The TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation’s State Tax Competitiveness Index enables policymakers, taxpayers, and business leaders to see how their states’ tax systems measure up across a wide range of tax measures. While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.

The Tax Foundation has published this study, previously called the State Business Tax Climate Index, since 2003. Last year, we updated the methodology to more comprehensively address a range of emerging tax issues. As with any methodological changes, we apply them to prior years as well to allow for an apples-to-apples comparison across years. Currently, backcasting under the new methodology stretches back to fiscal year 2020 (July 1, 2019).

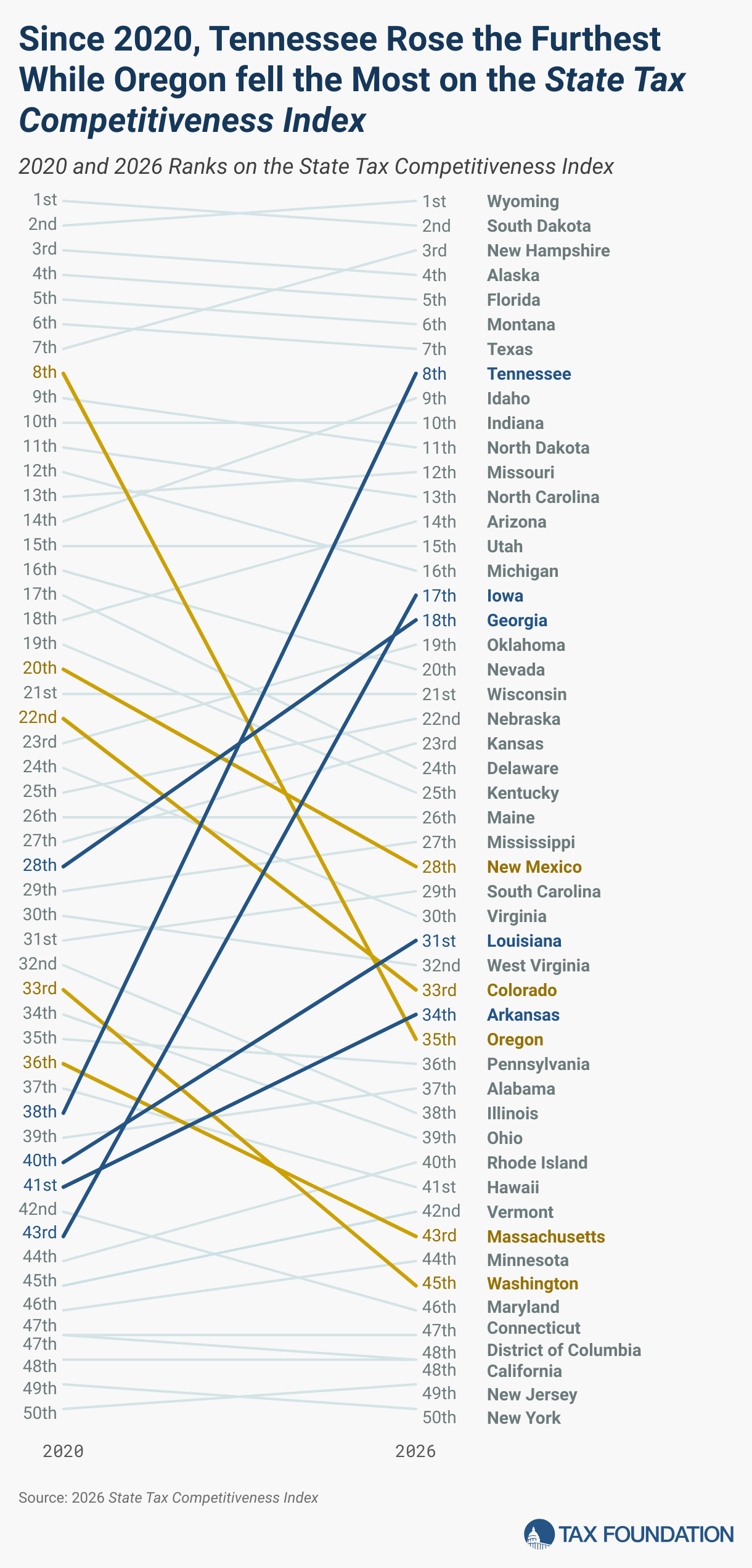

In the spirit of change and improvement, it’s worth looking back to see which states have truly embraced tax competitiveness since 2020, and which ones have lagged behind.

The five states that saw the largest improvements in their rank over the last six years are:

- Tennessee, which ranked 38th in 2020, now ranks 8th.

- Iowa, which ranked 43rd in 2020, now ranks 17th.

- Georgia, which ranked 28th in 2020, now ranks 18th.

- Louisiana, which ranked 40th in 2020, now ranks 31st.

- Arkansas, which ranked 41st in 2020, now ranks 34th.

The five states that fell the furthest in the rankings in the last six years are:

- Oregon, which ranked 8th in 2020, now ranks 35th.

- Washington, which ranked 33rd in 2020, now ranks 45th.

- Colorado, which ranked 22nd in 2020, now ranks 33rd.

- New Mexico, which ranked 20th in 2020, now ranks 28th.

- Massachusetts, which ranked 36th in 2020, now ranks 43rd.

Highlighting the Good

Amidst a country-wide flat tax revolution, the states that saw the greatest Index ranking improvements consolidated their individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source brackets and reduced rates across multiple major taxes, making their tax codes more attractive to businesses and individuals alike.

Tennessee reduced the rates of its corporate gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding., improved its treatment of business expensing, and fully phased out its tax on individual interest and dividends income, becoming one of eight states to have no individual income tax.

Iowa has been working toward comprehensive tax reform for several years, and its dedication is paying off. Since our 2020 ranking, the state repealed its alternative minimum tax, reduced its top corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate from 12 percent to 7.1 percent, and consolidated four brackets into two. On the individual side, the state reduced its top income tax rate from 8.53 percent in 2019 (and 8.98 percent before reforms adopted in 2018) to a highly competitive 3.8 percent and converted a nine-bracket system to a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets..

Georgia successfully turned its graduated individual income tax into a flat 5.19 percent tax. At the same time, it tied its corporate income tax rate to the individual rate, reducing it from 5.75 to 5.19 percent, while adopting other reforms.

Louisiana, too, has been working toward comprehensive tax reform for many years. Since the 2020 ranking, the state has eliminated its uncompetitive throwout rule and its policy of federal deductibility, reduced its corporation franchise tax rate, brought down the individual income tax rate from 6 percent to 3 percent, and consolidated five corporate income tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. into one, with a top rate reduction from 8 to 5.5 percent. Louisiana is also one of three states to adopt permanent full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. separate from federal provisions.

Arkansas saw rate reductions and bracket consolidation as well. Lawmakers reduced the corporate and individual income tax rates from 6.5 and 6.9 percent to 4.3 and 3.9 percent, respectively. The corporate income tax now features only four brackets, and the individual income tax has only two, while both previously had six. The state also improved its nonresident income tax provisions, among other reforms.

Learning from the Bad

Oregon adopted a modified gross receipts tax in addition to its normal corporate income tax. This new tax has relatively high rates, which compounds the tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action. caused by typical gross receipts taxes.

Washington previously had no income tax at all, and its individual income tax rank bolstered its overall Index score. However, in 2022, the state instituted a tax on individual capital gains income over $278,000 (with a top bracket now raised to $1 million), which is now imposed at a rate of 9.9 percent after a recent increase. Without the help of a strong income tax score, the state’s other categories weighed down its overall rank, which quickly plummeted.

Colorado did not make the large, negative changes of the other states in this list. Instead, it demonstrates a cautionary tale of resting on laurels at a time when states are really competing for the best tax code. Colorado was sitting comfortably at 22nd on the Index in 2020 because of its relatively low-rate flat taxes—and the state even reduced its income tax rate from 4.5 to 4.4 percent. However, unlike other states, Colorado did not address some of the inefficiencies in its tax code, like its throwback rule and taxation of net CFC-tested income (NCTI, formerly GILTI). The state has also failed to address its lack of a uniform sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. base and unified administration.

New Mexico bucked the trend of tax bracket consolidation, instead adding more individual income tax brackets (expanding from four brackets to six), increasing its top rate from 4.9 to 5.9 percent, and increasing the top rate kick-in from $16,000 to $210,000. The state did implement a flat corporate income tax, but did so by eliminating the benefit of a 4.8 percent lower rate and leaving an overall rate of 5.9 percent.

Massachusetts, through a 2022 ballot measure, changed its flat income tax into a progressive income tax by adding a top rate of 9 percent (compared to the previous rate of 5 percent) for income over $1,000,000. The state also enacted a new payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue..

Conclusion

A state’s ranking is not a permanent label—instead, it is meant to show states where they have done well and where they can still improve. If state legislators make pro-growth changes, they can jump up in the rankings, as these states prove. And many states have done just that in the last six years, truly prioritizing tax reform in such a way as to leave behind those states that are simply standing still. Every state can benefit from a simple, neutral, transparent, pro-growth tax structure.

Subscribe to our free newsletter to get the latest tax data, news and analysis.Stay informed on the tax policies impacting you.