Latest Updates

- Updated modeling and analysis of the House-passed “One, Big, Beautiful” reconciliation bill

- Updated analysis of the House-passed “One, Big, Beautiful” reconciliation bill on May 22, 2025.

The House passed the “One, Big, Beautiful” reconciliation bill on Thursday, May 22, addressing the expirations of the 2017 TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Cuts and Jobs Act (TCJA) and making additional changes to US tax policy and spending

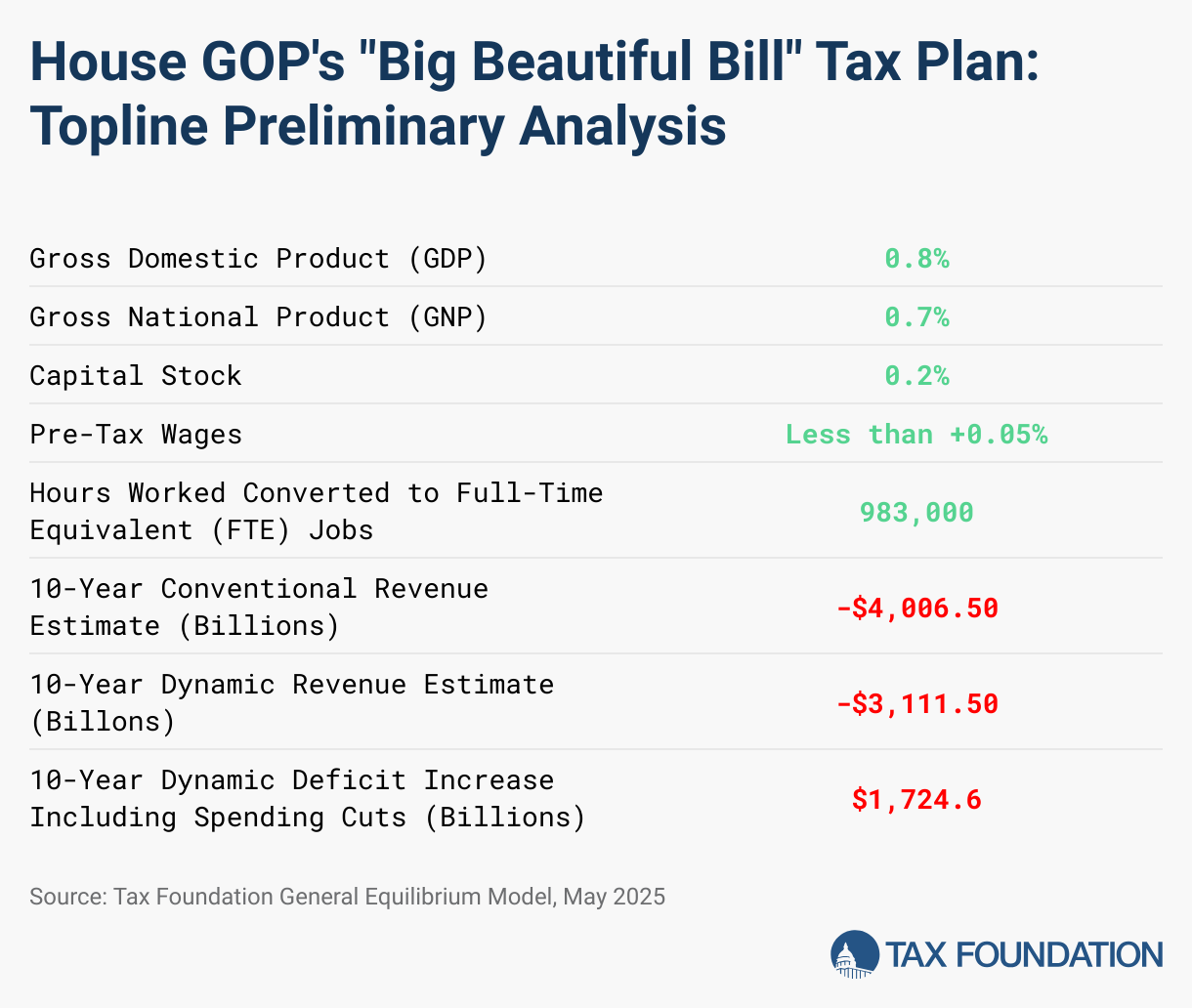

Our analysis finds the tax provisions included in the House-passed bill would increase long-run GDP by 0.8 percent. The bill’s provisions would reduce federal tax revenue by $4 trillion between 2025 and 2034, on a conventional basis. On a dynamic basis, incorporating the projected increase in long-run GDP of 0.8 percent, the dynamic score of the tax provisions falls to $3.1 trillion, meaning economic growth pays for 22 percent of the tax cuts. The bill’s net spending cuts of about $1.5 trillion offset some of the revenue reduction, leading to a total budget deficit increase of $1.7 trillion over 10 years on a dynamic basis.

Overall, the bill would prevent tax increases on 62 percent of taxpayers that would occur if the TCJA expired as scheduled. However, by introducing narrowly targeted new provisions and sunsetting the most pro-growth provisions, like bonus depreciation and research and development (R&D) expensing, it leaves economic growth on the table and complicates the structure of the tax code.

The House-passed budget resolution (which contains the instructions that committees must follow for the reconciliation process) would allow a $4.5 trillion increase in the deficit from tax cuts over the next decade so long as spending is cut by $1.7 trillion. But if spending is not cut by $1.7 trillion, the cap on tax cuts will be reduced dollar-for-dollar. The House-passed bill as currently estimated meets the requirements of the budget resolution.

Table 1. Summary of Preliminary Long-Run Economic and 10-Year Revenue Effects of House Reconciliation Bill Tax Package

| 10-Year Conventional Revenue Estimate (Billions) | 10-Year Dynamic Revenue Estimate (Billons) | 10-Year Dynamic Deficit Increase Including Spending Cuts (Billions) | Long-Run GDP | Long-Run GNP | Long-Run Wages | Long-Run Hours Worked Converted to FTE Jobs |

|---|---|---|---|---|---|---|

| -$4,006.5 | -$3,111.5 | $1,724.6 | +0.8% | +0.7% | Less than +0.05% | 983,000 |

Major Provisions and Effective Dates

We model the economic, revenue, and distributional effects of the following major provisions, effective after the end of 2025 unless other dates are specified:

Individual Provisions

- Make the expiring rate and bracket changes of the TCJA permanent and increase the inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. adjustment for all brackets excluding the 37 percent threshold

- Make the expiring standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. levels permanent and temporarily boost the standard deduction by $2,000 for joint filers, $1,500 for head of household filers, and $1,000 for all other filers from 2025 through the end of 2028

- Make the personal exemption elimination permanent

- Make the $750,000 limitation and the exclusion of interest on home equity loans for the home mortgage interest deductionThe mortgage interest deduction is an itemized deduction for interest paid on home mortgages. It reduces households’ taxable incomes and, consequently, their total taxes paid. The Tax Cuts and Jobs Act (TCJA) reduced the amount of principal and limited the types of loans that qualify for the deduction. permanent\

- Make the state and local tax (SALT) deduction cap permanent at a higher threshold of $40,000, phasing down to $10,000 at a rate of 30 percent beginning at modified adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.” of $250,000 for single filers and $500,000 for joint filers. The cap and income thresholds increase by 1 percent per year over the next 10 years.

- Make other changes and limitations to itemized deductions permanent, including: the limitation on personal casualty losses and wagering losses and termination of miscellaneous itemized deductions, Pease limitation on itemized deductions, and certain moving expenses

- Limit the value of itemized deductions to 32 or 35 cents on the dollar for those in the top tax bracket

- Make the expiring child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. permanent; temporarily increase the maximum credit to $2,500 from 2025 through the end of 2028; inflation adjust the $2,000 max in years thereafter

- Make the increase in the alternative minimum tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. and phaseout thresholds permanent and adjust related inflation indexingInflation indexing refers to automatic cost-of-living adjustments built into tax provisions to keep pace with inflation. Absent these adjustments, income taxes are subject to “bracket creep” and stealth increases on taxpayers, while excise taxes are vulnerable to erosion as taxes expressed in marginal dollars, rather than rates, slowly lose value. calculations

- Repeal several Inflation Reduction Act (IRA) green tax subsidies primarily aimed at individuals, such as electric vehicle and residential energy efficiency credits, after 2025

- Temporarily make tip income deductible for tax years 2025 through 2028 for individuals in traditionally and customarily tipped industries, excluding highly compensated employees

- Temporarily make auto loan interest deductible for itemizers and non-itemizers for autos with final assembly in the United States for tax years 2025 through 2028; deduction limited to $10,000 and phases out by $200 for every $1,000 of income above $100,000 for single filers and $200,000 for joint filers

- Temporarily increase the additional standard deduction for seniors by $4,000 for tax years 2025 through 2028 and extend the increase to itemizers; larger deduction phases out at a 4 percent rate when modified adjusted gross income exceeds $75,000 for single filers and $150,000 for joint filers

- Temporarily make overtime compensation deductible for the premium portion of overtime for itemizers and non-itemizers for tax years 2025 through 2028, excluding highly compensated employees and qualified tips

- Tighten rules on claims for premium tax credits (PTCs), the child tax credit, and the earned income tax credit (EITC). Repeal limitations on PTC clawbacks for credits advanced to taxpayers

Estate Provisions

- Permanently increase the estate and gift taxA gift tax is a tax on the transfer of property by a living individual, without payment or a valuable exchange in return. The donor, not the recipient of the gift, is typically liable for the tax. exemption to an inflation-indexed $15 million beginning in 2026

Business and International Provisions

- Permanently reduce the post-2025 global intangible low taxed income (GILTI) inclusion rate from 62.5 percent to 50.8 percent, increase the foreign-derived intangible income (FDII) deduction from 21.875 percent to 36.5 percent, and reduce the base erosion and anti-abuse tax (BEAT) rate from 12.5 percent to 10.1 percent.

- Make the Section 199A pass-through deduction permanent; increase the deduction percentage from 20 percent to 23 percent; modify the limitations based on W-2 wages and capital investment and for specified services and trade businesses (SSTBs)

- Close SALT cap workarounds for pass-through businesses that are considered SSTBs under Section 199A

- Make the noncorporate loss limitation permanent and tighten related rules

- Sunset major IRA clean electricity tax credits: clean electricity production tax credit (45Y) and clean electricity investment tax credit (48E) eliminated for projects for which construction begins more than 60 days after enactment or property placed in service after 2028, except for advanced nuclear projects under construction before 2029; nuclear electricity production tax credit (45U) eliminated after 2031; repeal hydrogen production credit (45V) for facilities beginning construction after 2025

- Phase out advanced manufacturing production credit (45x) for wind energy components after 2027, for all other eligible components after 2031

- Across several IRA green energy credits, further restrict credits based on involvement of foreign entities of concern (FEOC)

- Expand clean fuel production credit (45K)

- Tighten rules on the 162(m) limitation for executive compensation

- Limit deductibility of C corporation charitable contributions by implementing a 1 percent floor on the deduction

- Temporarily restore 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for short-lived investment from 2025 through 2029

- Temporarily restore immediate expensing for domestic research and development (R&D) expenses from 2025 through 2029

- Temporarily reinstate the EBITDA-based limitation on business net interest deductions from 2025 through 2029

- Temporarily provide 100 percent expensing of qualifying structures in manufacturing, extraction, and agriculture sectors for which construction begins before the end of 2028 and placed in service date occurs before the end of 2032

We incorporate revenue scores from the Joint Committee on Taxation for all other provisions not scored by Tax Foundation, including higher taxes on endowments and private foundations and other various rule changes. We incorporate spending change estimates from the Congressional Budget Office to estimate the full effect of the House bill on the budget deficit.

Long-Run Economic Results

We estimate that together, the major tax provisions we modeled would lower marginal tax rates on work in the United States, leading to a 0.8 percent expansion in the size of the long-run economy. The capital stock would grow by 0.2 percent, and pre-tax wages would grow by less than 0.05 percent. The capital stock and wages grow less than the broader economy due to higher marginal tax rates on housing investment under the limitations on itemized deductions. Hours worked would expand by 983,000 full-time equivalent jobs.

American incomes measured by GNP would increase by 0.7 percent. The deficit impact of the bill drives a wedge of 0.3 percent between the increase in economic output and the increase in American incomes.

The tax and spending provisions would increase the budget deficit by $1.7 trillion from 2025 through 2034 on a dynamic basis, and that higher budget deficit would require the US government to borrow more. As interest payments on the debt made to foreigners increase, American incomes decrease.

Table 2. Long-Run Economic Effects of House Reconciliation Bill Tax Package

| GDP | GNP | Capital Stock | Pre-Tax Wages | Hours Worked Converted to FTEs | |

|---|---|---|---|---|---|

| Lower rates and wider thresholds on certain brackets and inflation adjustments | 1.1% | 1.2% | 1.2% | 0.1% | 1,233,000 |

| AMT exemption and exemption threshold changes | -0.1% | -0.1% | Less than +0.05% | 0.1% | -125,000 |

| Larger standard deduction and inflation adjustments | -0.1% | 0.0% | -0.6% | -0.2% | 72,000 |

| No personal exemptions | -0.2% | -0.2% | -0.2% | Less than -0.05% | -166,170 |

| Permanence for TCJA child tax credit and other dependent tax credit expansion and inflation adjustments | 0.1% | 0.1% | 0.1% | 0.0% | 32,000 |

| $40,000 Cap on State and Local Tax Deductions, increased 1% annually for 10 years | -0.5% | -0.4% | -0.9% | -0.3% | -193,000 |

| Phase down $40,000 SALT cap to $10,000 at a 30% rate when income exceeds $500,000 | -0.1% | Less than -0.05% | -0.2% | -0.1% | -20,000 |

| Disallow SALT deduction cap workarounds for certain income | -0.1% | -0.1% | -0.3% | -0.1% | -37,000 |

| Other limitations on itemized deductions and Pease limitation repeal | -0.1% | Less than -0.05% | -0.3% | -0.1% | -18,000 |

| Section 199A pass-through deduction permanence at 23% deduction rate | 0.6% | 0.5% | 1.0% | 0.4% | 157,000 |

| Limit the value of itemized deductions for high earners | Less than -0.05% | Less than -0.05% | Less than -0.05% | 0.0% | -1,000 |

| Designate a 1% floor on corporate charitable deductions | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | -2,000 |

| Retain modified current policy GILTI, FDII, and BEAT rates | 0.2% | 0.2% | 0.4% | 0.2% | 52,000 |

| Make existing estate tax thresholds permanent and raise the estate tax exemption to $15 million (single) and $30 million (joint), indexed for inflation starting in 2026 | 0.0% | 0.0% | 0.0% | 0.0% | - |

| Make permanent and establish changes to the limitation on excess business losses of noncorporate taxpayers | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | -1,000 |

| Implement aggregation rules for 162(m) highly compensated employee deduction limits | Less than -0.05% | Less than -0.05% | Less than -0.05% | Less than -0.05% | -1,000 |

| Deficit Impact on American Incomes | 0.0% | -0.3% | 0.0% | 0.0% | - |

| Total | 0.8% | 0.7% | 0.2% | Less than +0.05% | 983,000 |

10-Year Revenue Results

We estimate the tax provisions would reduce federal revenues by $4.0 trillion between 2025 and 2034. Most of the revenue reduction comes after 2025, when the major provisions of the TCJA are scheduled to sunset.

On a dynamic basis, incorporating the projected increase in long-run GDP of 0.8 percent, the revenue loss falls by about 22 percent to $3.1 trillion over the 10-year budget window.

In total, accounting for all provisions, including about $1.5 trillion in net spending cuts estimated by CBO, we estimate the House bill would increase budget deficits by $1.7 trillion on a dynamic basis over 10 years.

The projected ratio of debt to GDP would increase from a baseline level of 162.3 percent in about 35 years to 174.3 percent on a conventional basis. After factoring in the revenue feedback from economic growth, debt to GDP would rise 5.7 percentage points to 168.0 percent by that 2059 target year.

We provide a detailed revenue table above available for download.

Table 3. 10-Year Revenue Effects and Deficit Impact of House Reconciliation Bill, Billions

| 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2025-2034 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Conventional Revenue Effect of House Tax Package | -$278.0 | -$556.9 | -$571.4 | -$530.1 | -$387.1 | -$222.6 | -$290.2 | -$335.1 | -$405.5 | -$429.6 | -$4,006.5 |

| Dynamic Revenue Effect of House Tax Package | -$251.7 | -$475.1 | -$464.1 | -$406.8 | -$269.8 | -$140.0 | -$203.9 | -$245.4 | -$318.5 | -$336.3 | -$3,111.5 |

| Conventional Deficit Change of House Reconciliation Bill | -$128.2 | -$542.8 | -$522.3 | -$436.2 | -$268.3 | -$69.3 | -$109.6 | -$136.3 | -$194.1 | -$212.5 | -$2,619.6 |

| Dynamic Deficit Change of House Reconciliation Bill | -$102.0 | -$461.0 | -$414.9 | -$313.0 | -$150.9 | $13.2 | -$23.3 | -$46.5 | -$107.0 | -$119.2 | -$1,724.6 |

Distributional Effects

We model the distributional effects of the major provisions listed above. Overall, the House bill has outlined significant tax cuts that would, on average, increase market incomes by 2.1 percent in 2025 and by 4.0 percent in 2026. The difference between 2025 and 2026 is primarily because the TCJA provisions do not expire until 2026, so extending them does not have an effect in 2025.

Some business provisions and increases to individual provisions are available in the first half of the budget window but sunset by the latter half, so by 2034, the increase in after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. would be smaller at 2.3 percent on average. On a dynamic basis, we estimate that market incomes would increase by 2.9 percent on average in 2034, reflecting the increase in economic output under the plan.

The after-tax market income for the bottom quintile in 2034 falls by 0.6 percent on a conventional basis as tighter rules for premium tax credits, the earned income credit, and the child tax credit take effect. However, after accounting for economic growth, after-tax income for the bottom quintile increases by 0.1 percent in 2034.

In general, the middle quintile sees the largest gains in the initial years, with after-tax income increasing 2.6 percent in 2025 and 4.3 percent in 2026 on a conventional basis. This is largely the result of extension and expansion of the TCJA’s expiring individual tax provisions as well as the temporary exemptions for tips and overtime and the deductions for seniors and auto loans.

In 2034, the top quintile sees the largest gains, with after-tax income increasing 3.1 percent after accounting for economic growth. This is largely due to extension and expansion of the TCJA’s expiring individual tax provisions.

Table 4. Distributional Effect of Major Provisions of House Big, Beautiful Bill Tax Package, Percent Change in After-Tax Market Income

| Market Income Percentile | 2025, Conventional | 2026, Conventional | 2034, Conventional | 2034, Dynamic |

|---|---|---|---|---|

| 0% - 20% | 0.8% | 1.6% | -0.6% | 0.1% |

| 20% - 40% | 2.5% | 4.2% | 1.1% | 1.7% |

| 40% - 60% | 2.6% | 4.3% | 2.0% | 2.7% |

| 60% - 80% | 2.3% | 4.3% | 2.3% | 2.9% |

| 80% - 100% | 1.9% | 3.9% | 2.5% | 3.1% |

| 80% - 90% | 2.1% | 3.9% | 2.3% | 2.9% |

| 90% - 95% | 1.6% | 3.8% | 2.8% | 3.4% |

| 95% - 99% | 1.6% | 4.1% | 2.9% | 3.6% |

| 99% - 100% | 2.1% | 3.8% | 1.9% | 2.6% |

| Total | 2.1% | 4.0% | 2.3% | 2.9% |

Source: Tax Foundation General Equilibrium Model, May 2025 Share this article