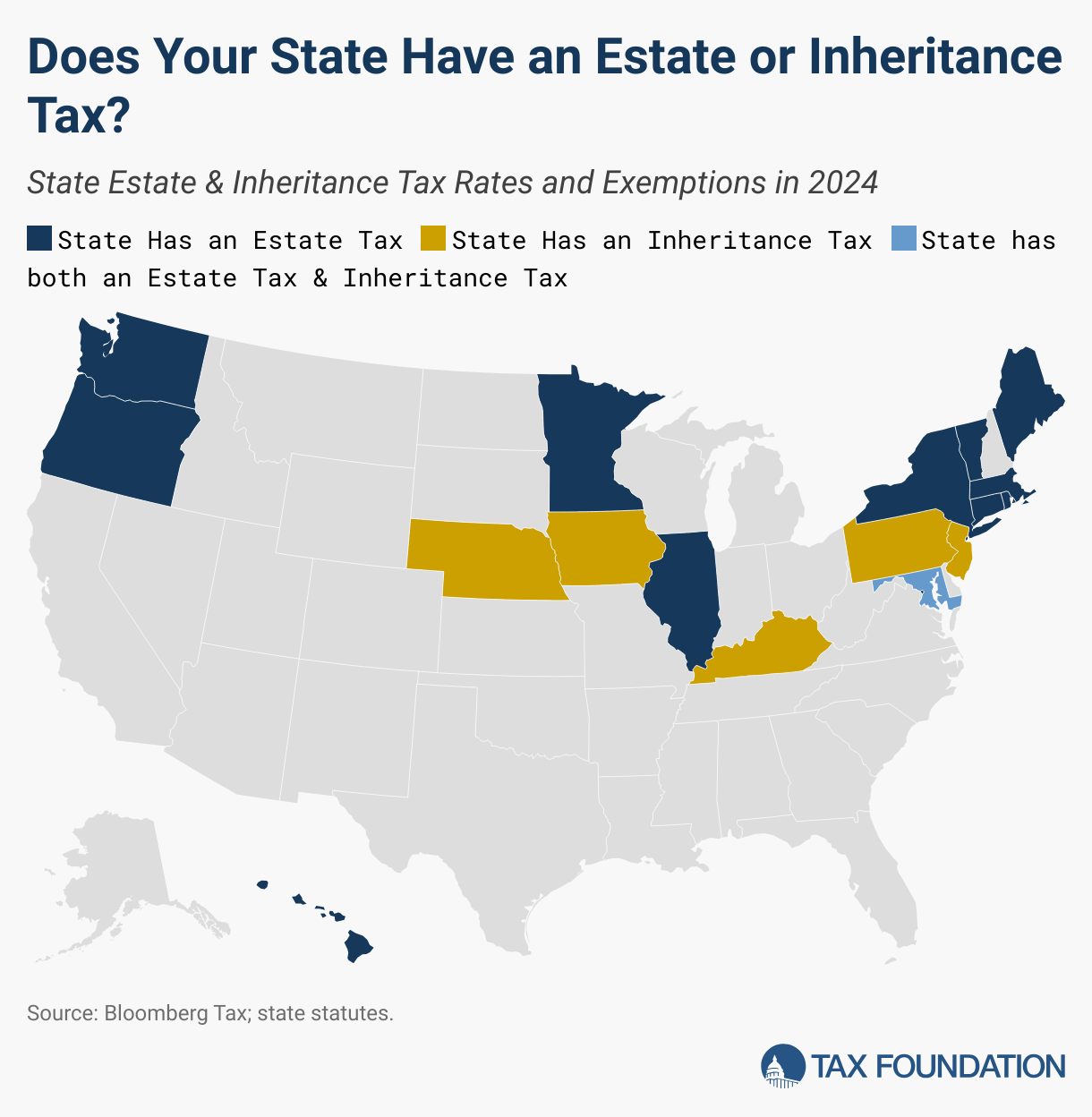

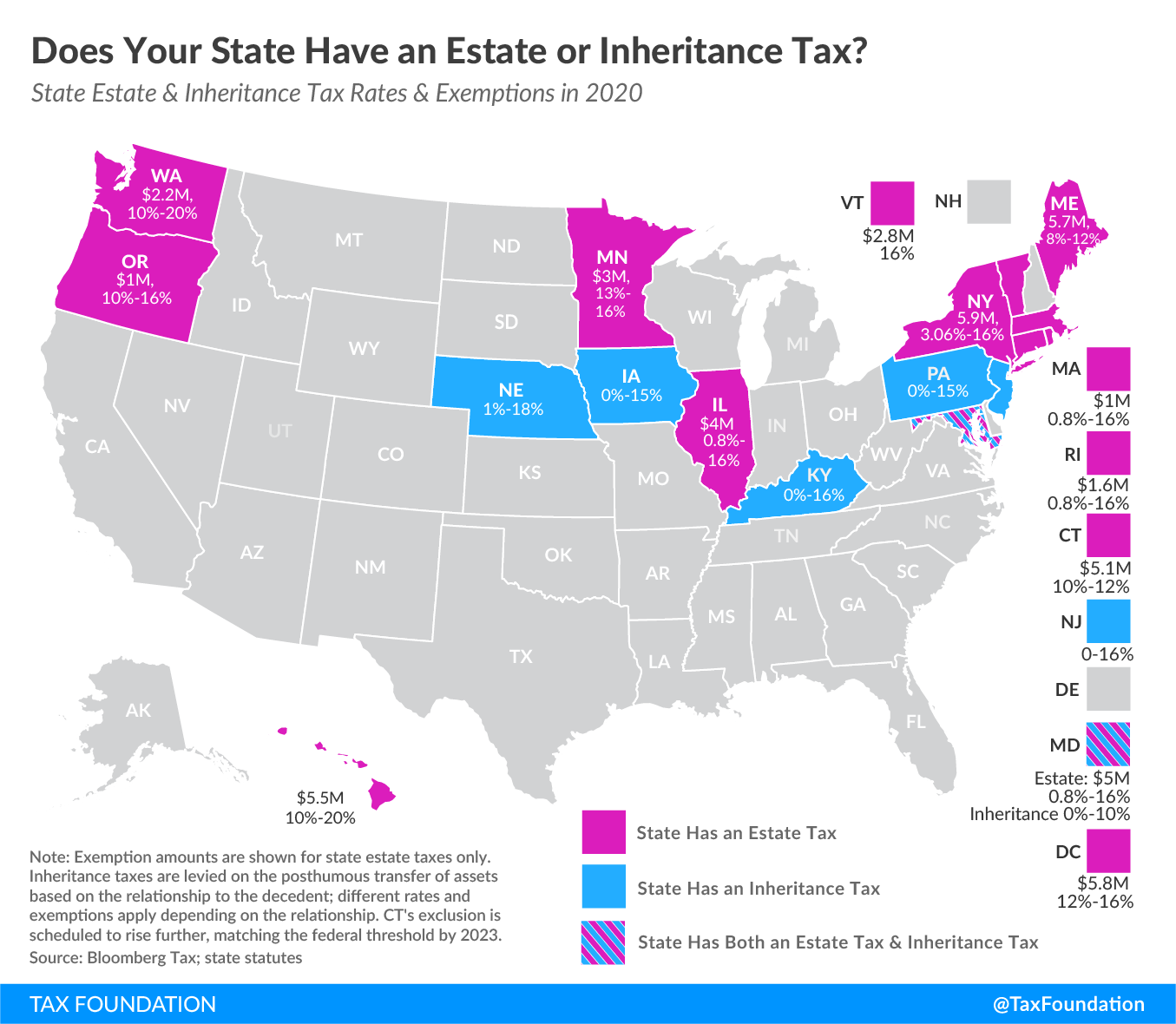

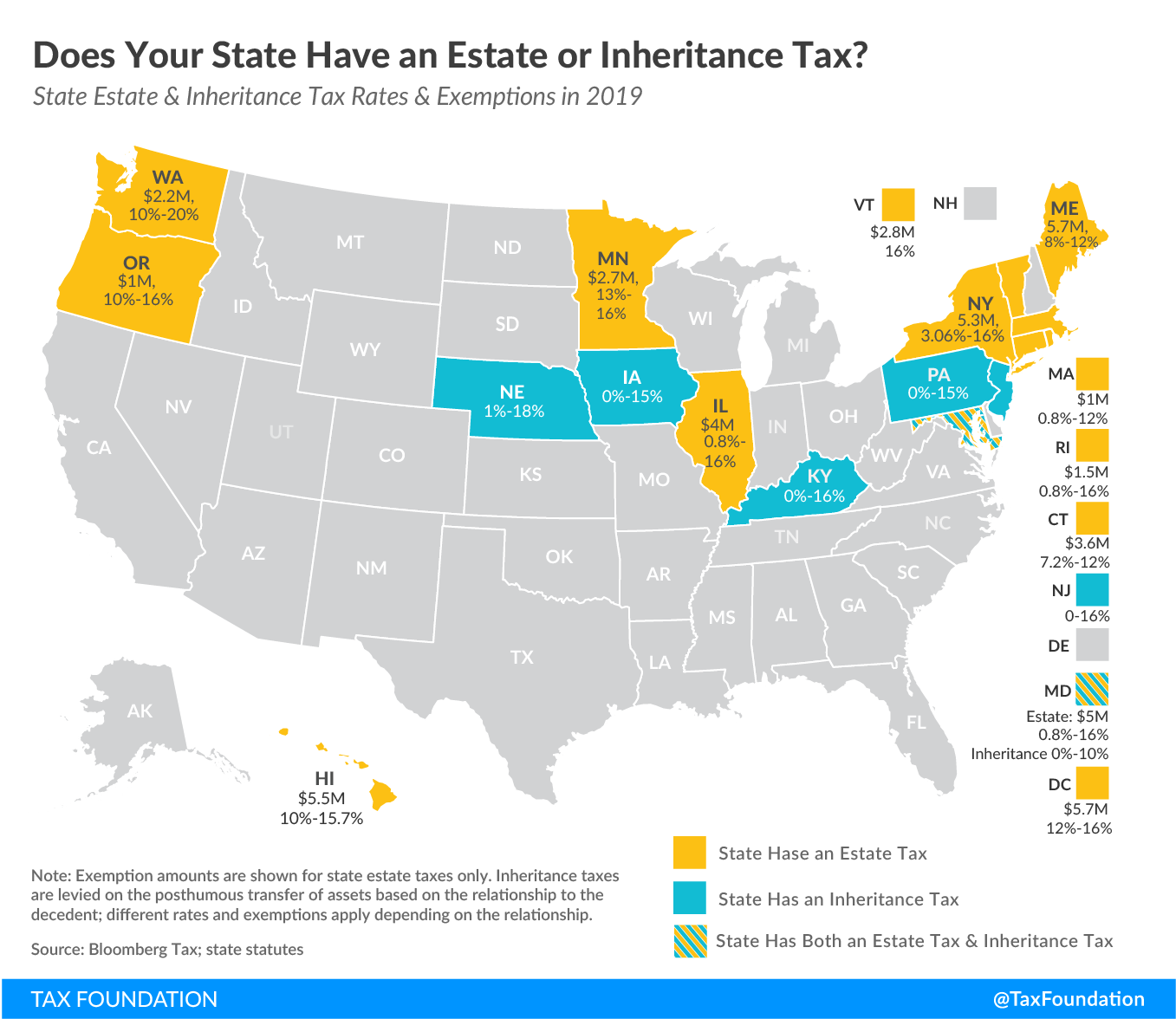

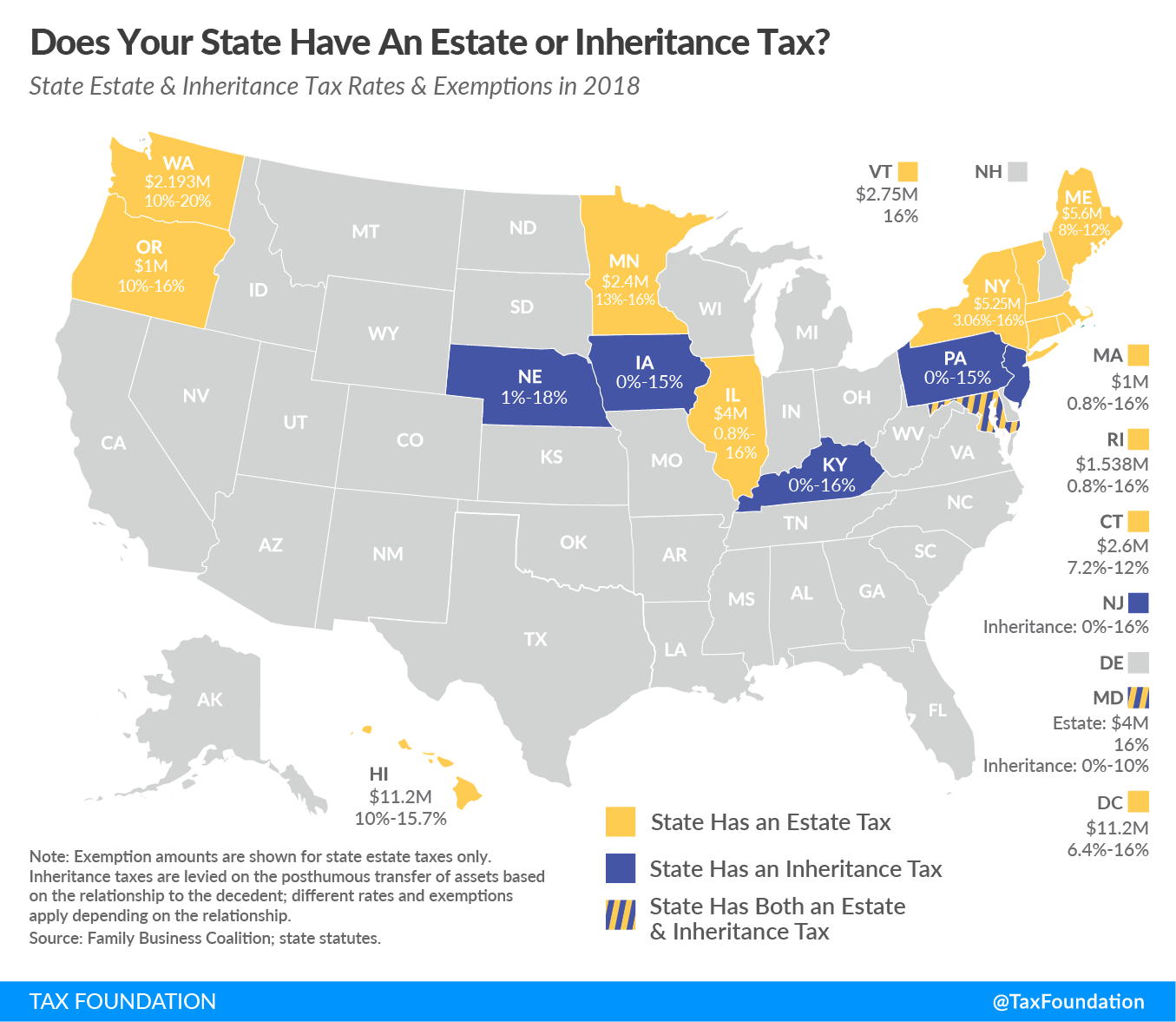

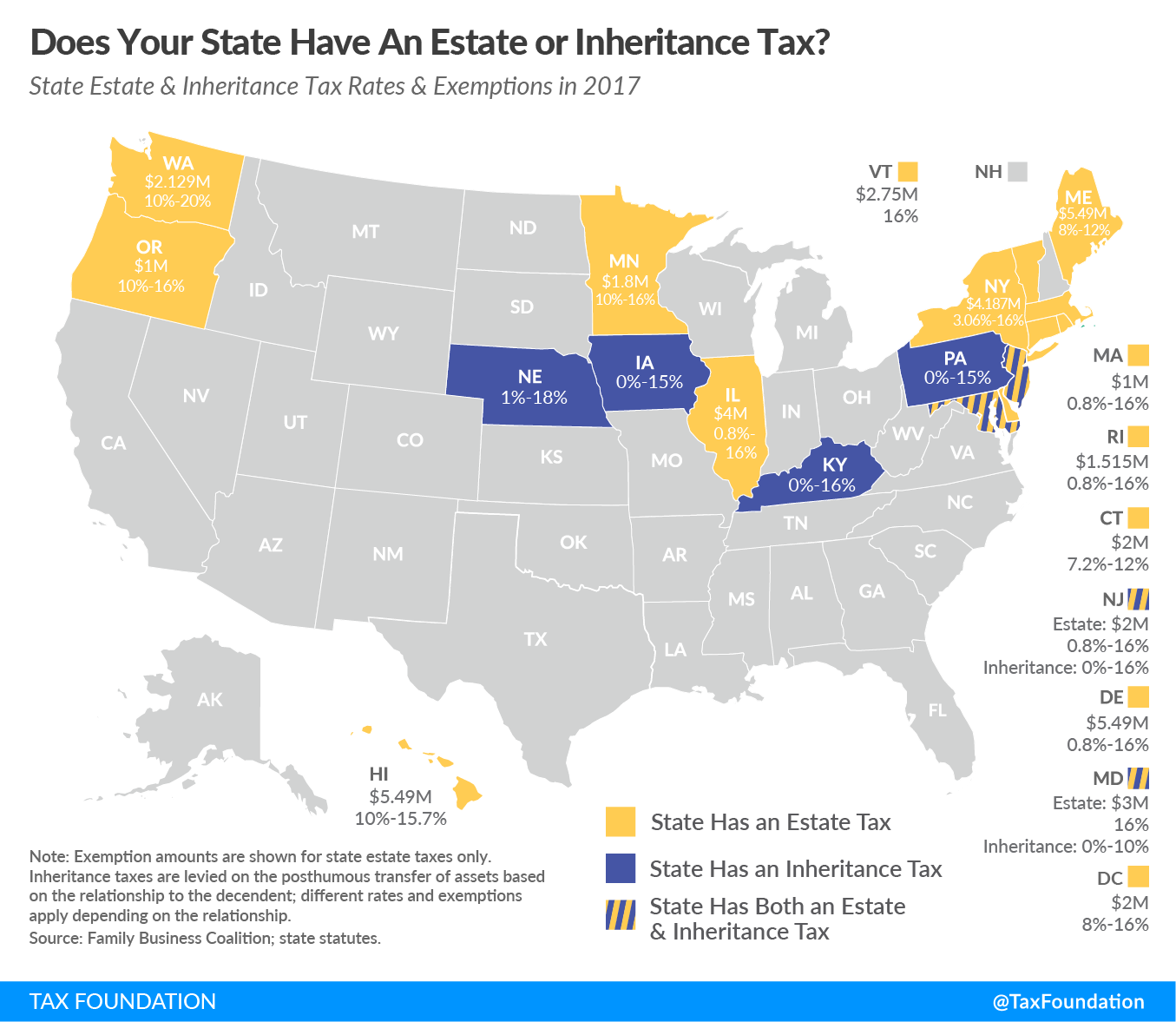

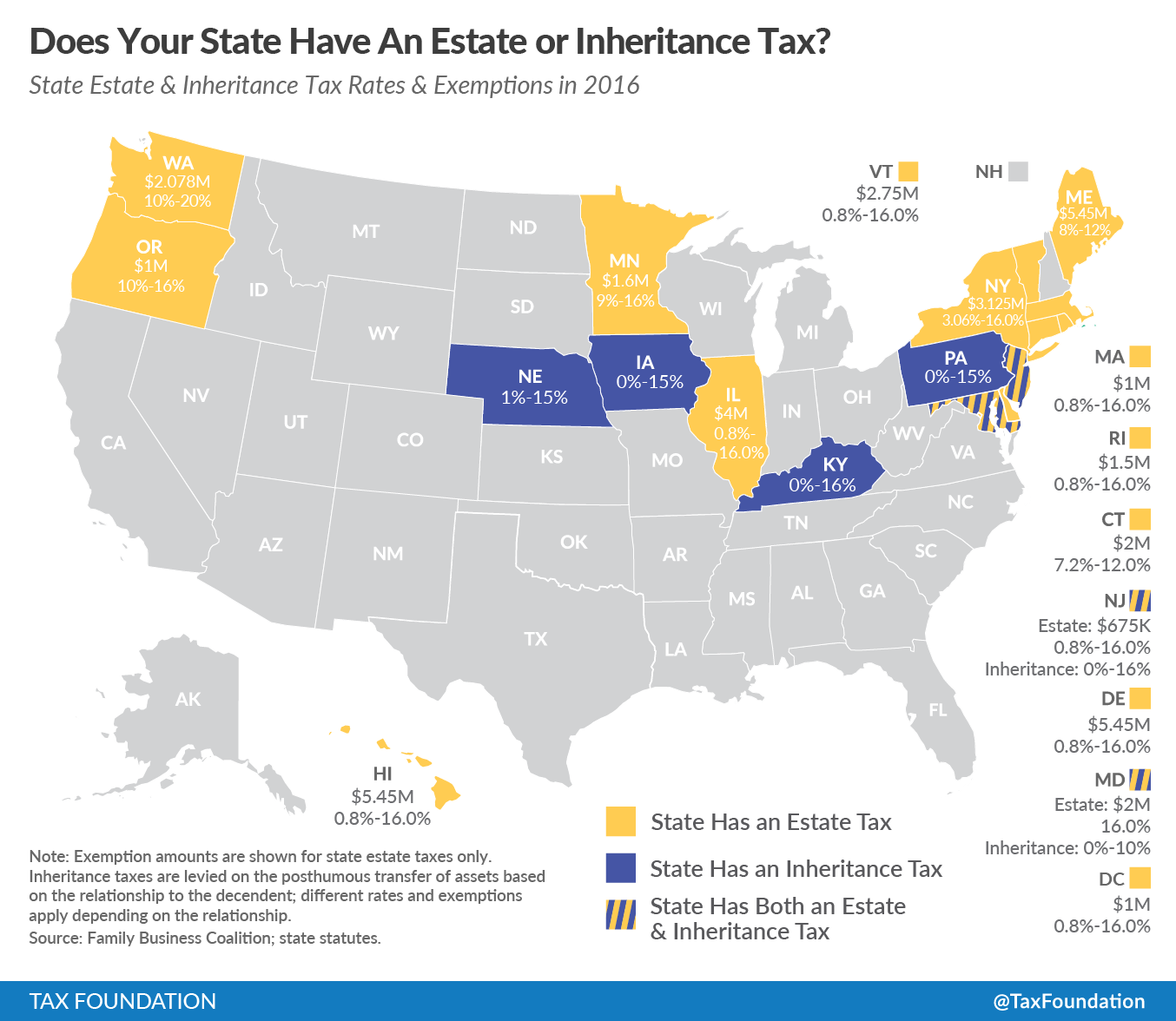

In addition to the federal estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs. , with a top rate of 40 percent, 12 states and the District of Columbia impose additional estate taxes, while six states levy inheritance taxes. Maryland is the only state that imposes both an estate and an inheritance taxAn inheritance tax is levied upon the value of inherited assets received by a beneficiary after a decedent’s death. Not to be confused with estate taxes, which are paid by the decedent’s estate based on the size of the total estate before assets are distributed, inheritance taxes are paid by the recipient or heir based on the value of the bequest received. .

Estate taxes are paid by a decedent’s estate before assets are distributed to heirs and are thus imposed on the overall value of the estate. Inheritance taxes are remitted by the recipient of a bequest and are thus based on the amount distributed to each beneficiary.

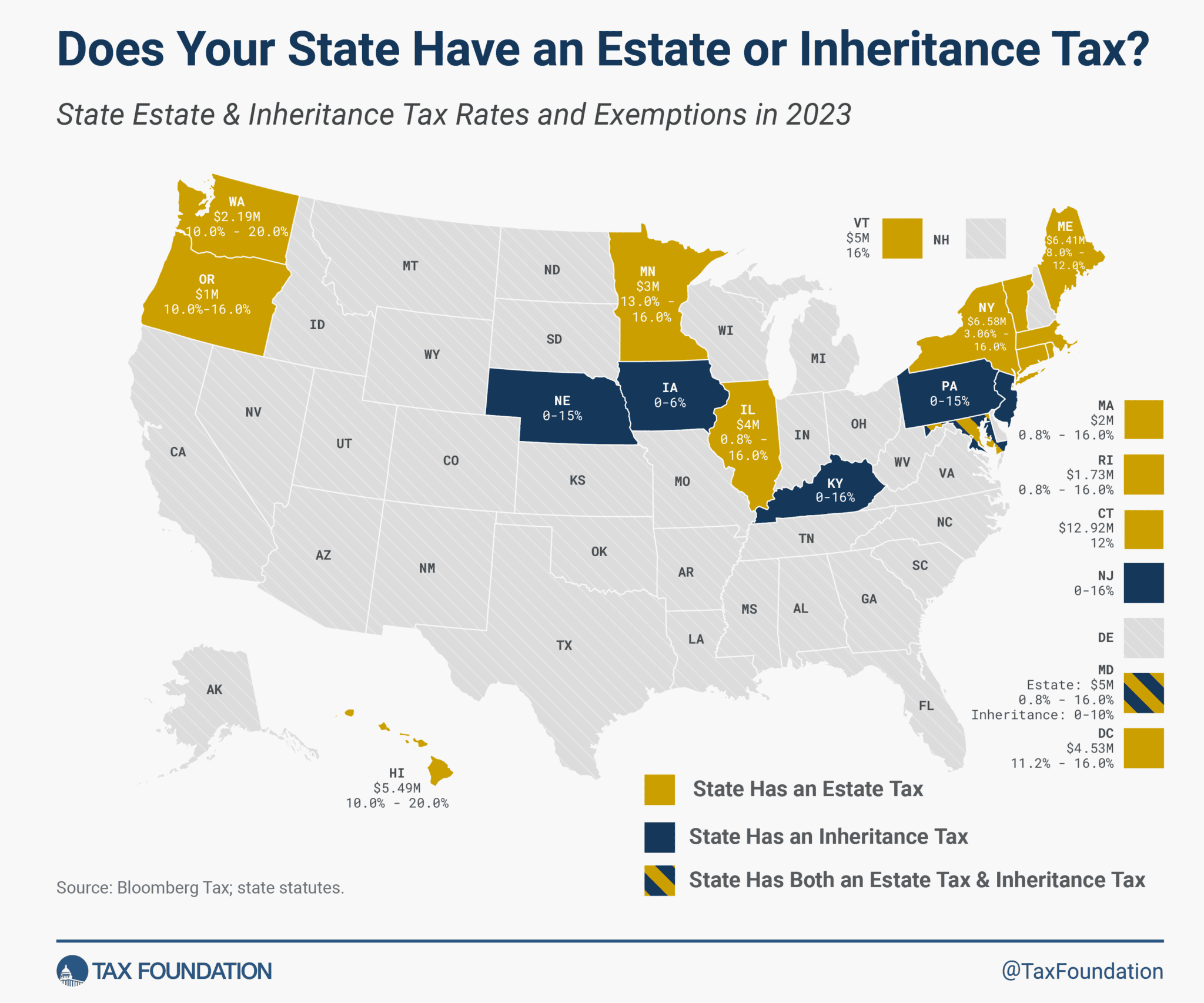

Most estate and inheritance taxes are progressive, with the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. on a decedent’s estate or a beneficiary’s inheritance exposed to rates that increase with the total value of assets. Hawaii and Washington have the highest top marginal estate tax rate at 20 percent, assessed on estates valued at $15.49 million and $9 million, respectively. Seven other states and the District of Columbia assess a 16 percent top marginal estate tax rate on estates valued between $2 million (Massachusetts) and $10.04 million (Illinois). Connecticut is the only state with a flat estate tax rate of 12 percent. Combined with its high exemption value of $13.61 million, Connecticut has a well-structured estate tax that makes it suitable for possible reforms and eventual elimination.

Likewise, Iowa has the lowest inheritance tax rate in the nation at 2 percent, while Kentucky and New Jersey have the highest top marginal inheritance tax rate of 16 percent as of January 1, 2024.

Does Your State Have an Estate or Inheritance Tax?

State Estate & Inheritance Tax Rates and Exemptions in 2024

| State | Estate Tax Exemption | Inheritance Tax Exemption | Estate Tax Rate | Inheritance Tax Rate |

|---|---|---|---|---|

| Connecticut | 13,610,000.00 $ | 12% | ||

| Hawaii | 5,490,000.00 $ | 10.0% - 20.0% | ||

| Illinois | 4,000,000.00 $ | 0.8% - 16.0% | ||

| Iowa | 0 - 2% | |||

| Kentucky | 1,000.00 $ | 0-16% | ||

| Maine | 6,800,000.00 $ | 8.0% - 12.0% | ||

| Maryland | 5,000,000.00 $ | 0.8% - 16.0% | 0-10% | |

| Massachusetts | 2,000,000.00 $ | 0.8% - 16.0% | ||

| Minnesota | 3,000,000.00 $ | 13.0% - 16.0% | ||

| Nebraska | 100,000.00 $ | 0-15% | ||

| New Jersey | 25,000.00 $ | 0-16% | ||

| New York | 6,940,000.00 $ | 3.06% - 16.0% | ||

| Oregon | 1,000,000.00 $ | 10.0%-16.0% | ||

| Pennsylvania | 0-15% | |||

| Rhode Island | 1,774,583.00 $ | 0.8% - 16.0% | ||

| Vermont | 5,000,000.00 $ | 16% | ||

| Washington | 2,193,000.00 $ | 10.0% - 20.0% | ||

| District of Columbia | 4,715,600.00 $ | 11.2% - 16.0% |

Data compiled by Joseph Johns

Estate and inheritance taxes are burdensome. They disincentivize investment and can drive high-net-worth individuals out of state. They also yield estate planning and tax avoidance strategies that are inefficient, not only for affected taxpayers but also for the economy at large. The handful of states that still impose them should consider gradually eliminating them or at least conforming to federal exemption levels.

Under the Tax Cuts and Jobs Act (TCJA) of 2017, the federal estate tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. was raised from $5.49 million to $11.18 million per person, with inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. adjustments (in tax year 2024, the federal exemption is $13.61 million), though this provision expires December 31, 2025. Connecticut is the sole state that pegged its state estate tax exemption threshold to the federal threshold for tax year 2024. New York has the second-highest exemption by excluding $6.94 million from its unusually high-rate estate tax.

Six states assess an alternative tax on bequests, known as the inheritance tax. New Jersey and Kentucky have the highest top marginal rates at 16 percent. Iowa is in its final year of phasing out its inheritance tax, and its rates currently range from 1 percent to 2 percent on inheritances valued between $12,500 and $150,000. This is a significant decrease since its top marginal rate was capped at 6 percent in 2023.

Because estate taxes in particular encourage wealthy individuals to move out of state—depriving the state of tax revenue that would have been generated during their lifetimes—many states eliminated their estate tax following federal law changes in the 2000s, and some are engaging in current legislative discussions about reforms to their estate and/or inheritance taxes. Connecticut, Iowa, Massachusetts, Minnesota, New York, Oregon, and Washington all featured legislative discussions surrounding changes to these taxes in 2024.

Prior to 2005, the federal government incentivized states to assess state-level estate taxes by offering a federal credit against state estate taxes. This made estate taxes an attractive option for states since taxpayers were paying the same amount in estate taxes whether their state levied the tax or not. After the federal government fully phased out the state estate tax credit in 2005, some states stopped collecting estate taxes by default, as their provisions were directly linked with the federal credit, while others responded by repealing their tax legislatively.

2024 Notable Changes

- Iowa reduced continued to reduce its inheritance tax rate from 5 percent to 1 percent in 2024.

- New York increased its exemption threshold by $360,000 from $6.58 million to $6.94 million in 2024.

- Maine increased its exemption threshold by $390,000 from $6.41 million to $6.8 million in 2024.

- Connecticut aligned with the federal exemption threshold of $13.61 million in 2024.

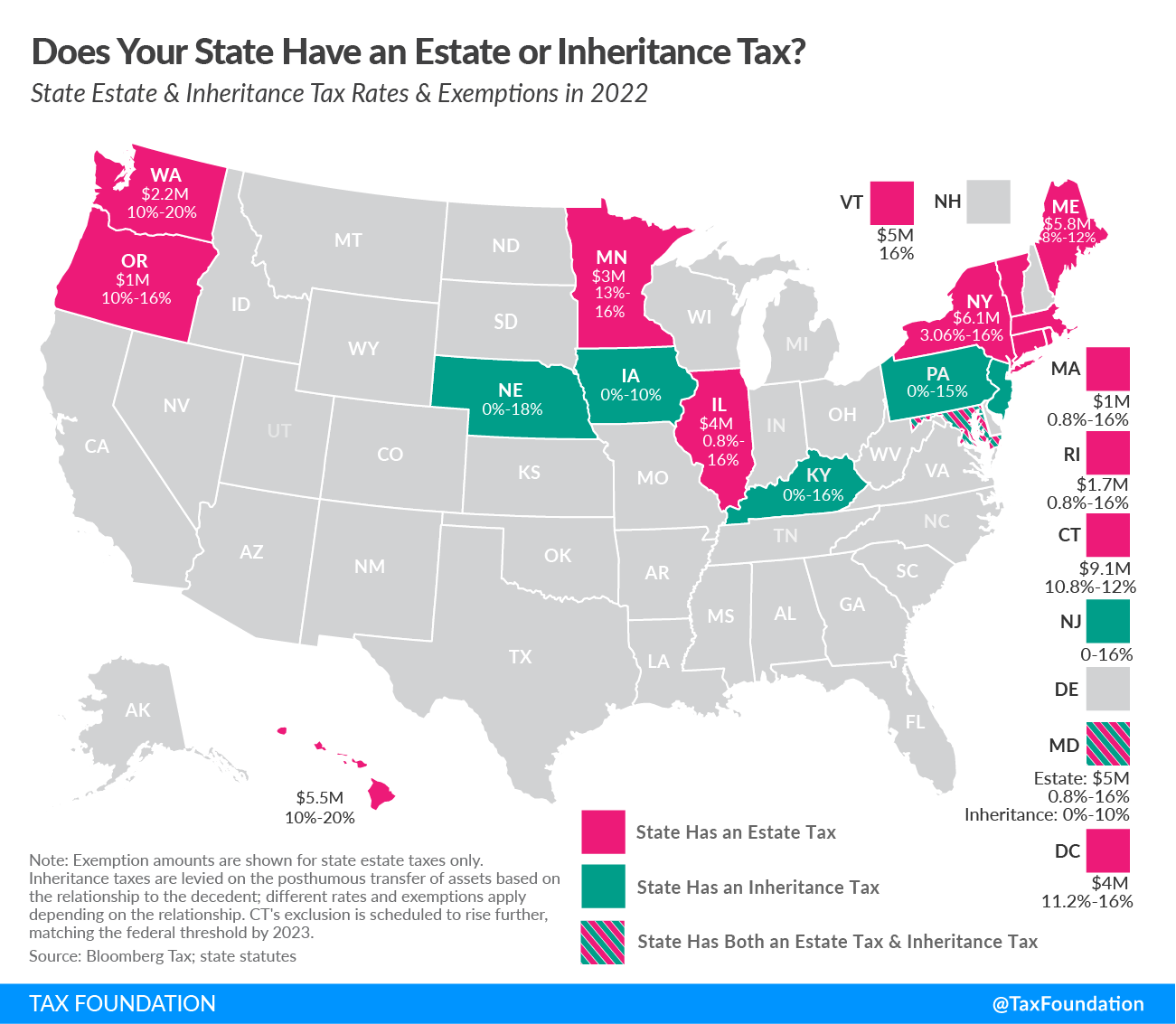

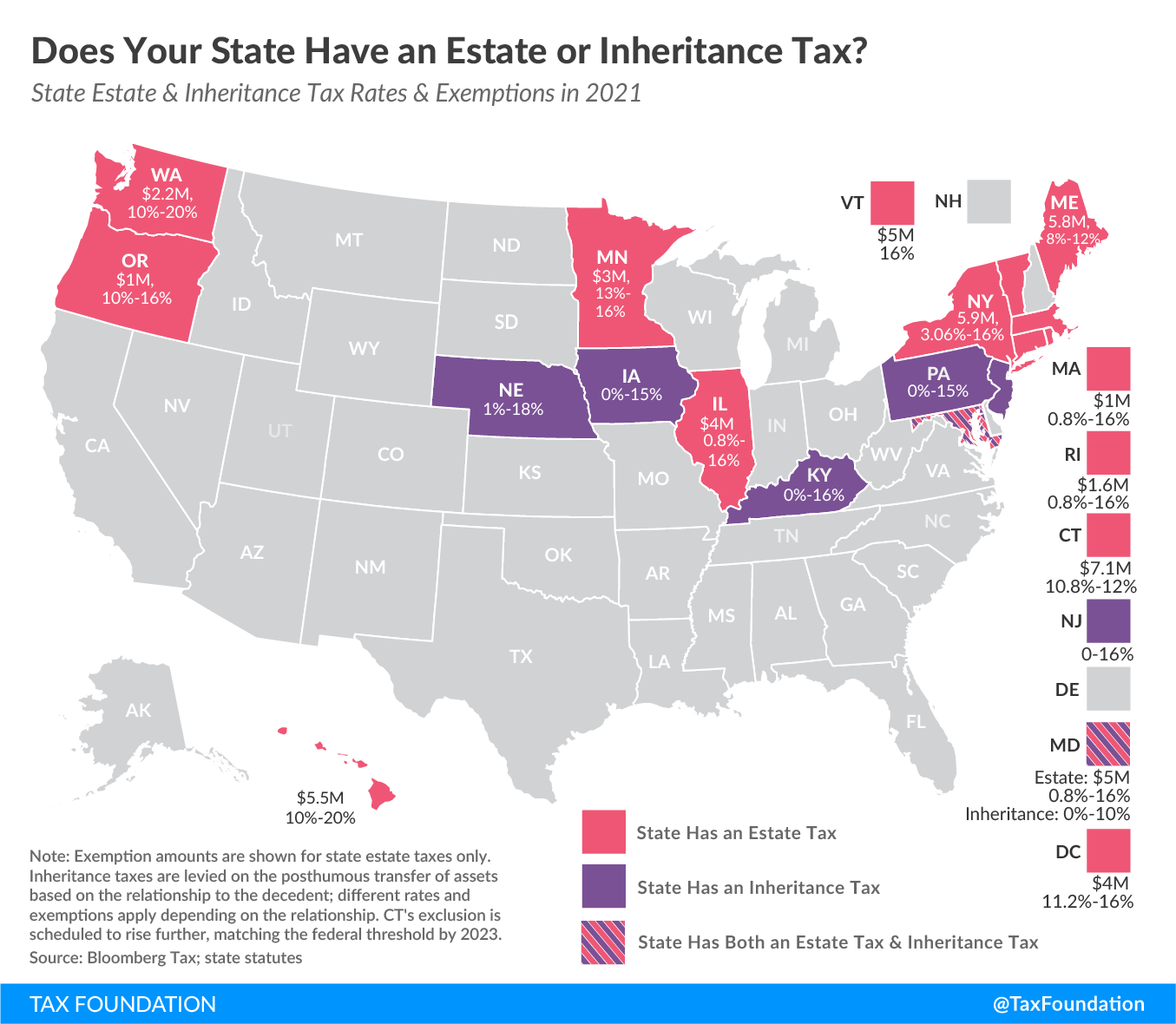

Particularly after 2005, most states have been moving away from estate or inheritance taxes or have raised their exemption levels, as these taxes hurt states’ competitiveness and create incentives to avoid paying them, especially for wealthy taxpayers. Delaware repealed its estate tax at the beginning of 2018. New Jersey finished phasing out its estate tax at the same time, and now only imposes an inheritance tax. Vermont finished phasing in an exemption increase in 2021, bringing the exemption to $5 million that year, compared to $4.5 million in 2020. Maine increased its threshold by the highest percentage, relative to 2023 values, boosting the exemption threshold by 5.7 percent in 2024. Connecticut also finished phasing in an increase to its exemption, matching the federal estate tax exemption, and simultaneously transitioned to the flat tax rate.

In two more states, Hawaii and Illinois, attempts to eliminate (Hawaii) or reform (Illinois) the estate tax fell short in 2024.

Four of the six states with inheritance taxes—Kentucky, Maryland, New Jersey, and Pennsylvania—structure their inheritance taxes such that the rate structure varies based on the proximity of the bequest recipients to the decedent. States with this proximity test give preferential treatment, usually lower rates or higher exemption thresholds, to immediate family members while taxing those further away from the decedent at higher rates. The 12 states that impose estate taxes increase the burdens for generational wealth transfers which can reduce economic growth due to this unnecessary tax. These states should consider ways to eventually phase out and eliminate this tax to promote the stability of family businesses, reduce transaction costs, and prevent government overreach during an already difficult time for the friends and family of the deceased.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe