All Related Articles

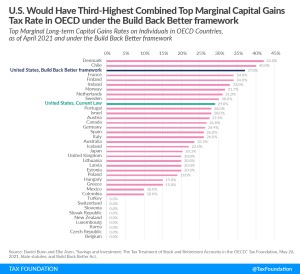

Proposed Top Combined Marginal Capital Gains Tax Rate Would Be Third-Highest in OECD

Under the new Build Back Better framework, the United States would tax capital gains at the third-highest top marginal rate among rich nations, averaging nearly 37 percent.

1 min read

Lawmakers Consider Untested and Complex Policies to Fund Reconciliation Bill

Congress is debating new ways to raise revenue that would make the tax code more complex and more difficult to administer. The new proposals—imposing an alternative minimum tax on corporate book income, applying an excise tax on stock buybacks, and, at one point this week, a tax on unrealized capital gains for billionaires—are unreliable and highly complex ways to raise revenue.

10 min read

Taxing Decisions, 2021: Minisode 2

President Biden and Congressional Democrats introduced a scaled-back proposal of their reconciliation package, with House leadership saying they hope to vote on this new trillion-dollar package ASAP. We talk through what made it into the deal, what was cut, and what the impact of these tax changes would be.

Fixing Tax Treatment of Capital Investments Could Improve Supply Chain Resiliency

While taxes are not at the root of supply chain disruptions, improvements to the tax code could make supply chains more resilient in the future.

3 min read

New Study Shows Tax Policy Has Strong Effects on Innovation

When examining how tax policy impacts the economy, researchers typically look at labor supply and investment responses. One other channel through which taxes impact the economy has been less studied: innovation.

3 min read

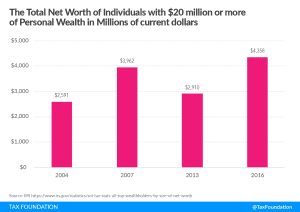

The Rich Are Not Monolithic and Taxing Their Wealth Invites Tax Collection Volatility

Congressional Democrats are reported to be weighing a special tax on the assets of billionaires to raise revenues to pay for their Build Back Better spending plan. There are two fundamental challenges to such a plan.

8 min read

How Would House Dems’ Tax Plan Change Competitiveness of U.S. Tax Code?

The legislation put forward by Democratic members of the House of Representatives would reverse many of the 2017 reforms while increasing burdens on businesses and workers.

2 min read

Washington Voters to Weigh in on New Capital Gains Income Tax

On May 4th, Gov. Jay Inslee (D) signed legislation creating a 7 percent capital gains tax, to take effect next year. On November 2nd, Washington lawmakers will learn what voters think about it.

5 min read

Lawmakers Could Pay for Reconciliation While Improving the Tax Code

With corporate and individual rate hikes potentially out of the Build Back Better (BBB) reconciliation package, lawmakers are weighing alternative options to raise revenue. Rather than come up with untested proposals and complicated changes to the tax base, they should prioritize options that raise revenue while improving the structure of the tax code.

4 min readProposed Minimum Tax on Book Income Would Hit Stock-Based Compensation

Raising taxes on stock-based compensation through a book income tax will disadvantage this form of compensation and produce more complexity in the tax system without providing benefits to workers.

5 min read

Funding for Democrats’ $3.5 Trillion Spending Plan Is Unstable and Unsustainable

One has to wonder how stable or sustainable the Democrats’ spending program can be if it must rely so heavily on the taxes paid by such a small number of taxpayers as in the top 1 percent.

5 min read

Louisiana Voters Have Chance to Simplify Taxes and Lower Burdens

Passage of Louisiana Amendments 1 and 2, which are aimed at the sales tax and individual and corporate income taxes, respectively, would substantially simplify the Pelican State’s tax code and provide tax relief in both the short and long term.

8 min read

Movers and Shakers in the International Tax Competitiveness Index, 2021

The Index provides lessons for policymakers when they are thinking of ways to remove distortions from their tax systems and remain competitive against their peers. The further up a country moves on the Index, the more likely it is to have broader tax bases, relatively lower rates, and policies that are less distortionary to individual or business decisions. Going the other way reveals a policy preference for narrow tax bases, special tax policy tools, and rules that make it difficult for compliance.

5 min read

Proposal for Reporting Requirements for Financial Institutions Misses the Mark

Reducing the tax gap is a good idea, but the reporting requirements for financial institutions could be better-targeted at the problem at hand.

4 min read

As Inflation Rises, So Will Tax Bills in Many States

Inflation is often called a hidden tax, but in many states it yields a far more literal tax increase as tax brackets fail to adjust for changes in consumer purchasing power.

5 min read

International Tax Competitiveness Index 2021

A well-structured tax code (that’s both competitive and neutral) is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

40 min read

Higher Taxes Under House Ways and Means Plan Emphasize Need for Corporate Integration

Under the House Ways and Means plan to raise taxes on corporations and individuals, the integrated tax rate on corporate income would rise to the third highest in the OECD. To reduce this burden, policymakers could explore integrating the individual and corporate tax systems.

8 min read