New Mexico Could Backslide If It Decouples from Pro-Growth Tax Policy

New Mexico’s SB 151 decouples from the OBBBA’s full expensing provision, making the state’s tax climate less competitive.

4 min read

New Mexico’s SB 151 decouples from the OBBBA’s full expensing provision, making the state’s tax climate less competitive.

4 min read

Ohio’s SB 9 will boost economic growth by conforming Ohio’s tax code to the domestic research and experimentation (R&E) immediate cost recovery provision in the One Big Beautiful Bill Act.

8 min read

State lawmakers around the country have begun their legislative sessions, and many are considering tax reform. This piece highlights some of the areas on which they are likely to focus.

4 min read

Although New York’s 2027 budget proposal avoids tax increases on income, sales, and property taxes, it is full of policy proposals that threaten the long-run integrity of the state’s finances and harm New York taxpayers.

5 min read

Several states have decoupled from GILTI by name rather than statutory citation. Lawmakers in those states should amend these statutes to ensure that their tax code does not accidentally incorporate a much more aggressive tax on international income than the tax from which they previously decoupled.

6 min read

Delaware Governor Matt Meyer’s proposal to decouple from the full expensing provision of the OBBBA would make the state’s tax code less friendly toward investment and undermine long-term growth.

5 min read

Some state lawmakers are considering decoupling from the pro-growth expensing provisions of the OBBBA due to revenue concerns, but it is valuable to recognize just how much the corporate tax base has expanded over the past decade.

6 min read

While the Council of DC is right to consider decoupling its tax code from several revenue-reducing provisions in the OBBBA, they should maintain conformity with the business expensing reforms that are strongly pro-growth, better align with sound tax principles, and primarily change the timing of revenues.

4 min read

In addition to the federal estate tax, which has a top marginal rate of 40 percent, 12 states and the District of Columbia impose estate taxes, while five states levy inheritance taxes.

8 min read

Massachusetts lawmakers should look for opportunities to reform the tax code, revamp the state’s competitiveness, and stem the tide of outmigration. This bill, by contrast, would double down on the economically uncompetitive features of the Commonwealth’s existing tax code. Aggressively expanding NCTI inclusion is not productive or competitive.

5 min read

Congress may have passed the One Big Beautiful Bill Act (OBBBA), but state lawmakers now face big choices. Most states link their tax codes to the federal system, meaning OBBBA’s provisions—good and bad—are about to ripple across state budgets.

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.

39 min read

However states choose to respond to other tax provisions of the One Big Beautiful Bill Act, they should conform to the pro-growth provisions, which represent a marked improvement in the corporate tax code.

12 min read

Alabama’s 2025 legislative session mostly demonstrates a commitment to pro-growth tax policies that enhance competitiveness and reduce compliance burdens.

4 min read

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

10 min read

New Jersey’s residents deserve tax relief, and the state must stem the tide of out-migration. Affordable reforms in the near term could pave the way for more sweeping, and competitive, reforms to take root in the future.

As the US House hashes out its “One, Big, Beautiful Bill,” statehouse lawmakers are watching closely, given the impact of both its tax and spending provisions on state budgets.

12 min read

The proposed changes to federal tax code conformity in Oregon are a good example of a change that could significantly reshape the state’s tax code in the future, despite being framed as temporary technical adjustments.

4 min read

With other states upping their game to attract ever-more-mobile people and businesses, lawmakers and the governor are not content to leave Tennessee’s business taxes in their current, uncompetitive form.

7 min read

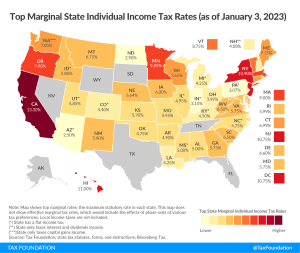

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections:

9 min read