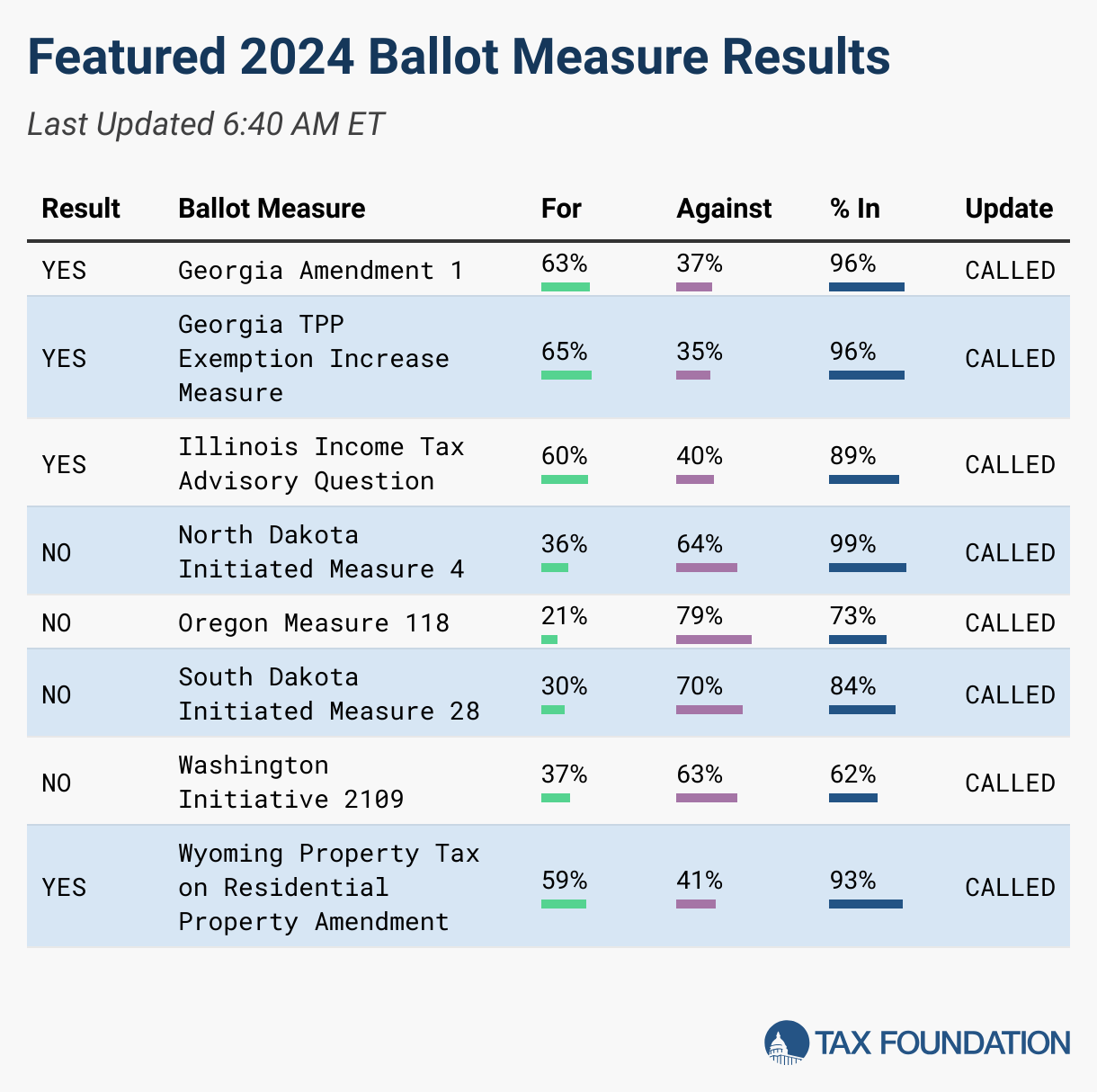

Featured Ballot Measures

Georgia

Georgia Amendment 1, Local Option Homestead Property Tax Exemption Amendment

Georgia’s Local Option Homestead Property Tax Exemption Amendment (also known as Amendment 1) is on the ballot this November. At face value, it may seem like a minor, albeit constitutional, amendment that would authorize a statewide local option homestead exemption from property taxes, while allowing localities the ability to opt out of using the exemption. However, its scope is much broader and could have far-reaching consequences for the property tax system in the state. The reason is that the fate of an important bill, HB 581, depends on the outcome of the November vote. This bill includes several major elements, which we briefly described elsewhere. They include three main elements. First, the combination of Amendment 1 and HB 581 would create a state-wide homestead exemption that effectively resembles an assessment limit. These two measures would enact an overly complex pathway for localities to opt-out of this homestead exemption by March 1, 2025. Finally, they would allow localities to impose an additional sales tax and use tax of up to 1 percent for property tax relief, subject to approval by local referendum. Taken together, these two measures would adversely affect smaller Georgia localities and introduce unnecessary complexity into the local Georgia tax structure. Click here to read more about this measure.

Georgia Personal Property Tax Exemption Increase Measure

This measure would increase the tangible personal property (TPP) de minimis exemption in Georgia from $7,500 to $20,000. As a result, small businesses would be able to exempt some (or most) of their machinery, equipment, fixtures, and supplies from property taxes. Compliance costs for businesses would decrease significantly, with minimal impact on the state government. While this is a positive development, the new exemption level would still be much lower than in many other states, such as Arizona, Colorado, Idaho, Indiana, Michigan, Montana, and Rhode Island (all have exemptions of $50,000 or more). To remain competitive and foster a favorable business climate for entrepreneurs, Georgia could consider further raising the TPP de minimis exemption or eliminating personal property from the property tax base altogether in the future. Click here for more information about this measure’s path to the ballot.

Illinois

Illinois Income Tax Advisory Question

Illinois’ Income Tax Advisory Question is a non-binding question that would not change Illinois law but is designed to gauge public opinion. This advisory question asks voters if the state constitution should be amended to create an additional 3 percent tax on income exceeding $1 million to generate new revenue for property tax relief. Illinois’ constitution requires a single-rate individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source, and the rate is currently statutorily set at 4.95 percent.

Notably, the advisory question does not specify exactly how the language of the state constitution would be amended, nor does it specify how the property tax relief would be distributed. If a 3 percent surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. on income exceeding $1 million were enshrined in the language of the constitution itself—similar to the surtax adopted in Massachusetts in 2022—a future constitutional amendment would be needed for that rate to ever be reduced or eliminated, requiring a three-fifths vote in both houses of the Illinois legislature followed by approval from a majority of Illinois voters in a general election. With an additional income tax rate of 3 percent, Illinois’ top marginal individual income tax rate would be 7.95 percent, making it the 10th highest in the country. Pass-through businesses, which face an existing surcharge, would have a new top rate of 9.45 percent. If the constitution were amended to simply remove the flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. requirement without prescribing new rates within the constitution, legislators could change Illinois’ income tax rate schedule in a manner that raises taxes on many Illinoisans. In 2020, a proposed constitutional amendment to remove the flat tax requirement was soundly rejected by Illinois voters.

North Dakota

North Dakota Initiated Measure 4, Prohibit Taxes on Assessed Value of Real Property Initiative

Initiated Measure 4 is a Constitutional Initiated Measure brought by North Dakota citizens to prohibit the state government and all local taxing entities from assessing a property tax on real or personal property, which could eliminate over $1.5 billion per year in local funding, with the intent that these localities would be made whole by the state. The measure does not, however, establish what revenue options the state could pursue to generate this additional revenue, and alternative sources—like higher income or sales taxes—would be more damaging to North Dakota’s economy than the existing property tax. Measure 4 also prohibits localities from issuing bonds after February 2, 2025. Click here to read more about this measure.

Oregon

Oregon Measure 118, Corporate Tax Revenue Rebate for Residents Initiative

Measure 118 (formerly IP-17) would establish a new 3 percent corporate minimum tax on Oregon gross sales above $25 million, adding another gross receipts tax to the state’s tax system and significantly altering the composition of state revenues. For a business with a 7 percent profit margin, this is equivalent to a 43 percent corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.. The new tax would be imposed in lieu of the corporate income tax for most taxpayers, but in addition to the 0.57 percent Corporate Activity Tax (CAT) and a range of local and regional business income taxes. While proponents argue that only the largest corporations would be affected, our estimates show that more than 1,500 firms would be subject to the tax, with the greatest impact on sectors with the lowest profit margins, such as retail trade. Moreover, Oregon-based businesses not directly subject to the tax would see an increased cost of doing business since many of their factors of production would be subject to the tax. Tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action. is likely, especially in value chains dominated by large corporations, which could lead to considerable price increases for Oregon residents while driving up the cost of doing business in Oregon. In return, Oregon residents who spend more than 200 days in the state would receive rebates financed through this new tax. For further analysis of this measure, click here, here, and here.

South Dakota

South Dakota Initiated Measure 28, Prohibit Food and Grocery Taxes Initiative

South Dakota Initiated Measure 28 would prohibit state sales taxes on items sold for human consumption, excluding alcoholic beverages, tobacco, and prepared foods. This measure, if passed, would eliminate the 4.2 percent state sales tax on groceries, potentially reducing state revenues by approximately $124 million annually, starting in July 2025. Local governments, however, would continue to be able to tax grocery purchases. Proponents argue it would alleviate food insecurity and promote economic fairness, while opponents warn of potentially significant budget shortfalls and consequent cuts to public services, which may aggravate hardships or lead to an increase in or imposition of other taxes. The measure would also reduce revenue neutrality and shrink the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.. Notably, while it makes intuitive sense that grocery exemptions would help low-income households, existing exemptions for purchases made with SNAP benefits result in the bulk of the benefit flowing to middle- and higher-income earners. Click here for a Tax Foundation analysis of grocery tax exemptions. For further analysis of this measure, click here.

Washington

Washington Initiative 2109, Repeal Capital Gains TaxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. Initiative

Initiative 2109 would repeal a controversial tax on capital gains income. Despite constitutional restrictions on income taxation, Washington lawmakers implemented—and the state supreme court affirmed—a tax on high earners’ net capital gains income, with the court concluding that the tax is on the privilege of earning income, not on the income itself, even if it is levied according to net capital gains income. While the tax only applies to capital gains income of $250,000 or more, opponents have pointed to the tax’s volatility, as it is uniquely sensitive to stock market swings, as well as its vulnerability to the outmigration of high-net-worth individuals. Additionally, while regular year-to-year payers of the tax are certainly wealthy, most people who pay the tax at some point in their lives will be ordinary taxpayers who have just sold a home or business. And the logic employed by the court in approving the tax despite constitutional constraints could just as easily apply to wage income (a tax on the privilege of employment, or of earning wage income), and lawmakers have already begun considering lowering the capital gains income threshold to capture far more taxpayers. For more on the existing tax, click here. Additional analysis of the ballot measure is forthcoming.

Wyoming

Wyoming Property Tax on Residential Property and Owner-Occupied Primary Residences Amendment

This legislatively referred constitutional amendment would add residential property as a fourth class of property to the state’s tax code. Additionally, the measure would authorize the legislature to create a new subclass of residential property for owner-occupied primary residences with a distinct assessment ratio. If approved, it would expand the state’s split roll (or differentiated) property tax system. Split roll property tax regimes introduce non-neutrality to the tax code by changing the incentives to own or invest in certain types of property over others. It also shifts more of the tax burden to renters, who often have lower incomes than homeowners. Moreover, a differentiated tax system can encourage lawmakers to increase the property tax burden on some classes of property, often to the detriment of businesses, to generate additional revenue without being seen as raising taxes on homeowners. These issues could be exacerbated if the amendment were to be approved by voters, and potentially more so if the legislature opts to create a new subclass of residential property with its own assessment ratio. See further Tax Foundation analysis of this amendment here.

All Tax-Related Ballot Measures

| State | Ballot Measure | Description |

|---|---|---|

| Arizona | Arizona Proposition 312, the Property Tax Refund for Non-Enforcement of Public Nuisance Laws Measure | Would allow property owners to apply for a property tax refund in certain situations, specifically when a city or locality fails to enforce public safety regulations related to illegal camping, loitering, public consumption of alcohol, and other issues. |

| California | California Proposition 35, the Managed Care Organization Tax Authorization Initiative | Permanently authorizes a tax on managed care organizations, which is currently set to expire in 2026, while capping the amount of the tax and allocating the revenue to Medi-Cal administration. |

| Colorado | Colorado Amendment G, the Property Tax Exemption for Veterans with Individual Unemployability Status Amendment | Would extend the existing homestead exemption to veterans who have a service-connected disability and qualify for a Total Disability Individual Unemployability (TDIU) rating from the US Department of Veterans Affairs, eligibility standards that are less onerous than the current restriction to veterans with a 100 percent permanent service-connected disability rating. |

| Colorado | Colorado Proposition JJ, the Retain Sports Betting Tax Revenue for Water Projects Measure | Would allow the state to collect tax revenue from sports betting above the $29 million cap approved by voters in 2019. |

| Colorado | Colorado Proposition KK, the Excise Tax on Firearms Dealers, Manufacturers, and Ammunition Vendors Measure | Would create a new 6.5 percent excise tax on the sale of firearms, firearm parts, and ammunition, with revenue exempt from the state’s revenue limit and used to fund support services for crime victims, mental health services for veterans and youth, and school safety programs. |

| Florida | Florida Amendment 5, the Annual Inflation Adjustment for Homestead Property Tax Exemption Value Amendment | Would inflation-index the Florida homestead property tax exemption, which applies to all taxing entities except school districts. |

| Georgia | Georgia’s Local Option Homestead Property Tax Exemption Amendment (Amendment 1) | Would authorize a statewide local option homestead exemption from property taxes, while granting counties and other local governments the ability to opt out of using the exemption under a process to be determined by the state legislature (Tax Foundation analysis here). |

| Georgia | Georgia’s Creation of Tax Court Amendment | Would establish the Georgia Tax Court, which would have concurrent jurisdiction with the state business court and superior courts in equity cases. |

| Georgia | Georgia’s Personal Property Tax Exemption Increase Measure | Would increase the tangible personal property de minimis exemption from $7,500 to $20,000, a positive development for small local businesses at a minimal cost to the state government. |

| Illinois | Illinois’ Income Tax Advisory Question | A non-binding measure, asks voters if the state constitution should be amended to create an additional 3 percent tax on income exceeding $1 million to generate new revenue for property tax relief, without specifying whether any constitutional amendment to accomplish this purpose would be limited to that rate and bracket, which would yield a 7.95 percent top rate for individuals and a 9.45 percent top rate for pass-through businesses. |

| Louisiana | Louisiana’s Property Tax Sales Administration Amendment | Would repeal certain constitutional provisions regarding state sales of properties on which there is a tax delinquency, instead leaving these matters up to the legislature through statutory law. |

| Nevada | Nevada Question 5, the Sales Tax Exemption for Diapers Measure | Would exempt child and adult diapers from the state’s sales and use tax. |

| New Mexico | New Mexico Constitutional Amendment 1, the Disabled Veteran Property Tax Exemption Amendment | Would extend the disabled veteran property tax exemption to all disabled veterans (or their widows or widowers) in proportion to their federal disability rating, rather than applying it only to veterans with a 100 percent disability rating. |

| New Mexico | New Mexico Constitutional Amendment 2, the Increase Veteran Property Tax Exemption Amendment | Would increase the property tax exemption for honorably discharged members of the armed forces or their widows or widowers from $4,000 to $10,000 beginning in tax year 2024 and inflation-adjust it thereafter. |

| North Dakota | North Dakota Initiated Measure 4, the Prohibit Taxes on Assessed Value of Real Property Initiative | Would repeal all property taxes on both real and personal property, and eliminate bonding authority after February 1, 2025 (Tax Foundation analysis here). |

| Oregon | Oregon Measure 118, the Corporate Tax Revenue Rebate for Residents Initiative | Would establish a new 3 percent gross receipts tax (in the form of a corporate minimum tax) on Oregon gross sales above $25 million, using the revenue from this nation’s-highest gross receipts tax to fund taxpayer rebates (Tax Foundation analysis here, here, and here). |

| South Dakota | South Dakota Initiated Measure 28, the Prohibit Food and Grocery Taxes Initiative | Would prohibit a state sales tax on anything sold for human consumption, except alcoholic beverages or prepared food, though local governments could continue to include groceries in their sales tax bases. (Tax Foundation analysis here). |

| Virginia | Virginia’s Property Tax Exemption for Veterans and Surviving Spouses Amendment | Would extend property tax exemptions to the surviving spouses of all veterans who died in the line of duty, not just those killed in action. |

| Washington | Washington’s Initiative 2109, the Repeal Capital Gains Tax Initiative | Would repeal the state’s new tax on the net capital gains income of high earners, which has the potential to be extended to a far broader range of taxpayers and was affirmed based on a constitutional interpretation that appears to open the door to a wage income tax. |

| Washington | Washington Initiative 2124, the Opt-Out of Long-Term Services Insurance Program Initiative | Would allow income earners to opt out of the state’s new payroll tax for long-term care in exchange for waiving the benefit of the state-operated long-term care insurance program, which would most likely undermine the financial viability of the program. |

| Wyoming | Wyoming’s Property Tax on Residential Property and Owner-Occupied Primary Residences Amendment | Would add residential property as a fourth class of property to the state’s tax code and authorize the legislature to create a new subclass of residential property for owner-occupied primary residences with a distinct assessment ratio, which could shift more of the tax burden onto renters and businesses (Tax Foundation analysis here). |

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe