Key Findings

- In general, large industrialized nations tend to have higher statutory corporate income tax rates than developing countries.

- The worldwide average statutory corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate, measured across 176 jurisdictions, is 24.18 percent. When weighted by GDP, the average statutory rate is 26.30 percent.

- Europe has the lowest regional average rate, at 20.27 percent (25.13 percent when weighted by GDP). Conversely, Africa has the highest regional average statutory rate, at 28.45 percent (28.15 percent weighted by GDP).

- The average top corporate rate among EU countries is 21.77 percent, 23.59 percent in OECD countries, and 27.65 percent in the G7.

- The worldwide average statutory corporate taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate has consistently decreased since 1980, with the largest decline occurring in the early 2000s.

- The average statutory corporate tax rate has declined in every region since 1980.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeIntroduction

In 1980, corporate tax rates around the world averaged 40.38 percent, and 46.67 percent when weighted by GDP.[1] Since then countries have recognized the impact that high corporate tax rates have on business investment decisions so that in 2019, the average is now 24.18 percent, and 26.30 when weighted by GDP, for 176 separate tax jurisdictions.

Declines have been seen in every major region of the world including in the largest economies. The 2017 tax reform in the United States brought the statutory corporate income tax rate from among the highest in the world closer to the middle of the distribution. Whereas in 2017 the United States had the fourth highest corporate income tax rate in the world,[3] it now ranks towards the middle of the countries and tax jurisdictions surveyed.

European countries tend to have lower corporate income tax rates than countries in other regions, and many developing countries have corporate income tax rates that are above the worldwide average.

Today, most countries have corporate tax rates below 30 percent.

The Highest and Lowest Corporate Tax Rates in the World[4]

The majority of the 218 separate jurisdictions surveyed for the year 2019 have corporate tax rates below 25 percent and 111 have tax rates between 20 and 30 percent. The average tax rate among the 218 jurisdictions is 22.79 percent.[5] The United States has the 84th highest corporate tax rate with a combined statutory rate of 25.89 percent.

The 20 countries with the highest statutory corporate income tax rates span every region, albeit unequally. While nine of the top 20 countries are in Africa, Europe appears only twice and Asia once. Of the remaining jurisdictions, one is in Oceania, and eight are in the Americas.[6]

The only countries with large economies in the top 20 are France (34.43 percent) and Brazil (34 percent).

| Note: The table includes 21 jurisdictions because Cameroon, Colombia, Saint Kitts and Nevis, and the Seychelles all have the same tax rate.

*The United Arab Emirates is a federation of seven separate emirates. Since 1960, each emirate has the discretion to levy up to a 55 percent corporate tax rate on any business. In practice, this tax is mostly levied on foreign banks and petroleum companies. For more information on the taxation system in the United Arab Emirates, see PwC, “Worldwide Tax Summaries – Corporate income tax (CIT) rates.” Sources: OECD, “Table II.1. Statutory corporate income tax rate,” updated April 2019, https://stats.oecd.org/index.aspx?DataSetCode=Table_II1; KPMG, “Corporate tax rates table,” https://home.kpmg/xx/en/home/services/tax/tax-tools-and-resources/tax-rates-online/corporate-tax-rates-table.html; and researched individually, see . |

||

| Country | Continent | Rate |

|---|---|---|

| United Arab Emirates* | Asia | 55% |

| Comoros | Africa | 50% |

| Puerto Rico | North America | 37.5% |

| Suriname | South America | 36% |

| Chad | Africa | 35% |

| Democratic Republic of the Congo | Africa | 35% |

| Equatorial Guinea | Africa | 35% |

| Guinea | Africa | 35% |

| Kiribati | Oceania | 35% |

| Malta | Europe | 35% |

| Saint Martin (French Part) | North America | 35% |

| Sint Maarten (Dutch part) | North America | 35% |

| Sudan | Africa | 35% |

| Zambia | Africa | 35% |

| France | Europe | 34.43% |

| Brazil | South America | 34% |

| Venezuela (Bolivarian Republic of) | South America | 34% |

| Cameroon | Africa | 33% |

| Colombia | South America | 33% |

| Saint Kitts and Nevis | North America | 33% |

| Seychelles | Africa | 33% |

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeOn the other end of the spectrum, the 20 countries with the lowest non-zero statutory corporate tax rates all charge rates lower than 15 percent. Eleven countries have statutory rates of 10 percent, six being small European nations (Andorra, Bosnia and Herzegovina, Bulgaria, Gibraltar, Kosovo, and Macedonia). The only two major industrialized nations[7] represented among the bottom 20 countries are Ireland and Hungary. Ireland is known for its low 12.5 percent rate, which has been in place since 2003. Hungary reduced its corporate income tax rate from 19 to 9 percent in 2017.[8]

| Note: Table includes 21 jurisdictions because Cyprus, Ireland, and Liechtenstein all have the same tax rate.

Sources: OECD, “Table II.1. Statutory corporate income tax rate”; KPMG, “Corporate tax rates table”; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates/.” |

||

| Country | Continent | Rate |

|---|---|---|

| Barbados | North America | 5.5% |

| Uzbekistan | Asia | 7.5% |

| Turkmenistan | Asia | 8% |

| Hungary | Europe | 9% |

| Montenegro | Europe | 9% |

| Andorra | Europe | 10% |

| Bosnia and Herzegovina | Europe | 10% |

| Bulgaria | Europe | 10% |

| Gibraltar | Europe | 10% |

| Kosovo, Republic of | Europe | 10% |

| Kyrgyzstan | Asia | 10% |

| Nauru | Oceania | 10% |

| Paraguay | South America | 10% |

| Qatar | Asia | 10% |

| The former Yugoslav Republic of Macedonia | Europe | 10% |

| Timor-Leste | Oceania | 10% |

| China, Macao Special Administrative Region | Asia | 12% |

| Republic of Moldova | Europe | 12% |

| Cyprus | Europe | 12.5% |

| Ireland | Europe | 12.5% |

| Liechtenstein | Europe | 12.5% |

Of the 218 jurisdictions surveyed, 13 currently do not impose a general corporate income tax. All these jurisdictions are small, island nations. A handful, such as the Cayman Islands and Bermuda, are well-known for their lack of corporate taxes. Bahrain has no general corporate income tax but has a targeted corporate income tax on oil companies.[9]

| Sources: OECD, “Table II.1. Statutory corporate income tax rate”; KPMG, “Corporate tax rates table”; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates.” | |

| Country | Continent |

|---|---|

| Anguilla | North America |

| Bahamas | North America |

| Bahrain | Asia |

| Bermuda | North America |

| British Virgin Islands | North America |

| Cayman Islands | North America |

| Guernsey | Europe |

| Isle of Man | Europe |

| Jersey | Europe |

| Saint Barthelemy | North America |

| Turks and Caicos Islands | North America |

| Vanuatu | Oceania |

| Wallis and Futuna Islands | Oceania |

Regional Variation in Corporate Tax Rates

Corporate tax rates can vary significantly by region. Africa has the highest average statutory corporate tax rate among all regions, at 28.45 percent. Europe has the lowest average statutory corporate tax rate among all regions, at 20.27 percent.

When weighted by GDP, South America has the highest average statutory corporate tax rate at 32.01 percent. Europe has the lowest weighted average statutory corporate income tax, at 25.13 percent.

In general, larger and more industrialized nations tend to have higher corporate income tax rates than smaller nations. These rates are often above the worldwide average. The G7, which is comprised of the seven wealthiest nations in the world, has an average statutory corporate income tax rate of 27.65 percent, and a weighted average rate of 27.22 percent. OECD member states have an average statutory corporate tax rate of 23.59 percent, and a rate of 26.53 percent when weighted by GDP. The BRICS[10] have an average statutory rate of 27.40 percent, and a weighted average statutory corporate income tax rate of 26.52 percent.

| Sources: Statutory corporate income tax rates are from OECD, “Table II.1. Statutory corporate income tax rate”; KPMG, “Corporate tax rates table”; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates.” GDP calculations are from the U.S. Department of Agriculture, “International Macroeconomics Data Set.” | |||

| Region | Average Rate | Average Rate Weighted by GDP | Number of Countries Covered |

|---|---|---|---|

| Africa | 28.45% | 28.15% | 49 |

| Asia | 21.32% | 26.08% | 46 |

| Europe | 20.27% | 25.13% | 39 |

| North America | 25.85% | 26.26% | 22 |

| Oceania | 23.75% | 29.74% | 8 |

| South America | 27.63% | 32.01% | 12 |

| G7 | 27.65% | 27.22% | 7 |

| OECD | 23.59% | 26.53% | 36 |

| BRICS | 27.40% | 26.52% | 5 |

| EU | 21.77% | 25.95% | 28 |

| G20 | 27.11% | 26.94% | 19 |

| World | 24.18% | 26.30% | 176 |

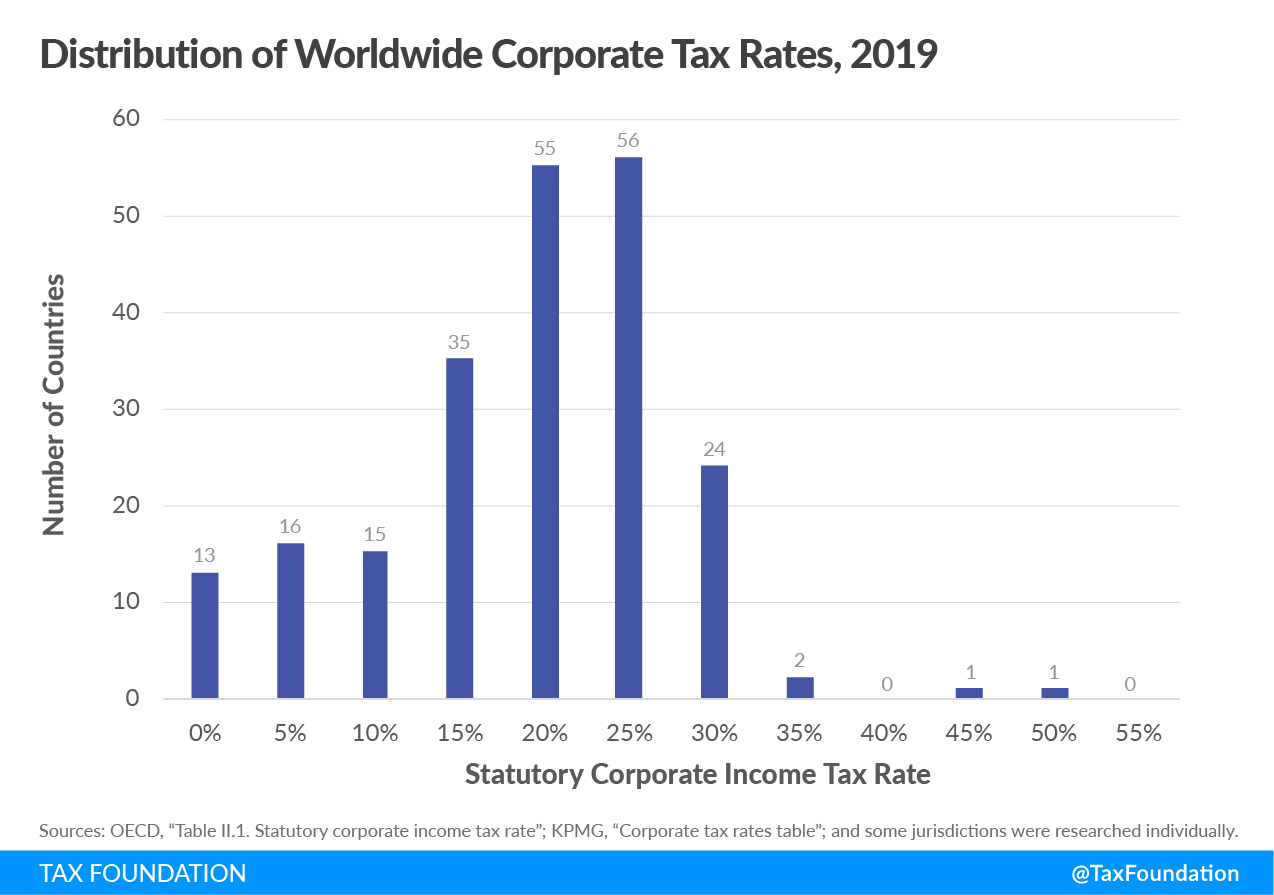

Distribution of Corporate Tax Rates[11]

Very few tax jurisdictions impose a corporate income tax at statutory rates greater than 35 percent. The following chart shows a distribution of corporate income tax rates among 218 jurisdictions in 2019. A plurality of countries (111 total) impose a rate between 20 and 30 percent. Twenty-four jurisdictions have a statutory corporate tax rate between 30 and 35 percent. Seventy-nine jurisdictions have a statutory corporate tax rate lower than 20 percent, and 190 jurisdictions have a corporate tax rate below 30 percent.

Figure 1.

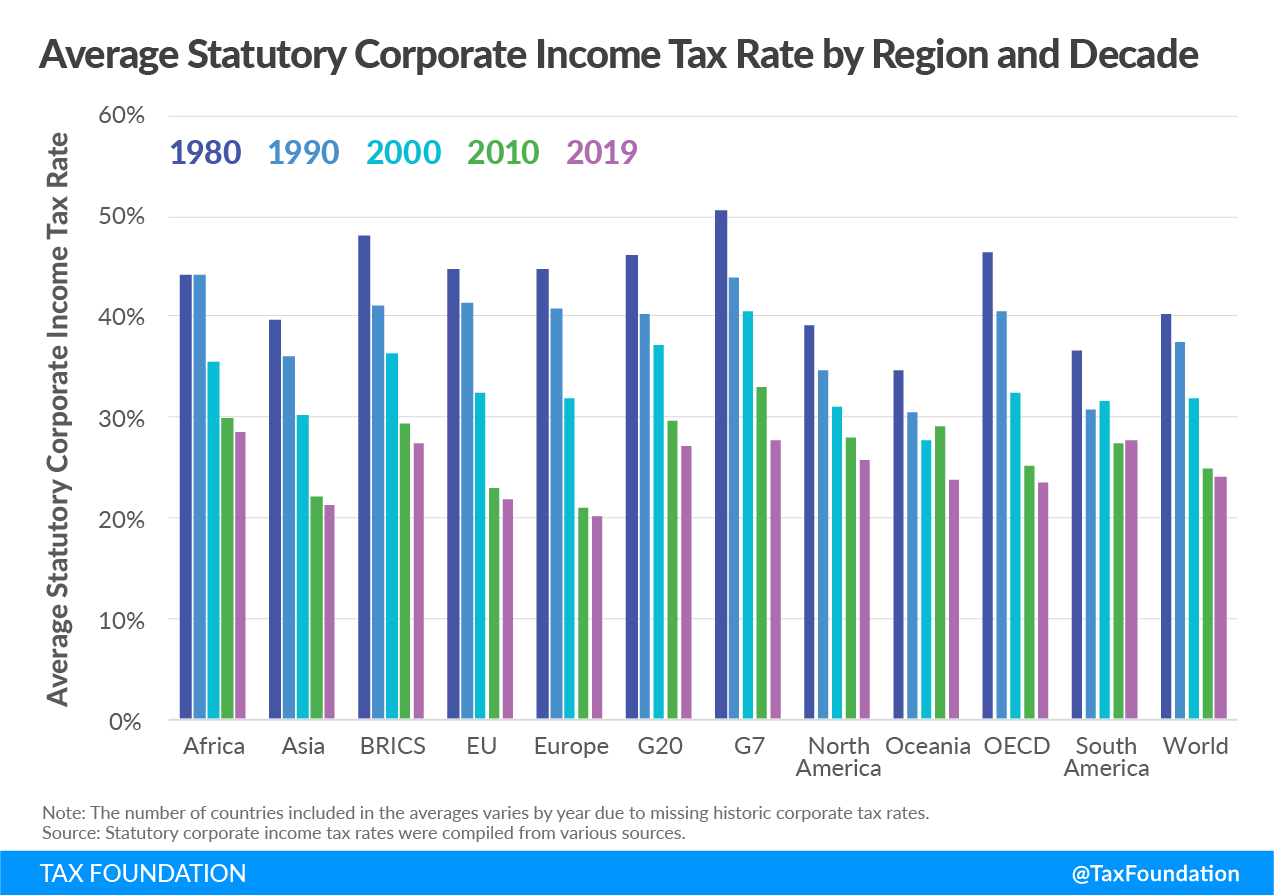

The Decline of Corporate Tax Rates Since 1980

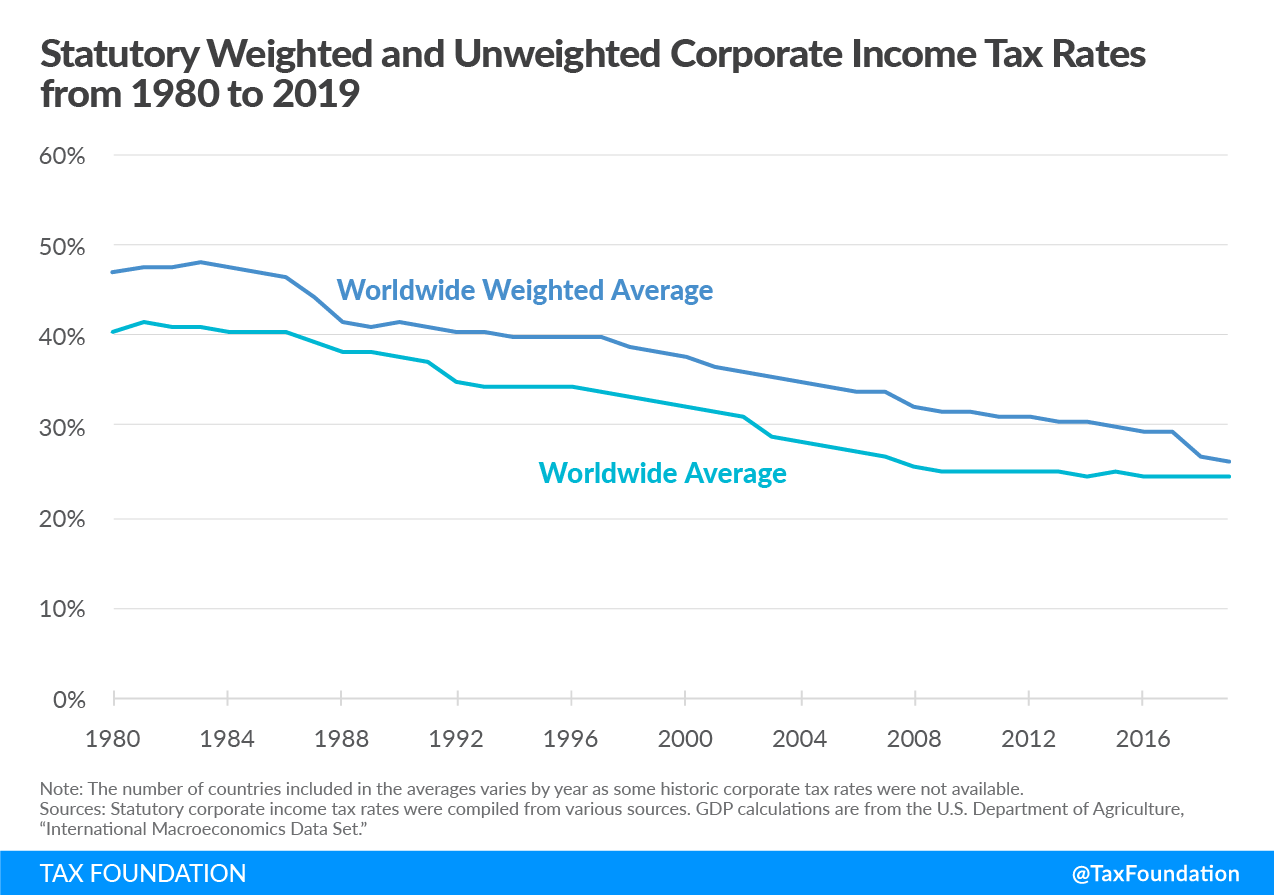

Over the past 39 years, corporate tax rates have consistently declined on a global basis. In 1980, the unweighted average worldwide statutory tax rate was 40.38 percent. Today, the average statutory rate stands at 24.18 percent, representing a 40 percent reduction over the 39 years surveyed.[12]

The weighted average statutory rate has remained higher than the simple average over this period. Prior to U.S. tax reform in 2017, the United States was largely responsible for keeping the weighted average so high, given its relatively high tax rate, as well as its significant contribution to global GDP. Figure 2 shows the significant impact the change in the U.S. corporate rate had on the worldwide weighted average. The weighted average statutory corporate income tax rate has declined from 46.67 percent in 1980 to 26.30 percent in 2019, representing a 44 percent reduction over the 39 years surveyed.

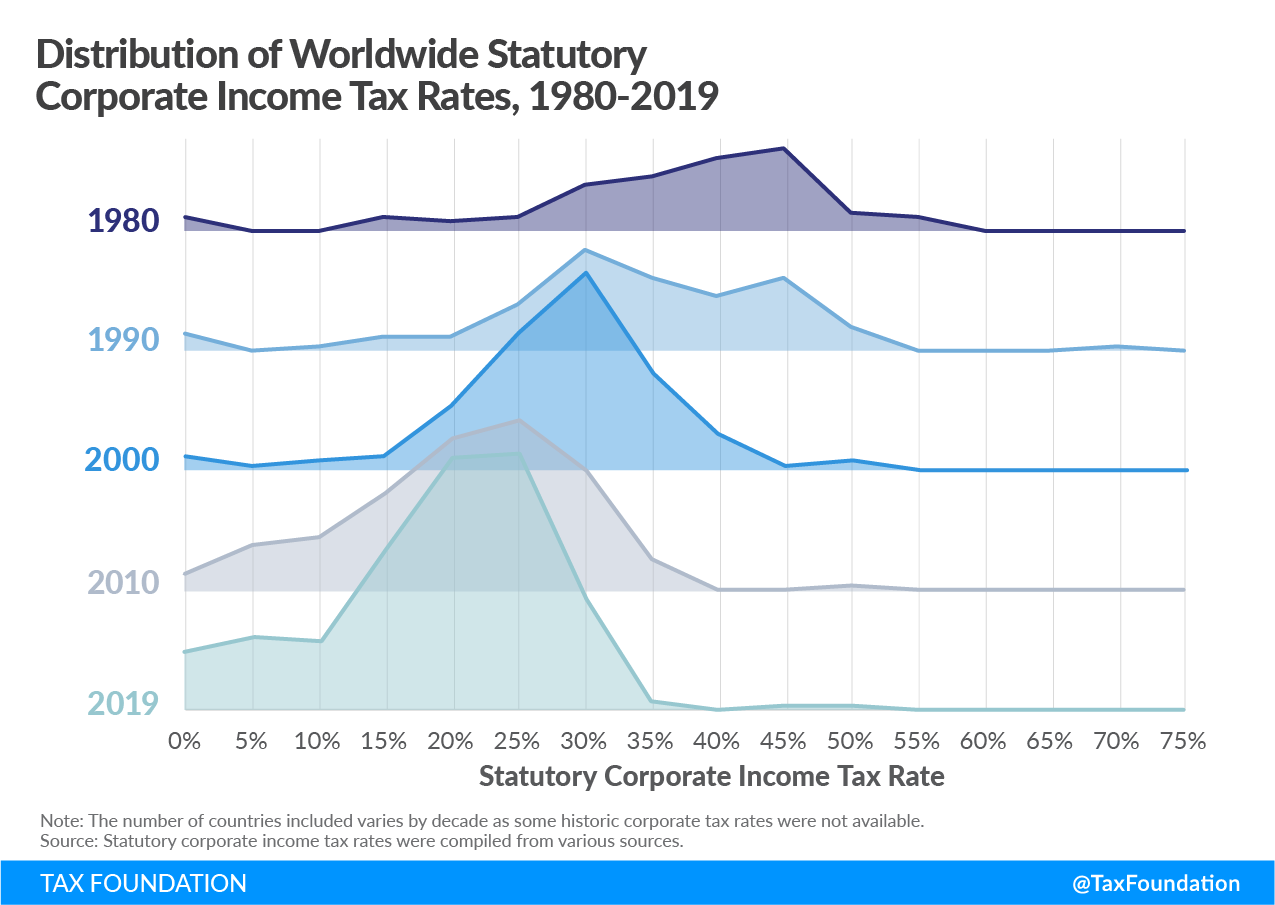

Over time, more countries have shifted to taxing corporations at rates lower than 30 percent, with the United States following this trend with its tax changes at the end of 2017. This changing distribution of corporate tax rates has been far from consistent. The largest shift occurred between 2000 and 2010, with 77 percent of countries imposing a statutory rate below 30 percent in 2010 and only 41 percent of countries imposing a statutory rate below 30 percent in 2000.[13]

All regions saw a net decline in average statutory rates between 1980 and 2019. The average declined the most in Europe, with the 1980 average of 44.6 percent dropping to 20.27 percent, representing almost a 55 percent rate reduction. South America has seen the smallest decline, with the average only decreasing by 25 percent, from 36.66 percent in 1980 to 27.63 percent in 2019.

Africa, Oceania, and South America all saw periods where the average statutory rate increased, although the average rates decreased in all regions over the full period. In each instance of an average rate increase, the change was relatively small, with the absolute change being less than 2 percentage points between decades.

Figure 2.

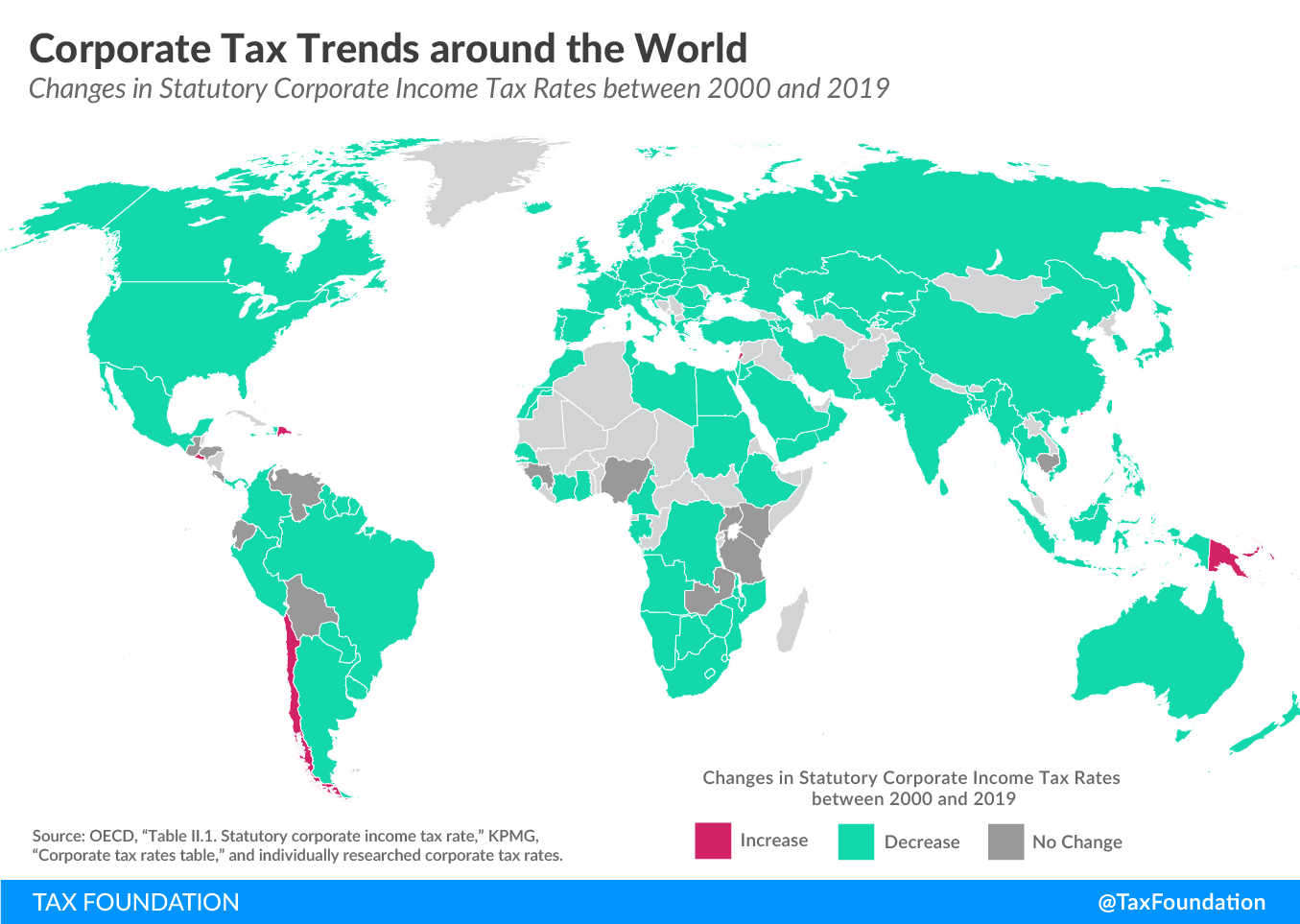

The following map illustrates the global trend towards lower corporate income tax rates. Of the 138 jurisdictions for which the dataset includes the statutory income tax rates for both the years 2000 and 2019, only six countries have increased their rates during that time frame: Chile (from 15 percent to 25 percent), the Dominican Republic (from 25 percent to 27 percent), El Salvador (from 25 percent to 30 percent), Hong Kong (from 16 percent to 16.5 percent), Lebanon (from 10 percent to 17 percent), and Papua New Guinea (from 25 percent to 30 percent). Nineteen jurisdictions have the same corporate income tax rate in 2019 as in 2000, and 113 jurisdictions have decreased their rates over that time period.

Figure 3

Figure 4

Figure 5

Conclusion

Worldwide and regional average top corporate tax rates have declined over the last decades, with most countries following the trend. Of 138 jurisdictions around the world, only six have increased their corporate income tax rates between 2000 and 2019, while nineteen have not changed their rates, and 113 have decreased them. The trend would seem to be continuing, as several countries are planning to reduce their corporate tax rates in the coming years.[14]

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeAppendix

The Dataset

Scope

The dataset compiled for this publication includes the 2019 statutory corporate income tax rates of 218 sovereign states and dependent territories around the world. Tax rates were researched only for jurisdictions that are among the almost 250 sovereign states and dependent territories that have been assigned a country code by the International Organization for Standardization (ISO). As a result, zones or territories that are independent taxing jurisdictions but do not have their own country code are not included in the dataset.

In addition, the dataset includes historic statutory corporate income tax rates for the time period 1980 to 2018. However, these years cover tax rates of fewer than 218 jurisdictions due to missing data points.

To be able to calculate average statutory corporate income tax rates weighted by GDP, the dataset includes GDP data for 176 jurisdictions. When used to calculate average statutory corporate income tax rates, either weighted by GDP or unweighted, only these 176 jurisdictions are included (to ensure the comparability of the unweighted and weighted averages).

Definition of Selected Corporate Income Tax Rate

The dataset captures standard top statutory corporate income tax rates levied on domestic businesses. This means:

- The dataset does not reflect special tax regimes, including but not limited to patent boxes, offshore regimes, or special rates for specific industries.

- A number of countries levy lower rates for businesses below a certain revenue threshold. The dataset does not capture these lower rates.

- A few countries levy gross revenue taxes on businesses instead of corporate income taxes. Since the tax rates of a corporate income tax and a gross revenue tax are not comparable, these countries are excluded from the dataset.

Sources

Tax Rates for the Year 2019

For OECD countries, the statutory corporate income tax rates used are the combined corporate income tax rates provided by the OECD; see OECD, “Table II.1. Statutory corporate income tax rate,” updated April 2019, https://stats.oecd.org/index.aspx?DataSetCode=Table_II1. The main source for non-OECD jurisdictions are the statutory rates provided by KPMG; see KPMG, “Corporate tax rates table,” 2019, https://home.kpmg/xx/en/home/services/tax/tax-tools-and-resources/tax-rates-online/corporate-tax-rates-table.html. Jurisdictions that are not part of either source were researched individually. The source for each of these jurisdictions is listed in a GitHub repository; see Tax Foundation, “worldwide-corporate-tax-rates,” GitHub, https://github.com/TaxFoundation/worldwide-corporate-tax-rates.

Tax Rates for the Years 1980-2018

Tax rates for the time frame between 1980 and 2018 are taken from a dataset compiled by the Tax Foundation over the last years. These historic rates come from multiple sources: PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2010-2018; KPMG, “Corporate Tax Rate Survey,” 1998- 2003; KPMG, “Corporate tax rates table,” 2003-2018; EY, “Worldwide Corporate Tax Guide,” 2004-2018; OECD, “Historical Table II.1 – Statutory corporate income tax rate,” 1999, http://www.oecd.org/tax/tax-policy/tax-database.htm#C_CorporateCaptial; the University of Michigan – Ross School of Business, “World Tax Database,” https://www.bus.umich.edu/otpr/otpr/default.asp; and numerous government websites.

Gross Domestic Product (GDP) for the years 1980-2019

GDP calculations are from the U.S. Department of Agriculture, “International Macroeconomics Data Set,” December 2018, https://www.ers.usda.gov/data-products/international-macroeconomic-data-set/.

[1] Unless otherwise noted, calculated averages of statutory corporate income tax rates only include jurisdictions for which GDP data is available for all years between 1980 and 2019. For 2019, the dataset includes statutory corporate income tax rates of 218 jurisdictions, but GDP data is available for only 176 jurisdictions, reducing the number of jurisdictions included in calculated averages to 176. For years prior to 2019, the number of countries included in calculated averages varies by year due to missing corporate tax rates; that is, the 1980 average includes statutory corporate income tax rates of 74 jurisdictions compared to 176 jurisdictions in 2019.

[2] Statutory corporate income tax rates are from OECD, “Table II.1. Statutory corporate income tax rate,” updated April 2019, https://stats.oecd.org/index.aspx?DataSetCode=Table_II1; KPMG, “Corporate tax rates table,” https://home.kpmg/xx/en/home/services/tax/tax-tools-and-resources/tax-rates-online/corporate-tax-rates-table.html; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates,” GitHub, https://github.com/TaxFoundation/worldwide-corporate-tax-rates. GDP calculations are from the U.S. Department of Agriculture, “International Macroeconomics Data Set,” December 2018, https://www.ers.usda.gov/data-products/international-macroeconomic-data-set/.

[3] Kari Jahnsen and Kyle Pomerleau, “Corporate Income Tax Rates around the World, 2017,” Tax Foundation, Sept. 7, 2017, https://taxfoundation.org/corporate-income-tax-rates-around-the-world-2017/.

[4] As no averages are presented in this section, it covers all 218 jurisdictions for which 2019 corporate income tax rates were found (thus including jurisdictions for which GDP data was not available).

[5] This average is lower than the average of the 176 jurisdictions because many of the jurisdictions for which no GDP data is available are small economies with low corporate income tax rates.

[6] Although called the “top 20 rates,” they include 21 jurisdictions because Cameroon, Colombia, Saint Kitts and Nevis, and the Seychelles all have the same corporate income tax rate of 33 percent.

[7] Major industrialized nations are those that are members of the OECD.

[8] Although called the “bottom 20 rates,” they include 21 jurisdictions because Cyprus, Ireland, and Liechtenstein all have the same tax rate.

[9] This tax rate can be as high as 46 percent. See Deloitte, “International Tax – Bahrain Highlights,” last updated April 2019, https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-bahrainhighlights-2019.pdf.

[10] BRICS is a group of countries with major emerging economies. The members of this group are Brazil, Russia, India, China, and South Africa.

[11] As no averages are presented in this chapter, it covers all 218 jurisdictions for which 2019 corporate income tax rates were found (thus including jurisdictions for which GDP data was not available).

[12] Historical data comes from multiple sources: PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2010-2018; KPMG, “Corporate Tax Rate Survey,” 1998- 2003; KPMG, “Corporate tax rates table,” 2003-2018; EY, “Worldwide Corporate Tax Guide,” 2004-2018; OECD, “Historical Table II.1 – Statutory corporate income tax rate,” 1999, http://www.oecd.org/tax/tax-policy/tax-database.htm#C_CorporateCaptial; the University of Michigan – Ross School of Business, “World Tax Database,” https://www.bus.umich.edu/otpr/otpr/default.asp; and numerous government websites.

[13] This section of the report covers all 218 jurisdictions for which 2019 corporate income tax rates were found (thus including jurisdictions for which GDP data was not available).

[14] Daniel Bunn, “Upcoming Corporate Tax Rate Reductions in Developed Countries,” Tax Foundation, Sept. 13, 2018, https://taxfoundation.org/upcoming-corporate-tax-rate-reductions-developed-countries/.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe