Introduction

Oklahoma policymakers have been grappling with taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform for decades, spurred by a desire to enhance the state’s competitiveness, and particularly by the success of the state’s neighbor to the south, which has harnessed a competitive tax system and other pro-growth policies to attract people, jobs, and businesses. Recently, lawmakers have enacted pro-growth and competitive reforms, but there remains important work to do in addressing the structural inefficiencies that keep Oklahoma from realizing its full potential.

This publication is designed to update our 2021 study and provide policymakers with a menu of options: some of them bold, comprehensive approaches and others small standalone policy tweaks, but all designed to make Oklahoma a more attractive place to live and work. Each major tax category—individual income taxes, corporate income taxes, sales taxes, and ad valorem and other property taxes—is considered in turn, with discrete reform options within each tax category. Additional options, however, cross categories, identifying ways to reform two taxes in tandem to maintain revenue neutrality while shifting toward more economically efficient forms of taxation.

Reforms Since 2021

Since 2021, Oklahoma lawmakers have made concerted efforts to make the state’s tax code more competitive and friendly to residents and businesses. This has included reductions in corporate and individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. rates, elimination of the state’s capital stock tax (franchise tax), and elimination of the marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples. .[2]

In 2022, corporate income taxpayers became subject to a competitive flat rate of 4 percent, down from 6 percent, tying Oklahoma with Missouri for the second lowest rate in the nation among states with a traditional corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. . Moreover, in 2023, Oklahoma became the first state to adopt permanent first-year full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for qualifying investments in machinery and equipment, followed by Mississippi (2024) and Louisiana (2025). This boosted the state’s competitiveness, particularly as the federal provision began to phase out, leaving those states that continue to conform to the federal provision less competitive in this regard.

At the same time, Oklahoma reduced its individual income tax by 0.25 percentage points across the board. Accordingly, the top rate—previously 5 percent—declined to 4.75 percent, the sixth lowest of states that levy an income tax. While the rate reduction is competitive, the individual income tax code still features six brackets and is not indexed for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. , exposing taxpayers to bracket creepBracket creep occurs when inflation pushes taxpayers into higher income tax brackets or reduces the value of credits, deductions, and exemptions. Bracket creep results in an increase in income taxes without an increase in real income. Many tax provisions—both at the federal and state level—are adjusted for inflation. , which occurs when inflation pushes a taxpayer from a lower bracket to a higher one when nominal income rises, but due to inflation, real income does not, or may even decline. And while Oklahoma’s brackets are quite narrow, rendering these effects small, adopting a single-rate tax can help lock in a competitive rate for years to come.

These rate cuts reduced state revenue, but Oklahoma policymakers identified an opportunity to pay for them out of growth. Oklahoma, like many other states, saw revenues increase during the pandemic. Although most of the revenue growth consisted of one-time funds, the state still experienced an increase of $552 million in recurring revenue,[3] with tax revenue growth of 5 percent in the general fund between fiscal years 2019 and 2021, sufficient to pay down permanent rate reductions.[4]

Oklahoma was not the only state with an eye on tax competitiveness in recent years. Since 2021, with burgeoning revenues in the wake of the coronavirus crisis and the prospect of workplace flexibility greatly enhancing the salience of tax competition, 28 states cut individual income tax rates and 15 states cut corporate income tax rates, some doing both.

The COVID-19 pandemic and subsequent years ushered in a time of substantially more revenue than expected. This is true even when looking exclusively at tax or other own-source revenue, and excluding all federal transfers under the CARES Act, the American Rescue Plan Act (ARPA), or other federal legislation enacted in response to the pandemic. Taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income. grew during this time, partly due to those time-limited federal infusions, but largely because longer-term economic trends continued almost unabated. States emerging from the public health crisis not only with adequate revenue, but in many cases robust growth, recognized an opportunity for tax relief. Many policymakers across the country saw it not just as an opportunity but as a necessity, a way of demonstrating their state’s commitment to tax and overall economic competitiveness in an increasingly mobile world, and Oklahoma was no exception.

Reliance on Severance Taxes

Oklahoma’s continued reliance on the severance tax, which is imposed on the extraction of oil and other minerals, should provide additional motivation for tax reform. Severance taxes represented the third highest tax revenue generator for the state in fiscal year 2023, behind income and sales taxes, and comprised 12.75 percent of state tax collections in fiscal year 2023.[5] While this is far from the state’s main source of revenue, fluctuations in the oil and gas industry can affect the state’s financial footing.

As helpful as this revenue can be, severance tax collections are extremely volatile, and a significant reliance on them as a funding source can create difficulties for revenue estimation and budgeting. From 2011 to 2023, the state saw severance revenues range from $331 million to $1.8 billion (in nominal dollars).

Since the 1960s, crude oil production in the state has also seen large fluctuations. Production reached a high in 1966 but dropped steeply in the 1990s and early 2000s. Since 2010, production has once again picked up, but Oklahoma cannot count on this trend to continue forever, especially with the rise of alternative energy sources. Oil, gas, and other natural resources will continue to play an important role in Oklahoma for the foreseeable future, but policymakers need to focus on diversification to prepare for a decline in the resource sector’s fortunes.

Oklahoma is seeking to gain ground in new energy sectors, or in new industries entirely. However, the state tax code includes many elements that may hold back the state in this endeavor. The state’s throwback rule disadvantages businesses that sell out of state, and the tax on inventory disadvantages businesses that sell within the state. The elimination of full expensing is a bold reform which targets manufacturers and other capital-intensive industries—precisely the businesses that Oklahoma will be looking to attract. Nevertheless, many individuals and businesses will continue to look to neighboring Texas, which forgoes an individual income tax, as an attractive alternative.

Consequently, lawmakers still have work to do to make improvements to Oklahoma’s tax code. They should seize the opportunity to implement tax reforms that improve the state’s competitiveness and enhance its appeals to employers and employees alike. Oklahoma has long recognized the need for a growth agenda, and while the state has made significant steps in the right direction, policymakers should recognize that tax competition is real and work to propel the state forward rather than wait for others to catch up.

Corporate Income Taxes

The corporate income tax is levied at a flat rate of 4 percent, tying the state with Missouri for the second-lowest rate in the nation, surpassed only by North Carolina’s 2.5 percent among states with a corporate income tax. The ideal rate of taxation on capital is zero, and corporate income taxes are a form of double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. since income is taxed again when distributed or taken in salary. Nevertheless, all but two states have either a corporate income tax, a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. , or both. Corporate income taxes are preferable to gross receipts taxes, and Oklahoma’s rate remains highly competitive.

Despite the low rate, however, Oklahoma’s corporate income tax advantage is hindered by several structural impediments. A throwback rule dramatically increases corporate income tax costs for some in-state businesses. Moreover, the state’s three-factor apportionmentApportionment is the determination of the percentage of a business’ profits subject to a given jurisdiction’s corporate income or other business taxes. U.S. states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. formula is increasingly out of line with a national trend toward single sales factor apportionment, which eliminates the tax’s bias against in-state investment. Recent efforts to amend the apportionment formula could have yielded positive gains for Oklahoma, but did not gain the necessary traction in the legislature.[6]

Oklahoma’s decoupling from the federal policy of full expensing of capital investment signaled the state’s commitment to a pro-growth tax code. Amending other policies would further enhance Oklahoma’s competitiveness. Addressing these issues within the corporate tax code would enhance the state’s attractiveness for C corporations at a time when mobility is at record highs.

The Throwback Rule

Ask most people what a throwback rule is, and they may explain the local requirement to throw back a visiting team’s home run from the hometown bleachers. Ask a member of the business community and she is likely to tell you about how the tax has affected her business. While opaque to the average citizen, the business community clearly understands the impact of the throwback rule due to its dramatic effect on a firm’s taxable income. It has also been shown to affect business location decision-making. Not unlike other complex tax policies, throwback rules are often enacted with one intent but end up causing unintended consequences.

However, before we can address the uncompetitive nature of throwback rules, it is first necessary to explain why they exist, how they work, and where they fit into a corporate income tax.[7]

Apportionment In Oklahoma

When C corporations conduct business in multiple states, it is necessary for states to apportion that income for tax purposes. That means they must determine what share of their income is taxable in each involved state.[8] Currently, states can use three factors in their apportionment formulas: the share of total property, payroll, and sales that a firm has located in each state. Historically, most states weighted these factors evenly. However, there is a pronounced trend toward giving greater—or even exclusive—weight to the sales factor. Doing so generally benefits in-state companies while exporting some of the tax burden to companies with sales, but less of a physical presence, in that state.[9]

The apportionment technique can make a huge difference in businesses’ tax burdens. Iowa, for example, has a high corporate income tax top rate of 9.8 percent, but manufacturers often face light corporate income tax burdens due to the state’s single sales factor apportionment.[10] On the other hand, Montana has a lower top rate of 6.75 percent, but it employs an evenly weighted three-factor apportionment formula. This creates an above-average corporate income tax burden on many manufacturers.[11]

Oklahoma has opted for the more traditional choice of evenly weighted three-factor apportionment. Notably, it also allows firms with capital investment of more than $200 million the choice of using double-weighted sales factor apportionment.

Courts have granted states substantial leeway in adopting competing approaches to apportionment, provided that the chosen approach meets two main criteria. First, the apportionment decision must have some rational relationship to the company’s activity in the state—a very permissive standard. Second, the apportionment must be internally consistent. In other words, if every state chose the same given apportionment formula, no more than 100 percent of a corporation’s income would be taxed. This criterion stands even if in practice the interaction of competing standards yields double taxation.[12]

The problem of taxing more than 100 percent of income has vexed taxpayers and practitioners, but states have often perceived a different problem: the possibility of taxing less than 100 percent of a corporation’s business income.

For states to levy taxes on a company, there must be a sufficient connection—termed “nexus”— between the state and the company’s economic activities. The chief limitation on state nexus is Public Law 86-272. This federal law prohibits states from taxing income arising from the sale of tangible property into the state by a company whose only activity in that state is the (remote) solicitation of sales. In other words, if a company maintains a warehouse in the state or even just a kiosk; if it has a sales office, or even just a traveling salesman; if it so much as delivers one of its products into the state with its own employees or in its own vehicle— if any of these factors are present, the company has nexus with the state and is taxable according to the state’s apportionment formula. If, however, any marketing is produced in another state, the sales office records the transactions in another state, and products are shipped to customers via a common carrier, it does not matter whether the sales into that state are 1 percent or 100 percent of the company’s revenues. By law, that sales income is not taxable in the destination state, because the contacts with the state are insufficient under federal law to establish nexus.[13]

Companies stand to benefit if they can avoid any economic activity other than the remote solicitation of sales into a state. This decision is made at the margin as many other factors influence the decision of where to locate facilities and employees. In fact, many larger businesses are resigned to the fact that they will have nexus almost everywhere. Indeed, many business models are structurally unsuited to avoiding the establishment of nexus in states where they have sales. Still, some companies have flexibility in where they produce and where they sell. These can benefit from locating their production in a single sales factor or low corporate income tax state all the while selling into states which lack the jurisdiction to tax them. This is where throwback rules come into play.

What Is a Throwback Rule?

The average citizen’s intuition in defining a throwback rule was not far off. In states where firms have no nexus for taxation, either because of apportionment rules or lack of jurisdiction, a firm’s sales to that state result in “nowhere income.” Throwback rules are designed to reclaim “nowhere income,” from a state that has no legal authority to tax it and give that income back to a state with jurisdiction over the taxpayer. Under a throwback rule, sales of tangible personal property are figuratively “thrown back” across state lines and incorporated into the numerator of the origin state’s sales factor—even though the state would not otherwise be able to claim that income.

How Throwback Rules Work

Although some states have adopted their own language, the standard throwback rule establishes uniform language promulgated as part of the Multistate Tax Compact,[14] which imposes two requirements. First, the taxing state must be the location from which the tangible property was shipped. Second, the income cannot be taxable in the state of the purchaser, either because the purchaser was the federal government or because the destination state lacks jurisdiction to levy a tax.

Importantly, throwback rules do not apply in cases where a state voluntarily chose not to tax corporate income. Throwback rules ask whether the corporation is taxable in the destination state, not whether it was taxed. (Sometimes, policymakers in states without a corporate income tax, or which provide incentives which zero out some corporations’ tax liability, express concern that the revenue they forgo is being swept up by another state’s throwback rules. They need not worry.)

A company’s income from one state cannot be thrown back to another if the firm can demonstrate that the good was subject to a net income, franchise, or capital stock tax in the destination state, or if that state possessed jurisdiction to levy a tax on the company but opted not to impose corporate taxes.

The list of applicable taxes in destination states is not exhaustive, and that is by design. A company immunized against destination state taxation under P.L. 86-272 cannot avoid throwback by exposing itself to some minimal business fee or tax in the destination state or making a voluntary payment; the tax must be a corporate income tax or a state’s alternative to one.[15]

Table 1. States with Throwback and Throwout Rules for Sales of Tangible Property

As of January 1, 2024

| State | Throwback | Throwout |

|---|---|---|

| Alaska | ✔ | |

| Arkansas | ✔ | |

| California | ✔ | |

| Colorado | ✔ | |

| District of Columbia | ✔ | |

| Hawaii | ✔ | |

| Idaho | ✔ | |

| Illinois | ✔ | |

| Kansas | ✔ | |

| Maine | ✔ | |

| Massachusetts | ✔ | |

| Mississippi | ✔ | |

| Montana | ✔ | |

| New Hampshire | ✔ | |

| New Mexico | ✔ | |

| North Dakota | ✔ | |

| Oklahoma | ✔ | |

| Oregon | ✔ | ✔ |

| Utah | ✔ | |

| Vermont | ✔ | |

| Wisconsin | ✔ |

Competitive and Economic Effects of Throwback Rules

While throwback rules were created to avoid the perceived under-taxation of corporate income, they can lead to double taxation and frequently impose tax burdens high enough to make the state unattractive for businesses.

In terms of attracting corporations to the Sooner State, Oklahoma is at a slight comparative disadvantage in that it does not rely on sales alone for its apportionment formula. Single sales factor apportionment has the effect of exporting part of the corporate income tax burden to out-of-state firms. The introduction of a throwback rule further erodes the competitive advantage otherwise held by in-state firms.

Whatever revenue Oklahoma generates from the throwback rule will most likely be offset by lost revenue as a result of firms’ relocations—the natural response to uncompetitive tax rates and apportionment rules. The throwback rule increases a firm’s in-state income by the sum of the firm’s “nowhere income.” Therefore, the sales factor ratio necessarily increases. Paradoxically, the more a throwback rule increases a firm’s sales factor, the larger a company’s effective tax rate, and the less relevant the state’s corporate income tax rate becomes.[16] Effective rates on the income actually generated in-state can become so high as to make certain types of business activity unviable in states with such rules, and over time, businesses have adjusted to this reality. The economic literature suggests that this self-sorting is so prevalent that, even though the throwback rule raises revenue from businesses which have not acted to avoid it, the rule may lose revenue in the long run due to activity driven out of state which would otherwise be subject to the full range of state taxes.

In terms of simplicity, Oklahoma’s corporate tax code does offer a silver lining. Unlike many states, Oklahoma requires separate reporting for unitary groups. This means that each company in a related group of corporations (parent companies, subsidiaries, and affiliates) files a separate tax return. Alternatively, many states opt for combined reporting where all related corporations file as a unitary group. Thanks to the separate reporting policy, Oklahoma avoids the added complexity that occurs when the challenges of throwback rules are exacerbated by combined reporting.

The Inequity of Throwback Rules

Four arguments speak to the inequity of throwback rules. First, the logic of the throwback rule suggests that an origination state has the right to tax income properly associated with another state simply because the other state is unable to tax the income itself. Proponents hold up throwback rules as a means of righting the perceived wrong of anything less than 100 percent taxability of business income. Opponents, for their part, tend to see the rule as “levying the wrong tax at the wrong rate in the wrong state.”[17] That a business has untaxed activity in one state is not, of itself, a clear reason why an outside jurisdiction should tax that activity.[18]

Second, the degree to which many businesses can avoid the consequences of throwback rules undermines the equity argument. The rules ultimately become a tax on a relatively small number of businesses that lack avoidance opportunities. Moreover, states’ equity concerns tend to be one-sided and preoccupied only with under-collection, not over-collection. For instance, there has been notably less handwringing from states since the courts have permitted a pastiche of mismatched apportionment formulas and rules which can lead to double taxation. In the words of one scholar, “Why should ‘nowhere income’ be any more unpalatable than the over-taxation or ‘imaginary income’ that results for some taxpayers?”[19]

Third, the result of throwback rules is not neutral taxation, since any income “thrown back” is taxed at the origination state’s rate, not the rate of the destination state which is unable to tax it. Companies with little ability or inclination to design their corporate structure around the tax code will face uncommonly high tax burdens, while other businesses may locate their sales activities in non-throwback states.[20]

Finally, throwback rules undermine the theoretical justification for making sales a factor in formulary apportionment in the first place. State authority to tax is premised on some connection between the activities of the taxpayer and either the costs they impose on the state or the benefits they receive from the state (though this requirement is construed broadly). There can be little doubt that companies benefit from the governance of states in which they have payroll or property. The justification for apportioning partly or entirely based on sales, however, has historically been that companies benefit from access to a marketplace for which the state is in some ways responsible. For a throwback state to tax income from outbound sales is in some respects a repudiation of that theory. It operates as if the other state conferred no benefits whatsoever and thereby left the tax revenue for the originating state to claim.[21]

Repealing the Throwback Rule

As a rule, tax cuts do not pay for themselves. Throwback rules, however, may very well be the exception. Since Oklahoma is on solid financial footing following the coronavirus pandemic, the state is well-positioned to cover any short-term transition costs associated with the repeal of its throwback rule. In the longer term, repeal will increase Oklahoma’s ability to attract and retain businesses, thereby expanding, stabilizing, and promoting greater equity within its corporate tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. .

Formulary Apportionment

As noted, Oklahoma is one of a dwindling number of states to use evenly weighted three-factor apportionment for most companies, with some permitted to elect double-weighted sales factor apportionment, where sales account for 50 percent of apportionment and payroll and property are responsible for 25 percent apiece. There are good historical reasons for including payroll and property in the apportionment formula, or even making them the only factors, to the exclusion of sales. These arguments work best, however, if such a formula is adopted uniformly across the states. At a time when many other states have shifted to single sales factor apportionment, Oklahoma’s choice undermines its competitiveness with its peers. Only seven states still use evenly weighted three factor apportionment as its primary apportionment factor.

Table 2. State Apportionment Formulas

As of January 1, 2025

| State | Single Sales | Sales Weighted | Three-Factor |

|---|---|---|---|

| Alabama | ✔ | ||

| Alaska* | ✔ | ||

| Arizona* | ✔ | ||

| Arkansas | ✔ | ||

| California | ✔ | ||

| Colorado | ✔ | ||

| Connecticut | ✔ | ||

| Delaware | ✔ | ||

| Florida** | ✔ | ✔ | |

| Georgia | ✔ | ||

| Hawaii | ✔ | ||

| Idaho | ✔ | ||

| Illinois | ✔ | ||

| Indiana | ✔ | ||

| Iowa | ✔ | ||

| Kansas | ✔ | ||

| Kentucky | ✔ | ||

| Louisiana* | ✔ | ||

| Maine | ✔ | ||

| Maryland | ✔ | ||

| Massachusetts | ✔ | ||

| Michigan | ✔ | ||

| Minnesota | ✔ | ||

| Mississippi | ✔ | ||

| Missouri | ✔ | ||

| Montana | ✔ | ||

| Nebraska | ✔ | ||

| New Hampshire* | ✔ | ||

| New Jersey | ✔ | ||

| New Mexico | ✔ | ||

| New York | ✔ | ||

| North Carolina | ✔ | ||

| North Dakota | ✔ | ||

| Oklahoma | ✔ | ||

| Oregon | ✔ | ||

| Pennsylvania | ✔ | ||

| Rhode Island | ✔ | ||

| South Carolina | ✔ | ||

| Tennessee** | ✔ | ✔ | |

| Utah* | ✔ | ||

| Vermont | ✔ | ||

| Virginia** | ✔ | ✔ | |

| West Virginia | ✔ | ||

| Wisconsin | ✔ |

** = State has weighted sales in addition to its apportionment factor.

Source: Bloomberg Tax.

The best argument for including payroll and property in the apportionment formula is that these factors capture the actual business activities which impose costs on government and are a proxy for the services those businesses receive. While the sales factor is justified on the grounds that companies exploit a state’s market and rely on government to ensure conditions conducive to commerce, this connection is much more nebulous than the idea that companies derive benefit from government services where, say, their offices and factories are located.

By taxing based on these factors, however, Oklahoma bases corporate income tax liability, in substantial degree, on a company’s footprint in the state. Single sales factor apportionment, by contrast, is based exclusively on sales activity into the state, without regard to the location of the company’s productive activity. This succeeds in exporting a significant portion of the tax burden to out-of-state companies, which many state policymakers like, but it also avoids “punishing” businesses for choosing to locate their facilities in-state.

One complicating factor for Oklahoma is its extractive industries. Oklahoma raises considerably less than it could from out-of-state businesses, but more than it would otherwise from its in-state businesses—including oil, gas, and mining operations which cannot easily leave the state. Policymakers would have to evaluate the trade-offs associated with shifting to single sales factor apportionment, but if it could be done without sacrificing revenue (as has been the case in many states), it would help reduce the corporate income tax’s discouraging effect on in-state operations.

Individual Income Tax

Oklahoma’s individual income tax is a six-bracket graduated-rate tax which will feature a top rate of 4.75 percent, the result of rate reductions effective in 2022. This is a competitive rate, though Oklahoma faces stiff competition from neighboring Texas, which does not levy an individual income tax. The current system also imposes a marriage penalty, where married couples filing jointly face a modestly higher tax burden than if each filed separately. Cognizant of the competitive edge associated with lower—or no—individual income taxes, reforming or even eliminating the income tax has been a significant theme in Oklahoma public policy circles.

The Economic Implications of Income Taxes

Migration and National Trends

Nine states forgo broad-based individual income taxes, including neighboring Texas, which has seen its economy grow almost 35 percent faster than Oklahoma’s over the past two decades. In real (inflation-adjusted) terms, Texas’s gross state product soared almost 88.72 percent between 2004 and 2023, while Oklahoma’s economy increased a much more modest 54.47 percent, only slightly above the national average of 46.74 percent growth for the period. Gross state product is 33.94 percent higher per capita in Texas than in Oklahoma, and personal incomes are 51.72 percent higher.

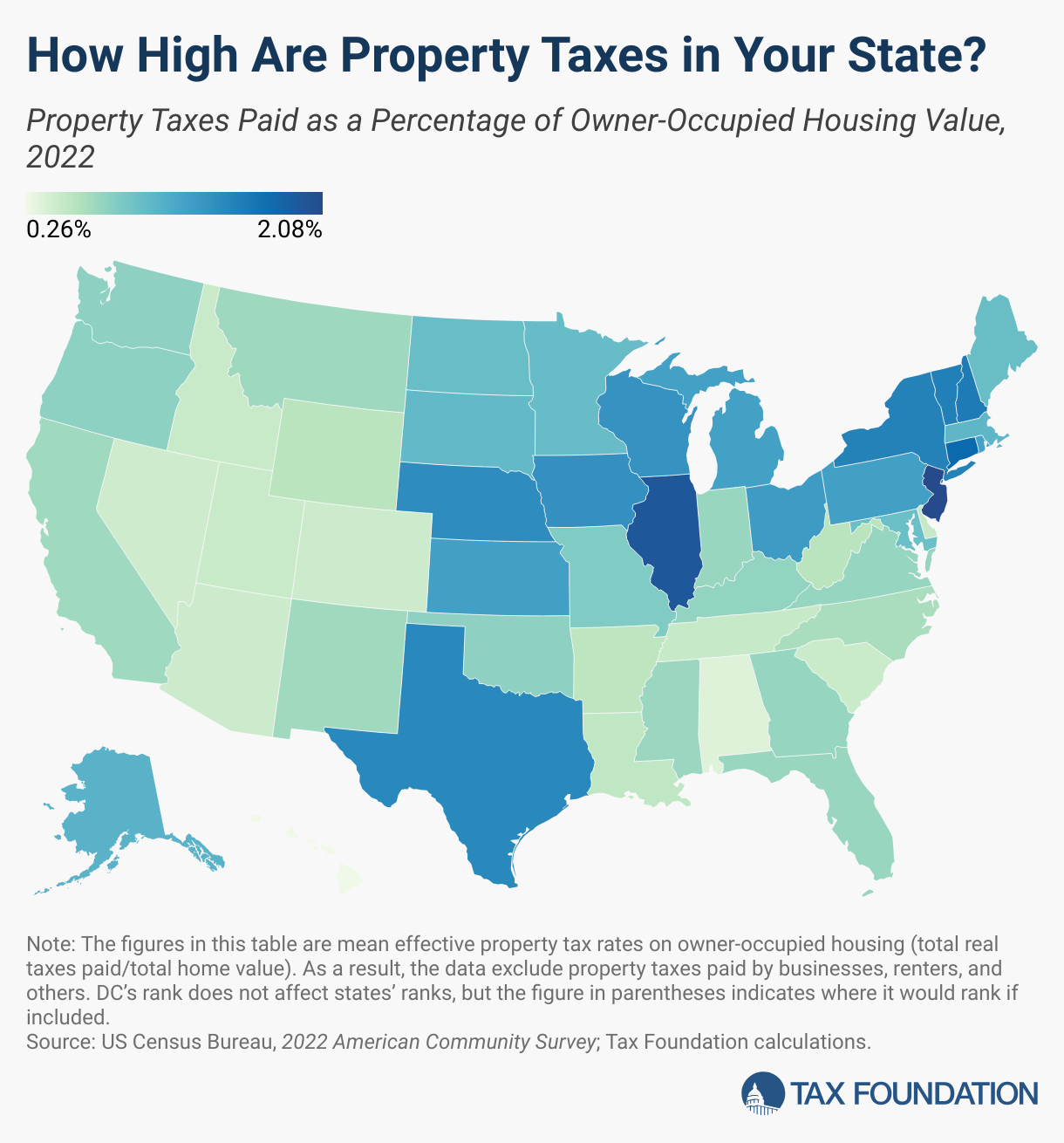

Texas is not an outlier in this regard. Recent history demonstrates states which forgo income taxes have seen their populations grow at marginally more (22.09 percent) than the national rate of 15.09 percent, and gross state product grew 13.77 percent faster in states without an income tax than it did in those with one over that period. In 2021 (the most recent year for which data are available), the 41 income tax states lost a net of 925,134 residents to the nine states without an income tax.[22] Oklahoma’s population has grown a modest 15.41 percent over the past two decades, less than one-third the national growth rate of 15.09 percent, while Texas’s population has burgeoned by 37.4 percent, well over twice the national rate. While income tax policy is hardly the only driver of economic activity in these states, it is little wonder that the Texas model—and that of other no- or low-income tax states—is highly attractive. And, in the case of Texas, population growth is occurring despite a relatively high property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. burden, especially compared to that of Oklahoma.

Oklahoma was among the 21 states cutting either their top or flat individual income tax rates in recent years, doing so from a place of moderate general fund revenue growth. Louisiana and Montana were, by far, the two states with the largest (double-digit) general fund revenue growth between FY 2021 and FY 2024. The remaining 19 states had an average revenue growth of 5.42 percent. This implies that Oklahoma was near the middle of the pack in terms of states which chose to cut individual income tax rates since it had an average growth rate of 5.96 percent during the same time period. From FY 2019 – FY 2021, seven of the 10 states which cut individual income taxes did so from double-digit biennial general revenue fund growth. More recently, states have been content with lower growth—but notably, every state which cut income tax top rates since 2021 still has higher (inflation-adjusted) tax revenue now than before the 2021 round of rate cutting began, even if sometimes only modestly.

Oklahoma’s income tax cut was modest, shaving a quarter of a percentage point off the state’s individual income tax rates starting in 2022, but it was also adopted amid economic growth that was slower than that experienced in some peer states.

Nearby, through a November 2024 special session, Louisiana enacted sweeping reform which included moving to flat rates for both individual, 3 percent, and corporate income, 5.5 percent, taxes. The state is attempting to stem the flow of out-migration by harnessing sound tax policy to attract and retain residents and businesses. Now, more than ever, Oklahoma faces significant regional competition outside of traditional rival Texas, and tax reform should become an even more urgent priority.

Table 3. States Cut Individual Income Taxes from Revenue Growth

General Fund Tax Revenue Growth Between FY 2021 and FY 2024

| State | Growth |

|---|---|

| Arizona | 0.72% |

| Arkansas | 0.45% |

| Colorado | 4.43% |

| Georgia | 8.82% |

| Idaho | 5.42% |

| Indiana | 3.53% |

| Iowa | 6.54% |

| Kentucky | 6.81% |

| Louisiana | 30.18% |

| Michigan | 7.89% |

| Mississippi | 3.94% |

| Missouri | 6.27% |

| Montana | 52.74% |

| Nebraska | 6.40% |

| New Hampshire | 5.14% |

| North Carolina | 5.60% |

| North Dakota | 7.57% |

| Ohio | 3.66% |

| Oklahoma | 5.96% |

| South Carolina | 7.60% |

| Utah | 8.73% |

| West Virginia | 5.41% |

Taxes are far from the only factor that influences location decision-making, but with job availability likely to become less salient as remote work arrangements increase in popularity, they are an important factor, and just as importantly, they are a factor that policymakers can control.

Comparison with Consumption Taxes

All taxes are not created equal. Any tax creates a certain amount of economic drag; this is unavoidable. There is truth to the adage that “whatever you tax, you get less of”—so it makes sense for policymakers to think carefully about what they choose to tax, and how. Individual income taxes fall on labor; on the margin, they lower the payoff to work, decreasing the supply of labor while increasing its cost.

An income tax can be conceptualized as a tax on consumption plus the change in savings, while a well-structured sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. is a tax on income less the change in savings (that is, on both the income spent now and on income saved to be spent in the future). An income tax reduces capacity for future consumption; economically, it acts like a sales tax that increases the cost of future consumption, with each additional hour of labor producing fewer goods in the future. Functionally, what this means is that income taxes penalize savings, while consumption taxes do not. Consumption taxes are much more economically neutral by comparison, and the economic literature consistently finds that sales taxes are less of an impediment to economic growth or location decisions than are income taxes.[23]

Consumption taxes do fall on suppliers of labor and capital, like income taxes, but they do so neutrally and—at least when well-designed—avoid double-taxing these factors. (Oklahoma, like all states, taxes some intermediate transactions in its sales tax, creating tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action. and diverging from the model of a pure consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible. .) Oklahoma’s sales tax is, appropriately, destination-sourced, meaning that the tax is imposed where a good or service is consumed, not where it is produced. Thus, unlike income taxes, the sales tax does not discourage investment or job creation.[24] This is, however, only true insofar as the tax falls on final consumption; when the tax falls on business inputs, it increases the cost of investing in-state.

Evidence of the adverse impact of individual income taxes has been documented at the local, state, federal, and even international level. In a series of Organisation for Economic Co-operation and Development (OECD) working papers, OECD-affiliated economists concluded that corporate income taxes are the most harmful to growth, followed by individual income taxes, while consumption and property taxes are less economically damaging. They found that a 1 percent shift of tax revenues from income taxes to consumption and property taxes would increase gross domestic product per capita by as much as 1 percent in the long run, and that income taxes were more strongly associated with lower incomes than were sales or consumption taxes.[25] A Canadian study, meanwhile, found that increases in sales taxes are generally associated with increases in economic growth, because they often replace income taxes and other taxes on investment.[26]

One interesting local tax study concluded that a 1 percentage point increase in a state individual income tax rate reduces annual population growth rates by 0.81 percentage points, while a similar 1 percentage point increase in local sales tax rates actually increases the annual growth rate by 0.83 percent,[27] evidently because residents favor the services provided by sales taxes more than they dislike the tax, whereas the opposite is true for local income taxes. The study’s authors also speculated that residents considered the sales tax to be more exportable, though the degree to which this is true may be greater for a locality than it is for a state.

Because a well-structured sales tax is more economically efficient than income taxes, using revenue from sales tax rate increases to pay down income tax rate reductions is economically competitive, as is generating revenue for the same purpose from sales tax base broadeningBase broadening is the expansion of the amount of economic activity subject to tax, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. Narrow tax bases are non-neutral, favoring one product or industry over another, and can undermine revenue stability. , provided that the base is broadened to previously untaxed final consumption and not to intermediate transactions.

Sales taxes also offer greater stability than income taxes, as can be seen in aggregate state tax collections during and immediately after the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. . By 2010, general sales taxes were down 8 percent from their 2008 peak, while individual income taxes fell 16 percent and corporate income tax collections plummeted a full 25 percent.[28] In Oklahoma in 2010, individual income tax collections were down 20 percent and corporate income tax receipts slipped 40 percent, while sales tax collections only declined 6 percent.[29]

The relative stability of sales taxes compared to income taxes was not unique to the Great Recession, and indeed, it makes logical sense. While most of us curtail some expenditures during an economic downturn, there is only so much we can—or are willing to—cut. Even those with no wage income continue to consume, supported by savings and governmental assistance, while those whose incomes decline are likely to reduce savings rates more drastically than consumption. Corporate income tax collections are the most volatile because, even in a deep recession, most individuals earn taxable income, whereas corporations may post actual losses and thus have no net income to tax.

Both income and consumption fall when the economy contracts, but not in tandem, with personal expenditures representing a greater share of income during a downturn. The coronavirus pandemic was the exception that proved the rule, however: sales tax collections were indeed stable, with revenues growing at a steady pace after an initial dip during stay-at-home orders. Rather than declining, however, income tax collections actually rose as fast or even faster than sales tax collections in many states, thanks to generous income infusions from the federal government which drove personal income to all-time highs. In the absence of such extraordinary intervention, consumption taxes provide a better buffer against the vicissitudes of the business cycle.

Impact on Pass-Through Businesses

Over 96 percent of all Oklahoma businesses are what is known as pass-through businesses, meaning that business income is taxed on (“passes through to”) the individual income tax returns of the owner or owners, rather than being taxed at the entity level like a traditional C corporation.[30] Pass-through businesses are often thought of as small businesses, but this is not entirely true. Most pass-through businesses are small businesses, but for that matter, most C corporations are as well. Over 99 percent of Oklahoma businesses meet the US Small Business Administration’s definition of a small business, and small businesses—the vast majority of which pay through the individual income tax—employ 51.1 percent of the state’s workforce.[31]

The individual income tax is therefore extremely important to businesses, because it is the tax that most businesses pay. And while the roughly 15,000 C corporations subject to the state’s corporate income tax[32] are also exceedingly important to the state’s economy, and punch substantially above their weight in share of the workforce, many of their suppliers and clients are subject to the individual income tax, so they too have a stake in lower individual income taxes.

Impact on Migration and Remote Work

Tulsa made waves as one of the first cities to offer a generous “move-in package” to attract newly mobile workers, extending $10,000 in cash and free access to coworking facilities to entice employees of out-of-state businesses who now have remote work flexibility. The Tulsa Remote program began before the pandemic, but its salience dramatically increased as remote work became increasingly possible because of—and extending beyond—the pandemic.[33] Such programs are not particularly scalable on a state level, and their local benefits have more to do with the marketing effect of growing a city’s brand and name recognition than they do in directly attracting residents through the incentive. However, local officials in Tulsa identified a very real phenomenon: a growing share of the workforce can now live anywhere with a high-speed internet connection, regardless of their employer’s location.

Traditionally, employees have been tied to specific geographies. When almost all work is performed in physical offices, an employer engaged in locational decision-making must find an equilibrium representing the optimal balance of a variety of often competing factors. They must balance costs of doing business (tax burdens, operating costs, regulatory costs, and labor costs) with access to a qualified workforce and quality of life considerations (schools, research universities, transportation systems, housing markets, cultural amenities) that are important to both executives and the workforce they want to attract. Depending on their business model, they may also need to be located close to clients, suppliers, or their customer base.

Simplify the decision, for a moment, to a question of attracting a qualified workforce. Certainly there are plenty of companies that could locate in Tulsa or Oklahoma City, and which the state of Oklahoma would love to attract to those locations. Tax policy is one way to bring in these employers. But for every business that is located elsewhere, there may still be some employees who would prefer to live in Oklahoma. Previously, that option was not available to them. The workforce balance that is optimal overall is never optimal for each individual. Some employees will gladly pay a premium for what more expensive cities have to offer, while others take little or no advantage of their amenities—even though they are paying for them through taxes and a high cost of living—and would far prefer a different arrangement. Traditionally, however, individual preferences are in tension with each other: a person may not appreciate any of the amenities they are paying for but appreciate working in a field which recruits heavily from people who do.

The rise of remote work changes the equation. To the extent that teams can operate virtually, employees can decide for themselves which bundle of amenities—priced in both cost of living and tax burdens—contribute to their quality of life and which do not, and choose where to live accordingly, knowing that their job will follow them there. Not everyone who takes advantage of this flexibility will do so in pursuit of financial savings. A highly compensated employee might abandon one high-cost, high-tax jurisdiction for another similarly costly locale because she prefers living in a resort destination to a major metropolitan area. Others, however, will move for lower taxes, a lower cost of living, or a higher (to them) quality of life—things that will often go together.

Oklahoma’s great challenge, of course, is its border with Texas, which forgoes an individual income tax. But Oklahoma does not need to go to zero to enhance its competitive standing. High property taxes are one of the trade-offs in Texas, where the effective tax rate on owner-occupied housing is almost twice Oklahoma’s rates (1.6 percent compared to 0.83 percent of market value).[34] With sufficiently low-rate income taxes, Oklahoma could be a highly attractive location for remote workers who care about low tax costs and a modest cost of living.

Reform Options

With a top rate of 4.75 percent, Oklahoma has the seventh-lowest rate among those states levying an individual income tax, and the 16th-lowest overall (counting states with no income tax).

This represents a continuation of efforts, dating to the late 1990s, to make the income tax more competitive, with many leading lawmakers—including multiple governors—articulating a vision of eventually eliminating it entirely. Governor Stitt recently urged lawmakers to enact “a half and a path,” a half point income tax cut and a path to elimination.[35]

Many policymakers want to build on these efforts of recent rate reductions. Lawmakers have a number of options in achieving this goal, including: (1) implementing a single-rate income tax, (2) enacting revenue triggers to phase in future rate reductions subject to revenue availability, (3) using sales tax base broadening to pay down income tax rate reductions, or even (4) converting the current income tax into a consumed income tax.

Implementing a Flat TaxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets.

Oklahoma currently imposes a six-bracket graduated-rate income tax, but the top rate (4.75 percent as of 2025) kicks in at $7,200 for single filers and $12,200 for joint filers. This means that the overwhelming share of all taxable income is exposed to the top marginal rate. The system is graduated, but the effect is relatively flat. The standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. of $6,350 (doubled for married filers) is considerably lower than the federal standard deduction ($15,000 in 2025), though Oklahoma does offer a $1,000 personal exemption per member of the household, which the federal government does not, and which provides a greater benefit to low-income households than the lower marginal rates. If all income were taxed at the top marginal rate without the benefit of lower brackets, a single taxpayer could face up to $189 in additional tax liability. However, if there were no standard deduction or personal exemption, a single filer’s liability could increase by $345.

The first five bracket widths are doubled for married couples filing jointly, but the top bracket kicks in at $12,200 for joint filers—$2,200 short of doubling the bracket width for single filers. This creates what is known as a marriage penalty, where joint filers have more income exposed to higher marginal rates than if the two were filing separately. That additional taxable income costs up to $95 in additional tax liability per household, which is not an enormous amount but still represents an inequity, particularly for lower-income households.

Eliminating the marriage penalty should be a goal of policymakers, but it comes at a cost: if the final bracket width were doubled, income tax revenues would decline by about $55 million. It is, however, possible that the state may eventually wish to absorb this loss to create fairer treatment of married couples, or to incorporate it into broader reforms, including the transition to a flat-rate income tax.

The economic literature on graduated-rate income taxes is unfavorable, since economic decision-making takes place on the margin—in this case, with regard to the top marginal rate, which is the relevant rate for most Oklahoma taxpayers, and for nearly all pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. activity. Furthermore, while recent rounds of rate reductions have yielded moderate rates, graduated-rate income taxes tend to be far easier to raise. When most or all taxpayers share in a tax increase, there is substantial political pressure to balance revenue needs with tax competitiveness. The ability to single out select taxpayers for higher rates—which will also fall on many small businesses—would make future tax increases easier. There are practical and political limits on how high a rate can go when it is applied uniformly, and these do not exist in the absence of a flat rate.

Fourteen states now have a flat rate income tax with six states adopting a flat rate between 2021 and 2024. North Carolina’s rate of 4.5 percent is the highest flat rate in the country. States like Illinois (4.95 percent) and Pennsylvania (3.07 percent), not known for a commitment to low taxes, have maintained low rates largely because of their flat-rate structure. Indeed, when Illinois lawmakers have sought to amend the state constitution to allow a graduated-rate tax, they have paired it with proposals that would, in some cases, yield double-digit top marginal rates. And whereas only Georgia has a flat tax with a rate higher than 5 percent (the state recently went to a flat tax and is in the process of phasing in rate reductions), states with graduated-rate income taxes have top rates as high as 13.3 percent in California, 10.9 percent in New York, 10.75 percent in New Jersey and the District of Columbia, 9.9 percent in Oregon, and 9.85 percent in Minnesota.[36] While Oklahoma would never adopt California-style rates, a flat-rate system would be an investment in keeping rates competitive for the long term.

Oklahoma could, for instance, adopt a higher standard deduction in exchange for a single-rate income tax. Increasing the standard deduction by $4,000, to $10,350, would not only bring the Oklahoma standard deduction closer to the federal one ($15,000 in 2025) but would also pull off a hat trick: providing tax relief for the lowest-income Oklahomans, ensuring that no one experiences a tax increase, and holding the revenue loss to what is effectively a rounding error.

This approach, moving to a flat-rate income tax with a 4.75 percent rate and a higher standard deduction, would not yield any significant immediate changes in tax liability, but it would help secure competitive rates going forward, providing a defense against high top marginal rates in the future. This competitive advantage could be locked in even more effectively if safeguarded by a constitutional amendment, as other states have. This reform could, of course, be adopted as a standalone policy or combined with revenue offsets or net tax cuts to reduce rates overall, which could make the plan even more attractive.

Reducing the Rate with Revenue Triggers

Oklahoma’s experience with revenue triggers was at most a qualified success. The state’s efforts to dedicate a share of future revenue growth to tax relief was complicated by a curious design which did a poor job of capturing actual revenue conditions. Properly designed triggers, however, would be a responsible way of returning a portion of future tax revenue growth with taxpayers in the form of lower income rates. This could stand alone or could complement other reforms.

Across the country, revenue triggers have emerged as an effective way to implement or phase in tax rate reductions or other tax reform measures as revenues permit. Tax triggers are a newer take on an old concept: contingent enactment of a legislative provision. States have long relied upon bills with contingent enactment clauses, providing that certain features of new legislation shall only be operative if certain conditions are met. Tax triggers build on this model, making tax reform measures contingent on state revenues meeting or exceeding established targets.[37]

Tax triggers can help ensure revenue stability and limit the uncertainty associated with changes to the tax code while providing an efficient way for states to dedicate some portion of revenue growth to tax relief. Their ability to do so, however, depends on their design. Poorly designed triggers can implement cuts when economic conditions do not warrant it or postpone reductions even when revenue growth would permit it. By contrast, properly constructed tax triggers are a valuable mechanism for providing meaningful rate relief.

Well-designed triggers require selecting a baseline revenue figure—either a given year’s revenue or a statutorily-established amount—and then establishing benchmarks that reflect meaningful revenue growth. While this may sound simple, Oklahoma and other states have learned that it is possible to get the benchmarks wrong.

Oklahoma’s previous triggers were designed to reduce the top marginal income tax rate from 5.25 percent to 4.85 percent in two stages. Ultimately, the second reduction was not implemented, and officials later lowered rates independently of the trigger. Notably, these triggers were based on year-over-year general fund balance projections, with each of the two stages of planned rate reductions implemented if thresholds were met. This approach had at least three shortcomings.

First, by focusing on single year revenue changes, Oklahoma opened itself up to the possibility of a downward ratchet effect, where recovery from a year of revenue decline could trigger a tax cut even if revenue levels are stagnant or even down over a longer time frame. For a variety of reasons, the COVID-19 pandemic did not yield the revenue losses many anticipated. Imagine, however, if revenues had slipped 5 percent rather than rising by a similar amount. If, the following year, revenues merely recovered to pre-pandemic levels, this would appear to be meaningful growth on a year-over-year basis, when it actually represents a revenue decline in real (inflation-adjusted) terms from a pre-pandemic baseline.

Second, it relied on projections rather than actual revenues. This was intended to make the triggers more forward-looking and aligned with the budget process, but the result was to divorce the process from real-world collections, merely looking at the change from one year’s projection to the next. Use the pandemic as an example once again. In the spring of 2020, state forecasts for the coming fiscal year were extremely pessimistic. In the spring of 2021, by contrast, most forecasts for FY 2022 were decidedly rosier. While revenues in FY 2022 are likely to be higher than FY 2021, comparing the two forecasts would yield a much sharper growth trajectory than would looking back at actual collections for each fiscal year.

And third, it was potentially subject to gamesmanship because it incorporated a fund balance component under which lawmakers could pre-authorize expenditures or divert funds to postpone otherwise scheduled tax cuts even in good years.[38]

Oklahoma can and should look at revenue triggers again, but with an emphasis on best practices. Instead of using year-over-year revenue changes, policymakers should establish a specific revenue baseline and employ benchmarks that measure real revenue growth, adjusted for inflation, over that base year amount. Ideally, reductions should not be tied to specific years, but instead triggered whenever real revenue growth is adequate to reduce rates by at least a given increment—say 10 or 25 basis points—with the actual size of the reduction based on a statutorily-established proportion of inflation-adjusted revenue growth.

There may, of course, also come a time when lawmakers determine that they have adequate revenues to implement an immediate tax rate reduction. Under a flat-rate tax with a $10,350 standard deduction, each percentage point of rate reductions would cost an estimated $875 million in current dollars, meaning that, for instance, adopting a flat 4 percent rate would forgo just under $660 million in lost revenue. Under the current graduated rate system with a lower standard deduction, an across-the-board rate reduction of one percentage point would cost just over $830 million.

Paying Down Rate Reductions with Sales Tax Modernization

With each passing year, Oklahoma’s sales tax becomes less representative of the state’s economy. Sales tax bases across the country are eroding as consumer spending patterns shift, so modernizing the sales tax base can generate revenue for income tax rate relief. Done properly, this is a win for taxpayers, as it reduces reliance on an uncompetitive tax by raising more money from a less damaging one, while creating a more neutral—and thus less inefficient—tax base for the sales tax by eliminating economically unsound carveouts and exclusions. Policymakers should, however, avoid the temptation to chase a rate—or the elimination of the individual income tax—if it means making unsound choices about base broadening. Highly significant reforms are possible even on an incremental basis.

A responsible expansion of the sales tax base, as enumerated elsewhere in this publication, could yield a 3 percent top marginal income tax rate without adjusting current sales tax rates. Further cuts could be achieved using a combination of base broadening and rate increases.

However, while reducing income tax burdens by shifting further toward consumption taxes is not only viable but desirable, full repeal of the individual income tax through a broader sales tax base, higher rates, or both would yield potentially unpalatable sales tax rates. Expanding to a broad, but still attainable, range of currently untaxed goods and services—outlined in the discussion of sales tax reform options—would generate about $732 million, enough to pay for an across-the-board rate reduction yielding a new top rate of about 3.87 percent.

If, moreover, local sales tax rates could be adjusted to make local collections revenue neutral on the new base, base broadening could pay for about a 2.3 percent top marginal income tax rate while aggregate sales tax rates remain identical—a higher state rate, but lower local rates, commensurate with the broader base on which revenue can be raised.

This is highly competitive, since the only seven states with income tax rates below 4 percent are Arizona (2.5 percent), Arkansas (3.9 percent), Indiana (3 percent), Louisiana (3 percent), North Dakota (2.5 percent), Ohio (3.5 percent), and Pennsylvania (3.07 percent), among the 41 states that impose wage income taxes.

But to zero out the income tax using this broader base, the state sales tax rate would have to increase substantially, from 4.5 percent now to about 8.3 percent. While an 8.3 percent state sales tax rate is high, it can be competitive in the proper environment—but less so in Oklahoma, where it would be combined with local option sales taxes which are quite high in their own right. Even with a broader base, Oklahomans would be looking at a combined average state and local sales tax rate of 10.8 percent to fully offset the elimination of the individual income tax if local sales tax rates were adjusted to reflect the expanded base, and 11.8 percent if they were not. The latter rate, in particular, is likely to be considered prohibitively high. Such a rate would likely induce additional cross border sales, and businesses which face sales taxes on their business-to-business transactions would be at a competitive disadvantage compared to their out-of-state peers.

If, instead, the sales tax base were broadened to include nearly all final consumer transactions—including things like health care and education, to the extent that they are legally taxable under federal law and regulations—the new combined sales tax rate would be about 11.8 percent (or 10.8 percent without a local adjustment), similar to the current (temporary) high of 10.12 percent in Louisiana and on a much broader base. And replacing the income tax with higher sales tax rates alone, in the absence of any base broadening, would require an entirely unrealistic all-in rate of 13.9 percent.

A prior effort to broaden the sales tax base to pay down reforms elsewhere gained little traction, with former Gov. Mary Fallin (R) proposing expansions that relied heavily on the taxation of intermediate transactions,[39] leading to tax pyramiding that would undercut the competitiveness of in-state businesses and lead to Oklahomans—particularly lower- and middle-income Oklahomans—paying the same tax several times over in some of their purchases.

It is crucial that policymakers avoid this mistake in considering sales tax base broadening as a way to pay down income tax rate reductions. There are responsible ways to broaden the base—but lawmakers should avoid the temptation of seeing every sales tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. as a potential revenue-raiser. Some exemptions are structurally necessary to avoid tax pyramiding. The ideal base is final consumption, so the exclusion of business inputs should not be deemed a carveout; it is, rather, consistent with the definition of consumption taxation.

Instead of the distraction of trying to identify sales tax base-broadening options to eliminate the income tax, policymakers could prioritize a more incremental—but still highly significant—reform, using sales tax base broadening to facilitate an across-the-board income tax cut, building on reforms adopted in 2021 to make Oklahoma’s income tax rates among the lowest in the country. The sales tax base-broadening options to pay for these reductions are delineated in our discussion of sales tax reforms.

The following table assumes that the full set of reasonable expansions to the sales tax base laid out in our discussion of the sales tax are adopted and looks at the revenue-neutral sales tax rate necessary to implement across-the-board rate reductions bringing the top income tax rate to 4 percent, 3 percent, 2 percent, and 1 percent, or to repeal it entirely. The sales tax rates necessary to achieve these targets using the current base are also included, starting from the current average combined state and local sales tax rate of about 9.01 percent. Finally, this analysis assumes that local option sales tax rates are proportionally reduced to make base broadening revenue neutral at the local level (options for doing so are discussed elsewhere), but a separate line is provided using the assumption that local sales tax rates remain the same, yielding increased revenue for localities.

Table 4. Sales Tax Rates to Achieve Income Tax Reduction Targets

| Income Tax Top Marginal Rate Target | ||||||

|---|---|---|---|---|---|---|

| Assumption | Current | 4% | 3% | 2% | 1% | 0% |

| Current Sales Tax Base | 9.0% | 9.8% | 10.8% | 11.8% | 12.9% | 13.9% |

| Modernized Sales Tax Base | ||||||

| — without local adjustment | 8.0% | 8.6% | 9.4% | 10.2% | 11.0% | 11.8% |

| — with local adjustment | 7.0% | 7.6% | 8.4% | 9.2% | 10.0% | 10.8% |

Notably, Oklahoma could achieve a top individual income tax rate of 3 percent without any change in sales tax rates if it right-sized its sales tax base as recommended elsewhere in our analysis.

Adopting Nonresident Filing and WithholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount of the employee requests. Exemptions

Oklahoma’s current treatment of nonresident earned income could be improved by implementing low-cost, simplifying reforms to its employee filing and employer withholding thresholds.

At present, Oklahoma requires nonresident individuals who earn $1,000 or more in any calendar year from Oklahoma sources to file a state income tax return. Employers must withhold state income tax if a nonresident employee earns over $300 in a calendar quarter for services performed within Oklahoma. The state’s neighbors aren’t much better, though New Mexico allows 15 days before employer withholding is required.

Thirteen states, however, offer more generous thresholds—and their number is growing. Thresholds can be denominated in days, in-state earnings, or both, though days in-state is preferable. For instance, Indiana and West Virginia recently exempted nonresident employees from state income tax filing and withholding requirements if they work in the state for 30 days or less within a calendar year, while Louisiana recently adopted a 25-day threshold. These policies reduce administrative and compliance burdens for taxpayers with little in-state liability.

Adopting a 30-day filing and withholding threshold in Oklahoma could offer several benefits. It would simplify tax compliance for nonresident workers who have only short-term assignments in the state, potentially making Oklahoma a more attractive destination for conferences and for businesses which require occasional in-state travel. It also reduces compliance costs dramatically, and eliminates the administrative burden of processing returns with negligible liability. For many filers who only spend a few days in-state, the cost of filing an additional state return can far exceed the amount owed.

Creating a Consumed Income Tax

Many economists have championed the idea of a consumed income tax as a replacement for the individual income tax. Such a tax would only apply to income used for consumption, excluding savings and thus eliminating the economic disadvantages inherent in traditional income taxation. An ideal consumed income tax would exclude all saved and invested income from the base until it is withdrawn from savings and used for consumption. This addresses the current income tax’s bias against investment and reduces its adverse effect on labor.

An ordinary income tax reduces the return on invested income twice, while reducing the returns to consumption only once, creating a bias against investment and, at the margin, reducing the incentive for work generating income above consumption levels. This issue is compounded by the effects of inflation, since the taxpayer will be taxed on nominal investment returns even if they reflect losses or low returns in real terms. A consumed income tax, by contrast, would not tax income while it is being invested, only when it is spent.

In practice, a state-level consumed income tax would likely require the creation of a state-recognized universal savings account through which taxpayers could save and invest, and where income would be exempt until withdrawn. In this way, it would be much like other tax-advantaged investment vehicles well-known to taxpayers, like IRAs and 401(k)s, except that there would be no contributions limit and no penalty for withdrawals—other than the imposition of tax when income is withdrawn to be spent.

To raise the same amount of revenue as the current income tax, a consumed income tax rate would have to be higher, since it operates on a narrower base. Oklahomans saved roughly $12.6 billion in 2018,[40] suggesting that the revenue neutral rate for a consumed income tax would be about 5.4 percent, compared to the 4.75 percent rate of the current income tax as of 2022. While this rate is higher, the tax base is much more economically efficient, as it does not discriminate against savings and investment the way the current income tax does.

Sales Taxes

Oklahoma’s reliance on the sales tax is slightly higher than average: the state brings in just under a third of its state and local tax collections from the sales tax, while most states rely on sales taxes for just under a quarter of collections. At issue is not the state sales tax, with its modest 4.5 percent rate on a fairly ordinary base, but rather local sales taxes, with rates that often rival the state rate. Sales taxes accounted for only 13.5 percent of local tax collections nationwide in 2022 but made up 40.2 percent of local collections in Oklahoma that same year.[41]

As addressed elsewhere, this heavy reliance on the sales tax can be partially explained by the limited number of local government entities given authority to levy property taxes (called the ad valorem tax in Oklahoma). Additionally, sales tax is an attractive way for localities to raise revenue, because it creates a possibility for some of the tax burden to be outsourced to those who shop across district lines.

This higher reliance is reflected in higher rates. The state-level rate is below average at 4.5 percent, but when combined with local rates, the average Oklahoman faces rates of 9.0 percent, the sixth-highest combined rate in the country. Oklahoma has remained in an unenviable position for many years, only moving from fifth to sixth due to other states increasing their rates, rather than any effort on Oklahoma’s part to lower the sales tax burden.

Table 5. Sales Tax Rates, Oklahoma and Bordering States

| State | State Rate | Average Local Rate | Combined Rate |

|---|---|---|---|

| Oklahoma | 4.50% | 4.51% | 9.01% |

| Arkansas | 6.50% | 3.06% | 9.56% |

| Colorado | 2.90% | 4.15% | 7.05% |

| Kansas | 6.50% | 2.05% | 8.55% |

| Missouri | 4.23% | 9.42% | 7.16% |

| New Mexico | 5.13% | 1.97% | 7.09% |

| Texas | 6.25% | 1.06% | 7.31% |

Neighboring Arkansas does experience a far higher average rate of 9.56 percent, but Oklahoma still surpasses most of its neighbors and compares unfavorably with rates throughout the rest of the country. The limited reach of the property tax plays a major role in these rates, but a modest sales tax base, combined with below-average per capita personal consumption, is at play as well. Modernizing the sales tax base and using revenue from base broadening to pay down income tax rate reductions at the state level and local option sales tax rate reductions at the municipal level, is a compelling way to address this issue.

Oklahoma’s Sales Tax Base Is Narrow and in Need of Modernization

Like most states, Oklahoma imposes its sales tax on a base that consists of most goods and relatively few services. With limited exceptions, the state’s sales tax is imposed on transactions involving tangible property—appliances but not apps, light fixtures but not landscaping. As is often the case, this was less of a conscious choice than an accident of history, a relic of the fact that Oklahoma’s sales tax was first imposed in 1933, at the height of the Great Depression. Services comprised a far smaller share of the economy, and it was administratively simpler in that earlier era to focus almost exclusively on retail sales of goods.

Today’s economy has little in common with that of 1933 or even 1993. Higher incomes and changing consumer tastes have shifted a greater share of consumption to services, while a digital economy is upending traditional categories. Not only does more disposable income go to the consumption of services, but some traditional consumption of goods has been displaced by services and subscriptions.

Oklahoma’s sales tax base is not as narrow as some of its peer states’ bases, but it remains narrow—and erodes further each year. In 2024, Oklahoma exempted groceries from the state sales tax. While politically popular, such narrowing of the sales tax base makes other reform efforts, like rate reductions, more difficult. Apples-to-apples comparisons of state sales tax bases are difficult, but one method is to calculate the value of taxed transactions as a percentage of personal income. Hawaii, for instance, has a sales tax breadth of 119 percent of state income.[42] The state exempts some transactions which arguably should be taxed, but double-taxes others. Oklahoma also exposes some transactions to multiple levels of taxation but omits far more transactions altogether. The state’s sales tax breadth, as a percentage of state income, is 36 percent.

Table 6. Sales Tax Breadth as a Percentage of Personal Income (FY 2022)

| State | Breadth |

|---|---|

| Oklahoma | 34% |

| Arkansas | 43% |

| Colorado | 34% |

| Kansas | 34% |

| Missouri | 30% |

| New Mexico | 76% |

| Texas | 43% |

A robust sales tax base would not reach 100 percent, as not all income is consumed in any given year, but, per personal consumption data, should be about 73 percent of state income in Oklahoma, suggesting that the state is only reaching half of its sales tax base potential.

The state’s sales tax breadth has seen a substantial decline over time. It saw an especially steep drop in the 1980s, reflecting rising incomes, growth of interstate sales, and an accelerating shift toward the consumption of services. Oklahoma has taken action to collect more taxes on online sales, but there is an opportunity to build on that change with broader efforts to stabilize the tax base.

Oklahoma Should Right-Size its Sales Tax Base

As Oklahoma’s sales tax base continues to shrink as a share of total personal consumption, the state has three choices: accept reduced revenue, raise sales tax rates, or shift collections to other taxes. Instead of increasing rates on a narrow base, lawmakers should consider broadening the base itself. Right-sizing the sales tax base would make the tax more neutral in its application, while generating additional state and local revenue that could be used to reduce reliance on more unstable or economically harmful taxes.

In this search for a more modern sales tax base, policymakers should keep in mind several main principles and features of sales taxation that are broadly accepted by public finance scholars and tax policy researchers across the board, namely:

- An ideal sales tax is imposed on all final consumption, both goods and services;

- An ideal sales tax exempts all intermediate transactions (business inputs) to avoid tax pyramiding;

- Sales taxes should be destination-based, meaning that tax is owed in the state and jurisdiction where the good or service is consumed;

- The sales tax is more economically efficient than many competing forms of taxation, including the income tax, because it only falls on present consumption, not saving or investment;

- Because lower-income individuals have lower savings rates and consume a greater share of their income, the sales tax can be regressive, though broadening the base to include additional consumer services (much more heavily consumed by higher-income individuals) represents a progressive change;