Latest Updates

- President Trump signed the bill into law on July 4, 2025.

- New modeling to reflect the amendments made in the Senate before final passage by both chambers of Congress.

- Updated analysis of the latest version of the major tax provisions in the Senate Finance "One Big Beautiful Bill Act" Tax Plan.

The Senate Finance Committee introduced its reconciliation taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. legislation on June 16, 2025, addressing the expirations of the 2017 Tax Cuts and Jobs Act (TCJA) and making additional changes to US tax policy and spending. On June 27, 2025, the Senate released a new version of the legislative text for the One Big Beautiful Bill (OBBB). On July 1, 2025, the Senate passed the OBBB after minor adjustments, and the House of Representatives passed the identical bill on July 3, 2025. President Trump signed the bill into law on July 4, 2025.

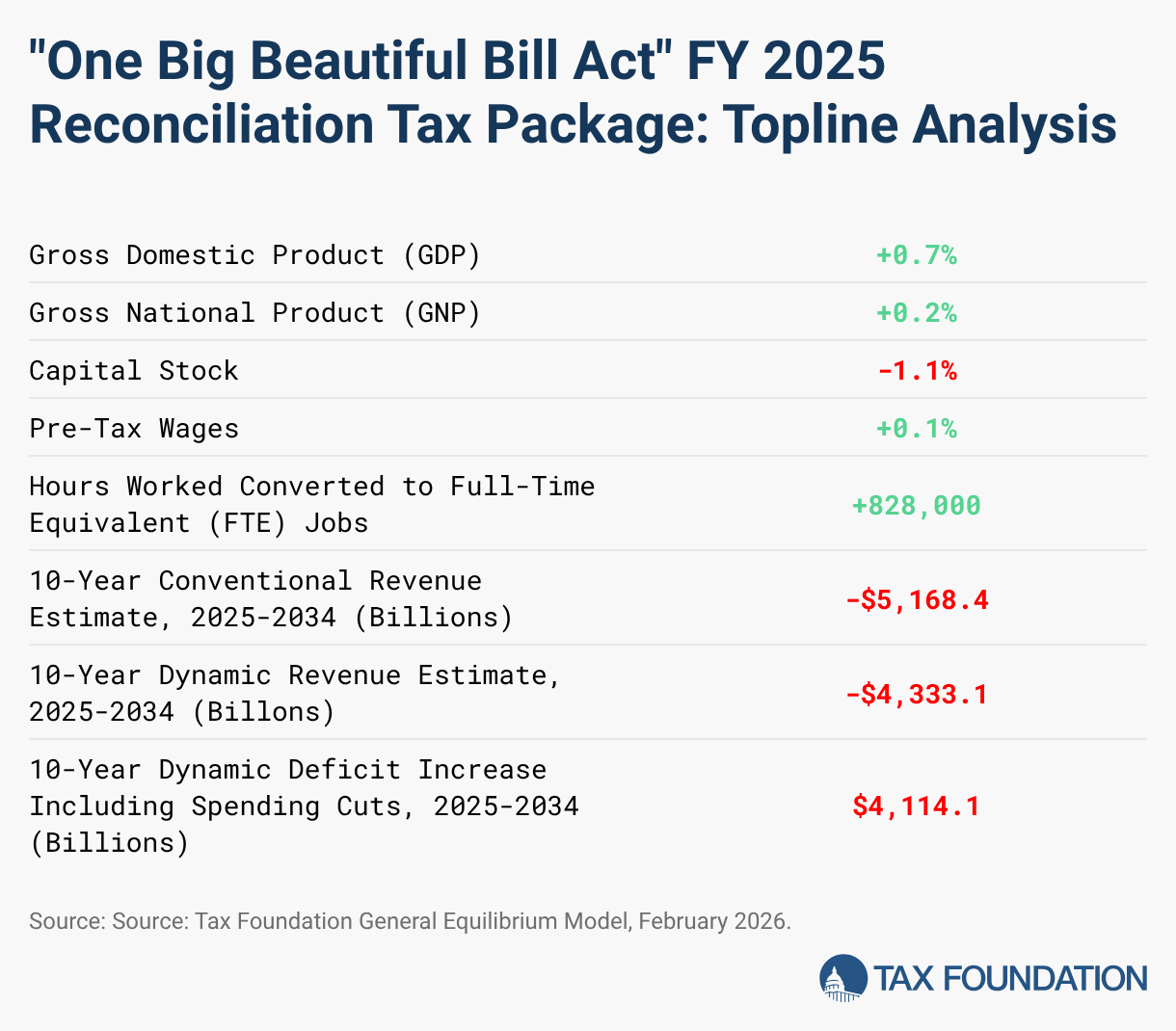

Our analysis of the major tax provisions included in the tax bill finds it would increase long-run GDP by 1.2 percent. The major tax provisions would reduce federal tax revenue by $5 trillion between 2025 and 2034, on a conventional basis. On a dynamic basis, incorporating the projected increase in long-run GDP of 1.2 percent, the dynamic score of the tax provisions falls by $940 billion to $4 trillion, meaning economic growth pays for about 19 percent of the major tax cuts.

Combined with the nearly $1.1 trillion in net spending reductions estimated by the Congressional Budget Office (CBO), we estimate the OBBB would increase federal budget deficits by $3.0 trillion from 2025 through 2034 on a dynamic basis. Further, we estimate that on a dynamic basis, increased borrowing would add $725 billion in higher interest costs over the decade, resulting in a total deficit increase of nearly $3.8 trillion on a dynamic basis.

The increased borrowing from higher deficits would reduce long-run American incomes as measured by GNP by nearly 0.6 percent, driving a wedge between the long-run effect on GDP of 1.2 percent and on GNP of 0.9 percent.

The debt-to-GDP ratio would rise by 9.6 percentage points, going from 117.1 percent in 2034 without the bill to 126.7 percent in 2034 on a conventional basis with the bill.

Overall, the bill would prevent tax increases on 62 percent of taxpayers that would occur if the TCJA expired as scheduled and significantly improve incentives to invest in the American economy. Though long-run GDP would be 1.2 percent higher under the OBBB, dynamic debt-to-GDP would increase from 162.3 percent to 175.5 percent in about 35 years, indicating the bill would bring higher economic growth as well as higher deficits and debt.

Major Provisions and Effective Dates

We model the economic, revenue, and distributional effects of the following major provisions, effective after the end of 2025 unless other dates are specified:

Individual Tax Provisions

- Make the expiring rate and bracket changes permanent and increase the inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. adjustment by an extra year for 10 percent, 12 percent, and 22 percent brackets.

- Make the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. increase permanence with an enhancement, starting in 2025 at $31,500 for joint filers, $23,625 for head of household, and $15,750 for all other filers, inflation adjusted thereafter.

- Make the personal exemption elimination permanent.

- Temporarily add a senior deduction of $6,000 for each qualifying individual for both itemizers and non-itemizers that phases out when modified adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, including inventory and certain labor costs. exceeds $75,000, available from 2025 through 2028.

- Make the expiring child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. permanent with an increased maximum of $2,200 in 2026, inflation adjusted thereafter.

- Make the $750,000 principal limit for the home mortgage interest deductionThe mortgage interest deduction is an itemized deduction for interest paid on home mortgages. It reduces households’ taxable incomes and, consequently, their total taxes paid. The Tax Cuts and Jobs Act (TCJA) reduced the amount of principal and limited the types of loans that qualify for the deduction. permanent.

- Temporarily increase the cap on the itemized deductionItemized deductions allow individuals to subtract designated expenses from their taxable income and can be claimed in lieu of the standard deduction. Itemized deductions include those for state and local taxes, charitable contributions, and mortgage interest. An estimated 13.7 percent of filers itemized in 2019, most being high-income taxpayers. for state and local taxes (SALT) to $40,000 for 2025 and increase the cap by 1 percent from that level through 2029, subject to a phaseout for taxpayers with incomes above $500,000, then reduce the cap to a flat $10,000 thereafter.

- Make other changes and limitations to itemized deduction permanent, including the limitation on personal casualty losses, termination of the miscellaneous itemized deduction (except for educator expenses), Pease limitation on itemized deductions, and certain moving expenses (except for active-duty members of the armed forces and members of the intelligence community).

- Limit the value of itemized deductions to 35 cents on the dollar for taxpayers in the top tax bracket.

- Make the increase in the alternative minimum tax (AMT) exemption permanent; revert AMT exemption phaseout thresholds to 2018 levels of $500,000 for single filers and $1 million for joint returns, indexed for inflation thereafter; increase the phaseout rate.

- Create a 0.5 percent floor on itemized deductions for charitable contributions.

- Create a permanent $1,000 above-the-line deduction for charitable contributions ($2,000 for joint filers).

- Repeal several Inflation Reduction Act green energy tax credits primarily aimed at individuals, such as electric vehicle and residential energy efficiency credits, either after 2025 or within a year of the law’s enactment.

- Temporarily make up to $25,000 of tip income deductible for individuals in traditionally and customarily tipped industries for tax years 2025 through 2028; deduction phases out at a 10 percent rate when adjusted gross income exceeds $150,000 ($300,000 for joint filers).

- Temporarily make up to $12,500 ($25,000 for joint filers) of the premium portion of overtime compensation deductible for itemizers and non-itemizers for tax years 2025 through 2028; the deduction phases out at a 10 percent rate when adjusted gross income exceeds $150,000 ($300,000 for joint filers).

- Temporarily make auto loan interest deductible for itemizers and non-itemizers for new autos with final assembly in the United States for tax years 2025 through 2028; deduction limited to $10,000 and phases out at a 20 percent rate when income exceeds $100,000 for single filers and $200,000 for joint filers.

Estate Tax Provisions

- Permanently increase the estate and lifetime gift tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. to an inflation-indexed $15 million for single filers and $30 million for joint filers beginning in 2026.

Business Tax Provisions

- Permanently restore immediate expensing for domestic research and development (R&D) expenses; small businesses with gross receipts of $31 million or less can retroactively expense R&D back to after 12/31/21; all other domestic R&D between 12/21/21 and 1/1/25 can accelerate remaining deductions over a one- or two-year period.

- Permanently reinstate the EBITDA-based limitation on business net interest deductions.

- Permanently restore 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for short-lived investments.

- Temporarily provide 100 percent expensing of qualifying structures, with the beginning of construction occurring after Jan. 19, 2025, and before Jan. 1, 2029, and placed in service before Jan. 1, 2031.

- Make the Section 199A pass-through deduction permanent; increase phase-in range of limitation by $50,000 for non-joint returns and $100,000 for joint returns; create a minimum deduction of $400 for taxpayers with $1,000 or more of qualified business income (QBI) for material participants.

- Implement a 1 percent floor on deduction of charitable contributions made by corporations.

- Eliminate clean electricity production credit (45Y) and investment credit (48E) for projects placed in service after 2027, except for projects that begin construction within 12 months of passage and baseload power sources such as nuclear, hydropower, geothermal, and battery storage; introduce restrictions related to foreign entities of concern (FEOC).

- Extend the clean fuel production credit (45Z) until 2030 and expand eligibility.

- Introduce FEOC restrictions for several other credits, including the nuclear production credit (45U), the clean fuel production credit (45Z), the carbon oxide sequestration credit (45Q), and the advanced manufacturing production credit (45X); alter phaseouts and eligibility for 45X and 45Q.

- Require intangible drilling and development costs to be taken into account for the purposes of computing adjusted financial statement income.

- Add income from hydrogen storage, carbon capture, advanced nuclear, hydropower, and geothermal energy to qualifying income of certain publicly traded partnerships treated as C corporations.

International Tax Provisions

- Rename GILTI to Net CFC Tested Income (NCTI) and establish a 12.6 percent to 14 percent top rate after foreign tax credit treatment. Eliminate indirect expense allocation, raise foreign tax creditability to 90 percent, and remove the QBAI (qualified business asset investment) exclusion for the deemed return on physical capital. Also includes some miscellaneous base broadeners that we do not model.

- Rename FDII to Foreign-Derived Deduction Eligible Income (FDDEI), and establish a 14 percent rate, with parallel changes to those in GILTI.

- Raise the BEAT rate to 10.5 percent and preserve current policy on allowability of US tax credits under BEAT.

We incorporate revenue scores from the Joint Committee on Taxation (JCT) for all other provisions not scored by Tax Foundation. To incorporate the effects of spending changes on the federal government’s budget, we will rely on CBO estimates of non-interest spending changes in the bill.

Provisions not explicitly modeled include, but are not limited to:

- Make permanent the CFC “Look-Through” Rule.

- Establish a 1 percent remittances tax, with many more transactions presumed exempt than under the House version.

- Change rules for premium tax credits (PTCs), the CTC, and the earned income tax credit (EITC).

- Expand the Section 179 expensing cap to an inflation-adjusted $2.5 million with a phasedown starting when the cost of qualifying property exceeds an inflation-adjusted $4 million; applies after Dec. 31, 2024.

- Raise the tax on student-adjusted endowment of certain private colleges and universities in a new bracketed structure with a top rate of 8 percent, exempting institutions with fewer than 3,000 full-time students.

- Expand the Section 4960 tax on excess compensation to any employee of an applicable tax-exempt organization that receives remuneration in excess of $1 million

Long-Run Economic Effects

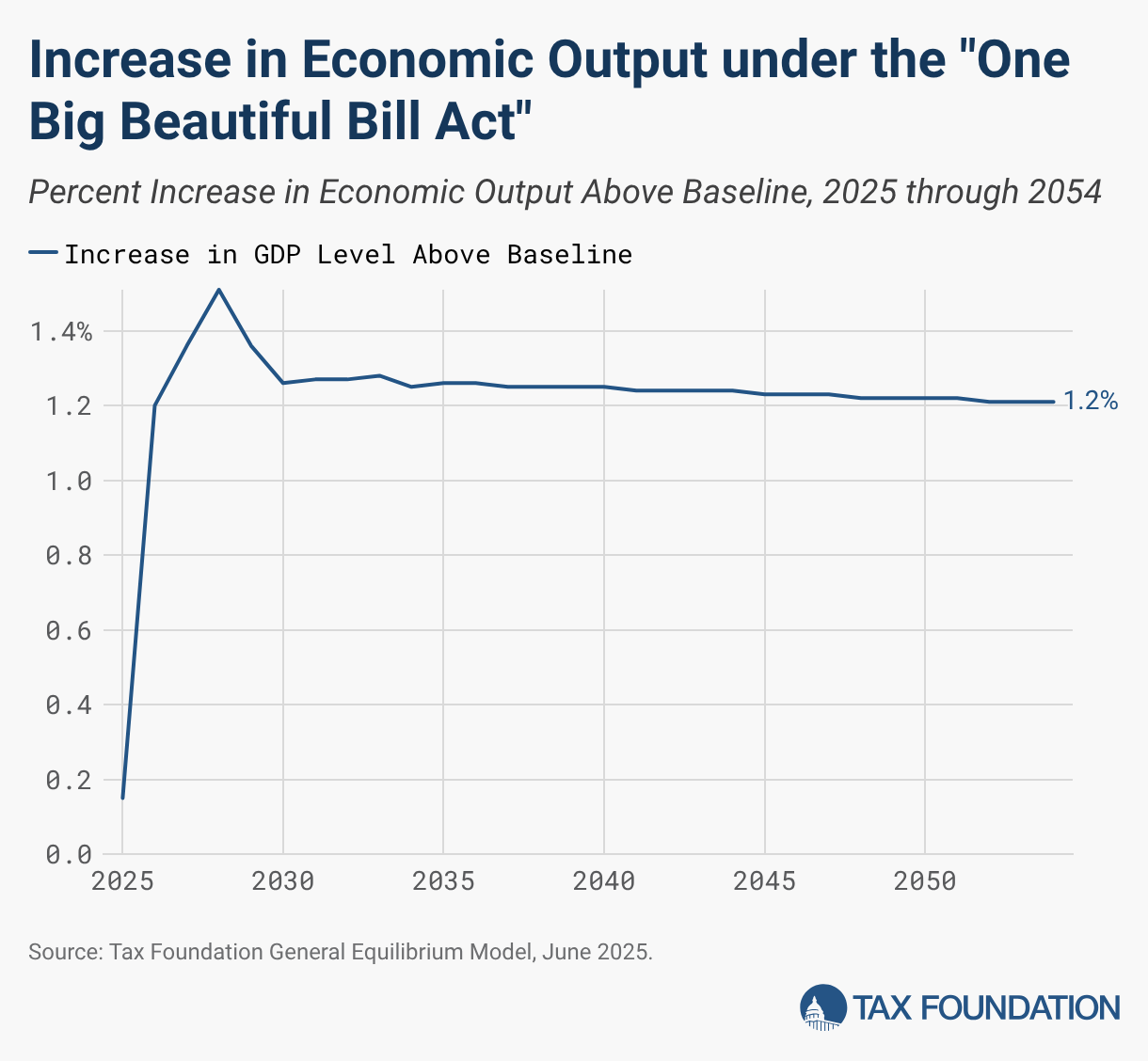

We estimate, on a preliminary basis, the major tax provisions we modeled would lower marginal tax rates on work, saving, and investment in the United States, leading to a 1.2 percent expansion in the size of the long-run economy. The capital stock would grow by 0.7, and pre-tax wages would grow by 0.4 percent. Hours worked would expand by 938,000 full-time equivalent jobs.

Though economic output would expand due to increased incentives to work, save, and invest, American incomes would not rise to the same degree. The bill would increase federal borrowing by pushing deficits $3.8 trillion higher (including added interest costs, on a dynamic basis) over the next decade, and increased foreign claims on future US output would reduce American incomes by nearly 0.6 percent, leaving American incomes 0.9 percent higher.

By the end of the budget window, debt-to-GDP would rise by 9.6 percentage points, increasing from 117.1 percent in 2034 without the bill to 126.7 percent in 2034 on a conventional basis with the bill. In the long run, dynamic debt-to-GDP would increase by 13.2 percentage points from 162.3 percent under the baseline to 175.5 percent under the OBBB.

Table 1. Preliminary Long-Run Economic Effects of Major Tax Provisions in the One Big Beautiful Bill Act

| Provision | GDP | GNP | Capital Stock | Pre-Tax Wages | Hours Worked Converted to FTE Jobs |

|---|---|---|---|---|---|

| TCJA Ordinary Rates and Brackets Permanence | 1.1% | 1.2% | 1.2% | 0.1% | 1.2 million |

| Ordinary Rates and Brackets Inflation Adjustment | Less than +0.05% | Less than +0.05% | Less than +0.05% | Less than +0.05% | 7,000 |

| TCJA AMT Permanence, Phaseout Threshold Adjustment, and Increased Phaseout Threshold Rate | Less than -0.05% | -0.1% | 0.2% | 0.1% | -132,000 |

| Permanent TCJA Standard Deduction Increase | -0.1% | Less than -0.05% | -0.6% | -0.2% | 69,000 |

| Permanent Further Standard Deduction Expansion | Less than -0.05% | Less than -0.05% | -0.1% | Less than -0.05% | 10,000 |

| TCJA Repeal of Personal Exemptions Permanence | -0.2% | -0.2% | -0.2% | -0.1% | -169,000 |

| TCJA CTC Permanence | Less than +0.05% | Less than +0.05% | 0.1% | Less than +0.05% | 31,000 |

| $2,200 CTC Expansion, CTC Inflation Adjustments, And CDCTC Expansion | Less than +0.05% | Less than +0.05% | Less than +0.05% | Less than +0.05% | 4,000 |

| $40,000 SALT Cap (2025-2029) with a 30% Phasedown to $10,000 SALT Cap Over $500K Income, $10,000 SALT Cap from 2030 Onward | -1.0% | -0.8% | -2.3% | -0.7% | -488,000 |

| TCJA $750K Home Mortgage Interest Deduction Limit Permanence | -0.1% | Less than -0.05% | -0.2% | -0.1% | -15,000 |

| TCJA Misc. Itemized Deduction Change Permanence | Less than -0.05% | Less than -0.05% | -0.1% | Less than -0.05% | -24,000 |

| TCJA Repeal of Pease Limitation Permanence | 0.1% | 0.1% | 0.1% | Less than +0.05% | 30,000 |

| TCJA 20% 199A Permanence and Changes to Phaseout Threshold Lengths | 0.5% | 0.4% | 0.9% | 0.4% | 136,000 |

| Temporary $6,000 Additional Senior Deduction with a 6% Phaseout for Incomes Over $75K Single/$150K Joint | 0.0% | 0.0% | 0.0% | 0.0% | 0 |

| Temporary Deduction for Overtime and Tip Income | 0.0% | 0.0% | 0.0% | 0.0% | 0 |

| Permanent Above the Line Charitable Deduction and Permanent 0.5 Percent of AGI Floor on Itemized Charitable Deductions | Less than -0.05% | Less than -0.05% | -0.1% | Less than -0.05% | 1,600 |

| Itemized Deductions Limited To 35% In Value for High Earners | 0.0% | 0.0% | 0.0% | 0.0% | 0 |

| Change Estate Tax Exemption To $15M Single / $30M Joint Indexed for Inflation In 2026 | 0.0% | Less than +0.05% | 0.0% | 0.0% | 0 |

| Designate a 1% floor on corporate charitable deductions | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -1,000 |

| Limitation On Excess Business Losses of Noncorporate Taxpayers | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | -2,000 |

| Implement Aggregation Rules For 162(M) Highly Compensated Employee Deduction Limits | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -1,000 |

| Permanent Domestic R&D Expensing with Retroactive Expensing for Certain Taxpayers | 0.1% | 0.1% | 0.2% | 0.1% | 33,000 |

| Permanent 100 Percent Bonus Depreciation | 0.6% | 0.5% | 1.0% | 0.5% | 145,000 |

| Temporary 100 Percent Depreciation Deduction for Certain Structures | 0.0% | 0.0% | 0.0% | 0.0% | 0 |

| Permanent Interest Limitation Set At 30% Of EBITDA Rather Than EBIT | 0.1% | 0.1% | 0.2% | 0.1% | 23,000 |

| International Changes To GILTI, FDII, And BEAT | 0.2% | 0.2% | 0.4% | 0.2% | 61,000 |

| Total Before Deficit Impact | 1.2% | 1.5% | 0.7% | 0.4% | 938,000 |

| Impact of Deficit on American Incomes | - | -0.6% | - | - | - |

| Total Including Deficit Impact | 1.2% | 0.9% | 0.7% | 0.4% | 938,000 |

Source: Tax Foundation General Equilibrium Model, June 2025.

In the short-run, the tax provisions would increase GDP by about 0.2 percent in 2025, rising to 1.2 percent in 2026 up to a peak of 1.5 percent in 2028 before falling and stabilizing at the long-run GDP increase of 1.2 percent. Temporary tax provisions including tax deductions for overtime and tipped income along with temporary expensing for structures would boost GDP from 2025 to 2028 before phasing out.

10-Year Revenue Effects

We estimate the major tax provisions modeled would reduce federal revenues by $5.0 trillion between 2025 and 2034. Most of the revenue reduction comes after 2025, when the major provisions of the TCJA are scheduled to sunset.

On a dynamic basis, incorporating the projected increase in long-run GDP of 1.2 percent, the revenue loss falls by about 19 percent, or $940 billion, to $4.1 trillion over the 10-year budget window.

Incorporating the CBO’s estimates of changes in non-interest spending, which total nearly $1.1 trillion over the decade, the OBBB would increase deficits by $3.0 trillion from 2025 through 2034 on a dynamic basis, before added interest costs.

We estimate additional borrowing due to higher deficits would increase interest costs by $917 billion on a conventional basis or by $725 billion on a dynamic basis. Incorporating the changes in interest spending, the OBBB would increase total deficits over the 2025 through 2034 budget window by $4.9 trillion on a conventional basis or by $3.8 trillion on a dynamic basis.

We provide a detailed revenue table above, available for download.

Table 2. Preliminary Revenue Effects of Major Provisions in the One Big Beautiful Bill Act

| 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2025-2034 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Conventional Total, Tax Revenue Effect | -$294.6 | -$627.5 | -$595.1 | -$587.3 | -$492.1 | -$439.5 | -$459.1 | -$475.4 | -$520.8 | -$549.8 | -$5,041.3 |

| Dynamic Total, Tax Revenue Effect | -$262.0 | -$540.1 | -$491.4 | -$466.8 | -$393.4 | -$347.4 | -$362.1 | -$373.4 | -$423.6 | -$444.2 | -$4,104.4 |

| Net Non-Interest Spending Changes (Scored by CBO) | -$124.3 | $13.7 | -$8.2 | -$48.1 | -$83.0 | -$123.3 | -$159.0 | -$181.9 | -$198.9 | -$155.4 | -$1,068.3 |

| Conventional Deficit Increase of Senate Finance Bill Before Interest Changes | $170.3 | $641.3 | $586.9 | $539.2 | $409.1 | $316.2 | $300.1 | $293.5 | $321.9 | $394.5 | $3,973.0 |

| Dynamic Deficit Increase of Senate Finance Bill Before Interest Changes | $137.7 | $553.8 | $483.2 | $418.7 | $310.4 | $224.1 | $203.1 | $191.6 | $224.7 | $288.8 | $3,036.1 |

| Increased Interest Costs from Additional Borrowing, Conventional | $7.0 | $32.2 | $56.0 | $77.6 | $93.9 | $106.1 | $117.7 | $129.1 | $141.4 | $156.2 | $917.3 |

| Increased Interest Costs from Additional Borrowing, Dynamic | $5.7 | $27.7 | $47.4 | $64.4 | $76.5 | $84.9 | $92.5 | $99.6 | $107.8 | $118.1 | $724.6 |

| Conventional Deficit Increase of Senate Finance Bill Including Interest Changes | $177.3 | $673.5 | $642.9 | $616.8 | $503.0 | $422.3 | $417.9 | $422.6 | $463.3 | $550.7 | $4,890.2 |

| Dynamic Deficit Increase of Senate Finance Bill Including Interest Changes | $143.4 | $581.5 | $530.6 | $483.1 | $387.0 | $309.0 | $295.6 | $291.2 | $332.4 | $407.0 | $3,760.7 |

If the expiring TCJA tax provisions are instead included in the baseline, we estimate the tax provisions in the package would reduce revenue by about $974 billion on a conventional basis from 2025 to 2034. The $974 billion cost relative to a current policy baseline is on top of the $4 trillion to permanently extend the TCJA individual, estate, and international provisions on a current law baseline.

Distributional Effects

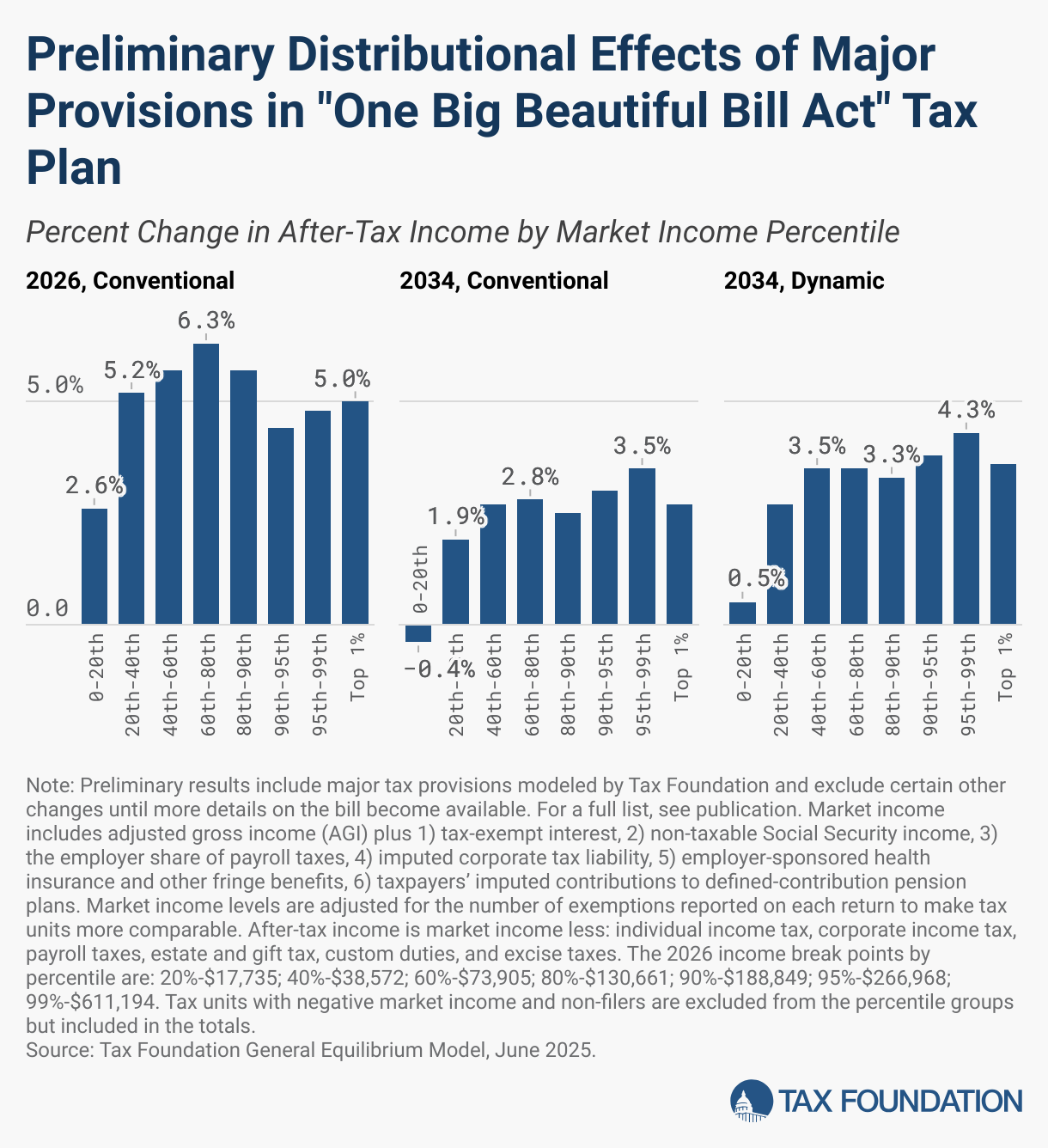

We distribute the tax burden of the major tax provisions explicitly modeled by Tax Foundation as well as several of the provisions modeled by the JCT, including changes to the eligibility of the CTC, EITC, and PTCs. We estimate the tax bill would increase after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. by 2.9 percent in 2025 and 5.4 percent in 2026. The income increase is higher in 2026 because the TCJA individual tax provisions are not scheduled to expire until after the end of 2025.

Because several tax cuts are available only on a temporary basis, the tax bill would raise market incomes by a smaller 2.8 percent in 2034. However, factoring in the economic growth driven by the plan’s permanent provisions, the bill would raise market incomes by 3.6 percent in 2034 on a dynamic basis.

Middle-income quintiles see the largest income increases in 2026 due to the combination of the individual TCJA extensions and the handful of targeted tax breaks for specific types of income, like overtime and tips as well as the bonus deduction for seniors (which provide large tax reductions to targeted groups of taxpayers in the middle quintile).

Meanwhile, larger after-tax incomes in 2034 are attributable to the permanent individual cuts from TCJA, permanent enhancements of certain provisions, as well as permanent expensing for equipment and R&D investment.

After-tax income for the bottom quintile in 2034 falls by 0.4 percent on a conventional basis as tighter rules for premium tax credits, the earned income credit, and the child tax credit take effect. However, after accounting for economic growth, after-tax income for the bottom quintile increases by 0.5 percent in 2034.

Table 3. Preliminary Distributional Effects of Major Provisions in the One Big Beautiful Bill Act

| Market Income Percentile | 2025, Conventional | 2026, Conventional | 2034, Conventional | 2034, Dynamic |

|---|---|---|---|---|

| 0% - 20.0% | 1.5% | 2.6% | -0.4% | 0.5% |

| 20.0% - 40.0% | 3.1% | 5.2% | 1.9% | 2.7% |

| 40.0% - 60.0% | 3.6% | 5.7% | 2.7% | 3.5% |

| 60.0% - 80.0% | 3.9% | 6.3% | 2.8% | 3.5% |

| 80.0% - 100% | 2.3% | 5.0% | 2.9% | 3.8% |

| 80.0% - 90.0% | 3.7% | 5.7% | 2.5% | 3.3% |

| 90.0% - 95.0% | 1.9% | 4.4% | 3.0% | 3.8% |

| 95.0% - 99.0% | 1.5% | 4.8% | 3.5% | 4.3% |

| 99.0% - 100% | 2.1% | 5.0% | 2.7% | 3.6% |

| Total | 2.9% | 5.4% | 2.8% | 3.6% |

Source: Tax Foundation General Equilibrium Model, June 2025.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe