Key Findings

- Individual income taxes are a major source of state government revenue, accounting for 37 percent of state taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. collections.

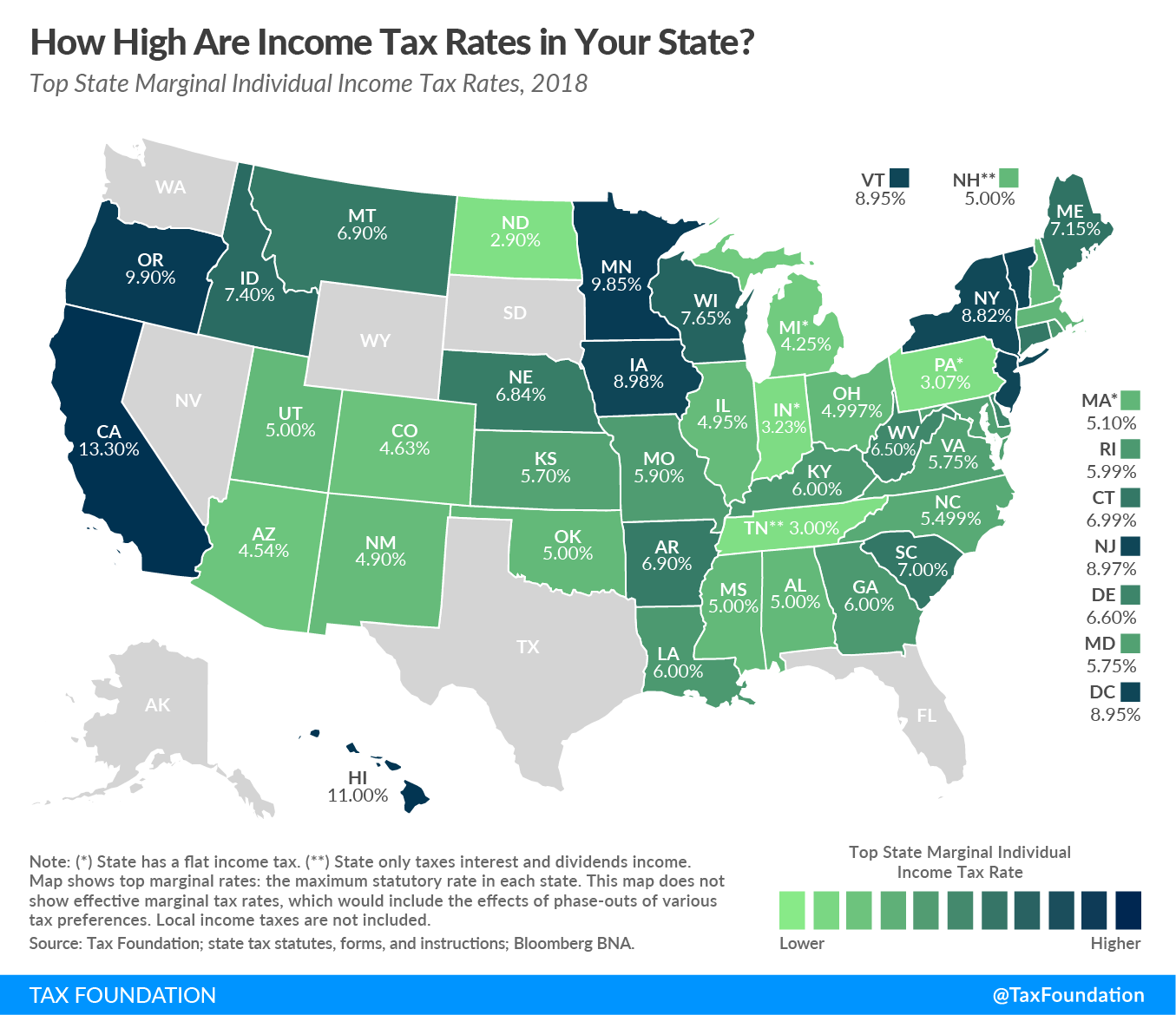

- Forty-three states levy individual income taxes. Forty-one tax wage and salary income, while two states—New Hampshire and Tennessee—exclusively tax dividend and interest income. Seven states levy no income tax at all.

- Of those states taxing wages, eight have single-rate tax structures, with one rate applying to all taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. . Conversely, 33 states levy graduated-rate income taxes, with the number of brackets varying widely by state. Hawaii now has 12 brackets, the most in the country.

- States’ approaches to income taxes vary in other details as well. Some states double their single-bracket widths for married filers to avoid the “marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples..” Some states index tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat., exemptions, and deductions for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin; many others do not. Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all.

Individual income taxes are a major source of state government revenue, accounting for 37 percent of state tax collections.[1] Their prominence in public policy considerations is further enhanced by the fact that individuals are actively responsible for filing their income taxes, in contrast to the indirect payment of sales and excise taxes.

Forty-three states levy individual income taxes. Forty-one tax wage and salary income, while two states—New Hampshire and Tennessee—exclusively tax dividend and interest. Seven states levy no income tax at all. Tennessee is currently phasing out its Hall Tax (income tax applied only to dividends and interest income) and is scheduled to repeal its income tax entirely by 2022.[2]

Of those states taxing wages, eight have single-rate tax structures, with one rate applying to all taxable income. Conversely, 33 states levy graduated-rate income taxes, with the number of brackets varying widely by state. Kansas, for example, imposes a two-bracket income tax system. At the other end of the spectrum, two states—California and Missouri—each have 10 tax brackets. Hawaii has 12 brackets. Top marginal rates range from North Dakota’s 2.9 percent to California’s 13.3 percent.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeIn some states, a large number of brackets are clustered within a narrow income band; Georgia’s taxpayers reach the state’s sixth and highest bracket at $7,000 in annual income. In other states, the top marginal rate kicks in at $500,000 (New Jersey) or even $1 million (California, when the state’s “millionaire’s tax” surcharge is included).

States’ approaches to income taxes vary in other details as well. Some states double their single-bracket widths for married filers to avoid the “marriage penalty.” Some states index tax brackets, exemptions, and deductions for inflation; many others do not. Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all. In the following table, we provide the most up-to-date data available on state individual income tax rates, brackets, standard deductions, and personal exemptions for both single and joint filers.

Following the 2017 federal tax reform, it remains to be seen if states that are coupled to the federal standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. and personal exemption will maintain that conformity or rather retain their previous deductions and exemptions amounts. The federal bill increased the standard deduction to $12,000 for single filers, but eliminated the personal exemption.[3]

Notable Individual Income TaxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source Changes in 2018

Several states changed key features of their individual income tax codes between 2017 and 2018, such as:

- Hawaii has reinstated its formerly temporary individual income tax brackets, ranging from 8.25 to 11 percent. [4]

- Mississippi began phasing out its 3 percent individual income tax bracket by exempting the first $1,000 in income. The bracket will be fully phased out by 2022.[5]

- Maine repealed the 3 percent income tax surcharge on earnings over $200,000 approved by voters in November 2016.[6]

[1] U.S. Census Bureau, “State & Local Government Finance, Fiscal Year 2015.” http://www.census.gov/govs/local/.

[2] Tennessee Department of Revenue, “Hall Income Tax Notice,” July 2016. https://www.tn.gov/content/dam/tn/revenue/documents/notices/income/16-05Hall.pdf.

[3] Jared Walczak, “Tax Reform Moves to the States: State Revenue Implications and Reform Opportunities Following Federal Tax Reform,” Tax Foundation, January 31, 2018. https://taxfoundation.org/state-conformity-federal-tax-reform/.

[4] Kari Jahnsen, ”Hawaii Hikes Income Taxes to Pay for Earned Income Credit,” Tax Foundation, July 24, 2017. https://taxfoundation.org/hawaii-income-taxes-earned-income-credit/.

[5] Joseph Bishop-Henchman, “Mississippi Approves Franchise Tax Phasedown, Income Tax Cut,” Tax Foundation, May 16, 2016. https://taxfoundation.org/mississippi-approves-franchise-tax-phasedown-income-tax-cut/.

[6] EY Tax News Update, “Maine 3% income tax surcharge repealed — revised withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount the employee requests. tables are effective immediately,” August 2, 2017. https://taxnews.ey.com/news/2017-1262-maine-3-percent-income-tax-surcharge-repealed-revised-withholding-tables-are-effective-immediately.

Share this article