Key Findings

- A typical American household with four phones on a “family share” plan, paying $100 per month for taxable wireless service, can expect to pay about $270 per year in taxes, fees, and surcharges—up from $260 in 2019.

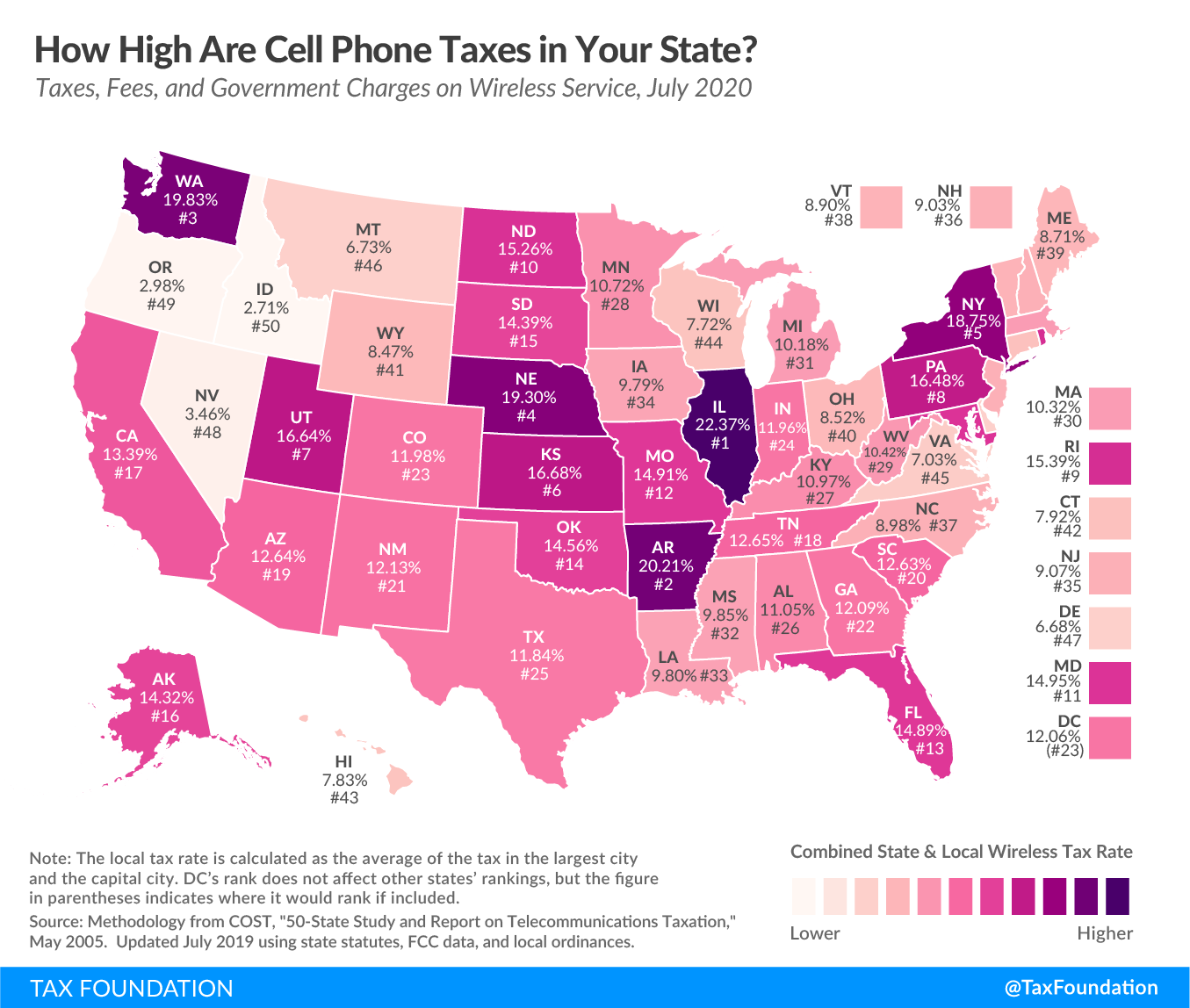

- Nationally, these impositions make up about 22.6 percent of the average bill—the highest rate ever. Illinois has the highest wireless taxes in the country at 32.2 percent, followed by Arkansas at 30.0 percent, Washington at 29.7 percent, Nebraska at 29.1 percent, and New York at 28.6 percent.

- Since 2008, average monthly wireless service bills per subscriber have dropped by 26 percent, from $50 per line to about $37 per line. However, wireless taxes have increased by 50 percent, from 15.1 percent to 22.6 percent of the average bill.

- At the end of 2019, over 67 percent of low-income adults had wireless as their phone service, and 58 percent of all adults were wireless-only. Excessive taxes and fees, especially the very high per-line charges, impose a disproportionate burden on low-income consumers. In Chicago, a family with four lines of taxable wireless service paying $100 per month is subjected to over $500 per year in taxes and fees.

Introduction

Taxes, fees, and government surcharges on wireless consumers increased again in 2020, jumping from 21.7 percent to 22.6 percent of a customer’s bill.[1] An American household with four wireless phones paying $100 per month for wireless voice service can expect to pay about $270 per year in wireless taxes, fees, and surcharges—up from $260 in 2019.

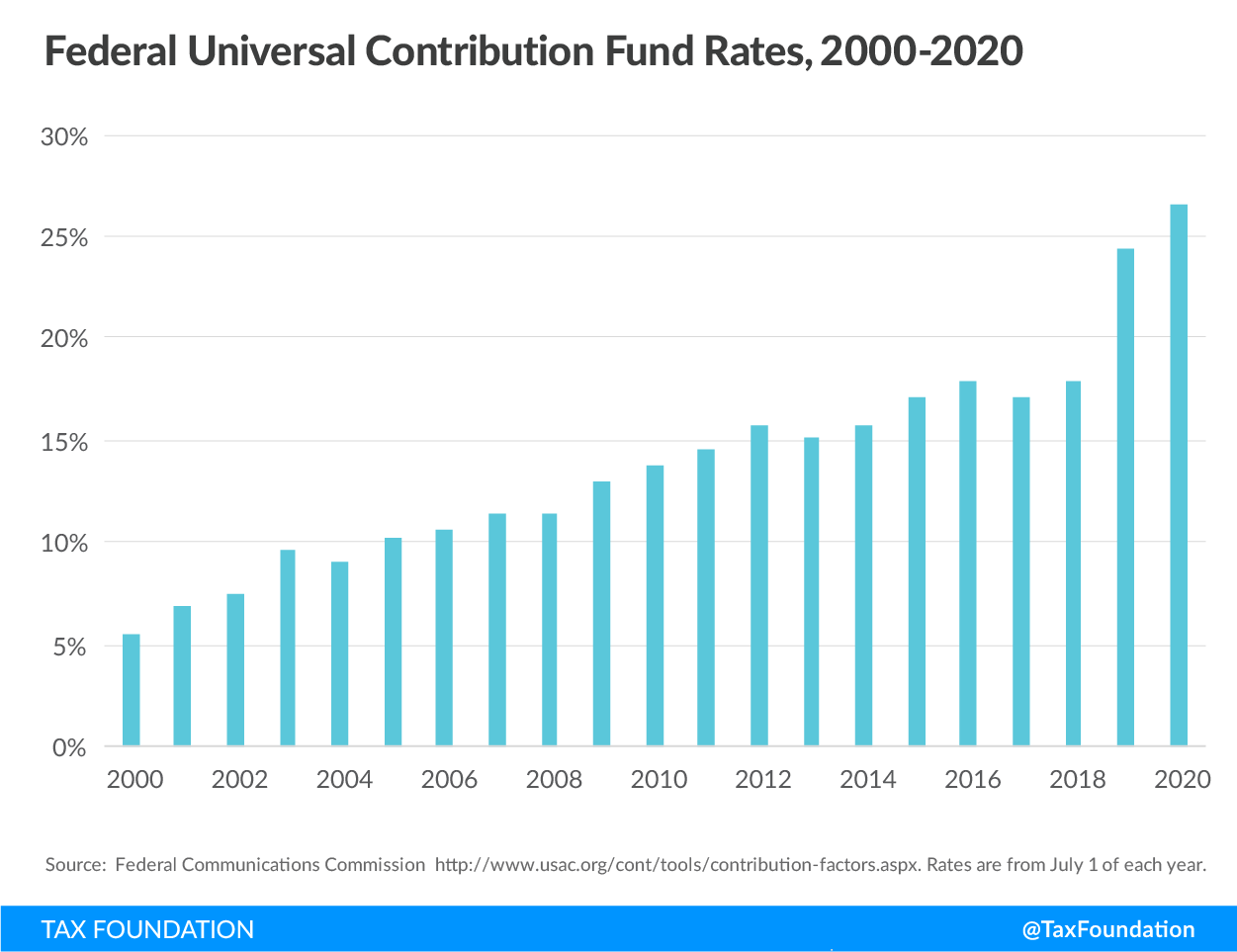

State and local taxes on wireless services increased slightly, from 12.7 percent to 12.8 percent, the seventh consecutive increase. The Federal Universal Service Fund (FUSF) surcharge increased from 9.1 percent to 9.8 percent of the typical wireless voice bill—a 9 percent increase in 2020, following a 36 percent increase in 2019.

Fortunately for wireless consumers, price competition continues to push down the average monthly per-line cost of wireless voice service. Average revenue per subscriber fell for the fourth consecutive year, from $41.50 per month in 2017 to $36.86 per month in 2020. Unfortunately, consumers were not able to fully enjoy this price reduction because taxes, fees, and surcharges increased again.

Wireless consumers will pay an estimated $17.5 billion in taxes, fees, and government surcharges to federal, state, and local governments in 2020 based on the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rates calculated in this report. These taxes, fees, and surcharges break down as follows:

- $5.6 billion in sales taxes and other non-discriminatory consumption taxes

- $6.3 billion in FUSF surcharges

- $3.5 billion in 911 fees, a category that includes hundreds of millions of dollars that are not actually used for 911 purposes in some states

- $2.1 billion in other industry-specific state and local taxes and fees

Consumers in Illinois continue to pay the highest wireless taxes in the country. This year, thanks to large increases in the 911 fee and other state charges, Arkansas now has the second highest wireless taxes in the country. Wireless users in Idaho, Oregon, and Nevada pay the lowest wireless taxes.

Wireless service is increasingly the sole means of communications and connectivity for many Americans, particularly young people, and those with lower incomes. At the end of 2019, according to the Centers for Disease Control and Prevention, about 67 percent of all low-income adults lived in wireless-only households and 58 percent of adults of all incomes lived in wireless-only households.[2] These excessive taxes and fees—especially those that impose high per-line taxes and fees—impose a disproportionate tax burden on those least able to afford them.

Wireless Taxes and Fees Increase in 2020

This is the eleventh in a series of reports that examine trends in taxes, fees, and government surcharges imposed on wireless voice service by federal, state, and local governments since 2003. The methodology, originally developed by the Council on State Taxation in a 1999 report, is detailed in Appendix A.

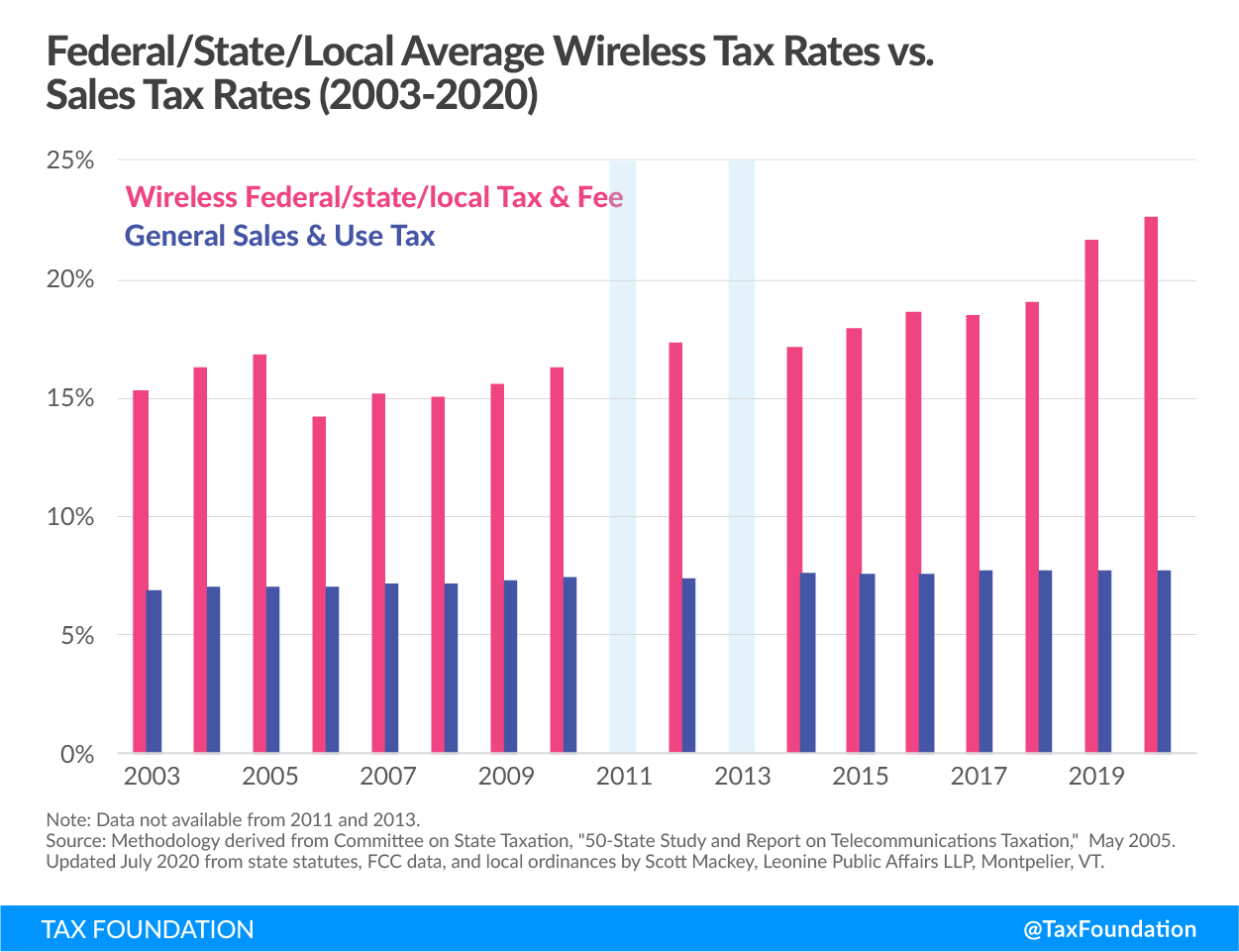

Table 1 shows national trends in tax rates imposed by all levels of government on taxable wireless service between 2003 and 2020. Between 2005 and 2006, wireless taxes decreased after the federal courts forced the IRS to end the imposition of the 3 percent federal excise tax on wireless service. After that court decision, wireless tax rates dropped to a low of 14.1 percent. Since then, however, wireless tax rates have climbed steadily to their current rate of 22.6 percent.

| Weighted Average | |||||

|---|---|---|---|---|---|

| Wireless: State & Local tax & fee | Wireless: Federal tax & fee | Wireless: Federal/State/Local tax & fee | General Sales/Use Tax | Disparity — Wireless Tax Over General Sales Tax | |

| 1/1/2003 | 10.20% | 5.07% | 15.27% | 6.87% | 3.33% |

| 4/1/2004 | 10.74% | 5.48% | 16.22% | 6.93% | 3.81% |

| 7/1/2005 | 10.94% | 5.91% | 16.85% | 6.94% | 4.00% |

| 7/1/2006 | 11.14% | 2.99% | 14.13% | 7.04% | 4.10% |

| 7/1/2007 | 11.00% | 4.19% | 15.19% | 7.07% | 3.93% |

| 7/1/2008 | 10.86% | 4.23% | 15.09% | 7.11% | 3.75% |

| 7/1/2009 | 10.74% | 4.79% | 15.53% | 7.26% | 3.48% |

| 7/1/2010 | 11.21% | 5.05% | 16.26% | 7.42% | 3.79% |

| 7/1/2012 | 11.36% | 5.82% | 17.18% | 7.33% | 4.03% |

| 7/1/2014 | 11.23% | 5.82% | 17.05% | 7.51% | 3.72% |

| 7/1/2015 | 11.50% | 6.46% | 17.96% | 7.57% | 3.93% |

| 7/1/2016 | 11.93% | 6.64% | 18.57% | 7.61% | 4.32% |

| 7/1/2017 | 12.11% | 6.34% | 18.46% | 7.65% | 4.46% |

| 7/1/2018 | 12.46% | 6.64% | 19.10% | 7.65% | 4.81% |

| 7/1/2019 | 12.65% | 9.05% | 21.70% | 7.74% | 4.91% |

| 7/1/2020 | 12.82% | 9.83% | 22.65% | 7.75% | 5.07% |

|

Note: Federal includes 3 percent federal excise tax (until May 2006) and Federal Universal Service Fund (FUSF) charge, which is set by the FCC and varies quarterly. FUSF charge as of July 1, 2020 is calculated by 37.1 percent interstate safe harbor times 26.5 percent contribution factor, which equals a 9.83 percent effective tax rate, http://www.usac.org/cont/tools/contribution-factors.aspx. Source: Methodology derived from Committee on State Taxation, “50-State Study and Report on Telecommunications Taxation,” May 2005; updated July 2020 from state statutes, FCC data, and local ordinances by Scott Mackey, Leonine Public Affairs LLP, Montpelier, VT. |

|||||

Table 1 also separates the impact of federal taxes and surcharges from state and local government taxes, fees, and surcharges. Throughout the period, state and local taxes have been trending upward steadily, from 10.20 percent in 2003 to their current level of 12.82 percent in 2020.

The FUSF surcharge has also increased throughout the period, but with dramatic increases since 2018. In just two years, the effective rate of the FUSF surcharge increased by 48 percent, from 6.64 percent to 9.83 percent of the average wireless bill. For a detailed explanation of the FUSF charge and how it is imposed, see Appendix B.Table 1 also separates the impact of federal taxes and surcharges from state and local government taxes, fees, and surcharges. Throughout the period, state and local taxes have been trending upward steadily, from 10.20 percent in 2003 to their current level of 12.82 percent in 2020.

Table 1 also shows the general trends in average tax rates of the sales and use tax, which is the primary broad-based consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or income taxes where all savings are tax-deductible. imposed by 45 states, the District of Columbia, and Puerto Rico. Since 2003, the average state-local sales tax rate has increased by 0.88 percentage points—from 6.87 percent to 7.75 percent. During that same period, wireless taxes increased by 2.62 percentage points—from 10.20 percent to 12.82 percent. Average wireless tax rates increased three times faster than average sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. rates.

Wireless industry competition has led to significant reductions in average monthly bills since 2008, a trend that accelerated between 2016 and 2020. Since 2008, average wireless monthly bills have decreased from just under $50 per month to $36.86 per month—a 26 percent reduction—while wireless taxes have increased from 15.1 percent to 22.6 percent—a 50 percent increase. Unfortunately, consumers have not enjoyed the full benefits of wireless price competition because taxes, fees, and government surcharges continue to increase.

Table 2 shows wireless tax, fee, and government surcharge rates as of July 2020. Column 1 shows the average combined state-local tax rate in the largest city and the capital city in each state, while column 2 shows the effective rate of the FUSF surcharge. In 2020, Illinois retained its ranking as the state with the highest wireless tax burden. Arkansas moved up from the sixth highest taxes in 2019 to the second highest in 2020, followed by Washington, Nebraska, and New York.

| State Rankings | 2020 Wireless State-Local Rate | 2019 Federal USF Rate | 2020 Combined Federal/State/Local Rate | |

|---|---|---|---|---|

| 1 | Illinois | 22.37% | 9.83% | 32.20% |

| 2 | Arkansas | 20.21% | 9.83% | 30.04% |

| 3 | Washington | 19.83% | 9.83% | 29.66% |

| 4 | Nebraska | 19.30% | 9.83% | 29.13% |

| 5 | New York | 18.75% | 9.83% | 28.59% |

| 6 | Kansas | 16.68% | 9.83% | 26.51% |

| 7 | Utah | 16.64% | 9.83% | 26.47% |

| 8 | Pennsylvania | 16.48% | 9.83% | 26.31% |

| 9 | Rhode Island | 15.39% | 9.83% | 25.22% |

| 10 | North Dakota | 15.26% | 9.83% | 25.09% |

| 11 | Maryland | 14.95% | 9.83% | 24.78% |

| 12 | Missouri | 14.91% | 9.83% | 24.74% |

| 13 | Florida | 14.89% | 9.83% | 24.72% |

| 14 | Oklahoma | 14.56% | 9.83% | 24.39% |

| 15 | South Dakota | 14.39% | 9.83% | 24.22% |

| 16 | Alaska | 14.32% | 9.83% | 24.16% |

| 17 | Puerto Rico | 13.73% | 9.83% | 23.56% |

| 18 | California | 13.39% | 9.83% | 23.22% |

| 19 | Tennessee | 12.65% | 9.83% | 22.48% |

| 20 | Arizona | 12.64% | 9.83% | 22.47% |

| 21 | South Carolina | 12.63% | 9.83% | 22.47% |

| 22 | New Mexico | 12.13% | 9.83% | 21.97% |

| 23 | Georgia | 12.09% | 9.83% | 21.92% |

| 24 | District of Columbia | 12.06% | 9.83% | 21.89% |

| 25 | Colorado | 11.98% | 9.83% | 21.81% |

| 26 | Indiana | 11.96% | 9.83% | 21.79% |

| 27 | Texas | 11.84% | 9.83% | 21.68% |

| 28 | Alabama | 11.05% | 9.83% | 20.88% |

| 29 | Kentucky | 10.97% | 9.83% | 20.80% |

| 30 | Minnesota | 10.72% | 9.83% | 20.55% |

| 31 | West Virginia | 10.42% | 9.83% | 20.25% |

| 32 | Massachusetts | 10.32% | 9.83% | 20.15% |

| 33 | Michigan | 10.18% | 9.83% | 20.01% |

| 34 | Mississippi | 9.85% | 9.83% | 19.68% |

| 35 | Louisiana | 9.80% | 9.83% | 19.63% |

| 36 | Iowa | 9.79% | 9.83% | 19.63% |

| 37 | New Jersey | 9.07% | 9.83% | 18.90% |

| 38 | New Hampshire | 9.03% | 9.83% | 18.87% |

| 39 | North Carolina | 8.98% | 9.83% | 18.81% |

| 40 | Vermont | 8.90% | 9.83% | 18.73% |

| 41 | Maine | 8.71% | 9.83% | 18.54% |

| 42 | Ohio | 8.52% | 9.83% | 18.35% |

| 43 | Wyoming | 8.47% | 9.83% | 18.30% |

| 44 | Connecticut | 7.92% | 9.83% | 17.76% |

| 45 | Hawaii | 7.83% | 9.83% | 17.66% |

| 46 | Wisconsin | 7.72% | 9.83% | 17.55% |

| 47 | Virginia | 7.03% | 9.83% | 16.87% |

| 48 | Montana | 6.73% | 9.83% | 16.57% |

| 49 | Delaware | 6.68% | 9.83% | 16.51% |

| 50 | Nevada | 3.46% | 9.83% | 13.29% |

| 51 | Oregon | 2.98% | 9.83% | 12.82% |

| 52 | Idaho | 2.71% | 9.83% | 12.54% |

| Weighted Avg. | 12.82% | 9.83% | 22.65% | |

| Simple Avg. | 11.81% | 9.83% | 21.64% | |

| Source: Methodology from COST, “50-State Study and Report on Telecommunications Taxation,” May 2005. Updated July 2020 using state statutes, FCC data, and local ordinances. | ||||

Figure 2 shows the states by average state-local rates, without including the FUSF imposition. Other than the cluster of low-tax states in the western United States, there does not appear to be any strong regional patterns to the distribution of high-tax and low-tax states. The New England states tend to have lower wireless tax rates, while the high-tax states are scattered throughout the country.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeOne of the longstanding arguments for reform of wireless taxation is the disparity in tax burdens on wireless as compared to broad-based consumption taxes imposed on other goods and taxable services subject to sales and use taxes. Wireless and other telecommunications services are one of the few services that are consistently subject to sales and use taxes by states with both narrow and broad sales tax bases. Furthermore, states like Delaware, Montana, and New Hampshire that do not impose a general sales tax have specific taxes on wireless and other communications services.

Table 3 ranks the states by comparing the disparity between the tax rates imposed on wireless service to the combined state and local sales tax rate in each state. Illinois leads all states in this regard, imposing wireless taxes that are more than twice as high as sales taxes—22.1 percent versus 10.0 percent. Other states with large disparities include Nebraska, Alaska, Arkansas, New York, and Washington. New Hampshire, Delaware, and Montana—all states that do not have general sales taxes but impose taxes on wireless service—rank relatively high on the disparity index even though their overall wireless tax rates are relatively low by national standards. Table 3 also shows that two states—Idaho and Nevada—impose lower taxes on wireless service than on other goods and services subject to the general sales tax.

Total Taxes Paid

Wireless consumers pay about $11.9 billion in taxes and fees that are specifically levied on telecommunications services but not on other taxable goods and services. This total includes approximately $6.3 billion in FUSF surcharges, $3.5 billion in 911 fees, and another $2.1 billion in other discriminatory state and local taxes, fees, and government surcharges. The remaining $5.6 billion in taxes on wireless service are non-discriminatory sales and use taxes that are imposed on other taxable goods and services.[3]

| State-Local Sales Tax Rate | State-Local Wireless Tax Rate | Wireless Over/Under Sales Tax Rate | Disparity Multiple | |

|---|---|---|---|---|

| Illinois | 10.00% | 22.37% | 12.37% | 2.24 |

| Nebraska | 7.13% | 19.30% | 12.17% | 2.71 |

| Alaska | 2.50% | 14.32% | 11.82% | 5.73 |

| Arkansas | 9.50% | 20.21% | 10.71% | 2.13 |

| New York | 8.44% | 18.75% | 10.31% | 2.22 |

| Washington | 9.75% | 19.83% | 10.08% | 2.03 |

| Pennsylvania | 7.00% | 16.48% | 9.48% | 2.35 |

| Utah | 7.50% | 16.64% | 9.14% | 2.22 |

| New Hampshire | 0.00% | 9.03% | 9.03% | NA |

| Maryland | 6.00% | 14.95% | 8.95% | 2.49 |

| Rhode Island | 7.00% | 15.39% | 8.39% | 2.20 |

| Kansas | 8.33% | 16.68% | 8.35% | 2.00 |

| North Dakota | 7.25% | 15.26% | 8.01% | 2.10 |

| South Dakota | 6.50% | 14.39% | 7.89% | 2.21 |

| Florida | 7.25% | 14.89% | 7.64% | 2.05 |

| Montana | 0.00% | 6.73% | 6.73% | NA |

| Delaware | 0.00% | 6.68% | 6.68% | NA |

| Missouri | 8.41% | 14.91% | 6.50% | 1.77 |

| District of Columbia | 6.00% | 12.06% | 6.06% | 2.01 |

| Oklahoma | 8.57% | 14.56% | 5.99% | 1.70 |

| Kentucky | 6.00% | 10.97% | 4.97% | 1.83 |

| Indiana | 7.00% | 11.96% | 4.96% | 1.71 |

| California | 9.13% | 13.39% | 4.27% | 1.47 |

| Michigan | 6.00% | 10.18% | 4.18% | 1.70 |

| South Carolina | 8.50% | 12.63% | 4.13% | 1.49 |

| Massachusetts | 6.25% | 10.32% | 4.07% | 1.65 |

| Arizona | 8.65% | 12.64% | 3.99% | 1.46 |

| New Mexico | 8.16% | 12.13% | 3.97% | 1.49 |

| Hawaii | 4.00% | 7.83% | 3.83% | 1.96 |

| Colorado | 8.28% | 11.98% | 3.70% | 1.45 |

| Georgia | 8.45% | 12.09% | 3.64% | 1.43 |

| Texas | 8.25% | 11.84% | 3.59% | 1.44 |

| West Virginia | 7.00% | 10.42% | 3.42% | 1.49 |

| Maine | 5.50% | 8.71% | 3.21% | 1.58 |

| Tennessee | 9.50% | 12.65% | 3.15% | 1.33 |

| Oregon | 0.00% | 2.98% | 2.98% | NA |

| Wyoming | 5.50% | 8.47% | 2.97% | 1.54 |

| Iowa | 7.00% | 9.79% | 2.79% | 1.40 |

| Minnesota | 7.96% | 10.72% | 2.76% | 1.35 |

| New Jersey | 6.63% | 9.07% | 2.44% | 1.37 |

| Vermont | 6.50% | 8.90% | 2.40% | 1.37 |

| Mississippi | 7.50% | 9.85% | 2.35% | 1.31 |

| Puerto Rico | 11.50% | 13.73% | 2.23% | 1.19 |

| Wisconsin | 5.50% | 7.72% | 2.22% | 1.40 |

| North Carolina | 7.25% | 8.98% | 1.73% | 1.24 |

| Connecticut | 6.35% | 7.92% | 1.57% | 1.25 |

| Virginia | 5.65% | 7.03% | 1.38% | 1.25 |

| Alabama | 10.00% | 11.05% | 1.05% | 1.10 |

| Ohio | 7.75% | 8.52% | 0.77% | 1.10 |

| Louisiana | 9.70% | 9.80% | 0.10% | 1.01 |

| Idaho | 6.00% | 2.71% | -3.29% | 0.45 |

| Nevada | 7.99% | 3.46% | -4.53% | 0.43 |

| US Weighted Average | 7.75% | 12.82% | 5.07% | 1.65 |

| Source: Methodology from COST, “50-State Study and Report on Telecommunications Taxation,” May 2005. Updated July 2020 using state statutes, FCC data, and local ordinances. | ||||

Appendix C provides a detailed breakdown of the specific taxes, fees, and government surcharges imposed in each state, including the respective rates of each. To facilitate interstate comparisons, local rates imposed in the most populated city and the capital city in each state are averaged into a single rate. In the case of taxes and fees that are imposed on a flat per-line basis—for example, $1.00 per month per line—the tax is converted from a flat amount to a percentage by dividing the flat amount by the industry average revenue per line of $36.86 per month. For a detailed description of the methodology in this report, please see Appendix A.

Trends in Wireless Taxes and Fees

911 Fees

Most states impose 911 fees to fund capital expenses associated with the 911 system, and in some states these fees fund operations as well. Wireless 911 fees vary greatly by state, from a low of zero in Missouri[4] to a high of $5.00 per line per month in the City of Chicago.

In 2020, Arkansas doubled the state 911 fee from $.65 per line per month to $1.30 per line per month. Oregon increased the 911 fee from $0.75 per line per month to $1.00 per line per month. Maine reduced the 911 fee from $0.45 per line per month to $0.35 per line per month.

Unfortunately, according to the Federal Communications Commission (FCC), some states and localities routinely divert 911 fees for other purposes.[5] For example, the City of Chicago used the authority granted by the legislature to increase its monthly 911 fee from $3.90 per line to $5.00 per line, effective January 1, 2018. Media reports suggested that the 911 fee increase was intended to cover a shortfall in city pension obligations.[6] The FCC report identified other states that routinely divert 911 fees paid by wireless consumers to other purposes: Nevada, New Jersey, New York, Rhode Island, and West Virginia.

State Universal Service Funds

Some states have their own universal service funds (USF) that provide subsidies for many of the same purposes as the FUSF. State USF surcharges are imposed on intrastate revenues, while the FUSF is imposed on interstate revenues. In states like Arkansas, Alaska, Kansas, Nebraska, and California, high state USF surcharge rates add significantly to the overall burden on wireless consumers. For example, the USF rate in Arkansas is 11.25 percent of all intrastate charges. Table B1 in Appendix B lists the rates in the 20 states that impose a state USF charge.

In 2020, state USF rates were increased in Arkansas, Kansas, Michigan, and South Carolina and were reduced in Nevada, New Mexico, and Wyoming.

State-Level Wireless Taxes

In addition to 911 fees and state USF charges, 14 states impose taxes on wireless service that are either in addition to state sales taxes or in lieu of sales taxes but imposed at a higher rate than the state sales tax. Table 4 lists these states. No states increased or decreased these discriminatory state wireless taxes in 2020.

| State Gross Receipts Tax in Addition to Sales Tax | Higher State Tax Rate in Lieu of Sales Tax | Wireless Tax but No State Sales Tax |

|---|---|---|

| Indiana | District of Columbia | Delaware |

| Kentucky | Florida | Montana |

| New York | Illinois | New Hampshire |

| North Dakota | Maine | |

| Pennsylvania | ||

| Rhode Island | ||

| South Dakota | ||

| Source:State Statutes | ||

Local Wireless Taxes

Many local governments also impose discriminatory taxes on wireless consumers. Many of these are legacy taxes and fees that were established during the regulated telephone monopoly era that existed prior to the late 1980s. Local governments in some states have longstanding authority to impose “right-of-way” (ROW) fees on telephone companies for placing poles, wires, and other landline infrastructure on public property. In other states, localities have the authority to impose franchise or license fees on telephone companies in exchange for an exclusive franchise agreement to provide service within the municipality.

In the late 1990s and early 2000s, when wireless service began to displace landline service, localities became concerned about losing taxes and fees from landline telephone services and sought to extend these taxes and fees to wireless services. This occurred even though wireless providers typically did not use the public right-of-way to place equipment or, when they did use public property like buildings, the usage was de minimis and paid for through negotiated rental agreements.

Local governments in 13 states currently impose some type of tax or fee on wireless service over and above any broad-based local sales tax. In most of these states, the local wireless tax is in addition to state taxes. California is the exception—wireless service is not subject to sales taxes but is subject to local Utility User Taxes (UUT) at rates as high as 11 percent. Table 5 provides a breakdown of the types of local wireless taxes.

| Privilege, License, or User Taxes | State-Authorized Telecom Taxes | School District and Other Special District Taxes |

|---|---|---|

| Arizona | Florida | Kentucky |

| California | Illinois | New York |

| Maryland | Maryland | |

| Missouri | New York | |

| Nebraska | Utah | |

| Nevada | ||

| South Carolina | ||

| Washington | ||

|

Note: Excludes local general sales taxes. Source: State statutes. |

||

Local government taxes have a significant impact on the overall tax burden on wireless consumers in many of the states that rank high in the overall wireless tax and fee burden. In most of the top 10 states shown in Table 2 with the highest wireless taxes, local taxes play a prominent role. Nebraska allows local business license taxes with rates as high as 6.25 percent. Washington allows municipal governments to impose “utility franchise taxes” with rates as high as 9 percent. New York allows New York City, other selected cities, school districts, and certain transit districts to levy various wireless taxes in addition to county 911 fees. Finally, Florida and Illinois have special state communications taxes with a local add-on that result in rates typically two times higher than the general sales tax rates.

Table 6 illustrates the impact of taxes and fees on consumers in selected large cities around the country. Wireless service is increasingly becoming the sole means of communication and connectivity for many Americans, particularly those struggling to overcome poverty. As noted previously, at the end of 2019, more than 67 percent of all low-income adults had wireless-only service, and 58 percent of all adults were wireless-only. Excessive local taxes and fees, especially the very high per line charges like those imposed in Chicago and Baltimore, impose a disproportionate burden on low-income consumers. In Chicago, the taxes on a family with four lines of taxable wireless service paying $100 per month are more than $500 per year—about 43 percent of their monthly bill.

| City | Tax on 4-line voice plan at $100 per month | Effective Tax Rate |

|---|---|---|

| Chicago, IL | $43.83 | 43.83% |

| Baltimore, MD | $37.03 | 37.03% |

| Omaha, NE | $32.00 | 32.00% |

| Little Rock, AR | $31.27 | 31.27% |

| New York, NY | $30.30 | 30.30% |

| Seattle, WA | $29.73 | 29.73% |

| Philadelphia, PA | $29.43 | 29.43% |

| Salt Lake City, UT | $29.40 | 29.40% |

| Providence, RI | $26.83 | 26.83% |

| Tallahassee, FL | $25.77 | 25.77% |

| City | Tax on Single Line Voice Plan Costing $36.86 per moth | Effective Tax Rate |

| Chicago, IL | $13.78 | 37.39% |

| Baltimore, MD | $11.13 | 30.21% |

| Little Rock, AR | $10.89 | 29.55% |

| Omaha, NE | $10.74 | 29.13% |

| Seattle, WA | $10.51 | 28.51% |

| New York, NY | $10.46 | 28.37% |

| Philadelphia, PA | $10.07 | 27.31% |

| Salt Lake City, UT | $9.85 | 26.72% |

| Tallahassee, FL | $9.31 | 25.26% |

| Providence, RI | $9.30 | 25.22% |

| Source: Author’s calculations, using state statutes and local ordinances. | ||

The Impact of Excessive Wireless Taxes

The popularity of wireless service, and the explosive growth in the number of wireless subscribers, has led some to question whether wireless taxes matter to wireless consumers and the wireless industry. However, there are two compelling reasons why policymakers should be cautious about expanding wireless taxes, fees, and surcharges. First, as discussed above, wireless taxes and fees are regressive and have a disproportionate impact on low-income citizens. Excessive taxes and fees increase the cost of access to wireless service for low-income consumers at a time when citizens are relying on wireless service for education and remote work during the coronavirus pandemic. Second, discriminatory taxes may slow investment in wireless infrastructure. Ample evidence exists that investments in wireless networks provide economic benefits to the broader economy because so many sectors—transportation, health care, energy, education, even government—use wireless networks to boost productivity and efficiency. These economic benefits are especially important during the current pandemic because they help employees work remotely and allow students to continue their studies remotely.

Network investment is important not only to consumers and businesses that use these networks but also to the entire American economy. A report by the International Chamber of Commerce (ICC) in Paris surveyed the evidence not only from the United States and Europe but from the developing world as well.[7] Economists that have examined the link between investments in communications and information technology infrastructure and economic growth have consistently found a strong link. Simply put, wireless infrastructure investment enables an entire entrepreneurial culture to focus on creating applications and devices to make businesses more productive and to improve the lives of consumers. These tools in turn make businesses more productive and profitable so that they can create new jobs that generate economic activity and tax revenues for governments.

While most infrastructure investments create these types of multiplier effects, the multiplier effects for telecommunications infrastructure are higher than other industries because communications and information technology are so deeply embedded in business processes. These infrastructure investments also benefit the government and nonprofit sectors in ways that do not necessarily show up directly in economic statistics, but nonetheless make these sectors more efficient and enable them to lower the cost of providing government services.

As noted in the ICC report, “Remedying the discriminatory tax treatment of telecom goods and services may reduce tax receipts in the short-term, but the longer-term increase in the use of advanced capability devices, service demand, and network deployment resulting from these tax reductions is likely to counteract this loss of revenue over time.”[8] Policymakers need to weigh the trade-offs between the short-term revenue benefits of excessive wireless taxes versus the long-term economic impact on the state from reduced infrastructure investment.

Conclusion

Wireless consumers continue to be burdened with high taxes, fees, and surcharges in many states and localities across the United States. While state and local government taxes and fees were relatively stable between 2019 and 2020, significant increases in the FUSF over the last two years have pushed taxes on wireless service to record-high levels. Excessive taxes on wireless consumers disproportionately impact low-income families and may have ramifications for long-term state economic development and growth. Higher taxes on wireless service, coupled with increased taxes on wireless investments, may lead to slower deployment of wireless network infrastructure, including fifth generation (5G) wireless broadband technologies.

States should study their existing communications tax structure and consider policies that transition their tax systems away from narrowly-based wireless taxes and toward broad-based tax sources that do not distort consumer purchasing decisions and do not slow investment in critical infrastructure like wireless broadband.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAppendix A

Methodology

The methodology used in this report to calculate wireless taxes compares the applicable federal, state, and local rates on wireless voice service in the capital city and the most populated city in each state. This methodology was developed by the Committee on State Taxation (COST) in its landmark “50-State Study and Report on Telecommunications Taxation,” first published in 2000.

The use of a consistent methodology allows for accurate time-series comparisons across states and over time. However, changes in consumer demand for wireless services pose challenges when measuring the impact of wireless taxes on consumer bills. Two trends in the industry are significantly impacting the amount of taxes that wireless consumers pay on their monthly bills.

First, a growing share of wireless consumer purchases is for internet access. U.S. Census Bureau data from 2018 suggests that about 49.7 percent of total wireless service revenues (which excludes sales and rental of equipment and other non-service operating revenue) for the industry as a whole are from the sale of internet access.[9] This percentage continues to grow as wireless consumers utilize more internet access and less voice telephone service each year.

Under federal law, as of July 1, 2020, all states are precluded from imposing taxes on internet access. This suggests that of the “typical” consumer’s monthly expenditure of $36.86 per month, approximately $18.32 is for non-taxable internet access and $18.54 is for taxable wireless service. A consumer applying the tax rates in this report to their total bill will find that the effective tax rate overstates their actual tax paid if their calling plan includes both taxable voice service and exempt internet access.

Second, the report’s methodology understates the tax rate impact of flat rate taxes and fees—those that are imposed as a set dollar amount per line. Under the report’s methodology, a $1.00 per month per line tax is converted to a percentage amount by dividing $1.00 by the $36.86 average monthly bill, resulting in a tax rate of 2.7 percent in this example. However, these flat rate taxes and fees are only permitted to be imposed on the portion of the wireless bill that is not internet access. In this same example, if the $1.00 per month were divided by the taxable portion of the bill ($18.54), the tax rate would be 5.4 percent.

Notwithstanding these methodological challenges, the authors have determined that the benefits of retaining the current methodology—consistent measurement of trends in tax rates over time—outweigh the benefits of changing the methodology to adjust to recent trends. This is particularly true since the Census Bureau has only been tracking the percentage of wireless expenditures on internet access since 2012, so it would not be possible to go back and retroactively adjust data prior to 2012.

Appendix B

What Are Universal Service Funds?

The Federal Universal Service Fund

The Federal Universal Service Fund (FUSF) is administered by the FCC under open-ended authority from Congress. The program subsidizes telecommunications services for schools, libraries, hospitals, low-income people, and rural telephone companies operating in high-cost areas. The FCC has also recently decided to use funds to subsidize broadband deployment.

The FCC has authority to set spending for these programs outside of the normal congressional appropriations process. After deciding what to spend on the various programs, the FCC sets the quarterly “contribution factor” or surcharge rate that telecommunications providers must remit to the FUSF to generate sufficient revenues to fund the expenditure commitments. Providers may elect to surcharge these “contributions” on their customer bills.

FUSF surcharges apply only to revenues from interstate telecommunications services. They currently do not apply to internet access service, information services, and intrastate telecommunications services.

Wireless carriers generally sell plans that include either unlimited voice minutes or a fixed number of voice minutes for a set amount. Since these plans include both interstate calls (subject to the FUSF) and intrastate calls (not subject to FUSF), the FCC allows providers to allocate the fixed monthly plans to interstate and intrastate calls by one of two methods. Carriers may use “traffic studies” to show the actual split between interstate and interstate calls for all subscribers and apply the FUSF to the aggregated interstate portion of subscriber calls.

Alternatively, carriers may use a single uniform national “safe harbor” percentage to its fixed monthly plans. The FCC currently sets this safe harbor at 37.1 percent of the fixed monthly charge. For example, when determining the FUSF, a $50 monthly wireless voice calling plan is deemed to include $18.55 in interstate calls and $31.45 in intrastate calls. If a carrier elects to use the safe harbor, the FUSF rate would be applied to $18.55 of the bill each month.

The FUSF rate is set by the FCC each quarter. For the period beginning July 1, 2020, the rate is 26.5 percent. Thus, the FUSF rate applied on assessable wireless revenues using the FCC safe harbor amount is 9.83 percent (26.5 percent times 37.1 percent).[10] Figure B1 highlights the significant growth in the FCC contribution rate since 2003.

Figure B1

Despite the growing burden on wireless consumers, Congress has shown little interest in restricting or otherwise limiting the growth of the programs funded through the FSUF.

State Universal Service Funds

States also have the authority to supplement the programs funded through the FUSF with their own programs funded through state universal service funds. The state programs are funded by surcharges applied to the intrastate portion of telephone charges. In this report, the inverse of the FUSF safe harbor is used to calculate the rates of the state USF in all states except Vermont, which imposes its state USF on both interstate and intrastate charges. As in the previous example, if a consumer has a $50 monthly wireless voice plan, 62.9 percent of that charge ($31.45) is deemed to be an intrastate service subject to the state USF charge and $18.55 is an interstate service not subject to state USF charges.

Like the FUSF, state universal service fund charges do not apply to internet access. State USF charges are a key factor in the high wireless tax burden in states like Arkansas, Alaska, Kansas, Nebraska, and California.

| State | Effective Rate | Calculation |

|---|---|---|

| Arkansas | 7.08% | 11.25% times FCC safe harbor |

| Alaska | 6.29% | 10.0% times FCC Intrastate safe harbor |

| Kansas | 5.91% | 9.4% x FCC safe harbor |

| Nebraska | 4.75% | $1.75 per line per month |

| California | 4.37% | 7.28% times FCC Intrastate safe harbor |

| Oklahoma | 3.95% | 6.28% times FCC safe harbor |

| Louisiana | 3.50% | Carrier rates assigned by Public Service Commission |

| Vermont | 2.40% | Funds 911 and other programs |

| New Mexico | 2.39% | $0.88 per line per month |

| Texas | 2.08% | 3.3% times FCC safe harbor |

| Colorado | 1.64% | 2.6% times FCC safe harbor |

| Utah | 1.63% | $0.60 per line per month |

| South Carolina | 1.37% | 2.18% times FCC safe harbor |

| Maine | 1.19% | $0.44 per line |

| Puerto Rico | 0.87% | 1.39% times FCC safe harbor |

| Wyoming | 0.69% | 1.1% times FCC safe harbor |

| Indiana | 0.69% | 1.09% times FCC safe harbor |

| Kentucky | 0.19% | $.07 per month |

| Wisconsin | 0.18% | 0.29% times FCC safe harbor |

| Maryland | 0.14% | $0.05 per month per line |

| Nevada | 0.11% | 0.17% times FCC Safe Harbor |

| Source: Author’s calculation from state statutes and state utility commisions. | ||

Appendix C

| State | Type of Tax | Rate | Comments |

|---|---|---|---|

| Alabama | |||

| AL Cell Service Tax | 6.00% | Access, interstate, and intrastate | |

| E911 | 5.05% | $1.86 per month | |

| TOTAL TRANSACTION TAX | 11.05% | ||

| Alaska | |||

| Local Sales Tax | 2.50% | Avg. of Juneau (5%) and Anchorage (0%) | |

| Local E911 | 5.29% | Anchorage: $2.00 and Juneau: $1.90 | |

| State USF | 6.29% | 10.0% times FCC safe harbor | |

| TRS fee | 0.24% | $0.09 per line | |

| TOTAL TRANSACTION TAX | 14.32% | ||

| Arizona | |||

| State sales (transaction priv.) | 5.60% | Intrastate telecommunications service | |

| County sales (transaction priv.) | 0.60% | Avg. of Phoenix (Maricopa) (0.7%) and Tucson (Pima) (0.5%) | |

| City telecommunications | 5.90% | Avg. Phoenix (4.7%) and Tucson (7.1%) | |

| 911 | 0.54% | $0.20 per month | |

| TOTAL TRANSACTION TAX | 12.64% | ||

| Arkansas | |||

| State sales tax | 6.50% | ||

| Local sales taxes | 3.00% | Avg. Little Rock (2.5%) and Fayetteville (3.5%) | |

| State High Cost Fund | 7.08% | 11.25% times FCC safe harbor | |

| Wireless 911 | 3.53% | $1.30 per month statewide. | |

| TRS service & TRS equipment | 0.11% | $0.04 per line per month | |

| TOTAL TRANSACTION TAX | 20.21% | ||

| California | |||

| Local Utility User Tax | 8.00% | Avg. of LA (9%) and Sacramento (7%) | |

| State 911 | 0.81% | $0.30 per line per month | |

| PUC fee | 0.21% | 0.34% times FCC safe harbor | |

| ULTS (lifeline) | 2.99% | 4.75% times FCC safe harbor | |

| Deaf/CRS | 0.31% | 0.5% times FCC safe harbor | |

| High Cost Funds A & B | 0.22% | 0.35% times FCC safe harbor | |

| Teleconnect Fund | 0.49% | 0.78% times FCC safe harbor | |

| CASF – advanced services fund | 0.35% | 0.56% times FCC safe harbor | |

| TOTAL TRANSACTION TAX | 13.39% | ||

| Colorado | |||

| State Sales Tax | 2.90% | Access and intrastate | |

| Local Sales Tax — City/County | 3.82% | Avg. of Denver (5.41%) and Colorado Springs (2.23%) | |

| 911 | 3.46% | Denver: $1.20 and Colorado Springs: $1.35 | |

| USF | 1.64% | 2.6% times FCC safe harbor | |

| TDD Tax | 0.16% | $0.06 per month | |

| TOTAL TRANSACTION TAX | 11.98% | ||

| Connecticut | |||

| State sales tax | 6.35% | Access, interstate, and intrastate | |

| 911 | 1.57% | $0.58 per line | |

| TOTAL TRANSACTION TAX | 7.92% | ||

| Delaware | |||

| Public Utility Gross Receipts Tax | 5.00% | Access and intrastate | |

| Local 911 tax | 1.63% | $0.60 per month | |

| TRS fee | 0.05% | $0.02 per line per month | |

| TOTAL TRANSACTION TAX | 6.68% | ||

| District of Columbia | |||

| Telecommunication Privilege Tax | 10.00% | Monthly gross charge; | |

| 911 | 2.06% | $0.76 per month | |

| TOTAL TRANSACTION TAX | 12.06% | ||

| Florida | |||

| State Communications services | 7.44% | Access, interstate, and intrastate | |

| Local Communications services | 6.36% | Jacksonville (5.82%) and Tallahassee (6.9%) | |

| 911 | 1.09% | $0.40 per month statewide | |

| TOTAL TRANSACTION TAX | 14.89% | ||

| Georgia | |||

| State sales tax | 3.80% | 4% of “access charge” — assume $35 | |

| Local sales tax | 4.23% | Avg. rate Atlanta (4.9%) and Augusta (4%) | |

| Local 911 | 4.07% | $1.50 per line statewide | |

| TOTAL TRANSACTION TAX | 12.09% | ||

| Hawaii | |||

| Public service company tax | 4.00% | ||

| Additional county tax | 1.89% | ||

| PUC Fee | 0.16% | 0.25% of intrastate charges | |

| Wireless 911 fee | 1.79% | $0.66 per month | |

| TOTAL TRANSACTION TAX | 7.83% | ||

| Idaho | |||

| Telephone service assistance program | 0.00% | Set annually by PUC (currently zero) | |

| Statewide wireless 911 | 2.71% | Boise: $1.00 per month | |

| TOTAL TRANSACTION TAX | 2.71% | ||

| Illinois | |||

| State telecom excise tax | 7.00% | Access, interstate, and intrastate | |

| Simplified municipal tax | 6.50% | Avg. of Chicago (7%) and Springfield (6%) | |

| Wireless 911 | 8.82% | Chicago: $5 per month and others: $1.50 per month | |

| TRS fee | 0.05% | $0.02 per line per month | |

| TOTAL TRANSACTION TAX | 22.37% | ||

| Indiana | |||

| State sales tax | 7.00% | Access and intrastate | |

| Utility receipts tax | 1.40% | Same base as sales tax | |

| Wireless 911 | 2.71% | $1.00 per month | |

| State USF | 0.69% | 1.09% times FCC safe harbor | |

| PUC fee | 0.08% | 0.13% times FCC safe harbor | |

| TRS fee | 0.08% | $0.03 per line per month | |

| TOTAL TRANSACTION TAX | 11.96% | ||

| Iowa | |||

| State sales tax | 6.00% | ||

| Local option sales taxes | 1.00% | Avg. of Cedar Rapids (1%) and Des Moines (1%) | |

| Wireless 911 | 2.71% | $1.00 per month | |

| Dual Party Relay Service fee | 0.08% | $0.03 per month | |

| TOTAL TRANSACTION TAX | 9.79% | ||

| Kansas | |||

| State sales tax | 6.50% | Intrastate and interstate | |

| Local option sales taxes | 1.83% | Avg. of Wichita (1.0%) and Topeka (2.65%) | |

| USF | 5.91% | 9.4% times FCC safe harbor | |

| Wireless 911 | 2.44% | $0.90 per month per line | |

| TOTAL TRANSACTION TAX | 16.68% | ||

| Kentucky | |||

| State sales tax | 6.00% | Access, interstate, and intrastate | |

| School utility gross receipts | 1.50% | Avg. of Frankfort (3%) and Lousiville (0%) | |

| Kentucky USF | 0.19% | $0.07 per month | |

| Kentucky TAP & TRS | 0.08% | TAP: $0.02 and TRS: $0.01 | |

| Wireless 911 | 1.90% | $0.70 per month | |

| Communications gross receipts tax | 1.30% | Access, interstate, and intrastate | |

| TOTAL TRANSACTION TAX | 10.97% | ||

| Louisiana | |||

| State sales tax | 3.45% | Intrastate rate | |

| Wireless 911 | 2.85% | New Orleans: $1.25 per month and Baton Rouge: $0.85 per month | |

| State USF | 3.50% | May vary by carrier | |

| TRS fee | 0.14% | $0.05 per line per month | |

| TOTAL TRANSACTION TAX | 9.80% | ||

| Maine | |||

| State service provider tax | 6.00% | ||

| 911 fee | 0.95% | $0.35 per month | |

| Maine USF | 1.19% | $0.44 per line | |

| MTEAF | 0.57% | $0.21 per line per month | |

| TOTAL TRANSACTION TAX | 8.71% | ||

| Maryland | |||

| State sales tax | 6.00% | ||

| Local telecom excise | 5.43% | Baltimore: $4.00 per month and Annapolis: $0.00 | |

| State 911 | 1.36% | $0.50 per month per line | |

| County 911 | 2.03% | Currently $0.75 per month in all counties | |

| State USF | 0.14% | $0.05 per account | |

| TOTAL TRANSACTION TAX | 14.95% | ||

| Massachusetts | |||

| State sales tax | 6.25% | Interstate and intrastate | |

| Wireless 911 | 4.07% | $1.50 per month | |

| TOTAL TRANSACTION TAX | 10.32% | ||

| Michigan | |||

| State sales tax | 6.00% | Interstate and intrastate | |

| State wireless 911 | 0.68% | $0.25 per month | |

| County wireless 911 | 3.01% | Detroit: $0.42 and Lansing: $1.80 | |

| Intrastate toll assessment | 0.49% | 0.78% of intrastate charges | |

| TOTAL TRANSACTION TAX | 10.18% | ||

| Minnesota | |||

| State sales tax | 6.88% | Interstate and intrastate | |

| Local sales tax | 1.08% | Avg. of Minneapolis (1.15%) and St. Paul (1.0%) | |

| 911 | 2.58% | $0.95 per month | |

| Telecom access MN fund | 0.19% | $0.07 per line per month | |

| TOTAL TRANSACTION TAX | 10.72% | ||

| Mississippi | |||

| State sales tax | 7.00% | Access, interstate, and intrastate | |

| Wireless 911 & 911 training fee | 2.85% | $1.05 per month per line | |

| TOTAL TRANSACTION TAX | 9.85% | ||

| Missouri | |||

| State sales tax | 4.23% | Access and intrastate | |

| Local sales taxes | 4.19% | Avg. Jefferson City (3.5%) and Kansas City (4.875%) | |

| Local business license tax | 6.50% | Avg. of Jefferson City (7%) and Kansas City (6% residential) | |

| TOTAL TRANSACTION TAX | 14.91% | ||

| Montana | |||

| Telecom excise tax | 3.75% | Access, interstate, and intrastate | |

| 911 & E911 tax | 2.71% | $1.00 per number per month | |

| TDD tax | 0.27% | $0.10 per number per month | |

| TOTAL TRANSACTION TAX | 6.73% | ||

| Nebraska | |||

| State sales tax | 5.50% | Access and intrastate | |

| Local sales tax | 1.63% | Avg. of Lincoln (1.75%) and Omaha (1.5%) | |

| City business and occupation tax | 6.13% | Avg. of Omaha (6.25%) and Lincoln (6.0%) | |

| State USF | 4.75% | $1.75 per line per month | |

| Wireless 911 | 1.22% | $0.45 per month | |

| TRS | 0.08% | $0.03 per month | |

| TOTAL TRANSACTION TAX | 19.30% | ||

| Nevada | |||

| Local franchise / gross receipts | 2.03% | 5% of first $15 intrastate revenues | |

| Local 911 tax | 1.15% | Washoe County: $0.85 per month and Clark County: $0.00 | |

| State deaf relay charge | 0.16% | $0.06 per access line | |

| Nevada USF | 0.11% | 0.17% times FCC Safe Harbor | |

| TOTAL TRANSACTION TAX | 3.46% | ||

| New Hampshire | |||

| Communication services tax | 7.00% | Access, interstate, and intrastate | |

| 911 tax | 2.03% | $0.75 per month | |

| TOTAL TRANSACTION TAX | 9.03% | ||

| New Jersey | |||

| State sales tax | 6.63% | ||

| Wireless 911 | 2.44% | $0.90 per month | |

| TOTAL TRANSACTION TAX | 9.07% | ||

| New Mexico | |||

| State gross receipts (sales) tax | 5.13% | Intrastate: 5.125% and interstate: 4.25% | |

| City and county gross receipts tax | 3.03% | Avg. Santa Fe (3.3125%) and Albuquerque (2.75%) | |

| Wireless 911 | 1.38% | $0.51 per month | |

| TRS surcharge | 0.21% | 0.33% times FCC safe harbor | |

| State USF | 2.39% | $0.88 per line per month | |

| TOTAL TRANSACTION TAX | 12.13% | ||

| New York | |||

| State sales tax | 4.00% | Intrastate and monthly access | |

| Local sales taxes | 4.25% | Avg. of NYC (4.5%) and Albany (4%) | |

| MCTD sales tax | 0.19% | Avg. of NYC (0.375%); and Albany (0%) | |

| State excise tax (186e) | 2.90% | Mobile telecom service — includes interstate | |

| MCTD excise/surcharge (186c) | 0.36% | NYC & surrounding counties: Avg. of 0.72% and Albany 0% | |

| Local utility gross receipts tax | 1.49% | Avg of. NYC (84% of 2.35%) and Albany (1%) | |

| State wireless 911 | 3.26% | $1.20 per month | |

| Local wireless 911 | 0.81% | $0.30 per month — NYC & most counties | |

| School district utility sales tax | 1.50% | Albany: 3% and NYC: 0% | |

| TOTAL TRANSACTION TAX | 18.75% | ||

| North Carolina | |||

| State and loccal sales tax | 7.00% | Statewide combined rate includes local rates | |

| Wireless 911 | 1.76% | $0.65 per month | |

| TRS Charge | 0.22% | $0.08 per month | |

| TOTAL TRANSACTION TAX | 8.98% | ||

| North Dakota | |||

| State sales tax | 5.00% | Access and intrastate | |

| Local sales taxes | 2.25% | Avg Fargo (2.5%) and Bismarck (2.0%) | |

| State gross receipts tax | 2.50% | Interstate and intrastate | |

| Statewide Interoperable Radio Network Tax | 1.36% | $0.50 per line per month | |

| Local 911 tax | 4.07% | Bismarck: $1.50 and Fargo: $1.50 | |

| TRS | 0.08% | Up to $0.11 per month (currently $0.03) | |

| TOTAL TRANSACTION TAX | 15.26% | ||

| Ohio | |||

| State sales tax | 5.75% | Access, interstate, and intrastate | |

| Local sales taxes | 2.00% | Avg. of Columbus (1.75%) and Cleveland (2.25%) | |

| Regulatory fee | 0.09% | 0.139% of intrastate revenues | |

| State/local wireless 911 | 0.68% | $0.25 per month per phone number | |

| TOTAL TRANSACTION TAX | 8.52% | ||

| Oklahoma | |||

| State sales tax | 4.50% | Access, interstate, and intrastate | |

| Local sales taxes | 4.07% | Avg. of OK City (4.125%) and Tulsa (4.017%) | |

| Local 911 | 2.03% | $0.75 per month in OK City and Tulsa | |

| USF | 3.95% | 6.28% times FCC safe harbor | |

| TOTAL TRANSACTION TAX | 14.56% | ||

| Oregon | |||

| Local utililty tax | 0.00% | No tax on wireless in Portland or Salem | |

| 911 tax | 2.71% | $1.00 per month | |

| RSPF Surcharge | 0.27% | $0.10 per month | |

| TOTAL TRANSACTION TAX | 2.98% | ||

| Pennsylvania | |||

| State sales tax | 6.00% | Access, interstate, and intrastate | |

| State gross receipts tax | 5.00% | Access, interstate, and intrastate | |

| Local sales tax | 1.00% | Avg. of Philadephia (2%) and Harrisburg (0%) | |

| Statewide wireless 911 | 4.48% | $1.65 per month | |

| TOTAL TRANSACTION TAX | 16.48% | ||

| Puerto Rico | IVU (Sales Tax) | 11.50% | |

| 911 fee | 1.36% | $0.50 per line | |

| USF | 0.87% | 1.39% times FCC safe harbor | |

| TOTAL TRANSACTION TAX | 13.73% | ||

| Rhode Island | |||

| State sales tax | 7.00% | Access, interstate, and intrastate | |

| Gross receipts tax | 5.00% | Access, interstate, and intrastate | |

| 911 and first responder fee | 3.39% | $1.25 per month | |

| TOTAL TRANSACTION TAX | 15.39% | ||

| South Carolina | |||

| State sales tax | 6.00% | Access, interstate, and intrastate | |

| Local sales tax | 2.50% | Avg. of Charleston (3%) and Columbia (2%) | |

| Municipal license tax | 1.00% | Charleston (1.0%) and Columbia (1.0%) | |

| Dual party relay charge | 0.08% | $0.03 per line per month | |

| State USF | 1.37% | 2.18% times FCC safe harbor | |

| 911 tax | 1.68% | $0.62 / month | |

| TOTAL TRANSACTION TAX | 12.63% | ||

| South Dakota | |||

| State sales tax | 4.50% | Access, interstate, and intrastate | |

| State gross receipts tax | 4.00% | ||

| local option sales tax | 2.00% | Avg. of Pierre (2.0%) and Sioux Falls (2.0%) | |

| 911 excise | 3.39% | $1.25 per month | |

| TRS fee | 0.41% | $0.15 per month by statute | |

| PUC fee | 0.09% | 0.15% of intrastate receipts | |

| TOTAL TRANSACTION TAX | 14.39% | ||

| Tennessee | |||

| State sales tax | 7.00% | Access, interstate, and intrastate | |

| Local sales tax | 2.50% | Statewide local rate for intrastate | |

| 911 tax | 3.15% | $1.16 per month | |

| TOTAL TRANSACTION TAX | 12.65% | ||

| Texas | |||

| State sales tax | 6.25% | Access, interstate, and intrastate | |

| Local sales tax | 2.00% | Austin (2.0%) and Houston (2.0%) | |

| Wireless 911 tax | 1.36% | $0.50 per month per line | |

| Texas USF | 2.08% | 3.3% times FCC safe harbor | |

| 911 Equalization surcharge | 0.16% | $0.06 per line | |

| TOTAL TRANSACTION TAX | 11.84% | ||

| Utah | |||

| State sales tax | 4.85% | Access and intrastate | |

| Local sales taxes | 2.65% | Avg. of Salt Lake City (2.9%) and Provo (2.4%) | |

| Local utility wireless | 3.50% | Levied at 3.5% max. in SLC and Provo | |

| State 911 service charges | 2.60% | $0.96 per line per month | |

| State Radio Network charge | 1.41% | $0.52 per line per month | |

| State USF | 1.63% | $0.60 per line per month | |

| TOTAL TRANSACTION TAX | 16.64% | ||

| Vermont | |||

| State sales tax | 6.00% | Access, interstate, and intrastate | |

| Local sales tax | 0.50% | Avg. of Montpelier (0%) and Burlington (1%) | |

| State 911/USF | 2.40% | Funds 911 and other programs | |

| TOTAL TRANSACTION TAX | 8.90% | ||

| Virginia | |||

| State communications sales tax | 5.00% | ||

| Wireless 911 | 2.03% | $0.75 per month | |

| TOTAL TRANSACTION TAX | 7.03% | ||

| Washington | |||

| State sales tax | 6.50% | Access, interstate, and intrastate | |

| Local sales taxes | 3.25% | Avg. of Olympia (2.9%) and Seattle (3.6%) | |

| B&O / Utility Franchise — local | 7.50% | Avg. of Olympia (9%) and Seattle (6%) | |

| 911 — state | 0.68% | $0.25 per month | |

| 911 — local | 1.90% | $0.70 per month | |

| TOTAL TRANSACTION TAX | 19.83% | ||

| West Virginia | |||

| State sales tax | 0.00% | No sales tax on wireless | |

| Wireless 911 / public safety / tower fee | 10.42% | $3.84 per month | |

| TOTAL TRANSACTION TAX | 10.42% | ||

| Wisconsin | |||

| State sales tax | 5.00% | Access, intrastate, and interstate | |

| Local sales tax | 0.50% | Avg. of Milwaukee (0.5%) and Madison (0.5%) | |

| Police and Fire Protection Fee | 2.03% | $0.75 per month | |

| State USF | 0.18% | 0.29% times FCC safe harbor | |

| TOTAL TRANSACTION TAX | 7.72% | ||

| Wyoming | |||

| State sales tax | 4.00% | Access and intrastate | |

| Local sales tax | 1.50% | Avg. of Cheyenne (2%) and Casper (1%) | |

| TRS | 0.24% | Up to $0.25/month ($0.09 currently) | |

| USF | 0.69% | 1.1% times FCC safe harbor | |

| 911 tax | 2.03% | $0.75 per month in Cheyenne and Casper | |

| TOTAL TRANSACTION TAX | 8.47% | ||

| ARPU= 36.86 | |||

| FCC Safe Harbor = 62.9% | |||

| Sources & Methodology: Committee on State Taxation, 50-State Study and Report on Telecommunications Taxation, May 2005. Updated July 2020 by Scott Mackey, Leonine Public Affairs LLP, using state statutes and regulations. Average Monthly Revenue Per Unit (ARPU): $36.86 per Cellular Telephone and Internet Association, July 2020. | |||

[1] Whenever this paper refers to taxes as a percentage of the wireless services bill, it refers exclusively to the taxable portion of that bill. Internet access is not taxable according to federal law. More details in Appendix A. See House Judiciary Committee, “H. Rept. 113-510 – Permanent Internet Tax Freedom Act,” 2013-2014, July 3, 2014, https://www.congress.gov/congressional-report/113th-congress/house-report/510/1.

[2] Stephen J. Blumberg and Julian V. Luke, “Wireless Substitution: Early Release of Estimates from the National Health Interview Survey, January-June 2019,” National Center for Health Statistics, May 2020, 8,https://www.cdc.gov/nchs/data/nhis/earlyrelease/wireless202005-508.pdf.

[3] These estimates are calculated by applying the rates of percentage-based taxes in each state by the average monthly bill after excluding the estimated 49.4 percent of the average monthly bill representing internet access. For flat rate per line impositions, the per line rate is multiplied by the estimated number of postpaid wireless lines.

[4] Missouri enacted HB1456 in 2018 that authorizes certain cities and counties to impose wireless 911 fees on or after January 1, 2019 if approved by voters. As of this writing, no local jurisdictions had imposed a wireless 911 fee.

[5] Federal Communications Commission, “Eleventh Annual Report to Congress on State Collection and Distribution of 911 Fees and Enhanced 911 Fees and Charges for the Period January 1, 2018 to December 31, 2018,” Dec. 19, 2019, https://www.fcc.gov/files/11thannual911feereport2019pdf.

[6] Bill Ruthhart and Hal Dardick, “Emanuel’s Latest Possible Tax Hike: 911 Phone Fees,” Chicago Tribune, June 1, 2017, http://www.chicagotribune.com/news/local/politics/ct-rahm-emanuel-phone-fee-increase-met-0602-20170601-story.html.

[7] International Chamber of Commerce, “ICC Discussion Paper on the Adverse Effects of Discriminatory Taxes on Telecommunications Service,” Oct. 26, 2010. https://cdn.iccwbo.org/content/uploads/sites/3/2010/10/ICC-discussion-paper-on-the-adverse-effects-of-discriminatory-taxes-on-telecommunications-services.pdf.

[8] “International Chamber of Commerce, “ICC Discussion Paper on the Adverse Effects of Discriminatory Taxes on Telecommunications Service,” 2.

[9] U.S. Census Bureau, “Service Annual Survey Latest Data (NAICS-basis),” Nov. 26, 2019, https://www.census.gov/data/tables/2018/econ/services/sas-naics.html.

[10] For the purposes of this report, the FCC safe harbor percentage is used. This allows for consistent multiyear comparisons of taxes, fees, and surcharges.

Share this article