Key Findings

- Individual income taxes are a major source of state government revenue, accounting for 37 percent of state taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. collections in fiscal year (FY) 2017.

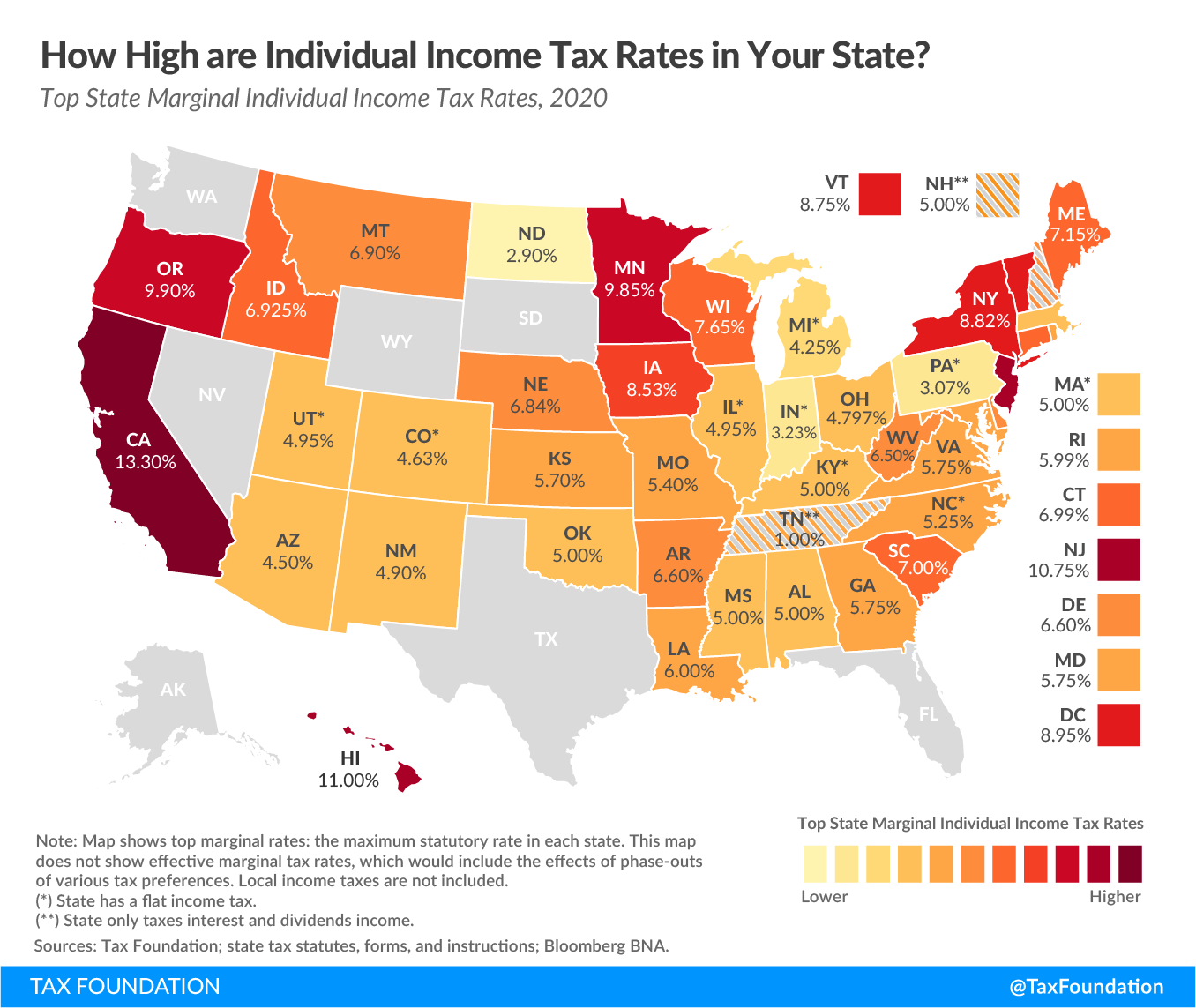

- Forty-three states levy individual income taxes. Forty-one tax wage and salary income, while two states—New Hampshire and Tennessee—exclusively tax dividend and interest income. Seven states levy no individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source at all.

- Of those states taxing wages, nine have single-rate tax structures, with one rate applying to all taxable income. Conversely, 32 states and the District of Columbia levy graduated-rate income taxes, with the number of brackets varying widely by state. Hawaii has 12 brackets, the most in the country.

- States’ approaches to income taxes vary in other details as well. Some states double their single-bracket widths for married filers to avoid a “marriage penalty.” Some states index tax brackets, exemptions, and deductions for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin; many others do not. Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all.

Individual income taxes are a major source of state government revenue, accounting for 37 percent of state tax collections.[1] Their prominence in public policy considerations is further enhanced in that individuals are actively responsible for filing their income taxes, in contrast to the indirect payment of sales and excise taxes.

Forty-three states levy individual income taxes. Forty-one tax wage and salary income, while two states—New Hampshire and Tennessee—exclusively tax dividend and interest income. Seven states levy no income tax at all. Tennessee is currently phasing out its Hall Tax (an income tax applied only to dividends and interest income), with complete repeal scheduled for tax years beginning January 1, 2021.[2]

Of those states taxing wages, nine have single-rate tax structures, with one rate applying to all taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. . Conversely, 32 states levy graduated-rate income taxes, with the number of brackets varying widely by state. Kansas, for example, imposes a three-bracket income tax system. At the other end of the spectrum, Hawaii has 12 brackets. Top marginal rates range from North Dakota’s 2.9 percent to California’s 13.3 percent.

In some states, a large number of brackets are clustered within a narrow income band; Georgia’s taxpayers reach the state’s sixth and highest bracket at $7,000 in annual income. In the District of Columbia, the top rate kicks in at $1 million, as it does in California (when the state’s “millionaire’s tax” surcharge is included). New York and New Jersey’s top rates kick in at even higher levels of marginal income: $1,077,550 and $5 million, respectively.

States’ approaches to income taxes vary in other details as well. Some states double their single filer bracket widths for married filers to avoid imposing a “marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples..” Some states index tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat., exemptions, and deductions for inflation; many others do not.[3] Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all. In the following table, we provide the most up-to-date data available on state individual income tax rates, brackets, standard deductions, and personal exemptions for both single and joint filers.

The federal Tax Cuts and Jobs Act of 2017 (TCJA) increased the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. (set at $12,400 for single filers and $24,800 for joint filers in 2020), while suspending the personal exemption by reducing it to $0 through 2025. Because many states use the federal tax code as the starting point for their own standard deduction and personal exemption calculations, some states that coupled to the federal tax code updated their conformity statutes in recent years to either adopt federal changes or retain their previous deduction and exemption amounts.

Notable Individual Income Tax Changes in 2020

Several states changed key features of their individual income tax codes going into tax year 2020. In addition, some states adopted legislation in 2019 that changed various individual income tax provisions and made those changes retroactive to the beginning of tax year 2019. Notable changes include the following:

- In June 2019, Arizona became the most recent state to conform to a post-TCJA version of the Internal Revenue Code (IRC). Specifically, with enactment of House Bill 2757, Arizona’s standard deduction more than doubled to match the new, more generous, federal standard deduction. That legislation also reduced Arizona’s marginal individual income tax rates while consolidating five brackets into four, and it replaced the dependent exemption with a slightly more generous child tax credit.[4]

- Arkansas built upon individual income tax rate reductions in 2015 and 2017 with a third phase of reforms in 2019. Arkansas is unique among states in that it has three entirely different individual income tax rate schedules depending on total taxable income. As taxpayers’ incomes rise, they not only face higher marginal rates but also shift into an entirely different rate schedule. For tax year 2020, Arkansas’s individual income tax rate schedule for high earners has been consolidated from six brackets into four and the top marginal rate dropped from 6.9 to 6.6 percent. For those subject to the middle rate schedule, the top rate has dropped from 6.0 to 5.9 percent.[5]

- Massachusetts’ single-rate individual income tax dropped from 5.05 to 5.0 percent for tax year 2020, due to the state meeting revenue targets outlined in a tax trigger law that was enacted in 2002.[6] The 2002 law established a system by which, in any year in which revenue growth exceeded a specified baseline, the individual income tax rate would be reduced by 0.05 percentage points until the rate reached 5.0 percent. As such, the reduction to 5.0 percent for tax year 2020 is the last triggered reduction.[7]

- In Michigan, Senate Bill 748, signed into law in February 2018, made changes to Michigan’s personal exemption to prevent it from being zeroed out due to the state’s rolling conformity with federal individual income tax provisions. For tax year 2020, Michigan’s personal exemption has increased from $4,400 to $4,750 as part of a four-year phase-in that began in tax year 2018. By tax year 2021, the personal exemption will reach $4,900, and starting in tax year 2020, it will be indexed annually for inflation.[8]

- Like Arizona, Minnesota was one of the last states to adopt legislation to bring its tax code into conformity with a post-TCJA version of the federal tax code, doing so in May 2019. With this law, Minnesota adopted a standard deduction that matches the federal amount. The state permitted the zeroing out of its personal exemption but created a new dependent exemption, and these changes were made effective starting in tax year 2019.[9]

- In November 2019, North Carolina Senate Bill 557 was signed into law, increasing the standard deduction by 7.5 percent for all filing statuses beginning in tax year 2020.[10]

- House Bill 166, Ohio’s FY 2020-2021 biennial budget, was signed into law in July 2019 and included several individual income tax changes that were retroactive to the beginning of tax year 2019. The state’s seven individual income tax brackets were consolidated into five (with the first two brackets eliminated), and each of the remaining marginal rates was reduced by 4 percent. Indexing of the brackets was frozen at 2018 levels for tax years 2019 and 2020 but is set to resume in 2021.[11]

- Tennessee’s “Hall Tax,” which applies to investment income but not to wage income, is continuing to phase out, with the rate dropping from 2 to 1 percent for 2020. Starting in 2021, Tennessee will be among the states with no individual income tax.[12]

- Virginia House Bill 2529, enacted in February 2019, increased Virginia’s standard deduction, retroactive to the start of that tax year and applicable through 2025.[13]

- In July 2019, Wisconsin Assembly Bill 56 (Act 9) was enacted, reducing Wisconsin’s second marginal individual income tax rate from 5.84 to 5.21 percent, retroactive to the beginning of tax year 2019. Assembly Bill 251 (Act 10), also enacted in July 2019, separately prescribed a reduction in Wisconsin’s first two marginal individual income tax rates to offset the influx in online sales tax revenue attributable to the state’s response to the U.S. Supreme Court’s South Dakota v. Wayfair Specifically, Act 10 required the Wisconsin Department of Revenue to reduce the first two marginal rates for tax year 2019 based on the actual influx in online sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. collections between October 1, 2018, and September 30, 2019, that were attributable to the Wayfair decision. Act 10 further specifies that for tax year 2020, the amount of actual Wayfair-related sales tax revenue collected between October 1, 2019, and September 30, 2020, will be used to determine the first two marginal rates for 2020, and that the 2020 rates will apply for tax years 2021 and beyond. As a result, the interaction between Act 9 and Act 10 is expected to result in Wisconsin’s first two marginal rates for tax year 2020 being reduced below the rates shown in the following table. Final 2020 rates will be published once actual sales tax collections data becomes available (after September 30, 2020).[14]

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeUpdate: This table was updated on February 12, 2020 and July 16, 2020 to reflect the most recent data available for Maine, Maryland, Nebraska, and Oregon.

Related Resources

Notes

[1] U.S. Census Bureau, “State & Local Government Finance,” Fiscal Year 2017, https://www.census.gov/data/datasets/2017/econ/local/public-use-datasets.html.

[2] Tennessee Department of Revenue, “Hall Income Tax Notice,” May 2017, https://www.tn.gov/revenue/taxes/hall-income-tax/due-date-and-tax-rates.html.

[3] See Jared Walczak, “Inflation Adjusting State Tax Codes: A Primer,” Tax Foundation, Oct. 29, 2019, https://taxfoundation.org/inflation-adjusting-state-tax-codes/.

[4] Jared Walczak, “Arizona Delivers Rate Cuts and Tax Conformity,” Tax Foundation, June 6, 2019, https://taxfoundation.org/arizona-income-tax-cuts-tax-conformity/.

[5] Katherine Loughead, “State Tax Changes as of January 1, 2020,” Tax Foundation, Dec. 20, 2019, https://taxfoundation.org/2020-state-tax-changes-january-1/.

[6] Mary Markos, “Massachusetts Income Tax Drops to 5% Flat Rate – 20 Years After Passage,” Boston Herald, Dec. 16, 2019, https://www.bostonherald.com/2019/12/13/massachusetts-income-tax-drops-to-5-flat-rate-20-years-after-passage/.

[7] Patrick Marvin, “Baker-Polito Administration Announces Massachusetts Income Tax Rate Dropping to 5% on January 1, 2020,” Mass.gov, Dec. 13, 2019, https://www.mass.gov/news/baker-polito-administration-announces-massachusetts-income-tax-rate-dropping-to-5-on-january-1.

[8] “Michigan Increases Personal Exemption, Removes IRC References,” RSM, Mar. 2, 2018, https://rsmus.com/what-we-do/services/tax/state-and-local-tax/income-and-franchise/michigan-increases-personal-exemption-removes-irc-references.html.

[9] Jared Walczak, “Minnesota Policymakers Strike Tax Conformity Deal,” Tax Foundation, June 11, 2019, https://taxfoundation.org/minnesota-tax-conformity/.

[10] Jamie Rathjen, “North Carolina Increases Standard Deduction for 2020,” Bloomberg Tax, Nov. 12, 2019, https://news.bloombergtax.com/payroll/north-carolina-increases-standard-deduction-for-2020.

[11] “Ohio Enacts Tax Law Changes as Part of 2020-21 Budget,” EY, July 26, 2019, https://taxnews.ey.com/news/2019-1338-ohio-enacts-tax-law-changes-as-part-of-2020-21-budget.

[12] “Due Dates and Tax Rates,” Tennessee Department of Revenue, https://www.tn.gov/revenue/taxes/hall-income-tax/due-date-and-tax-rates.html.

[13] Timothy D. Hugo, “HB 2529 Income tax, state; conformity of taxation system with the IRC, taxable income deductions, etc.,” Virginia’s Legislative Information System, https://lis.virginia.gov/cgi-bin/legp604.exe?191+sum+HB2529.

[14] Bob Lang, “Updated Information on Tax Year 2019 Individual Income Tax Reductions Under Wisconsin Acts 9 and 10,” Wisconsin Legislative Fiscal Bureau, Nov. 4, 2019, https://docs.legis.wisconsin.gov/misc/lfb/misc/205_updated_information_on_tax_year_2019_individual_income_tax_reductions_under_wisconsin_acts_9_and_10_11_4_19.

Share this article