All Related Articles

How Controlled Foreign Corporation Rules Look Around the World: Spain

The CFC legislation in Spain is not as complicated as it is in some other countries, and it is aligned with the standards recommended by the OECD. The Spanish rules have evolved in a way that the rules are designed to comply with the EU principles not to interrupt the functioning of the Union and its single market.

4 min read

Profit Shifting: Evaluating the Evidence and Policies to Address It

The OECD has been working to assess the impact of their program of work, and it will be critical for this assessment to take into account impacts not only on revenues, but also on growth and investment.

7 min read

FAQ on Digital Services Taxes and the OECD’s BEPS Project

What is a digital services tax (DST)? What countries have announced, proposed, or implemented a DST? What are some of the criticisms of a DST? What are alternatives to a DST? What is the OECD BEPS project and what is its main objective? What is the main objective of OECD Pillar 1? What is the main objective of OECD Pillar 2?

8 min read

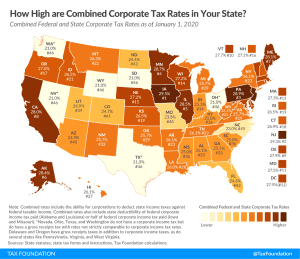

State Corporate Income Tax Rates and Brackets, 2020

Forty-four states currently levy a corporate income tax. Rates range from 2.5 percent in North Carolina to 12 percent in Iowa. Over the past year, several states, including Florida, Georgia, Indiana, Mississippi, Missouri, and New Jersey, implemented notable corporate income tax changes.

7 min read

The Davos Digital (Tax) Détente?

The past week has been nearly nonstop with news on various fronts of a dispute over taxation of digital businesses. The main characters have been the U.S., France, and the UK, although the EU and the OECD have also played roles. Though the dust is still settling, it is worth trying to tie the various events and arguments together.

7 min read

How Controlled Foreign Corporation Rules Look Around the World: France

In France, Controlled Foreign Corporation (CFC) rules were first enacted in 1980. The French tax regime operates on a strict territorial basis, where only profits generated in the country are subject to tax in France.

5 min read

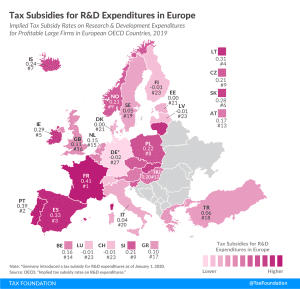

Territoriality of Tax Systems in Europe

3 min read

How Controlled Foreign Corporation Rules Look Around the World: China

The Chinese approach to base erosion and profit shifting is more focused on the application of transfer pricing rules and not on the application of CFC rules. Even with the rules in place, the Chinese tax authorities have not enforced the rules as much as other countries have.

3 min read

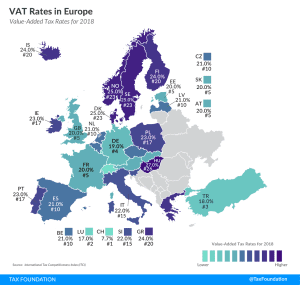

VAT Rates in Europe, 2020

4 min read