Key Findings

- Individual income taxes are a major source of state government revenue, constituting 38 percent of state taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. collections in fiscal year 2022, the latest year for which data are available.

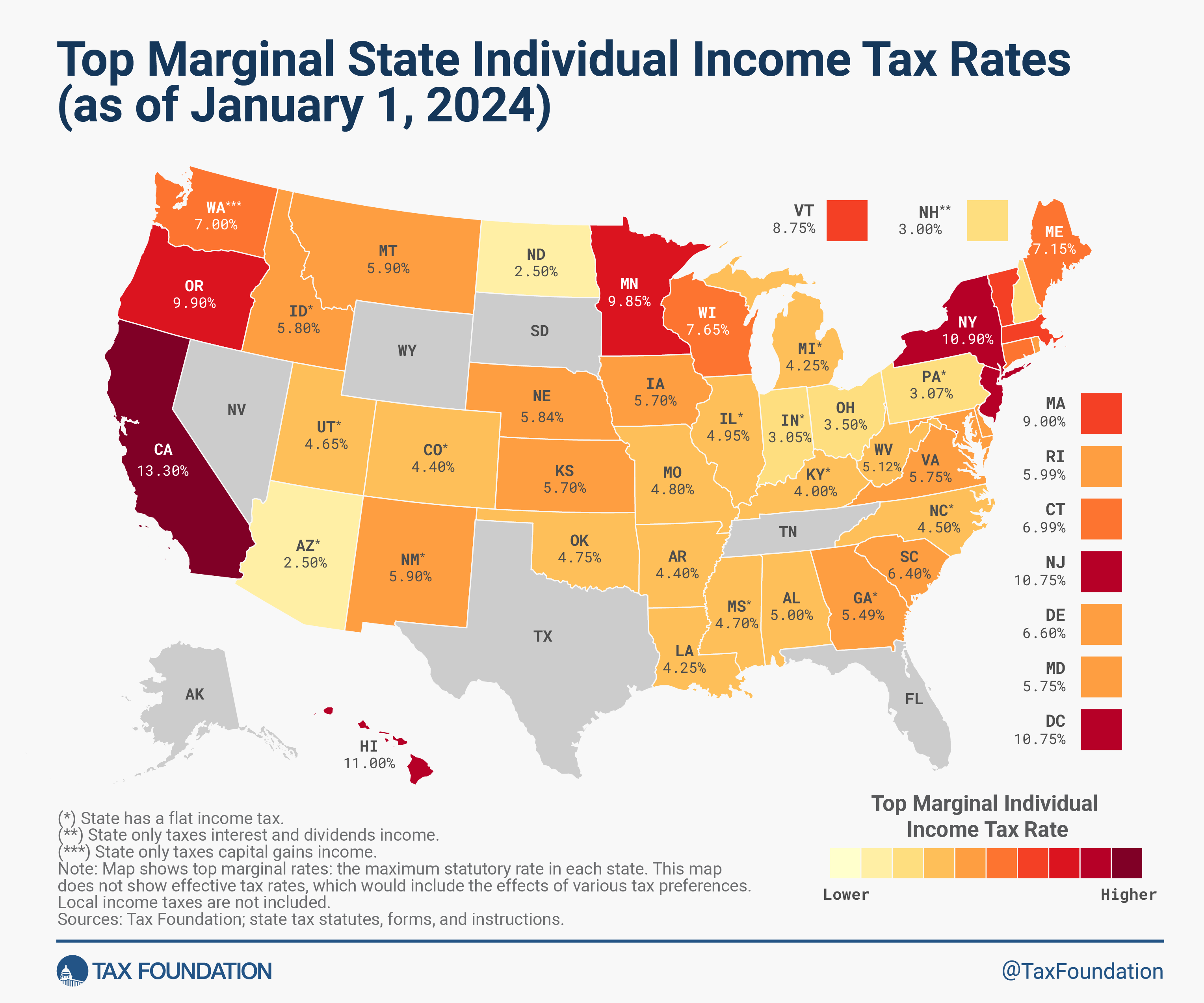

- Forty-three states and the District of Columbia levy individual income taxes. Forty-one tax wage and salary income. New Hampshire exclusively taxes dividend and interest income while Washington only taxes capital gains income. Seven states levy no individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source at all.

- Among those states taxing wages, 12 have a single-rate tax structure, with one rate applying to all taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. . Conversely, 29 states and the District of Columbia levy graduated-rate income taxes, with the number of brackets varying widely by state. Hawaii has 12 brackets, the most in the country.

- States’ approaches to income taxes vary in other details as well. Some states double their single-filer bracket widths for married filers to avoid a “marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples..” Some states index tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat., exemptions, and deductions for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin; many others do not. Some states tie their standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. and personal exemption to the federal tax code, while others set their own or offer none at all.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign UpIndividual income taxes are a major source of state government revenue, accounting for 38 percent of state tax collections. Their significance in public policy is further enhanced by individuals being actively responsible for filing their income taxes, in contrast to the indirect payment of sales and excise taxes.

Forty-three states levy individual income taxes. Forty-one tax wage and salary income. New Hampshire exclusively taxes dividend and interest income while Washington only taxes capital gains income. Seven states levy no individual income tax at all.

Of those states taxing wages, 12 have single-rate tax structures, with one rate applying to all taxable income. Conversely, 29 states and the District of Columbia levy graduated-rate income taxes, with the number of brackets varying widely by state. Montana, for example, is one of several states with a two-bracket income tax system. At the other end of the spectrum, Hawaii has 12 brackets. Top marginal rates span from Arizona’s and North Dakota’s 2.5 percent to California’s 13.3 percent. (California also imposes a 1.1 percent payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. on wage income, bringing the all-in top rate to 14.4 percent as of this year.)

In some states, a large number of brackets are clustered within a narrow income band. For example, Virginia’s taxpayers reach the state’s fourth and highest bracket at $17,000 in taxable income. In other states, the top rate kicks in at a much higher level of marginal income. For example, the top rate kicks in at or above $1 million in California (when the “millionaire’s tax” surcharge is included), Massachusetts, New Jersey, New York, and the District of Columbia.

The table below shows how each state’s individual income tax is structured. Compare states with no income tax, flat income taxes, or graduated-rate income tax.

Income Tax Structures by State

2024 State Individual Income Tax Structures

| States with No Income Tax | States with a Flat Income Tax | States with a Graduated-Rate Income Tax |

|---|---|---|

| Alaska | Arizona | Alabama |

| Florida | Colorado | Arkansas |

| Nevada | Georgia | California |

| South Dakota | Idaho | Connecticut |

| Tennessee | Illinois | Delaware |

| Texas | Indiana | Hawaii |

| Wyoming | Kentucky | Iowa |

| Michigan | Kansas | |

| Mississippi | Louisiana | |

| New Hampshire* | Maine | |

| North Carolina | Maryland | |

| Pennsylvania | Massachusetts | |

| Utah | Minnesota | |

| Washington** | Missouri | |

| Montana | ||

| Nebraska | ||

| New Jersey | ||

| New Mexico | ||

| New York | ||

| North Dakota | ||

| Ohio | ||

| Oklahoma | ||

| Oregon | ||

| Rhode Island | ||

| South Carolina | ||

| Vermont | ||

| Virginia | ||

| West Virginia | ||

| Wisconsin | ||

| Washington, DC |

Sources: Tax Foundation; state tax statutes, forms, and instructions.

States’ approaches to income taxes vary in other details as well. Some states double their single-filer bracket widths for married filers to avoid imposing a “marriage penalty.” Some states index tax brackets, exemptions, and deductions for inflation, while many others do not. Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all.

The Tax Cuts and Jobs Act (TCJA) increased the standard deduction (set at $14,600 for single filers and $29,200 for joint filers in 2024) while suspending the personal exemption by reducing it to $0 through 2025. As many states use the federal tax code as the starting point for their own standard deduction and personal exemption calculations, some states that previously linked to these provisions in the federal tax code have updated their conformity statutes in recent years. They either adopted federal changes, retained their previous deduction and exemption amounts, or maintained their own separate system while increasing the state-provided deduction or exemption amounts.

In the following tables, we have compiled the most up-to-date data available on state individual income tax rates, brackets, standard deductions, and personal exemptions for both single and joint filers. Following the tables, we document notable individual income tax changes implemented in 2024.

2024 State Income Tax Rates and Brackets

State Individual Income Tax Rates and Brackets, as of January 1, 2024

| State | Single Filer Rates | Single Filer Brackets | Married Filing Jointly Rates | Married Filing Jointly Brackets | Standard Deduction (Single) | Standard Deduction (Couple) | Personal Exemption (Single) | Personal Exemption (Couple) | Personal Exemption (Dependent) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama (a, b, c) | 2.00% | > | $0 | 2.00% | > | $0 | $3,000 | $8,500 | $1,500 | $3,000 | $1,000 |

| Alabama | 4.00% | > | $500 | 4.00% | > | $1,000 | |||||

| Alabama | 5.00% | > | $3,000 | 5.00% | > | $6,000 | |||||

| Alaska | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Arizona (e, f, u) | 2.50% | > | $0 | 2.50% | > | $0 | $14,600 | $29,200 | n.a. | n.a. | $100 credit |

| Arkansas (g, h, bb, ll) | 2.00% | > | $0 | 2.00% | > | $0 | $2,340 | $4,680 | $29 credit | $58 credit | $29 credit |

| Arkansas | 4.00% | > | $4,400 | 4.00% | > | $4,400 | |||||

| Arkansas | 4.40% | > | $8,800 | 4.40% | > | $8,800 | |||||

| California (a, h, j, k, l, m, n, oo) | 1.00% | > | $0 | 1.00% | > | $0 | $5,363 | $10,726 | $144 credit | $288 credit | $446 credit |

| California | 2.00% | > | $10,412 | 2.00% | > | $20,824 | |||||

| California | 4.00% | > | $24,684 | 4.00% | > | $49,368 | |||||

| California | 6.00% | > | $38,959 | 6.00% | > | $77,918 | |||||

| California | 8.00% | > | $54,081 | 8.00% | > | $108,162 | |||||

| California | 9.30% | > | $68,350 | 9.30% | > | $136,700 | |||||

| California | 10.30% | > | $349,137 | 10.30% | > | $698,274 | |||||

| California | 11.30% | > | $418,961 | 11.30% | > | $837,922 | |||||

| California | 12.30% | > | $698,271 | 12.30% | > | $1,000,000 | |||||

| California | 13.30% | > | $1,000,000 | 13.30% | > | $1,396,542 | |||||

| Colorado (a, o) | 4.40% | > | $0 | 4.40% | > | $0 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Connecticut ((i, p, q, r) | 2.00% | > | $0 | 2.00% | > | $0 | n.a. | n.a. | $15,000 | $24,000 | $0 |

| Connecticut | 4.50% | > | $10,000 | 4.50% | > | $20,000 | |||||

| Connecticut | 5.50% | > | $50,000 | 5.50% | > | $100,000 | |||||

| Connecticut | 6.00% | > | $100,000 | 6.00% | > | $200,000 | |||||

| Connecticut | 6.50% | > | $200,000 | 6.50% | > | $400,000 | |||||

| Connecticut | 6.90% | > | $250,000 | 6.90% | > | $500,000 | |||||

| Connecticut | 6.99% | > | $500,000 | 6.99% | > | $1,000,000 | |||||

| Delaware (a, h, m, s) | 2.20% | > | $2,000 | 2.20% | > | $2,000 | $3,250 | $6,500 | $110 credit | $220 credit | $110 credit |

| Delaware | 3.90% | > | $5,000 | 3.90% | > | $5,000 | |||||

| Delaware | 4.80% | > | $10,000 | 4.80% | > | $10,000 | |||||

| Delaware | 5.20% | > | $20,000 | 5.20% | > | $20,000 | |||||

| Delaware | 5.55% | > | $25,000 | 5.55% | > | $25,000 | |||||

| Delaware | 6.60% | > | $60,000 | 6.60% | > | $60,000 | |||||

| Florida | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Georgia | 5.49% | > | $0 | 5.49% | > | $0 | $12,000 | $24,000 | n.a. | n.a. | $3,000 |

| Hawaii (m, t) | 1.40% | > | $0 | 1.40% | > | $0 | $2,200 | $4,400 | $1,144 | $2,288 | $1,144 |

| Hawaii | 3.20% | > | $2,400 | 3.20% | > | $4,800 | |||||

| Hawaii | 5.50% | > | $4,800 | 5.50% | > | $9,600 | |||||

| Hawaii | 6.40% | > | $9,600 | 6.40% | > | $19,200 | |||||

| Hawaii | 6.80% | > | $14,400 | 6.80% | > | $28,800 | |||||

| Hawaii | 7.20% | > | $19,200 | 7.20% | > | $38,400 | |||||

| Hawaii | 7.60% | > | $24,000 | 7.60% | > | $48,000 | |||||

| Hawaii | 7.90% | > | $36,000 | 7.90% | > | $72,000 | |||||

| Hawaii | 8.25% | > | $48,000 | 8.25% | > | $96,000 | |||||

| Hawaii | 9.00% | > | $150,000 | 9.00% | > | $300,000 | |||||

| Hawaii | 10.00% | > | $175,000 | 10.00% | > | $350,000 | |||||

| Hawaii | 11.00% | > | $200,000 | 11.00% | > | $400,000 | |||||

| Idaho (m, u) | 5.8% | > | $4,489 | 5.8% | > | $8,978 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Illinois (d, m, v) | 4.95% | > | $0 | 4.95% | > | $0 | n.a. | n.a. | $2,775 | $5,550 | $2,775 |

| Indiana (a, m, w) | 3.05% | > | $0 | 3.05% | > | $0 | n.a. | n.a. | $1,000 | $2,000 | $1,000 |

| Iowa (a, d, h) | 4.40% | > | $0 | 4.40% | > | $0 | n.a. | n.a. | $40 credit | $80 credit | $40 credit |

| Iowa | 4.82% | > | $6,210 | 4.82% | > | $12,420 | |||||

| Iowa | 5.70% | > | $31,050 | 5.70% | > | $62,100 | |||||

| Kansas (a, m) | 3.10% | > | $0 | 3.10% | > | $0 | $3,500 | $8,000 | $2,250 | $4,500 | $2,250 |

| Kansas | 5.25% | > | $15,000 | 5.25% | > | $30,000 | |||||

| Kansas | 5.70% | > | $30,000 | 5.70% | > | $60,000 | |||||

| Kentucky (a, d) | 4.00% | > | $0 | 4.00% | > | $0 | $3,160 | $6,320 | n.a. | n.a. | n.a. |

| Kentucky | |||||||||||

| Louisiana (x) | 1.85% | > | $0 | 1.85% | > | $0 | n.a. | n.a. | $4,500 | $9,000 | $1,000 |

| Louisiana | 3.50% | > | $12,500 | 3.50% | > | $25,000 | |||||

| Louisiana | 4.25% | > | $50,000 | 4.25% | > | $100,000 | |||||

| Maine (u, y, bb) | 5.80% | > | $0 | 5.80% | > | $0 | $14,600 | $29,200 | $5,000 | $10,000 | $300 credit |

| Maine | 6.75% | > | $26,050 | 6.75% | > | $52,100 | |||||

| Maine | 7.15% | > | $61,600 | 7.15% | > | $123,250 | |||||

| Maryland (a, m, n, z, aa) | 2.00% | > | $0 | 2.00% | > | $0 | $2,550 | $5,150 | $3,200 | $6,400 | $3,200 |

| Maryland | 3.00% | > | $1,000 | 3.00% | > | $1,000 | |||||

| Maryland | 4.00% | > | $2,000 | 4.00% | > | $2,000 | |||||

| Maryland | 4.75% | > | $3,000 | 4.75% | > | $3,000 | |||||

| Maryland | 5.00% | > | $100,000 | 5.00% | > | $150,000 | |||||

| Maryland | 5.25% | > | $125,000 | 5.25% | > | $175,000 | |||||

| Maryland | 5.50% | > | $150,000 | 5.50% | > | $225,000 | |||||

| Maryland | 5.75% | > | $250,000 | 5.75% | > | $300,000 | |||||

| Massachusetts | 5.00% | > | $0 | 5.00% | > | $0 | n.a. | n.a. | $4,400 | $8,800 | $1,000 |

| Massachusetts | 9.00% | > | $1,000,000 | 9.00% | > | $1,000,000 | |||||

| Michigan (a, d, n) | 4.25% | > | $0 | 4.25% | > | $0 | n.a. | n.a. | $5,600 | $11,200 | $5,600 |

| Minnesota (d, bb, cc, pp) | 5.35% | > | $0 | 5.35% | > | $0 | $14,575 | $29,150 | n.a. | n.a. | $5,050 |

| Minnesota | 6.80% | > | $31,690 | 6.80% | > | $46,330 | |||||

| Minnesota | 7.85% | > | $104,090 | 7.85% | > | $184,040 | |||||

| Minnesota | 9.85% | > | $193,240 | 9.85% | > | $321,450 | |||||

| Mississippi | 4.70% | > | $10,000 | 4.70% | > | $10,000 | $2,300 | $4,600 | $6,000 | $12,000 | $1,500 |

| Missouri (a, b, j, m, u) | 2.00% | > | $1,273 | 2.00% | > | $1,207 | $14,600 | $29,200 | n.a | n.a | n.a |

| Missouri | 2.50% | > | $2,546 | 2.50% | > | $2,414 | |||||

| Missouri | 3.00% | > | $3,819 | 3.00% | > | $3,621 | |||||

| Missouri | 3.50% | > | $5,092 | 3.50% | > | $4,828 | |||||

| Missouri | 4.00% | > | $6,365 | 4.00% | > | $6,035 | |||||

| Missouri | 4.50% | > | $7,638 | 4.50% | > | $7,242 | |||||

| Missouri | 4.80% | > | $8,911 | 4.80% | > | $8,449 | |||||

| Montana (b, d, u, bb) | 4.70% | > | $0 | 4.70% | > | $0 | $14,600 | $29,200 | n.a | n.a | n.a |

| Montana | 5.90% | > | $20,500 | 5.90% | > | $41,000 | |||||

| Nebraska (d, h, m, bb) | 2.46% | > | $0 | 2.46% | > | $0 | $7,900 | $15,800 | $157 credit | $314 credit | $157 credit |

| Nebraska | 3.51% | > | $3,700 | 3.51% | > | $7,390 | |||||

| Nebraska | 5.01% | > | $22,170 | 5.01% | > | $44,350 | |||||

| Nebraska | 5.84% | > | $35,730 | 5.84% | > | $71,460 | |||||

| Nevada | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| New Hampshire (dd) | 3% on interest and dividends only | 3% on interest and dividends only | n.a | n.a | $2,400 | $4,800 | n.a. | ||||

| New Jersey (a) | 1.400% | > | $0 | 1.400% | > | $0 | n.a. | n.a. | $1,000 | $2,000 | $1,500 |

| New Jersey | 1.750% | > | $20,000 | 1.750% | > | $20,000 | |||||

| New Jersey | 3.500% | > | $35,000 | 2.450% | > | $50,000 | |||||

| New Jersey | 5.525% | > | $40,000 | 3.500% | > | $70,000 | |||||

| New Jersey | 6.370% | > | $75,000 | 5.525% | > | $80,000 | |||||

| New Jersey | 8.970% | > | $500,000 | 6.370% | > | $150,000 | |||||

| New Jersey | 10.750% | > | $1,000,000 | 8.970% | > | $500,000 | |||||

| New Jersey | 10.750% | > | $1,000,000 | ||||||||

| New Mexico (m, u, kk) | 1.70% | > | $0 | 1.70% | > | $0 | $14,600 | $29,200 | n.a. | n.a. | $4,000 |

| New Mexico | 3.20% | > | $5,500 | 3.20% | > | $8,000 | |||||

| New Mexico | 4.70% | > | $11,000 | 4.70% | > | $16,000 | |||||

| New Mexico | 4.90% | > | $16,000 | 4.90% | > | $24,000 | |||||

| New Mexico | 5.90% | > | $210,000 | 5.90% | > | $315,000 | |||||

| New York (a, i) | 4.00% | > | $0 | 4.00% | > | $0 | $8,000 | $16,050 | n.a. | n.a. | $1,000 |

| New York | 4.50% | > | $8,500 | 4.50% | > | $17,150 | |||||

| New York | 5.25% | > | $11,700 | 5.25% | > | $23,600 | |||||

| New York | 5.50% | > | $13,900 | 5.50% | > | $27,900 | |||||

| New York | 6.00% | > | $80,650 | 6.00% | > | $161,550 | |||||

| New York | 6.85% | > | $215,400 | 6.85% | > | $323,200 | |||||

| New York | 9.65% | > | $1,077,550 | 9.65% | > | $2,155,350 | |||||

| New York | 10.30% | > | $5,000,000 | 10.30% | > | $5,000,000 | |||||

| New York | 10.90% | > | $25,000,000 | 10.90% | > | $25,000,000 | |||||

| North Carolina | 4.50% | > | $0 | 4.50% | > | $0 | $12,750 | $25,500 | n.a. | n.a. | n.a. |

| North Dakota (j, o, u) | 1.95% | > | $44,725 | 1.95% | > | $74,750 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| North Dakota | 2.50% | > | $225,975 | 2.50% | > | $275,100 | |||||

| Ohio (a, j, n, ee) | 2.750% | > | $26,050 | 2.750% | > | $26,050 | n.a. | n.a. | $2,400 | $4,800 | $2,500 |

| Ohio | 3.500% | > | $92,150 | 3.500% | > | $92,150 | |||||

| Oklahoma (m) | 0.25% | > | $0 | 0.25% | > | $0 | $6,350 | $12,700 | $1,000 | $2,000 | $1,000 |

| Oklahoma | 0.75% | > | $1,000 | 0.75% | > | $2,000 | |||||

| Oklahoma | 1.75% | > | $2,500 | 1.75% | > | $5,000 | |||||

| Oklahoma | 2.75% | > | $3,750 | 2.75% | > | $7,500 | |||||

| Oklahoma | 3.75% | > | $4,900 | 3.75% | > | $9,800 | |||||

| Oklahoma | 4.75% | > | $7,200 | 4.75% | > | $12,200 | |||||

| Oregon (a, b, d, h, m, bb, ff, oo) | 4.75% | > | $0 | 4.75% | > | $0 | $2,745 | $5,495 | $249 credit | $498 credit | $249 credit |

| Oregon | 6.75% | > | $4,300 | 6.75% | > | $8,600 | |||||

| Oregon | 8.75% | > | $10,750 | 8.75% | > | $21,500 | |||||

| Oregon | 9.90% | > | $125,000 | 9.90% | > | $250,000 | |||||

| Pennsylvania (a) | 3.07% | > | $0 | 3.07% | > | $0 | n.a. | n.a. | n.a. | n.a. | n.a. |

| Rhode Island (d, bb, gg) | 3.75% | > | $0 | 3.75% | > | $0 | $10,550 | $21,150 | $4,950 | $9,900 | $4,950 |

| Rhode Island | 4.75% | > | $77,450 | 4.75% | > | $77,450 | |||||

| Rhode Island | 5.99% | > | $176,050 | 5.99% | > | $176,050 | |||||

| South Carolina (d, o, u, bb) | 0.00% | > | $0 | 0.00% | > | $0 | $14,600 | $29,200 | n.a. | n.a. | $4,610 (o) |

| South Carolina | 3.00% | > | $3,460 | 3.00% | > | $3,460 | |||||

| South Carolina | 6.40% | > | $17,330 | 6.40% | > | $17,330 | |||||

| South Dakota | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Tennessee | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Texas | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Utah (d, h, hh) | 4.65% | > | $0 | 4.65% | > | $0 | $876 credit | $1,752 credit | n.a. | n.a. | $1,941 |

| Vermont (j, n, ii, nn) | 3.35% | > | $0 | 3.35% | > | $0 | $7,000 | $14,050 | $4,850 | $9,700 | $4,850 |

| Vermont | 6.60% | > | $45,400 | 6.60% | > | $75,850 | |||||

| Vermont | 7.60% | > | $110,050 | 7.60% | > | $183,400 | |||||

| Vermont | 8.75% | > | $229,550 | 8.75% | > | $279,450 | |||||

| Virginia (m, mm) | 2.00% | > | $0 | 2.00% | > | $0 | $8,000 | $16,000 | $930 | $1,860 | $930 |

| Virginia | 3.00% | > | $3,000 | 3.00% | > | $3,000 | |||||

| Virginia | 5.00% | > | $5,000 | 5.00% | > | $5,000 | |||||

| Virginia | 5.75% | > | $17,000 | 5.75% | > | $17,000 | |||||

| Washington | 7.0% on capital gains income only | 7.0% on capital gains income only | $250,000 | $250,000 | n.a. | n.a. | n.a. | ||||

| West Virginia (a, m) | 2.36% | > | $0 | 2.36% | > | $0 | n.a. | n.a. | $2,000 | $4,000 | $2,000 |

| West Virginia | 3.15% | > | $10,000 | 3.15% | > | $10,000 | |||||

| West Virginia | 3.54% | > | $25,000 | 3.54% | > | $25,000 | |||||

| West Virginia | 4.72% | > | $40,000 | 4.72% | > | $40,000 | |||||

| West Virginia | 5.12% | > | $60,000 | 5.12% | > | $60,000 | |||||

| Wisconsin (d, m, bb, jj) | 3.50% | > | $0 | 3.50% | > | $0 | $13,230 | $24,490 | $700 | $1,400 | $700 |

| Wisconsin | 4.40% | > | $14,320 | 4.40% | > | $19,090 | |||||

| Wisconsin | 5.30% | > | $28,640 | 5.30% | > | $38,190 | |||||

| Wisconsin | 7.65% | > | $315,310 | 7.65% | > | $420,420 | |||||

| Wyoming | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | ||||

| Washington, DC (u) | 4.00% | > | $0 | 4.00% | > | $0 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Washington, DC | 6.00% | > | $10,000 | 6.00% | > | $10,000 | |||||

| Washington, DC | 6.50% | > | $40,000 | 6.50% | > | $40,000 | |||||

| Washington, DC | 8.50% | > | $60,000 | 8.50% | > | $60,000 | |||||

| Washington, DC | 9.25% | > | $250,000 | 9.25% | > | $250,000 | |||||

| Washington, DC | 9.75% | > | $500,000 | 9.75% | > | $500,000 | |||||

| Washington, DC | 10.75% | > | $1,000,000 | 10.75% | > | $1,000,000 |

(b) These states allow some or all of federal income tax paid to be deducted from state taxable income.

(c) For single taxpayers with AGI below $25,999, the standard deduction is $3,000. This standard deduction amount is reduced by $25 for every additional $500 of AGI, not to fall below $2,500. For Married Filing Joint (MFJ) taxpayers with AGI below $25,999, the standard deduction is $8,500. This standard deduction amount is reduced by $175 for every additional $500 of AGI, not to fall below $5,000. For all taxpayers with AGI of $50,000 or less and claiming a dependent, the dependent exemption is $1,000. This amount is reduced to $500 per dependent for taxpayers with AGI above $50,000 and equal to or less than $100,000. For taxpayers with more than $100,000 in AGI, the dependent exemption is $300 per dependent.

(d) Standard deduction and/or personal exemption is adjusted annually for inflation. Inflation-adjusted amounts for tax year 2024 are shown.

(e) Arizona's standard deduction can be adjusted upward by an amount equal to 31 percent of the amount the taxpayer would have claimed in charitable deductions if the taxpayer had claimed itemized deductions.

(f) In lieu of a dependent exemption, Arizona offers a dependent tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. of $100 per dependent under the age of 17 and $25 per dependent age 17 and older. The credit begins to phase out for taxpayers with federal adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods (FAGI) above $200,000 (single filers) or $400,000 (MFJ).

(g) Rates apply to individuals earning more than $87,000. A separate tax tables exist for individuals earning $87,000 or less, with rates of 2 percent on income greater than or equal to $5,300; 3 percent on income greater than or equal to $10,600; 3.4 percent on income greater than or equal to $15,100; and 4.4 percent on income greater than $25,000 but less than or equal to $87,000.

(h) Standard deduction or personal exemption is structured as a tax credit.

(i) Connecticut and New York have "tax benefit recapture," by which many high-income taxpayers pay their top tax rate on all income, not just on amounts above the benefit threshold.

(j) Bracket levels adjusted for inflation each year. Inflation-adjusted bracket widths for 2024 were not available as of publication, so table reflects 2023 inflation-adjusted bracket widths.

(k) Exemption credits phase out for single taxpayers by $6 for each $2,500 of federal AGI above $237,035 and for MFJ filers by $12 for each $2,500 of federal AGI above $474,075. The credit cannot be reduced to below zero.

(l) Rates include the additional mental health services tax at the rate of 1 percent on taxable income in excess of $1 million. Rates exclude a payroll tax of 1.1 percent to fund the state’s disability insurance program. As of 2024, there is no wage ceiling for this payroll tax, which means that the state’s top individual income tax rate on wage income becomes 14.4 percent.

(m) State provides a state-defined personal exemption amount for each exemption available and/or deductible under the Internal Revenue Code. Under the Tax Cuts and Jobs Act, the personal exemption is set at $0 until 2026 but not eliminated. Because it is still available, these state-defined personal exemptions remain available in some states but are set to $0 in other states.

(n) Standard deduction and/or personal exemption adjusted annually for inflation, but the 2024 inflation adjustment was not available at time of publication, so table reflects actual 2023 amount(s).

(o) Colorado, Montana, New Mexico, North Dakota, and South Carolina include the federal standard deduction in their income starting point.

(p) Connecticut has a complex set of phaseout provisions. For each single taxpayer whose Connecticut AGI exceeds $56,500, the amount of the taxpayer's Connecticut taxable income to which the 2 percent tax rate applies shall be reduced by $1,000 for each $5,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds said amount. Any such amount will have a tax rate of 4.5 percent instead of 2 percent. Each single taxpayer whose Connecticut AGI exceeds $105,000 shall pay an amount equal to $25 for each $5,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds $105,000, up to a maximum payment of $250. Additionally, each single taxpayer whose Connecticut AGI exceeds $200,000 shall pay an amount equal to $90 for each $5,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds $200,000 but is less than $500,000, and by an additional $50 for each $5,000, or fraction thereof, by which the taxpayer’s AGI exceeds $500,000, up to a maximum payment of $3,150. For each MFJ taxpayer whose Connecticut AGI exceeds $100,500, the amount of the taxpayer's Connecticut taxable income to which the 2 percent tax rate applies shall be reduced by $2,000 for each $5,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds said amount. Any such amount of Connecticut taxable income to which, as provided in the preceding sentence, the 2 percent tax rate does not apply shall be an amount to which the 4.5 percent tax rate shall apply. Each MFJ whose Connecticut AGI exceeds $210,000 shall pay an amount equal to $50 for each $10,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds $210,000, up to a maximum payment of $500. Additionally, each MFJ taxpayer whose Connecticut AGI exceeds $400,000 shall pay, in addition to the amount above, an amount equal to $180 for each $10,000, or fraction thereof, by which the taxpayer's Connecticut AGI exceeds $400,000, up to a maximum of $5,400, and a further $100 for each $10,000, or fraction thereof, by which Connecticut AGI exceeds $1 million, up to a combined maximum payment of $6,300.

(q) Connecticut taxpayers are also given personal tax credits (1-75%) based upon adjusted gross income.

(r) Connecticut's personal exemption phases out by $1,000 for each $1,000, or fraction thereof, by which a single filer's Connecticut AGI exceeds $30,000 and a MFJ filer's Connecticut AGI exceeds $48,000.

(s) In addition to the personal income tax rates, Delaware imposes a tax on lump-sum distributions.

(t) Additionally, Hawaii allows any taxpayer, other than a corporation, acting as a business entity in more than one state and required by law to file a return, to report and pay a tax of 0.5 percent of its annual gross sales (1) where the taxpayer's only activities in Hawaii consist of sales, (2) when the taxpayer does not own or rent real estate or tangible personal property, and (3) when the taxpayer’s annual gross sales in or into Hawaii do not exceed $100,000. Haw. Rev. Stat. § 235-51 (2015).

(u) Deduction and/or exemption tied to federal tax system. Federal deductions and exemptions are indexed for inflation, and where applicable, the tax year 2024 inflation-adjusted amounts are shown.

(v) As of June 1, 2017, taxpayers cannot claim the personal exemption if their adjusted gross income exceeds $250,000 (single filers) or $500,000 (MFJ).

(w) $1,000 is a base exemption. If dependents meet certain conditions, filers can take an additional $1,500 exemption for each. If a taxpayer is claiming a child as a dependent for the first taxable year in which the exemption is allowed, the taxpayer is now permitted to claim an amount of $3,000, instead of $1,500.

(x) Standard deduction and personal exemptions are combined: $4,500 for single and married filing separately; $9,000 MFJ and head of household.

(y) Maine's personal exemption begins to phase out for taxpayers with income exceeding $305,150 (single filers) or $366,100 (MFJ). The standard deduction amounts for 2024 are phased out for taxpayers with Maine income over $97,150 (single filers) or $194,300 (MFJ). The dependent personal exemption is structured as a tax credit and begins to phase out for taxpayers with income exceeding $200,000 (head of household) or $400,000 (married filing jointly).

(z) The standard deduction is 15 percent of income with a minimum of $1,700 and a cap of $2,550 for single filers and married filing separately filers. The standard deduction is a minimum of $3,450 and capped at $5,150 for MFJ filers, head of household filers, and qualifying surviving spouses. The minimum and maximum standard deduction amounts are adjusted annually for inflation. 2024 inflation-adjusted amounts were not announced as of publication, so 2023 inflation-adjusted amounts are shown.

(aa) The exemption amount has the following phaseout schedule: If AGI is above $100,000 for single filers and above $150,000 for married filers, the $3,200 exemption begins to be phased out. If AGI is above $150,000 for single filers and above $200,000 for married filers, the exemption is phased out entirely.

(bb) Bracket levels adjusted for inflation each year. Inflation-adjusted bracket levels for 2024 are shown.

(cc) For taxpayers whose AGI exceeds $116,250 (married filing separately) or $232,500 (all other filers), Minnesota’s standard deduction is reduced by the lesser of 3 percent of the excess of the taxpayer’s federal AGI over the applicable amount or 80 percent of the standard deduction otherwise allowable.

(dd) Applies to interest and dividend income only.

(ee) Ohio's personal exemption is $2,400 for an AGI of $40,000 or less, $2,150 if AGI is more than $40,000 but less than or equal to $80,000, and $1,900 if AGI is greater than $80,000. Ohio's dependent exemption for children under the age of 18 is $2,500.

(ff) The personal exemption credit is not allowed if federal AGI exceeds $100,000 for single filers or $200,000 for MFJ.

(gg) The phaseout range for the standard deduction, personal exemption, and dependency exemption is $246,450 to $274,650. For taxpayers with modified Federal AGI exceeding $274,650, no standard deduction, personal exemption, or dependency exemption is available.

(hh) The standard deduction is taken in the form of a nonrefundable credit of 6 percent of the federal standard or itemized deductionItemized deductions allow individuals to subtract designated expenses from their taxable income and can be claimed in lieu of the standard deduction. Itemized deductions include those for state and local taxes, charitable contributions, and mortgage interest. An estimated 13.7 percent of filers itemized in 2019, most being high-income taxpayers. amount, excluding the deduction for state or local income tax. This credit phases out at 1.3 cents per dollar of AGI above $16,742 ($33,484 for MFJ).

(ii) For taxpayers with federal AGI that exceeds $150,000, the taxpayer will pay the greater of state income tax or 3 percent of federal AGI.

(jj) The standard deduction begins to phase out at $19,069 in income for single filers and $27,519 in income for joint filers. The standard deduction phases out to zero at $129,319 for single filers and $151,344 for joint filers.

(kk) In lieu of the suspended personal exemption, New Mexico offers a deduction of $4,000 for all but one of a taxpayer’s dependents.

(ll) Taxpayers with net income greater than or equal to $87,000 but not greater than $90,800 shall reduce the amount of tax due by deducting a bracket adjustment amount. The bracket adjustment amount starts at $380 for individuals with net income of $87,001 and decreases by $10 for every $100 in additional net income.

(mm) The standard deduction for 2024 will be $8,500 for single taxpayers and $17,000 for MFJ taxpayers if certain revenue growth projections are met.

(nn) Taxpayers also receive an additional deduction of $1,050 for each standard deduction box checked on federal Form 1040.

(oo) California and Oregon do not fully index their top brackets.

(pp) Minnesota imposes a surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. on individuals, estates, and trusts equal to 1% of net investment income over $1 million.

Notable 2024 State Individual Income Tax Changes

Last year continued the historic pace of income tax rate reductions. In total, 26 states enacted individual income tax rate reductions from 2021 to 2023. Only Massachusetts and the District of Columbia increased their top marginal tax rates in those years. Several changes implemented later in 2023 were retroactive to January 1, 2023. However, a number of notable changes come into effect on January 1, 2024, or are set to occur on specific future dates, with rates phasing down incrementally over time. Some of the scheduled future rate reductions rely on tax triggers, where specific changes to tax rates will occur once certain revenue benchmarks are met. Notable changes to major individual income tax provisions already certified for 2024 include the following:

Arkansas

Under S.B. 8, enacted in September 2023, the top individual income tax rate in Arkansas was reduced from 4.7 percent to 4.4 percent for tax years beginning on or after January 1, 2024. This top rate applies to incomes between $24,300 and $87,000 for taxpayers earning $87,000 or less and to incomes over $8,801 for taxpayers earning more than $87,000.

Connecticut

As part of the state budget bill, H.B. 6941, Connecticut legislators reduced individual income tax rates for the two lowest brackets, from 3 percent to 2 percent and from 5 percent to 4.5 percent, respectively. The change comes into effect on January 1, 2024. The reduction will not affect taxpayers with an annual income of $150,000 or above ($300,000 or above for married couples filing a joint return).

Georgia

On January 1, 2024, Georgia transitions from a graduated individual income tax with a top rate of 5.75 percent to a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. with a rate of 5.49 percent. Additionally, the state significantly increased its personal exemption (to $12,000 for single taxpayers and $18,500 for married couples filing a joint return). These changes were enacted by H.B. 1437 in April 2022.

Indiana

Under H.B. 1001, enacted in May 2023, Indiana accelerated its previously enacted tax rate reductions, lowering the individual income tax rate from 3.15 in 2023 to 3.05 percent in 2024. The law also repealed previously enacted tax triggers, instead prescribing a rate reduction to 3.0 percent in 2025, 2.95 percent in 2026, and 2.9 percent in 2027 and beyond.

Iowa

As part of its comprehensive tax reform, effective January 1, 2024, Iowa consolidated its four individual income tax brackets into three (H.F. 2317). As a result, its top rate decreased from 6 percent to 5.7 percent. The state is currently transitioning to a flat income tax system with a rate of 3.9 percent by 2026.

Kentucky

H.B. 1, signed into law in February 2023, reduced Kentucky’s flat individual income tax rate from 4.5 percent in 2023 to 4.0 percent starting in 2024, codifying a reduction that was triggered under the conditions established by H.B. 8, enacted in 2022.

Mississippi

Under H.B. 531, enacted in April 2022, Mississippi will continue reducing its flat individual income tax rate from 2024 to 2026. Effective January 1, 2024, the tax rate decreased from 5 percent to 4.7 percent (applied on taxable income exceeding $10,000).

Missouri

Effective January 1, 2024, Missouri’s Department of Revenue reduced its top individual income tax rate from 4.95 percent to 4.8 percent as the respective revenue triggers were met in the previous fiscal year, per S.B. 3 enacted in October 2022.

Montana

S.B. 121, enacted in March 2023, simplified the individual income tax system in Montana and, effective January 1, 2024, reduced the number of tax brackets from seven to two with the top tax rate of 5.9 percent. Additionally, starting in 2024, taxpayers will use their federal taxable income as a base for calculating Montana taxable income, implying that the federal standard deduction or the sum of itemized deductions will be automatically accounted for.

Nebraska

L.B. 754, enacted in May 2023, reduced the top individual income tax rate from 6.64 percent in 2023 to 5.84 percent in 2024 and outlined the gradual reduction of the state’s top rate to 3.99 percent by 2027.

New Hampshire

New Hampshire continues to phase out its interest and dividends tax. In 2024, per H.B. 2, the tax rate will go down from 4 percent to 3 percent. Starting in 2025, the tax will be repealed, two years earlier than initially planned.

North Carolina

Under H.B. 259, enacted in September 2023, North Carolina accelerated the reduction of its flat individual income tax rate. Effective January 1, 2024, the tax rate decreased from 4.75 percent to 4.5 percent. The rate is scheduled to decline to 3.99 percent by 2026.

Ohio

H.B. 33, enacted in July 2023, reduced the number of individual income tax brackets in Ohio from three to two and lowered the top rate from 3.75 percent to 3.5 percent, continuing the individual income tax rate reduction and simplification trend that state legislators started in 2021.

South Carolina

Effective January 1, 2024, South Carolina reduced its top individual income tax rate from 6.5 percent to 6.4 percent, per S.B. 1087. Further reductions to 6 percent are scheduled but are subject to general fund revenue triggers. Governor McMaster’s executive budget assumes that the revenue trigger for the previous fiscal year was met, and the top rate must go down further to 6.3 percent, as per the statutory schedule. The change has not yet been confirmed by the state’s Department of Revenue.