Key Findings

- Many provisions of the One Big Beautiful Bill Act (OBBBA) flow through to state taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. codes through their conformity with the Internal Revenue Code.

- Incorporation of these provisions depends both on the currentness of a state’s conformity and whether the state incorporates, decouples from, or modifies each specific federal provision.

- The new or enhanced personal deductions (the temporarily higher standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. for seniors and the temporary deductions for qualified tips, car loan interest, and overtime premium pay) each flow through to some or all of the seven states that begin with federal taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. .

- Eighteen states’ property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. deductions will increase in line with the higher federal state and local tax deductionA tax deduction allows taxpayers to subtract certain deductible expenses and other items to reduce how much of their income is taxed, which reduces how much tax they owe. For individuals, some deductions are available to all taxpayers, while others are reserved only for taxpayers who itemize. For businesses, most business expenses are fully and immediately deductible in the year they occur, but others, particularly for capital investment and research and development (R&D), must be deducted over time. (SALT) cap.

- The restoration of full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for machinery and equipment under § 168(k) is slated to impact 17 states, a higher § 179 cap for small business expensing will flow through to 38, and the restoration of § 174 research and development expensing and the creation of a new § 168(n) cost recoveryCost recovery refers to how the tax system permits businesses to recover the cost of investments through depreciation or amortization. Depreciation and amortization deductions affect taxable income, effective tax rates, and investment decisions. provision for certain structures will show up in virtually all states’ tax structures.

- Within the international tax regime, the transition from a tax on global intangible low-taxed income (GILTI) to one on net CFC-tested income (NCTI) makes continued state conformity to the provision less tenable, as states only incorporate an incoherent patchwork of the regime’s provisions.

- Beginning in FY 2028, new limitations on Medicaid provider taxes will reduce states’ federal matching funds.

- While many of the temporary provisions confer very little economic benefit, the restored and enhanced business expensing provisions are pro-growth, represent sound tax policy, and merit incorporation into state tax codes.

- Up-to-date conformity has many practical benefits for taxpayers and tax administrators alike; it is better to decouple from specific provisions than to pause conformity.

- This paper indicates which states conform to each relevant tax provision and provides estimates of the revenue impacts of conformity.

Introduction

For Congress, work on the One Big Beautiful Bill Act (OBBBA) is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code (IRC) conformity date in others.

Most states use the IRC as the basis of their own individual and corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. codes, so changes to the federal tax code can adjust state tax codes as well. But all states decouple from certain IRC provisions and modify others, and states vary on how current their alignment with the IRC is. While some states automatically conform to the current version of the federal code, others conform to it as it existed at some earlier date and thus may not bring in the new provisions for quite some time, if ever.

Provisions that at least potentially flow through to states include personal tax changes like the new deductions for qualified tips, overtime premium pay, and automobile loan interest; the higher standard deduction; the permanently higher alternative minimum tax (AMT) threshold; the higher estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs. threshold; and the $1,000 charitable deduction for non-itemizers. For business taxpayers, provisions with relevance to state tax codes include new first-year expensing provisions under § 168(k), § 174, § 179, and the new § 168(n); the conversion of the global intangible low-taxed income (GILTI) regime to the net CFC-tested income (NCTI) regime; and the reinstatement of EBITDA (earnings before interest, taxes, depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. , and amortization) for calculation of the net interest deduction limit. Additionally, while not a matter of IRC conformity, the new federal law obligates future changes to most states’ Medicaid provider taxes.

For each provision, incorporation of the federal tax change into states’ own individual and corporate income tax codes is governed by a two-part test:

- Is the state’s tax code written in such a way that, if and when the state code is conformed to a post-OBBBA version of the IRC, it would incorporate the provision? Some states expressly decouple from the relevant IRC sections, and a few states have limited, highly selective incorporation of the IRC.

- Assuming the provision would be incorporated, does the state have rolling conformity, and thus automatically align its own tax code with the most recent version of the IRC, or does it have static (fixed date) conformity, where the incorporation of these changes would await the legislature’s decision to manually update the state’s IRC conformity date? In some static conformity states, moreover, the conformity date is almost always current, with lawmakers updating it as a matter of routine, whereas in others, lawmakers have allowed it to fall out of date. While a prior commitment to currentness is no guarantee of future conformity updates following the passage of the OBBBA, states with near-current fixed date conformity are more likely to incorporate the new provisions than those that have not updated their conformity dates in years.

These changes confront lawmakers with choices. They must decide whether to maintain or adopt conformity with a post-OBBBA version of the IRC, and, if so, whether to modify or selectively decouple from some of the new provisions. The benefits of general conformity are considerable for taxpayers and tax administrators alike—a point in favor of maintaining currentness. That, however, does not resolve the question of whether to diverge from certain new federal policies. This analysis provides estimates of the costs of conformity to each provision by state, where possible, along with an analysis of the purpose and effects of each policy. Some changes reduce tax collections with scant economic benefit while providing poorly targeted relief, and might well be discarded by lawmakers. Others represent pro-growth improvements to the tax code, and many lawmakers might find that their costs—often quite modest—are well worth absorbing.

None of these decisions, however, should be made in the absence of good information. This publication is intended to help lawmakers and those in the broader policy community navigate these issues and determine the best course for their respective states.

General Conformity

While each state’s tax code is different, most share a common starting point: the Internal Revenue Code. States conform to provisions of the federal tax code for a variety of reasons, largely focused on reducing compliance and administrative burdens of state taxation. Conformity allows state administrators and taxpayers alike to rely on federal statutes, rulings, and interpretations, which are generally more detailed and extensive than what any individual state could produce. It provides consistency of definitions for those filing in multiple states and reduces duplication of effort in filing federal and state taxes. It permits substantial reliance on federal audits and enforcement, along with federal taxpayer data. It helps to curtail tax arbitrage and reduce double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. . For the filer, it can make things easier by allowing the filer to copy lines directly from their federal tax forms. Federal conformity represents a case of “delegating up,” allowing states to conserve legislative, administrative, and judicial resources while reducing taxpayer compliance burdens.[1]

No state, however, adopts the IRC outright. Every state modifies it in various ways—with additions and subtractions, by decoupling from certain IRC provisions, and through discrete state-specific tax provisions. States also vary in whether they always conform to the IRC in its current form, or whether they conform to a version specified by the legislature. This is, of course, highly relevant in the wake of the OBBBA’s enactment.

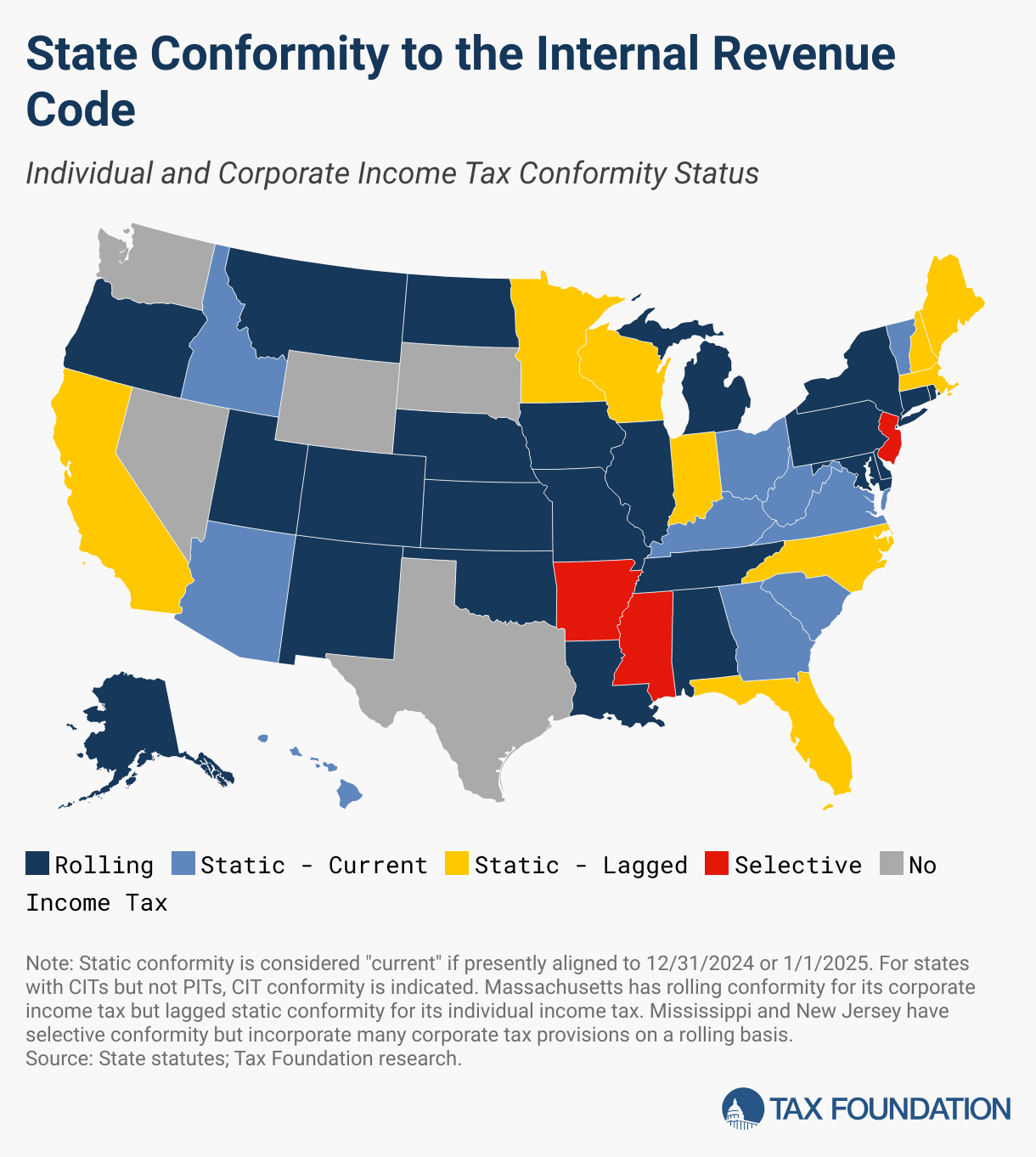

For individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. purposes, 20 states and the District of Columbia have rolling conformity, automatically aligning with the current version of the IRC. Seventeen states have static (fixed date) conformity, 10 of which are, as of the enactment of the OBBBA, conformed to a version of the IRC as it existed on either December 31, 2024, or January 1, 2025. In these states, updating conformity dates is largely a pro forma exercise even though it requires a vote of the legislature, though it is of course possible that lawmakers may consider the annual update less rote in the wake of the OBBBA’s enactment. Another four states have “selective” conformity, largely designing their own income tax codes and only conforming to select IRC provisions. Finally, nine states forgo a broad-based income tax.

Most states with individual income taxes use adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, including inventory and certain labor costs. (AGI) as their income starting point. However, seven states—Colorado, Idaho, Iowa, Montana, North Dakota, Oregon, and South Carolina—begin with federal taxable income, which exposes those states to the inclusion of new deductions that would not automatically flow through to other states.

Twenty-six states and the District of Columbia have rolling conformity for their corporate income tax, including two states that technically have selective conformity but begin their own calculations with the IRC’s calculation of taxable income before net operating loss deduction and special deductions, which, for OBBBA purposes, is tantamount to conformity. Eighteen states have static conformity, one is truly selective, and five states go without corporate income taxes.[2] Of states with static conformity, 10 are essentially up to date, aligning with the latest pre-OBBBA version of the IRC, and under ordinary circumstances could be reasonably expected to undergo an annual update in the 2026 legislative sessions.

Table 1. State Tax Conformity with the Internal Revenue Code

| State | PIT Conformity | CIT Conformity |

|---|---|---|

| Alabama | Rolling | Rolling |

| Alaska | No PIT | Rolling |

| Arizona | Static - Current | Static - Current |

| Arkansas | Selective | Selective |

| California | Static - Lagged | Static - Lagged |

| Colorado* | Rolling | Rolling |

| Connecticut | Rolling | Rolling |

| Delaware | Rolling | Rolling |

| District of Columbia | Rolling | Rolling |

| Florida | No PIT | Static - Lagged |

| Georgia | Static - Current | Static - Current |

| Hawaii | Static - Current | Static - Current |

| Idaho* | Static - Current | Static - Current |

| Illinois | Rolling | Rolling |

| Indiana | Static - Lagged | Static - Lagged |

| Iowa* | Rolling | Rolling |

| Kansas | Rolling | Rolling |

| Kentucky | Static - Current | Static - Current |

| Louisiana | Rolling | Rolling |

| Maine | Static - Lagged | Static - Lagged |

| Maryland | Rolling | Rolling |

| Massachusetts | Static - Lagged | Rolling |

| Michigan | Rolling | Rolling |

| Minnesota | Static - Lagged | Static - Lagged |

| Mississippi | Selective | Rolling |

| Missouri | Rolling | Rolling |

| Montana* | Rolling | Rolling |

| Nebraska | Rolling | Rolling |

| Nevada | No PIT | No CIT |

| New Hampshire | No PIT | Static - Lagged |

| New Jersey | Selective | Rolling |

| New Mexico | Rolling | Rolling |

| New York | Rolling | Rolling |

| North Carolina | Static - Lagged | Static - Lagged |

| North Dakota* | Rolling | Rolling |

| Ohio | Static - Current | Static - Current |

| Oklahoma | Rolling | Rolling |

| Oregon* | Rolling | Rolling |

| Pennsylvania | Selective | Rolling |

| Rhode Island | Rolling | Rolling |

| South Carolina* | Static - Current | Static - Current |

| South Dakota | No PIT | No CIT |

| Tennessee | No PIT | Rolling |

| Texas | No PIT | No CIT |

| Utah | Rolling | Rolling |

| Vermont | Static - Current | Static - Current |

| Virginia | Static - Current | Static - Current |

| Washington | No PIT | No CIT |

| West Virginia | Static - Current | Static - Current |

| Wisconsin | Static - Lagged | Static - Lagged |

| Wyoming | No PIT | No CIT |

Note: For static conformity states, “current” indicates that the state conforms to the IRC as it existed immediately pre-OBBBA, aligned with either the December 31, 2024, or January 1, 2025, version of the code.

Source: State statutes; Bloomberg Tax; Tax Foundation research.

Personal Deductions

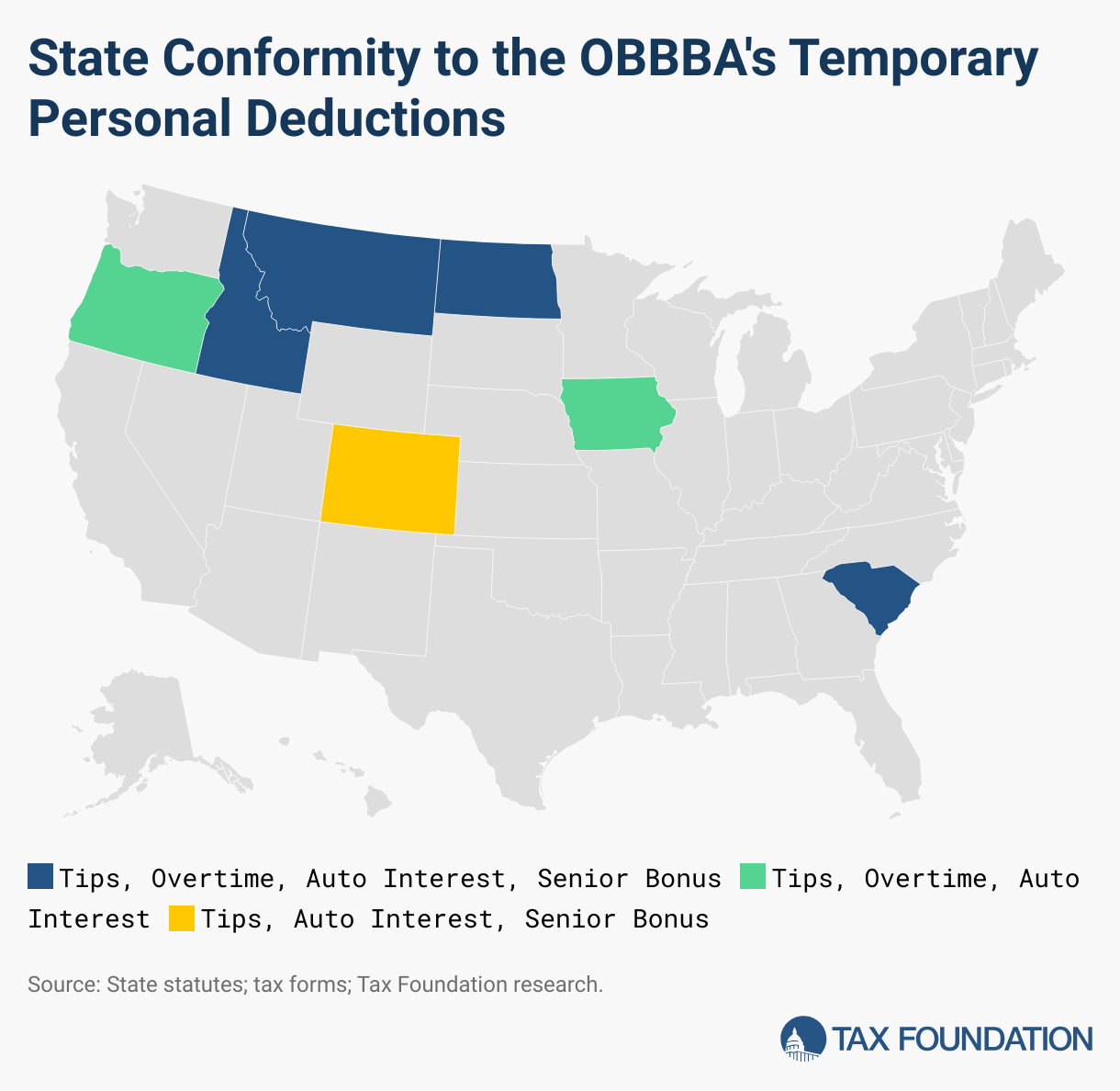

The OBBBA implements a range of tax changes for individual taxpayers, many of which have implications for state tax systems. These provisions include making the higher standard deduction permanent and increasing the enhanced deduction for seniors; raising the state and local tax (SALT) deduction cap to $40,000, subject to a phasedown for high earners; and adopting three temporary deductions: for car loan interest, qualified tips, and overtime premium pay. The higher standard deduction flows through to nine states and the District of Columbia (indicated in Table 2), either because they use federal taxable income as their income starting point or conform separately to the federal standard deduction. The higher SALT deduction cap has implications for 18 states that derive their own deductions for local property taxes from the federal deduction. Finally, the three temporary deductions are only in line to flow through to the seven states that conform to federal taxable income.

Standard Deduction and Temporarily Higher Senior Deduction

With the reconciliation bill’s enactment, the higher standard deduction levels established under the Tax Cuts and Jobs Act (TCJA) are made permanent, with a temporary $6,000 enhancement of the deduction for qualified senior citizens for tax years 2025-2028. Ten states (Arizona, Colorado, Idaho, Iowa, Missouri, Montana, New Mexico, North Dakota, South Carolina, and Utah) and the District of Columbia conform to the federal standard deduction—or, in the case of Utah, incorporate it into a state-specific credit calculation—and thus are in line to retain these higher standard deductions as well. This comes at a cost compared to allowing the higher standard deduction to expire, but it does not impose any additional cost beyond the ongoing inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. adjustment compared to current policy.

Although six states currently conform to the additional standard deductions available for seniors and the blind, the additional temporary $6,000 deduction for qualified senior citizens is separate from this existing provision, as it is drawn to the IRC section dealing with personal exemptions, which were otherwise eliminated as of the enactment of the TCJA.

While many states use the number of federal personal exemptions to provide their own personal exemptions, four of the states that begin with federal taxable income—Colorado, Idaho, North Dakota, and South Carolina—appear in line to bring in the new bonus deduction for seniors, which phases out above $75,000 in income for single filers and $150,000 for joint filers.

Because Idaho and South Carolina have static conformity, this change would only take place once their conformity date is updated. Revenue losses across these states run an estimated $367 million. Additional details can be found in Table 2.

No Tax on Tips

Consistent with one of President Trump’s campaign pledges, OBBBA exempts qualified tips from income taxation for tax years 2025-2028, structured as a deduction available to itemizers and non-itemizers alike. To limit tax avoidance, a qualified tip is defined as a cash tip received as an individual in an occupation “which traditionally and customarily received tips on or before December 31, 2024,” with exclusions for highly compensated employees. Only states that begin their income tax calculations with federal taxable income rather than adjusted gross income incorporate this exemption automatically. However, the policy has been introduced through legislation in numerous states, despite the tax benefit being poorly targeted. Among workers in the bottom half of hourly wages, only 4 percent are in tipped professions.

Across the seven conforming states, we estimate an aggregate impact of $124 million in 2026. Implementing the policy nationwide would cost an estimated $1.5 billion per year (see Table 2). Our estimates show a $0 impact for North Dakota even though the state would be in line to incorporate the provision and thus experience some amount of revenue loss, because we estimate revenue effects by applying the blended state rate applied to taxable income of $20,000 – $40,000, and North Dakota’s lowest rate (1.95 percent) does not kick in until $48,475 in taxable income above the state’s federal (currently $15,000) standard deduction.

No Tax on Car Loan Interest

Under the budget bill, personal passenger vehicle loan interest is deductible up to $10,000 per year, with a phaseout for high earners beginning at $100,000 in income ($200,000 for joint filers). Initially, under the House bill, this provision reduced AGI and thus flowed through to most states. As enacted, however, it reduces federal taxable income, like the deductions for tips and overtime pay, and thus only flows through to five states. We estimate that it would reduce tax collections by $213 million across the seven conforming states, and if all states adopted this provision, the annual cost would run about $2.36 billion (see Table 2).

No Tax on Overtime Premium Pay

The new law makes the premium portion of overtime deductible for both itemizers and non-itemizers for tax years 2025-2028, with some exclusions, such as for highly compensated employees. As with the other temporary deductions, this provision would only flow through automatically to the states that use federal taxable income as their income starting point, excluding Colorado, which decoupled from the provision preemptively. In Idaho and South Carolina, the provision would only apply when the state updates its fixed conformity date. Across these six states, exempting the premium portion of overtime could generate losses of $793 million in 2026, and if all income taxing states adopted a similar exemption, the annual cost would exceed $11 billion (see Table 2). The actual cost could be even higher, because the preferential treatment of overtime would create incentives to shift more work to premium overtime rather than hiring additional workers, and might also lead workers to find creative ways to characterize more of their income as qualifying overtime pay.

Table 2 shows estimated costs for each provision if a state were to adopt it, with amounts in bold where a state—subject to a conformity update, where applicable—would be in line to do so based on current law. States with such impacts are Idaho ($167 million), Iowa ($134 million), Montana ($67 million), North Dakota ($29 million), Oregon ($419 million), and South Carolina ($521 million).

Table 2. State Income Tax Costs of OBBBA Temporary Personal Deductions

In Millions of Dollars, Tax Year 2026

| State | Tips | Overtime | Auto Interest | Senior SD Bonus | Possible | Incorporated |

|---|---|---|---|---|---|---|

| Alabama | $22.9 | $177.9 | $57.9 | $119.6 | $378.4 | $0.0 |

| Alaska | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Arizona | $25.8 | $135.8 | $39.9 | $96.3 | $297.7 | $0.0 |

| Arkansas | $10.4 | $82.0 | $26.7 | $56.5 | $175.7 | $0.0 |

| California | $216.9 | $3,012.2 | $566.2 | $1,326.6 | $5,121.9 | $0.0 |

| Colorado | $49.0 | $208.7 | $42.6 | $126.6 | $426.9 | $377.9 |

| Connecticut | $23.5 | $171.3 | $26.0 | $111.9 | $332.7 | $0.0 |

| Delaware | $9.0 | $47.1 | $5.3 | $44.9 | $106.4 | $0.0 |

| District of Columbia | $21.3 | $47.1 | $15.8 | $16.2 | $100.4 | $0.0 |

| Florida | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Georgia | $71.3 | $407.8 | $146.0 | $237.5 | $862.6 | $0.0 |

| Hawaii | $24.3 | $69.0 | $15.6 | $68.1 | $176.9 | $0.0 |

| Idaho | $10.7 | $78.7 | $18.8 | $59.3 | $167.4 | $167.4 |

| Illinois | $83.8 | $514.3 | $98.5 | $325.8 | $1,022.3 | $0.0 |

| Indiana | $21.1 | $181.1 | $34.3 | $123.5 | $360.0 | $0.0 |

| Iowa | $10.3 | $104.3 | $19.1 | $70.6 | $204.3 | $133.6 |

| Kansas | $16.2 | $129.8 | $25.8 | $95.1 | $266.9 | $0.0 |

| Kentucky | $18.3 | $139.7 | $31.3 | $88.6 | $277.8 | $0.0 |

| Louisiana | $15.3 | $101.7 | $33.0 | $63.4 | $213.4 | $0.0 |

| Maine | $14.6 | $75.7 | $15.8 | $73.2 | $179.3 | $0.0 |

| Maryland | $34.0 | $190.4 | $56.7 | $130.4 | $411.5 | $0.0 |

| Massachusetts | $67.4 | $324.7 | $43.3 | $191.9 | $627.4 | $0.0 |

| Michigan | $43.3 | $342.7 | $64.5 | $285.5 | $736.0 | $0.0 |

| Minnesota | $41.1 | $369.7 | $49.7 | $230.6 | $691.2 | $0.0 |

| Mississippi | $10.2 | $77.4 | $31.3 | $57.1 | $176.0 | $0.0 |

| Missouri | $35.7 | $223.0 | $46.2 | $171.6 | $476.6 | $0.0 |

| Montana | $8.5 | $47.1 | $11.1 | $42.8 | $109.5 | $66.6 |

| Nebraska | $8.8 | $84.0 | $14.4 | $55.9 | $163.1 | $0.0 |

| Nevada | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| New Hampshire | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| New Jersey | $25.7 | $412.7 | $85.7 | $259.9 | $783.9 | $0.0 |

| New Mexico | $10.4 | $60.5 | $25.6 | $60.9 | $157.5 | $0.0 |

| New York | $190.8 | $812.1 | $145.4 | $546.4 | $1,694.7 | $0.0 |

| North Carolina | $55.5 | $326.3 | $91.4 | $227.9 | $701.2 | $0.0 |

| North Dakota | $0.0 | $17.1 | $3.3 | $8.2 | $28.6 | $28.6 |

| Ohio | $24.9 | $261.1 | $58.4 | $195.0 | $539.4 | $0.0 |

| Oklahoma | $19.4 | $125.5 | $40.2 | $92.5 | $277.7 | $0.0 |

| Oregon | $50.6 | $322.0 | $46.7 | $203.9 | $623.2 | $419.3 |

| Pennsylvania | $40.6 | $317.7 | $56.2 | $255.4 | $670.0 | $0.0 |

| Rhode Island | $7.5 | $27.7 | $5.9 | $24.2 | $65.3 | $0.0 |

| South Carolina | $44.2 | $224.2 | $71.2 | $181.5 | $521.1 | $521.1 |

| South Dakota | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Tennessee | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Texas | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Utah | $13.8 | $122.1 | $27.4 | $55.1 | $218.5 | $0.0 |

| Vermont | $2.7 | $32.9 | $7.2 | $32.9 | $75.6 | $0.0 |

| Virginia | $67.3 | $324.0 | $88.1 | $239.5 | $718.8 | $0.0 |

| Washington | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| West Virginia | $4.6 | $57.9 | $17.7 | $54.0 | $134.1 | $0.0 |

| Wisconsin | $27.0 | $278.4 | $49.3 | $203.4 | $558.1 | $0.0 |

| Wyoming | n.a. | n.a. | n.a. | n.a. | $0.0 | n.a. |

| US Total Possible | $1,498.7 | $11,065.5 | $2,355.5 | $6,910.4 | $21,830.1 | -- |

| US Total Incorporated | $173.2 | $793.3 | $212.8 | $367.4 | -- | $1,714.6 |

Source: US Bureau of Labor Statistics; Internal Revenue Service; US Department of Agriculture; US Census Bureau; New York Federal Reserve Bank; Edmunds; Tax Foundation calculations.

Higher Property Tax Deduction

Many states provide a deduction against local property taxes under their own individual income taxes, and this provision is typically tied to the federal SALT deduction, usually after adding back income tax deductibility to avoid circularity. Under the OBBBA, the SALT deduction, which was capped at $10,000 under the TCJA, is increased to $40,000 per household. The additional deduction phases out between $500,000 and $600,000 in household income, above which only the $10,000 deduction is available, but for many taxpayers, this higher cap will reduce both federal and state income tax liability.

Eighteen states use the federal cap for their own local property tax deductions, either by directly conforming to the provision or through incorporation of federal itemizations. The remaining states with income taxes either (1) allow uncapped property tax deductions in their own right, (2) set standalone caps, or (3) deny taxpayers a deduction for local property taxes. The following states will see their own cap increase in line with the increased federal cap, either by allowing federal itemized deductions generally or through a state deduction conforming in relevant part to the federal SALT cap:

Table 3. States with Property Tax Deductions Tied to the Federal SALT Cap

| Alabama | Iowa | New Mexico |

| Arizona | Maryland | North Dakota |

| Colorado | Mississippi | Oklahoma |

| Delaware | Missouri | Oregon |

| Georgia | Montana | South Carolina |

| Idaho | Nebraska | Utah |

Business Expensing Provisions

Whereas the temporary personal deductions (for qualified tips, overtime premium pay, and auto loan interest), which only flow automatically to a few states’ tax systems, reduce revenues without generating much economic benefit, the new law’s provisions about the expensing of corporate investment affect most states and possess a compelling economic justification. However states choose to respond to other provisions of the bill, they should conform to these pro-growth provisions, which represent a marked improvement in the corporate tax code.

Because corporate income taxes are intended to be a levy on net income (profits), most business expenses are deductible. That includes compensation, the cost of goods sold, and other ordinary business expenses. But when it comes to capital investments, which lawmakers frequently say they want to encourage, the deductions can be somewhat stingy. Instead of claiming an immediate deduction for the cost of new investment, businesses often see their deductions amortized over many years, according to depreciation schedules which vary in length depending on asset class.

Depreciation makes sense in accounting. If a company buys a $10 million piece of equipment, it is not $10 million poorer. It has less cash on hand, but it has a piece of equipment worth a similar amount. Yet there’s no way in which the money invested in the equipment is profit, any more than the amount spent on compensation is. Depreciation schedules have no place in well-structured tax policy.

The OBBBA makes four significant changes around business expensing, all of which are relevant to states as well. This piece outlines those provisions, indicates which states are in line to incorporate them into their own tax codes, and provides state-by-state estimates of revenue impacts. The four business expensing changes are as follows:

- The § 168(k) full expensing provision for machinery, equipment, and certain other tangible property is restored and made permanent.

- The recent shift to amortizing research and experimental expenditures under § 174 is reversed, restoring immediate cost recovery for research and development costs.

- A new § 168(n) is created, providing first-year expensing for qualified production property (e.g., factories).

- The cap on the § 179 expensing deduction for small businesses is raised from $1 million to $2.5 million.

Under the Tax Cuts and Jobs Act (TCJA) of 2017, corporations were temporarily permitted to fully expense certain capital investments in the first year, but that provision was phasing out. Another much more modest expensing provision, primarily targeted at small businesses but available to pass-throughs as well as C corporations, had its annual limit raised from $25,000 to $1 million. And, as a pay-for in the back half of the 10-year budget window that most lawmakers expected to be eliminated, the TCJA required research and development expenditures to be capitalized and amortized beginning in 2022, a departure from the prior ability of businesses to deduct these costs immediately.

The § 168(k) change is slated to impact 17 states. The higher § 179 cap is ultimately in line to flow through to 38. And the restoration of § 174 expensing and the creation of a new § 168(n) cost recovery provision will ultimately show up in virtually all states’ tax codes.

These provisions come at a cost of revenue (see Table 5), just as the new deductions for qualified tips, overtime premium pay, and auto loan interest do for the smaller number of states in line to conform to them. But unlike those new deductions, these capital expensing provisions also have a strong economic justification. They are pro-growth, they make the corporate tax code more neutral and economically efficient, and, for § 168(k) and § 174, they represent a return to the policies that conforming states were already following until a few years ago.

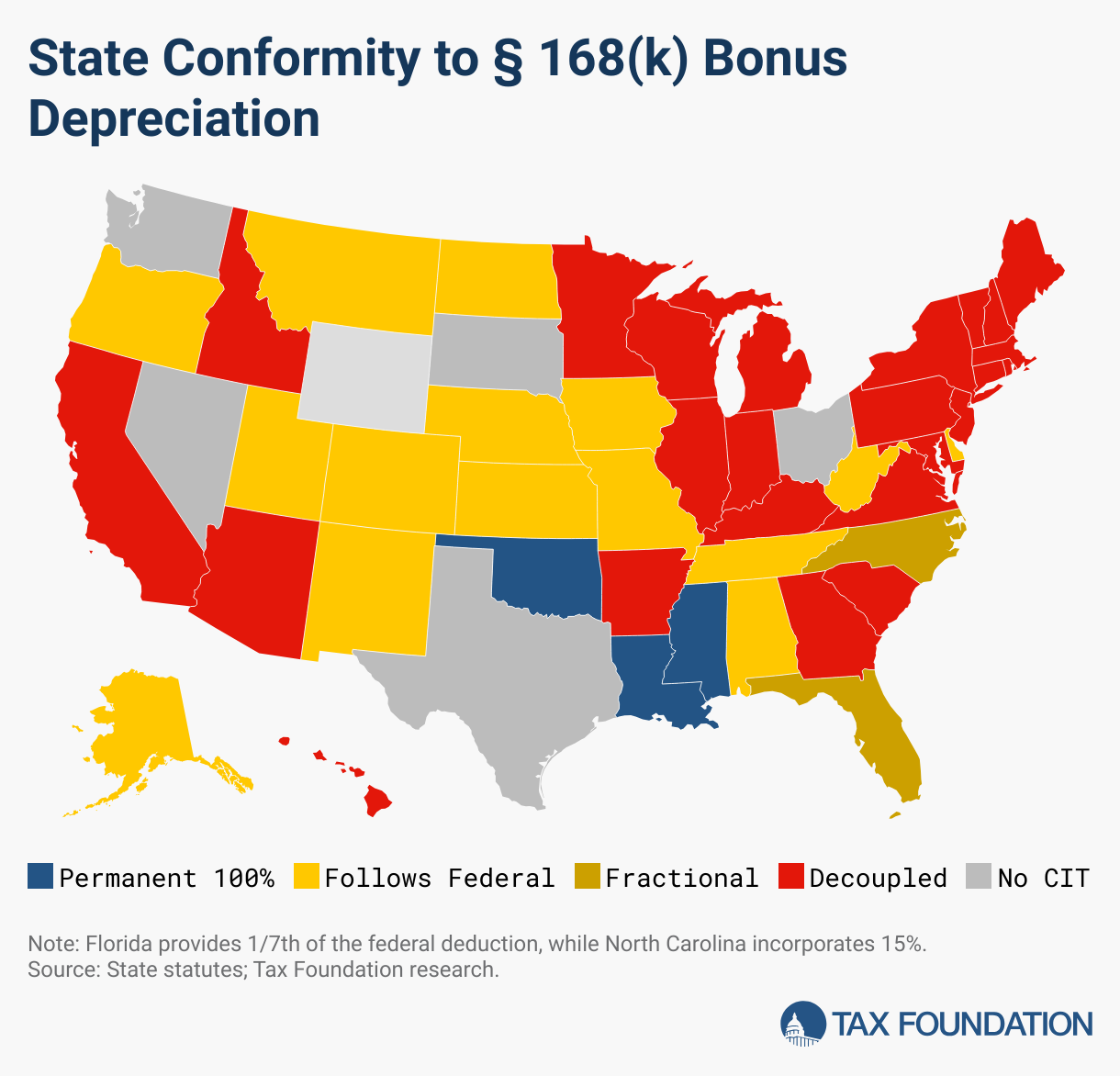

§ 168(k) Bonus DepreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

Fifteen states offer § 168(k) first-year expensing to the same degree that the federal government does. Two more offer a small fraction of the first-year amount allowed under the Internal Revenue Code, while another three have established permanent full expensing regardless of federal policy. The 17 states conforming fully or fractionally to § 168(k) would see their first-year expensing restored to where it stood from late 2017 through the end of 2022, after which it began phasing out, standing at 40 percent first-year “bonus depreciation” in 2025 prior to the enactment of the OBBBA. Full expensing represents sound tax policy, and this is a provision to which states are prudent to conform. States that have decoupled from § 168(k) should consider conforming to the restored federal policy.[3]

§ 174 Research & Experimentation Cost Recovery

Requiring five-year amortization of research and development costs under the § 174 was never really intended to go into effect. That gimmick (a “cost savings” in the TCJA that was not meant to be realized) is fair game for criticism, but the Research & Experimentation (R&E) expensing provision is so popular, and such clearly appropriate policy, that many observers were surprised the capitalization and amortization provision was permitted to take effect in 2022. Corporations have been allowed to deduct R&E expenditures — the IRC’s term for what is generally considered research and development (R&D) costs — in the year in which the expense is incurred since 1954, and every state with a corporate income tax has followed suit. When the federal government shifted to five-year amortization beginning in 2022, 10 states continued to offer immediate expensing of R&E, either through express policy or, as in the case of California, by conforming to a pre-TCJA version of the Internal Revenue Code (IRC). All other states with corporate income taxes followed the federal government’s lead in setting aside the R&E policy that had prevailed for 68 years. By conforming to its restoration, states will be accepting a “cost” compared to the policy of the past three and a half years, but one that was fully baked into their tax code for the better part of seven decades. Any effort to decouple from this provision would be short-sighted.

§ 168(n) Qualified Production Property Deduction

For the first time, the federal tax code will now provide first-year expensing for certain structures. However, the new provision, at § 168(n), is both temporary (expiring after 2028) and largely limited to manufacturing plants. Neutral cost recovery for structures is good policy, and this temporary provision might ultimately become a permanent one. As a temporary policy, though, its economic benefits are not as large as they could be, and the temporary provision will move up the timeline for construction projects in addition to inducing greater construction overall. Still, particularly given the possibility that this provision will be extended or made permanent, it represents an improvement in the tax code, and one with relatively low costs. While § 168(n) is a new section of the tax code, all but four states with corporate income taxes conform to the provisions of § 168 generally, only decoupling (if at all) from specific named provisions, and thus most states would be in line to incorporate the new provision into their own tax codes.

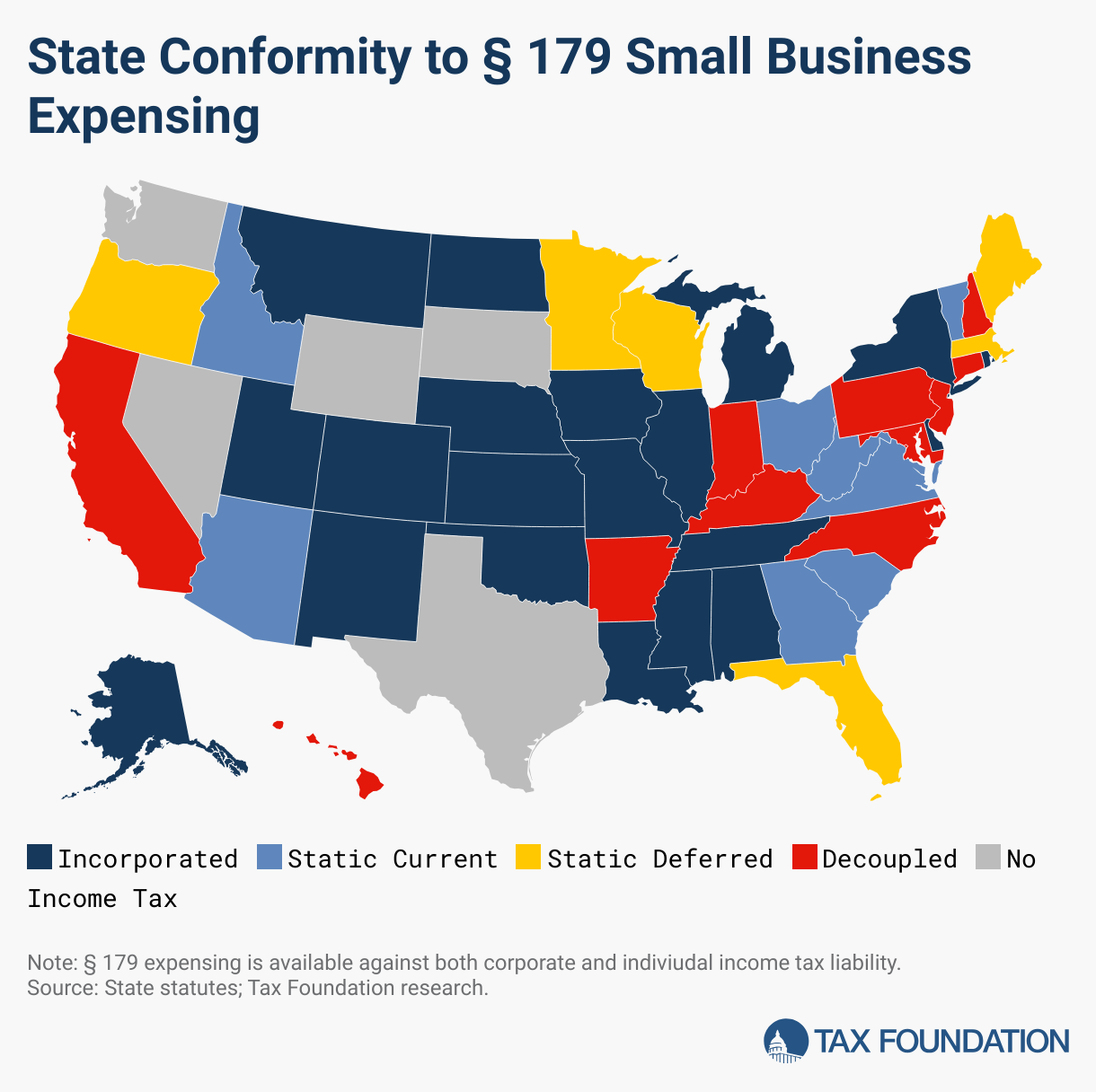

§ 179 Small Business Expensing

Finally, the OBBBA raises the cap on § 179 first-year expensing from $1 million to $2.5 million with inflation adjustments. (In practice, the $1 million cap was worth $1.25 million in 2025, and the new $2.5 million cap would be adjusted to $3.13 million.) While § 179 comes with a dollar limit, unlike § 168(k), it also has an important place in cost recovery policy, because it is available to pass-through businesses as well as C corporations, and because some assets (including used machinery and equipment and HVAC) are eligible under § 179 but not § 168(k).[4] This provision is only available to small businesses, with benefits beginning to phase out above an investment threshold that rises, under the new federal law, from $3.13 million to $5.0 million under existing inflation adjustments. Most states incorporate the IRC’s cap and phaseout threshold, though 12 adopt their own lower caps, ranging from $25,000 to $500,000.

Without these four expensing provisions, businesses only get the benefit of these deductions over time: for periods as long as 20 years for assets eligible for immediate expensing under § 168(k), and for 39 years for the factories eligible for first-year expensing under § 168(n). That imposes real costs, due to inflation and the time value of money. The present value of a deduction spread over the next 5, 10, 20, or even 39 years is less than the value of receiving the full deduction now. The tax code embeds disincentives for capital investment, and each of these new provisions represents an improvement in the treatment of those investments. For that reason, it makes sense for states to align with them, enhancing the competitiveness of their own tax codes and reducing the tax system’s bias against investment and growth.

Broadly speaking, states use the IRC as a starting point for their own corporate income taxes, which is why these provisions generally flow through to states. There are, however, two sources of disconnect: first, some states conform to an out-of-date version of the IRC, meaning that they won’t incorporate these changes until their conformity date catches up with the effective date of the OBBBA; and second, some states expressly modify or decouple from select provisions, as with the states that decouple from § 168(k) bonus depreciation, or set their own lower caps for § 179 small business expensing. Of course, some modifications also run in the other direction, as with the states that offer 100 percent first-year expensing under § 168(k) regardless of federal policy, or those that maintained § 174 R&E first-year expensing even when the federal government temporarily abandoned it. The change in federal policy has no direct effect on these states, except through the simplifying element of federal policy re-aligning with state policy.

The table below indicates states’ conformity to each of these expensing provisions and notes the state’s conformity status, with a subsequent table providing projected revenue implications. States that offer 100 percent first-year expensing in their own right, regardless of federal policy, are noted. Some have rolling conformity, thus automatically conforming to the newest version of the IRC, while others have static (fixed date) conformity. It should be noted that in most static conformity states, updating the conformity date is typically a pro forma exercise, with a one-year advance adopted by the legislature each year. A few states, however, lag further behind in IRC conformity. States that presently conform to the IRC as it existed as of December 31, 2024, or January 1, 2025, are indicated as “Static – Current,” while those with earlier conformity dates are indicated by “Static – Lagged.” Of course, an update to the conformity date is never guaranteed, particularly after the enactment of significant federal tax changes.

Table 4. State Conformity with the OBBBA’s Expensing Provisions

| State | Conformity Status | § 168(k) | § 168(n) | § 174 | § 179 |

|---|---|---|---|---|---|

| Alabama | Rolling | ✓ | ✓ | 100% | ✓ |

| Alaska | Rolling | ✓ | ✓ | ✓ | ✓ |

| Arizona | Static - Current | ✓ | ✓ | ✓ | |

| Arkansas | Selective | ✓ | |||

| California | Static - Lagged | ✓ | |||

| Colorado | Rolling | ✓ | ✓ | ✓ | ✓ |

| Connecticut | Rolling | ✓ | ✓ | ||

| Delaware | Rolling | ✓ | ✓ | ✓ | ✓ |

| District of Columbia | Rolling | ✓ | ✓ | ||

| Florida | Static - Lagged | ✓ | ✓ | ✓ | ✓ |

| Georgia | Static - Current | 100% | ✓ | ||

| Hawaii | Static - Current | ✓ | ✓ | ||

| Idaho | Static - Current | ✓ | ✓ | ✓ | |

| Illinois | Rolling | ✓ | ✓ | ✓ | |

| Indiana | Static - Lagged | ✓ | 100% | ||

| Iowa | Rolling | ✓ | ✓ | ✓ | ✓ |

| Kansas | Rolling | ✓ | ✓ | ✓ | ✓ |

| Kentucky | Static - Current | ✓ | |||

| Louisiana | Rolling | 100% | ✓ | 100% | ✓ |

| Maine | Static - Lagged | ✓ | ✓ | ✓ | |

| Maryland | Rolling | ✓ | ✓ | ||

| Massachusetts | Rolling | ✓ | ✓ | ✓ | |

| Michigan | Rolling | ✓ | ✓ | ✓ | |

| Minnesota | Static - Lagged | ✓ | ✓ | ✓ | |

| Mississippi | Rolling | 100% | ✓ | 100% | ✓ |

| Missouri | Rolling | ✓ | ✓ | ✓ | ✓ |

| Montana | Rolling | ✓ | ✓ | ✓ | ✓ |

| Nebraska | Rolling | ✓ | ✓ | 100% | ✓ |

| Nevada | n.a. | No Income Tax | |||

| New Hampshire | Static - Lagged | ✓ | ✓ | ||

| New Jersey | Rolling | ✓ | 100% | ||

| New Mexico | Rolling | ✓ | ✓ | ✓ | ✓ |

| New York | Rolling | ✓ | ✓ | ✓ | |

| North Carolina | Static - Lagged | ✓ | ✓ | ||

| North Dakota | Rolling | ✓ | ✓ | ✓ | ✓ |

| Ohio | Static - Current | No CIT | ✓ | ||

| Oklahoma | Rolling | 100% | ✓ | ✓ | ✓ |

| Oregon | Rolling | ✓ | ✓ | ✓ | ✓ |

| Pennsylvania | Rolling | ✓ | ✓ | ||

| Rhode Island | Rolling | ✓ | ✓ | ✓ | |

| South Carolina | Static - Current | ✓ | ✓ | ✓ | |

| South Dakota | n.a. | No Income Tax | |||

| Tennessee | Rolling | ✓ | ✓ | 100% | ✓ |

| Texas | n.a. | No Income Tax | |||

| Utah | Rolling | ✓ | ✓ | ✓ | ✓ |

| Vermont | Static - Current | ✓ | ✓ | ✓ | |

| Virginia | Static - Current | ✓ | ✓ | ✓ | |

| Washington | n.a. | No Income Tax | |||

| West Virginia | Static - Current | ✓ | ✓ | ✓ | ✓ |

| Wisconsin | Static - Lagged | ✓ | 100% | ✓ | |

| Wyoming | n.a. | No Income Tax |

Sources: state statutes; Tax Foundation research.

Estimating the revenue implications of these provisions for all 50 states is difficult, and we would defer to the figures generated by state revenue agencies where available. Nevertheless, we offer the following estimates as reasonable approximations to provide state lawmakers with a sense of their cost. These figures are, if anything, a substantial overestimate, as they assume that the forgone taxable income would otherwise be fully taxable. In practice, tax credits, abatements, and other incentives are often available to businesses making significant capital investments, which may lower their initial effective rates and thus reduce the cost of expensing policies relative to the status quo.

If all states currently in line to conform to these provisions maintained that conformity, we estimate that the nationwide cost would be $12.8 billion per year, which is less than 0.4 percent of state revenues. If all states chose to conform to all provisions, the nationwide cost would rise to $20.7 billion per year, or about 0.6 percent of state revenues.

First-year expensing provisions, of course, frontload costs. Some of this reduction in state revenue is real and permanent, since better cost recovery systems remove the penalty imposed on businesses through amortization, which imposes a price in terms of inflation and the time value of money. Much of the cost for initial years, however, disappears in later years. Added to this effect, the § 168(k) provision has a catch-up element that allows businesses to claim full expensing retroactively for years in which the provision was phasing down.

Consequently, costs are significantly higher in 2025 and 2026, and much lower or even negative compared to the baseline (because costs were shifted in time) in subsequent years. Below, we provide cost estimates for both for a 10-year average and for tax year 2026, with the 10-year average providing a better estimate of the long-term costs of implementing these pro-growth provisions. For 2026, however, the nationwide cost for all states in line to conform with these provisions would be $17.3 billion, and if every state chose to align with federal policy, the cost would be $38.2 billion.

Figures are in millions, and a figure in bold indicates that the state conforms to a given provision if and when its conformity date aligns with a post-OBBBA version of the IRC. Italics indicate that a state already provides the benefit just adopted by the federal government, and therefore there is no additional cost associated with conformity.

Revenue Estimates for State Conformity to the OBBBA’s Expensing Provisions

Estimates for Average Annual Costs over the Budget Window and for 2026, in Millions of Dollars

| Ten Year Average | Tax Year 2026 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| State | § 168(k) | § 168(n) | § 174 | § 179 | § 168(k) | § 168(n) | § 174 | § 179 | |

| Alabama | $47 | $26 | $0 | $6 | $303 | $30 | $0 | $9 | |

| Alaska | $9 | $5 | $32 | $0 | $59 | $6 | $38 | $0 | |

| Arizona | $40 | $22 | $141 | $5 | $259 | $25 | $165 | $7 | |

| Arkansas | $18 | $10 | $62 | $2 | $114 | $11 | $73 | $4 | |

| California | $843 | $471 | $2,977 | $119 | $5,466 | $534 | $3,493 | $172 | |

| Colorado | $54 | $30 | $192 | $9 | $352 | $34 | $225 | $13 | |

| Connecticut | $73 | $41 | $259 | $9 | $476 | $46 | $304 | $13 | |

| Delaware | $13 | $7 | $44 | $2 | $81 | $8 | $52 | $2 | |

| District of Columbia | $27 | $15 | $94 | $3 | $173 | $17 | $110 | $5 | |

| Florida | $128* | $72 | $453 | $3 | $832* | $81 | $532 | $4 | |

| Georgia | $76 | $42 | $0 | $15 | $490 | $48 | $0 | $22 | |

| Hawaii | $10 | $5 | $35 | $3 | $64 | $6 | $41 | $4 | |

| Idaho | $23 | $13 | $82 | $4 | $151 | $15 | $96 | $6 | |

| Illinois | $242 | $135 | $856 | $22 | $1,572 | $153 | $1,005 | $32 | |

| Indiana | $22 | $12 | $0 | $5 | $142 | $14 | $0 | $8 | |

| Iowa | $20 | $11 | $72 | $3 | $132 | $13 | $84 | $5 | |

| Kansas | $30 | $17 | $107 | $5 | $196 | $19 | $125 | $7 | |

| Kentucky | $50 | $28 | $176 | $4 | $324 | $32 | $207 | $6 | |

| Louisiana | $0 | $11 | $0 | $3 | $0 | $13 | $0 | $5 | |

| Maine | $9 | $5 | $33 | $3 | $61 | $6 | $39 | $4 | |

| Maryland | $103 | $58 | $364 | $10 | $669 | $65 | $427 | $14 | |

| Massachusetts | $140 | $78 | $496 | $16 | $910 | $89 | $582 | $24 | |

| Michigan | $62 | $35 | $219 | $11 | $401 | $39 | $257 | $15 | |

| Minnesota | $129 | $72 | $456 | $14 | $837 | $82 | $535 | $20 | |

| Mississippi | $0 | $6 | $0 | $2 | $0 | $7 | $0 | $3 | |

| Missouri | $35 | $20 | $124 | $7 | $227 | $22 | $145 | $11 | |

| Montana | $7 | $4 | $23 | $2 | $42 | $4 | $27 | $4 | |

| Nebraska | $26 | $14 | $0 | $4 | $167 | $16 | $0 | $5 | |

| Nevada | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Hampshire | $25 | $14 | $87 | $1 | $160 | $16 | $102 | $1 | |

| New Jersey | $196 | $110 | $0 | $21 | $1,273 | $124 | $0 | $31 | |

| New Mexico | $17 | $9 | $59 | $2 | $108 | $11 | $69 | $3 | |

| New York | $584 | $327 | $2,064 | $47 | $3,790 | $370 | $2,422 | $68 | |

| North Carolina | $36* | $20 | $127 | $12 | $233* | $23 | $149 | $17 | |

| North Dakota | $7 | $4 | $23 | $1 | $43 | $4 | $27 | $1 | |

| Ohio | $0 | $0 | $0 | $7 | $0 | $0 | $0 | $10 | |

| Oklahoma | $0 | $8 | $51 | $4 | $0 | $9 | $59 | $6 | |

| Oregon | $34 | $19 | $121 | $10 | $222 | $22 | $142 | $15 | |

| Pennsylvania | $102 | $57 | $362 | $12 | $664 | $65 | $424 | $17 | |

| Rhode Island | $12 | $7 | $43 | $1 | $79 | $8 | $51 | $2 | |

| South Carolina | $32 | $18 | $114 | $9 | $208 | $20 | $133 | $12 | |

| South Dakota | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Tennessee | $61 | $34 | $0 | $1 | $398 | $39 | $0 | $2 | |

| Texas | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Utah | $32 | $18 | $111 | $5 | $205 | $20 | $131 | $8 | |

| Vermont | $6 | $4 | $22 | $1 | $41 | $4 | $26 | $2 | |

| Virginia | $61 | $34 | $216 | $15 | $397 | $39 | $254 | $21 | |

| Washington | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| West Virginia | $9 | $5 | $33 | $1 | $61 | $6 | $39 | $2 | |

| Wisconsin | $51 | $28 | $0 | $10 | $329 | $32 | $0 | $14 | |

| Wyoming | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total - Conforming States | $424 | $1,430 | $10,730 | $250 | $2,750 | $1,622 | $12,593 | $364 | |

| Total - All States | $3,502 | $1,983 | $10,730 | $4,526 | $22,711 | $2,246 | $12,593 | $669 |

* Florida and North Carolina only conform to a small fraction of federal § 168(k) amounts. They are indicated as not conforming and the cost of full conformity is given, but under current policy, the states’ additional annual costs would be $18 and $5 million per year respectively. These amounts are included in the “conforming states” subtotals.

While the incorporation of these provisions is not without cost, state revenues have risen dramatically in recent years, with tax collections rising 19.4 percent in real terms since the implementation of the TCJA in 2017 and 50 percent in the past two decades. Even as revenues have stabilized more recently, most states have the capacity to incorporate these pro-growth provisions into their codes—and they should. The larger provisions, after all, are not even new: many states conformed to § 168(k) when it provided full expensing prior to 2023, and all states with a corporate income tax conformed to first-year cost recovery for research and development until 2022. Those provisions worked for years, and in the case of research and development deductions, for nearly seven decades. There is no reason for states to abandon them now.

International Provisions

The OBBBA’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Whereas the conversion of the global intangible low-taxed income (GILTI) regime to the new net CFC-tested income (NCTI) regime contains both revenue raisers and tax savings that represent a net tax cut at the federal level, these provisions are haphazardly incorporated into the tax codes of states that have heretofore included GILTI. The result is not just an increase in state tax liability, but an inversion of the intent of the federal reforms. The changes to the federal base have their own pitfalls and shortcomings, but they are still largely designed to align with GILTI’s purpose—a guardrail against profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens. to low-tax countries after the US moved to a largely territorial tax systemTerritorial taxation is a system that excludes foreign earnings from a country’s domestic tax base. This is common throughout the world and is the opposite of worldwide taxation, where foreign earnings are included in the domestic tax base. —while, perversely, states would increasingly do the opposite, increasing taxes on multinational businesses when they owe more tax abroad.

This double taxation is undesirable in its own right and undermines the competitiveness of states choosing to implement it. But high rates of international tax are also a good indication that the activity of a corporation’s foreign affiliates is genuine foreign activity (e.g., European sales) rather than profit-shifting activity (e.g., locating intellectual property in a low-tax country and having related companies pay royalties to it, shifting their profits to a country where the tax rate is lower).

GILTI and the States

Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, the US taxed the worldwide income of US corporations and their affiliates, including controlled foreign corporations (CFCs) based abroad, while allowing such companies to take credits against their US liability for foreign taxes paid. Under the TCJA’s territorial tax system, foreign income is not taxed by default, but Congress wanted to avoid profit-shifting activity in response. GILTI was intended as a minimum tax on certain foreign earnings, undermining the potential tax benefit of such profit shifting. The new NCTI regime arguably provides a better calibration at the federal level, but a far worse one for states incorporating the provision into their own tax codes.

Under GILTI, federal law sought to distinguish between routine and “supernormal” returns, with lawmakers postulating that a CFC’s returns above 10 percent of the value of its tangible assets very likely constituted income from intangibles (e.g., patents, trademarks, copyrights, and other forms of intellectual property from which royalties are derived). This initial 10 percent was excluded under the qualified business asset investment (QBAI) exclusion, which represented a rough-and-ready deemed return on physical capital. Any returns above 10 percent were subject to GILTI.

The remaining income, subject to GILTI, received both a deduction (initially 50 percent) and an offset worth 80 percent of foreign taxes paid. The deduction meant that the US tax rate on GILTI was lower than the rate on US income, reflecting the fact that it was earned abroad and is not an ordinary part of the tax base. The 50 percent deduction under § 250, therefore, functionally turned the 21 percent corporate income tax rate into a 10.5 percent rate on GILTI. (The deduction was scheduled to decline to 37.5 percent in 2026, yielding a 13.125 percent rate.) Actual foreign taxes paid, moreover, yielded foreign tax credits, and 80 percent of their value could be applied against GILTI. The system was far from perfect, but it was designed to tax CFCs’ income to the extent that it was “undertaxed” abroad, potentially (but not always) indicative of US tax avoidance rather than genuine economic activity in other countries.

Unfortunately, when states incorporated GILTI after the enactment of the TCJA, parts of this system immediately fell apart. The federal provisions were not adopted with states in mind, and states’ corporate apportionmentApportionment is the determination of the percentage of a business’s profits subject to a given jurisdiction’s corporate income tax or other business tax. US states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. rules weren’t designed to handle foreign income.

The foreign taxes generating the federal credits were paid by the foreign corporations that US-based multinationals owned or in which they had a substantial investment stake. As a pure matter of accounting, if the US shareholding entity is to be treated as having paid those taxes itself, an equivalent share must also be included in the company’s GILTI income, to avoid a double benefit. The 80 percent of credited taxes are first included in the US company’s income for GILTI purposes under the § 78 “gross-up,” and then the credit is applied. At the federal level, that all worked. But states rarely allow foreign tax credits, while they do conform to the gross-up, so their GILTI bases included 80 percent of the value of taxes paid by CFCs abroad, without the tax credits that gross-up was intended to facilitate. Rather than reducing tax liability based on foreign taxes having already been paid on the income, states’ GILTI regimes tax this income more because of the foreign taxes paid on it. The foreign taxes paid by the CFCs of corporations doing business in a state are not, of course, even remotely US corporate profits, which is what state corporate income taxes are intended to tax.

Converting to NCTI

For states, converting to NCTI makes the problem worse. To begin with, it eliminates the QBAI exclusion, bringing all the income of CFCs into the GILTI/NCTI base rather than just the “supernormal” returns. At the federal level, this base expansion is substantially offset through other changes, but for states, some of them turn into tax multipliers instead. Additionally, under NCTI, the § 250 deduction (which had been at 50 percent but was scheduled to fall to 37.5 percent in 2026), is made permanent at 40 percent, which has the effect of increasing states’ effective rates on this broader base.

But NCTI changes far more than this. Previously, under the GILTI regime, many expenses by US-based multinationals were sourced to their CFCs to the extent that they were deemed to benefit them. Since these business expenses would have ordinarily been deductions from the US company’s taxable income, these expense allocation rules (1) increased US tax liability for US-based multinationals, since they were denied deductions for some of their business expenses; but, at the same time, (2) provided deductions for the CFCs, reducing their taxable income potentially subject to GILTI.

On net, businesses would have preferred to have the deduction for their US-based corporations, as the ordinary rate is higher than the GILTI rate and because foreign taxes paid on ordinary business activity of CFCs abroad often yield credits in excess of GILTI tax liability, leaving some credits unused. (GILTI is, after all, a minimum tax. Foreign tax liability can often exceed its minimum.) Under NCTI, changes in expense allocation rules mean that more of these deductions are taken by the US parent corporation. Consequently, there are fewer deductions for their CFCs, yielding a larger NCTI base than the old GILTI base. That’s a welcome shift for many corporations with significant tax liability in other countries, because they get the benefit of the US deductions and can use more of their foreign tax credits against the new NCTI base. Simultaneously, the new law reduces the limitation on foreign tax credits (called the “FTC haircut”), raising the inclusion amount from 80 to 90 percent with a commensurate increase in the § 78 gross-up.

It’s not hard to imagine where this goes wrong at the state level. The NCTI base expands yet again, and the greater allowance for foreign tax credits, rather than offsetting liability, is picked up as additional income to be taxed. All four major changes—scrapping the QBAI exclusion, adjusting the § 250 deduction, trimming the FTC haircut with a commensurate increase in the § 78 gross-up, and revising expense allocation rules—make state taxation of NCTI more aggressive than state taxation of GILTI, whereas these changes yield a net tax cut at the federal level.

State Incorporation of GILTI and NCTI

Twenty-one states currently include at least some GILTI in their base, though many reduce GILTI taxability in some way, typically by subjecting it to the state’s dividends received deduction. Eleven states and the District of Columbia bring in 50 percent of GILTI (the full amount possible under the § 250 deduction) and would be on track to bring in 60 percent of NCTI since the § 250 deduction would decline to 40 percent. Nine other states bring in lesser shares of GILTI, ranging from 5 to 30 percent.

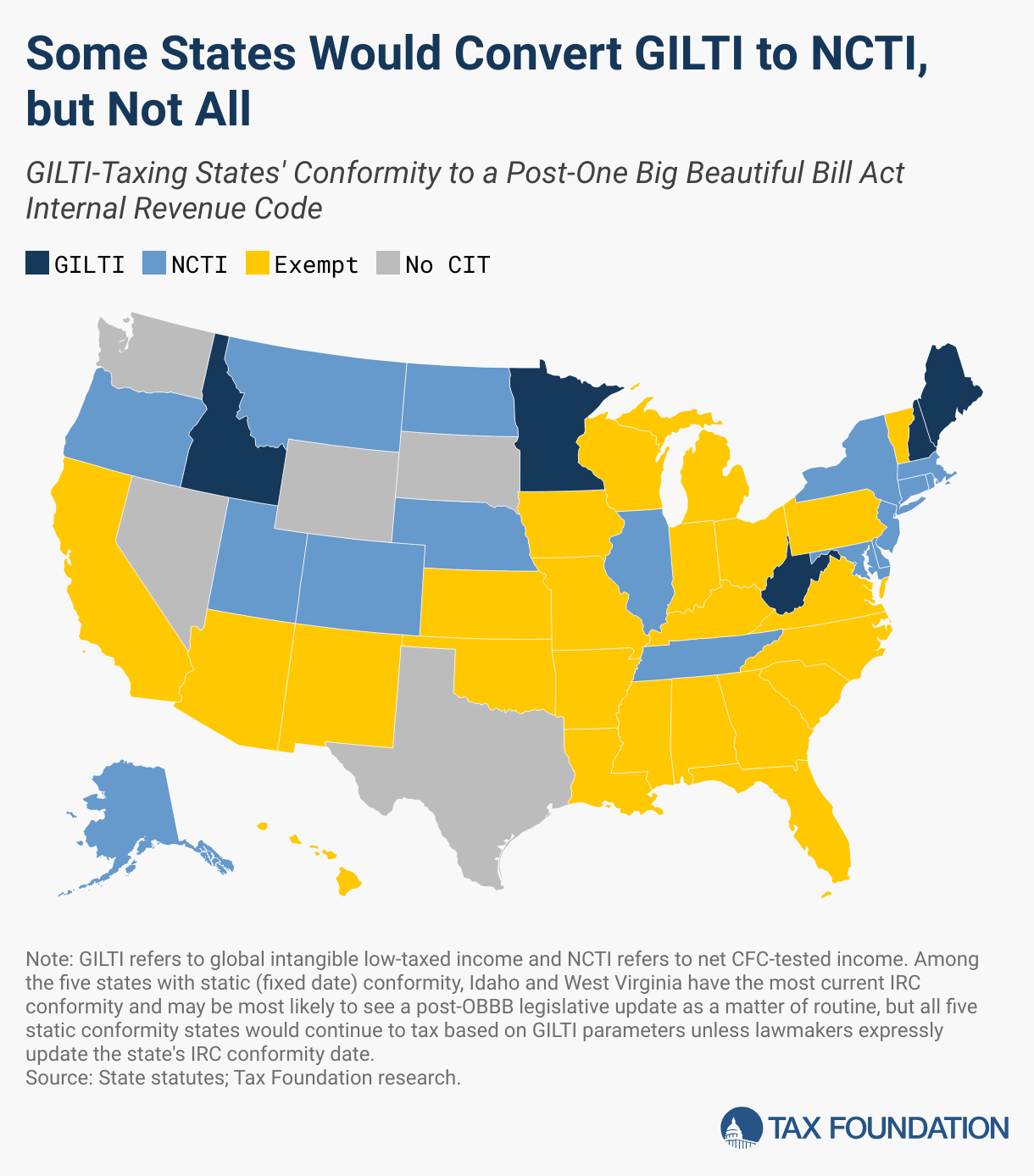

Fifteen states and the District of Columbia will automatically follow the federal government in switching from GILTI to NCTI. These GILTI-including states, which have rolling conformity to changes in the Internal Revenue Code (IRC), are Alaska, Colorado, Connecticut, Delaware, Maryland, Massachusetts, Montana, Nebraska, New Jersey, New York, North Dakota, Oregon, Rhode Island, Tennessee, Utah, and the District of Columbia. Another five states that currently tax GILTI have static (fixed date) conformity to the IRC, and thus would continue to apply GILTI rules unless and until state lawmakers update their state tax code’s conformity to a post-OBBB version. Of these, Idaho and West Virginia, while static conformity states, were “current” prior to the enactment of the OBBB and have generally seen annual conformity updates. Maine, Minnesota, and New Hampshire are all lagging on IRC conformity.

Should a state incorporate GILTI (or, more precisely, IRC § 951A) but conform to a version of the IRC prior to the enactment of the OBBB, it would continue to tax based on GILTI parameters rather than transitioning to NCTI. Such states would need to publish guidance and worksheets for making this conversion, though some states’ inability to issue guidance on other GILTI issues eight years into their taxation of it does not augur well for timely guidance in all relevant states.

State taxation of GILTI never made much sense. The federal government’s purposes in enacting a guardrail against profit shifting had little to do with states, which have not historically taxed international income (with very limited exceptions). Apportionment of the income of these CFCs to states in which the US-based related corporations operate never bore much relation to any activity in the states in question. Taxing the § 78 gross-up always meant that part of the state tax base was foreign tax liability, while states failed to bring in the foreign tax credits that were an integral part of the system. And apportionment has never worked properly for GILTI, as most states deny all factor representation (and only one state, New Mexico, fully provides it), with GILTI put in the numerator of the apportionment factor but not added to the denominator, resulting in an overweighting.

But taxing NCTI makes even less sense. Without the QBAI exclusion, the base includes all income of these CFCs, not just their supernormal returns. And whereas the federal system now relies even more heavily on foreign tax credits (and revised expense allocation rules) to make NCTI a tax on foreign income that faced low taxes abroad, the lack of similar tax credits at the state level obliterates that distinction and renders void the mechanism the new federal system employs to prevent NCTI from being a tax on all of the income of US companies’ foreign affiliates.

This matters not just because state-level NCTI taxation has little logic or justification, but also because it makes the taxing states less competitive. Companies may take steps to reduce in-state sales into states that tax GILTI by using third-party distributors or routing billing through out-of-state entities, thus also reducing their exposure to that state’s ordinary taxes. And under some states’ GILTI regimes, the location of a corporate headquarters in the state can dramatically increase exposure to GILTI, since intangible receipts are sourced to commercial domiciles and some states put net GILTI in the sales factor. GILTI is only responsible for a fraction of a percent of state revenues, but it can be a significant factor for some of the businesses states most want to attract.

States that tax GILTI should regard the federal change as the impetus to get out of the business of taxing this class of international income entirely, under GILTI or NCTI rules. Virtually nothing of its federal purpose or even its intended federal base is retained when incorporated into state tax codes. States can and should say no to NCTI.

Medicaid Provider Taxes

For decades, states have leaned on Medicaid provider taxes to acquire additional federal matching funds. States levy a tax on health care providers, raising revenue that is then spent on Medicaid, generating a federal match.

The federal government covers 90 percent of spending on the expansion group under the Affordable Care Act (ACA), with the Federal Medical Assistance Percentage (FMAP) varying by state for the traditional Medicaid population, based on state incomes. Nationwide, states contribute slightly under one-third of the total cost of Medicaid spending. Using provider taxes, states can boost their Medicaid spending, raising base rates or creating add-on payments that largely make the taxpaying institutions whole while drawing down additional federal dollars.

This arrangement, however, can often look like a mere accounting trick, and the federal government has long constrained states’ abilities to levy these taxes, establishing an approval process and adopting a safe harbor under which such taxes are generally permissible, and over which they are not. That safe harbor has long stood at 6 percent of net patient revenue. Under the OBBBA, the limit will phase down, 0.5 percentage points at a time, to 3.5 percent for states that adopted Medicaid expansion—a list consisting of 39 states and the District of Columbia.

Taxes on nursing homes and intermediate care facilities are exempted from the phase-down. Taxes already levied by non-expansion states are grandfathered in at rates up to 6 percent, and the ability to levy new provider taxes or raise the rates of existing ones is frozen under the new law. Federal law already required that these taxes be broad-based and uniform, but the OBBBA also curtails the existing waiver system for those requirements, likely invalidating some existing tax systems.

Not all states maxed out their possible provider taxes, so even among expansion states, there are varying degrees of exposure to the safe harbor phasedown, which begins in FY 2028 and reaches 3.5 percent in FY 2032. Reportedly, however, many states made submissions for new or higher provider taxes immediately prior to the deadline in the OBBBA.

The Congressional Budget Office (CBO) estimates that the new provider tax restrictions will save the federal government $191 billion over the 10-year budget window, and $34 billion a year by the time the reduction is fully phased in, but this does not translate directly into a commensurate reduction in state budgets compared to current policy. The federal government makes assumptions about future Medicaid expansion and the implementation of new or higher provider taxes not yet on the books, so the estimated federal budgetary savings are not just reductions against current law, but also against assumptions of the further proliferation of provider taxes, and of higher FMAPs due to Medicaid expansion, absent the change.

We preliminarily estimate that the impact of just phasing down existing provider taxes is substantially smaller, perhaps on the order of $16 billion per year by FY 2032, when the safe harbor will be reduced to 3.5 percent. Importantly, our calculations and the CBO’s are for budgetary impact, not just tax impact. For instance, if a state has a combined traditional and expanded Medicaid FMAP of 66.7 percent, then a provider tax that raises $100 million will yield about $200 million in federal matching funds, and it is this larger impact that we attempt to estimate.

Other Provisions

The TCJA tightened limits on business interest deductibility, restricting them to 30 percent of earnings before interest, taxes, depreciation, and amortization (EBITDA). In 2022, the limitation became more stringent, shifting to 30 percent of earnings before interest and taxes (EBIT). States tend to incorporate the new business interest limitations, even though many did not incorporate the first-year expensing provisions for which they helped to pay. Under the OBBBA, the broader definition of earnings (EBITDA) is restored.

Several other OBBBA provisions have implications for select states. The permanently higher AMT threshold is relevant to Colorado and Connecticut, both of which use the federal AMT in assessing their own minimum taxes. (California and Minnesota also impose AMTs but do so under state-specific rules.) The permanently higher federal estate tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. also affects Connecticut, the only state with an estate tax that conforms to the federal exemption. And states that begin their income tax calculations with federal taxable income are in line to incorporate a non-itemizer $1,000 charitable contribution deduction.

Conclusion

With so many changes, lawmakers may be tempted to postpone conformity to a post-OBBBA version of the IRC. That, however, would surrender the many practical benefits of up-to-date conformity for taxpayers and tax administrators alike. Instead, lawmakers should weigh the costs and benefits of specific provisions of the new law, decoupling from certain provisions as necessary, and perhaps conforming to pro-growth provisions with which their codes do not currently align.

The temporary deductions for qualified tips, overtime premium pay, and auto loan interest reduce tax collections in a few states while offering limited economic benefit, whereas the business expensing provisions make the tax code more neutral and pro-growth. The shift from GILTI to NCTI, moreover, enhances the case for decoupling from the law’s international tax regime, because the patchwork way that its provisions flow through to state tax codes yields state-level taxes that bear little resemblance to the tax Congress created.

State tax revenues have risen dramatically in recent years, in part due to the base-broadening provisions of the TCJA, which flowed through to most states’ tax codes. While lawmakers cannot be indifferent to the costs of further tax changes, they do have the capacity to act judiciously, preserving those that improve the neutrality and economic efficiency of the tax system, while potentially decoupling from new provisions (mostly temporary) with scant economic benefit.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeMethodology

Senior Bonus Standard Deduction: Total estimated US reduction in federal taxable income is allocated to states based on their 2023 share of additional standard deductions, using IRS Statistics of Income data. Income tax revenue losses are calculated against a blended marginal rate for each state across $60,000 – $80,000 in taxable income.

Qualified Tips Deduction: Total estimated US reduction in federal taxable income is allocated to states using each state’s share of total annual compensation for full-service restaurant workers as a proxy for the distribution of tipped professions across the country, using data from the BLS Quarterly Census of Employment and Wages. Income tax revenue losses are calculated against a blended marginal rate for each state across $20,000 – $40,000 in taxable income.

Overtime Premium Pay Deduction: Total estimated US reduction in federal taxable income is allocated to states according to their share of total state compensation from key overtime-earning sectors weighted by assumed shares associated with premium overtime pay: 1.2 percent for Construction; 1.3 percent for Manufacturing; 1.1 percent for Health Care; 0.8 percent for Trade, Transportation, & Utilities; 1.6 percent for Mining and Natural Resources; and 0.7 percent for Retail, via BLS Quarterly Census of Employment and Wages data. Income tax revenue losses are calculated against a blended marginal rate for each state across $60,000 – $80,000 in taxable income.

Auto Loan Interest Deduction: Total estimated US reduction in federal adjusted gross income is allocated to states according to a share calculated using New York Fed data on outstanding auto loan principal per capita, for which annual interest payments are derived using the average of new and used car loan APYs by state from Edmunds. Income tax revenue losses are calculated against a blended marginal rate for each state across $60,000 – $80,000 in taxable income. The total reduction takes the phaseout into account, but no effort is made to adjust for variations in the share of taxpayers subject to phaseout across states.

Business Expensing Provisions: Total estimated US reduction in federal taxable income for each provision is apportioned according to each state’s share of state-level corporate income tax bases, derived through rate-adjusted Census QTAX data for the four most recent quarters (through Q1 2025). Tax revenue losses are calculated against each state’s top marginal corporate income tax rate, since most states have single-rate corporate income taxes and most expensing is against the top marginal rate even where states impose graduated-rate structures.

Estimates of reductions in taxable income are derived from the Tax Foundation General Equilibrium Model, except for § 179, where the reduction in taxable income is estimated from Office of Management and Budget revenue projections. For § 179, which is primarily claimed against the individual income tax, 10.6 percent of the reduction in taxable income is assessed against corporate income taxes, while the remainder is applied to individual income tax liability, consistent with Joint Committee on Taxation expenditure estimates. For the individual income tax portion, each state’s share of the reduction in federal taxable income is allocated based on state shares of federal income tax liability from IRS Statistics of Income, against which a blended average rate for upper-middle-class earners in each state is applied.

Provider Tax Budgetary Impact: A preliminary nationwide estimate of state costs of reduced provider tax authority was derived using estimates of state hospital and MCO provider tax rates from the Kaiser Family Foundation, supplemented by Tax Foundation research. Data from the Centers for Medicare and Medicaid Services (CMS) were used for state and federal Medicaid spending by state, grossed up to the appropriate years using CMS actuarial projections, and for expansion states with estimated hospital and MCO provider tax rates in excess of 3.5 percent, the loss of the reduced share was calculated against estimated expenditures against the state’s current blended traditional and expansion FMAP.

Footnotes

[1] Ruth Mason, “Delegating Up: State Conformity with the Federal Tax Base,” Duke Law Journal 62:7 (April 2013), https://scholarship.law.duke.edu/cgi/viewcontent.cgi?article=3382&context=dlj.

[2] Texas’s Margin Tax, a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. , has lagging static conformity to the IRC, but lacks any of the tax features that make OBBBA conformity relevant, and is not included in conformity counts here.

[3] Jared Walczak, “States Should Make Full Expensing Permanent to Help Curb Inflation,” Tax Foundation, Nov. 29, 2022, https://taxfoundation.org/blog/inflation-permanent-full-expensing.

[4] Alex Muresianu, “Section 179 Expensing: Good First Step?,” Tax Foundation, Aug. 23, 2023, https://taxfoundation.org/blog/section-179-expensing/.

Share this article