Recreational marijuana taxation is a hot policy issue in the US. Many states have elected to regulate and taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. legal marijuana sales and consumption, despite the ongoing federal prohibition. In December, President Trump signed an executive order directing the Attorney General to expedite the reclassification of marijuana from a Schedule I to a Schedule III drug under the Controlled Substances Act.

Today’s map shows states that have nullified the federal prohibition to establish a legal recreational cannabis market subject to an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections.. Legalization shifts consumers to safer legal markets while generating tax revenue for state programs. Harms associated with recreational marijuana are still somewhat understudied, but as more states allow legal markets and potential federal rescheduling enables medical study, more information will be available to optimize tax design.

Approaches to tax structure vary significantly across states. Some states tax by weight, some by price, and others by THC content. Ad valorem taxes are simpler but are associated with greater revenue volatility and do not target any specific harm-causing element. Ad quantum taxes on weight or quantity produce more stable revenues and better target the harm-causing element, but do not account for potency. Ad quantum taxes based on THC content most directly target the harm-causing element, but this adds complexity to the tax, and the technology to measure THC content can be so expensive that constant THC testing makes compliance costs unreasonable.

Disparate structures render state-by-state comparisons of rates or overall tax burden difficult. With federal prohibition still in effect, interstate commerce remains illegal, which creates a siloed market within each legalized state. Possible federal legalization may encourage harmony between state systems. When states legalize marijuana, taxes on legal product should be low enough to allow legal markets to compete with illicit markets, thereby reducing individual and societal harm while generating more revenues.

2026 Recreational Marijuana Taxes by State

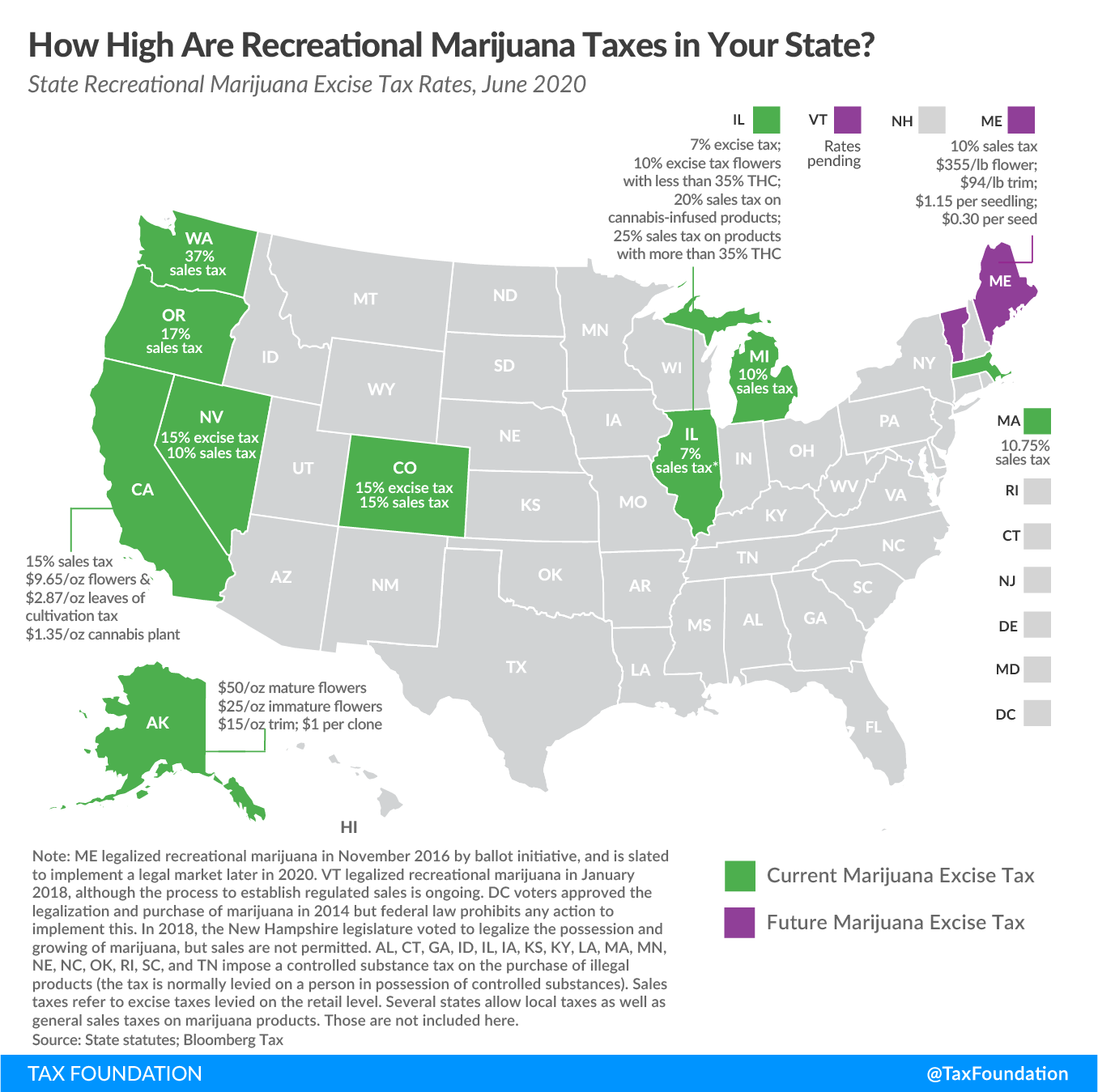

State Excise Tax Rates on Recreational Marijuana, January 2026

| State | Tax Rate |

|---|---|

| Alaska | $50/oz. mature flowers; $25/oz. immature flowers; $15/oz. trim; $1 per clone |

| Arizona | 16% on Retail Sales |

| California | 15% on Retail Gross Receipts |

| Colorado | 15% on Wholesale Average Market Rate ($658 per Pound of Bud); 15% on Retail Sales |

| Connecticut | 3% on Retail Sales; $0.00625 per milligram of THC in plants; $0.0275 per milligram of THC in edibles; $0.009 per milligram of THC in other cannabis products; $1 per THC Infused Beverage |

| Delaware | 15% on Retail Sales |

| Illinois | 7% on Wholesale Gross Receipts; 10% on Retail Sales of cannabis products with ≤35% THC; 20% on Retail Sales of cannabis-infused products like edibles; 25% on Retail Sales of any product with a THC concentration >35% |

| Maine | 10% on Retail Sales; $335/lb. flower; $94/lb. trim; $35 per mature plant; $1.5 per immature plant or seedling; $0.30 per seed |

| Maryland | 9% on Retail Sales |

| Massachusetts | 10.75% on Retail Sales |

| Michigan | 10% on Retail Sales |

| Minnesota (a) | 10% on Retail Gross Receipts |

| Missouri | 6% on Retail Sales |

| Montana | 20% on Retail Sales |

| Nevada | 15% on Wholesale Fair Market Value ($1,296 per Pound of Flower); 10% on Retail Sales |

| New Jersey | $2.50 per ounce |

| New Mexico (b) | 12% on Retail Sales |

| New York | 9% on Wholesale Sales; 13% on Retail Sales |

| Ohio | 10% on Retail Sales |

| Oregon | 17% on Retail Sales |

| Rhode Island | 13% on Retail Sales |

| Vermont | 14% on Retail Sales |

| Washington | 37% on Retail Sales |

Source: State statutes.

Data compiled by Jacob Macumber-Rosin , Adam Hoffer

2025 Recreational Marijuana Taxes by State

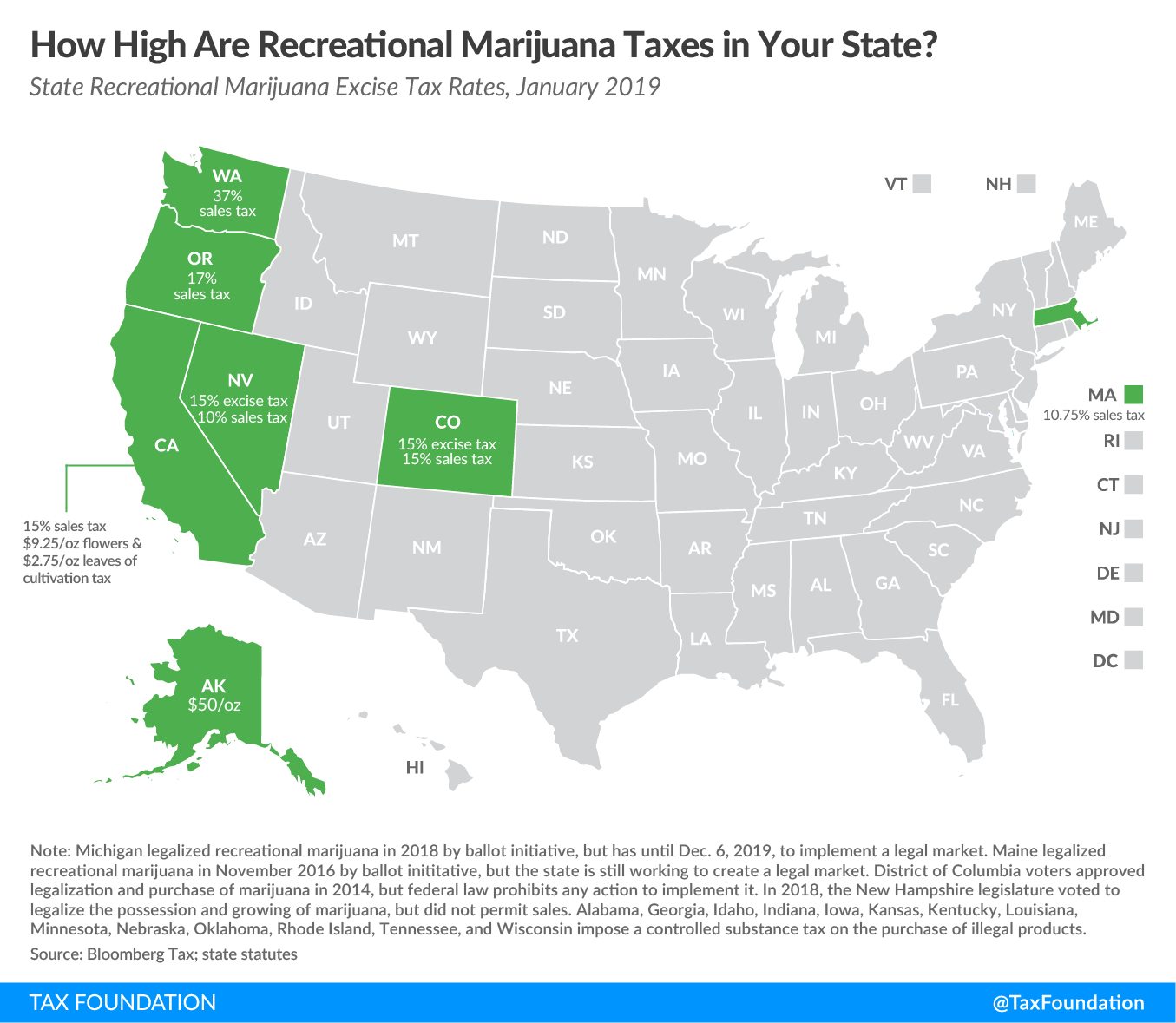

State Excise Tax Rates on Recreational Marijuana, as of January 2025

| State | Tax Rate |

|---|---|

| Alaska | $50/oz. mature flowers; $25/oz. immature flowers; $15/oz. trim; $1 per clone |

| Arizona | 16% on Retail Sales |

| California (a) | 15% on Retail Gross Receipts |

| Colorado | 15% on Wholesale Average Market Rate ($658 per Pound of Bud); 15% on Retail Sales |

| Connecticut | 3% on Retail Sales; $0.00625 per milligram of THC in plants; $0.0275 per milligram of THC in edibles; $0.009 per milligram of THC in other cannabis products; $1 per THC Infused Beverage |

| Delaware (b) | 15% on Retail Sales |

| Illinois | 7% on Wholesale Gross Receipts; 10% on Retail Sales of cannabis products with ≤35% THC; 20% on Retail Sales of cannabis-infused products like edibles; 25% on Retail Sales of any product with a THC concentration >35% |

| Maine | 10% on Retail Sales; $335/lb. flower; $94/lb. trim; $35 per mature plant; $1.5 per immature plant or seedling; $0.30 per seed |

| Maryland | 9% on Retail Sales |

| Massachusetts | 10.75% on Retail Sales |

| Michigan | 10% on Retail Sales |

| Minnesota (b) | 10% on Retail Gross Receipts |

| Missouri | 6% on Retail Sales |

| Montana | 20% on Retail Sales |

| Nevada | 15% on Wholesale Fair Market Value ($1,296 per Pound of Flower); 10% on Retail Sales |

| New Jersey | $2.50 per ounce |

| New Mexico (a) | 12% on Retail Sales |

| New York | 9% on Wholesale Sales; 13% on Retail Sales |

| Ohio | 10% on Retail Sales |

| Oregon | 17% on Retail Sales |

| Rhode Island | 13% on Retail Sales |

| Vermont | 14% on Retail Sales |

| Washington | 37% on Retail Sales |

(a) Rate scheduled to increase July 1, 2025

(b) Actual retail sales not yet begun as of January 2025

Source: State Statutes; Bloomberg Tax

Data compiled by Adam Hoffer, Jacob Macumber-Rosin

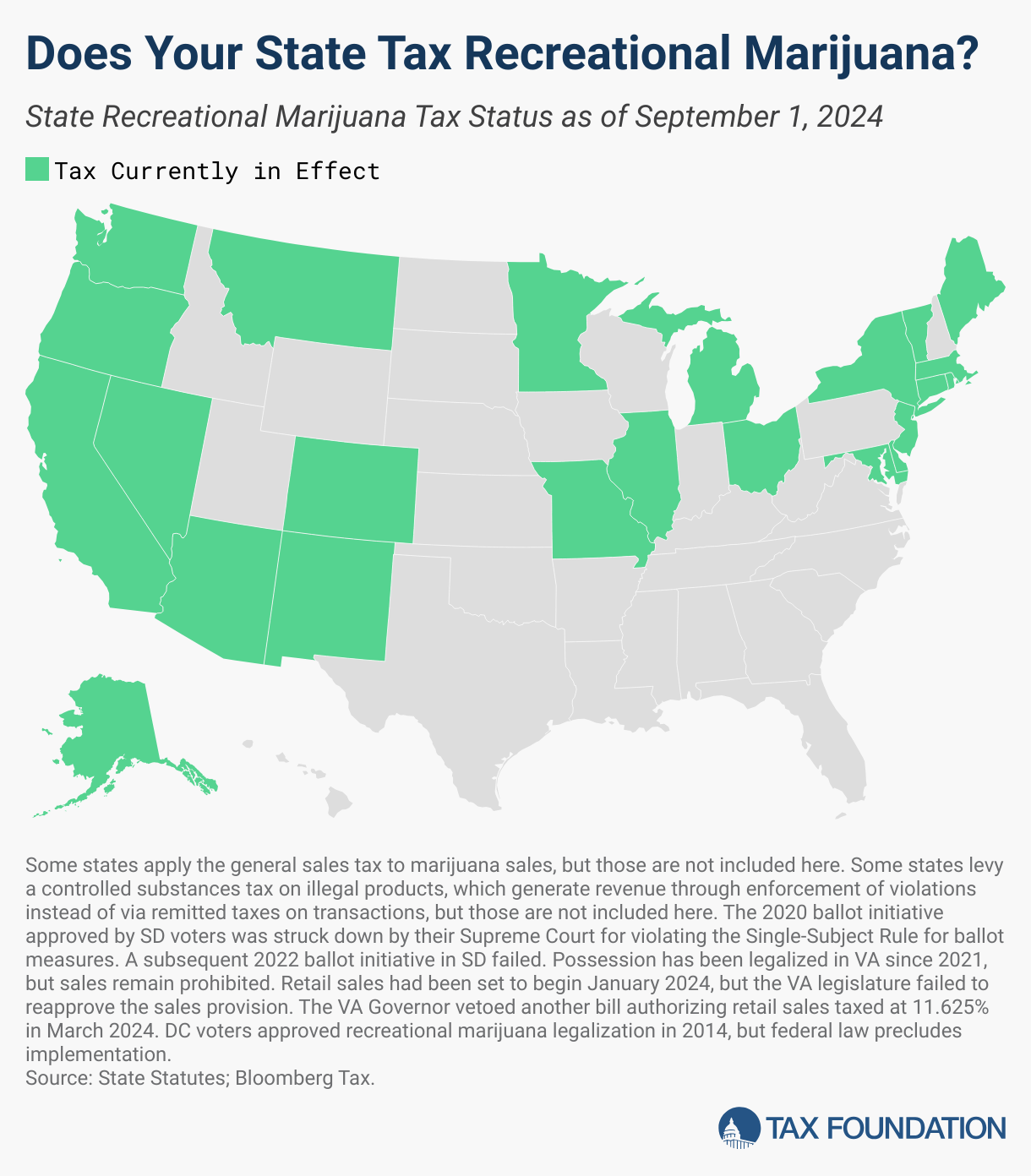

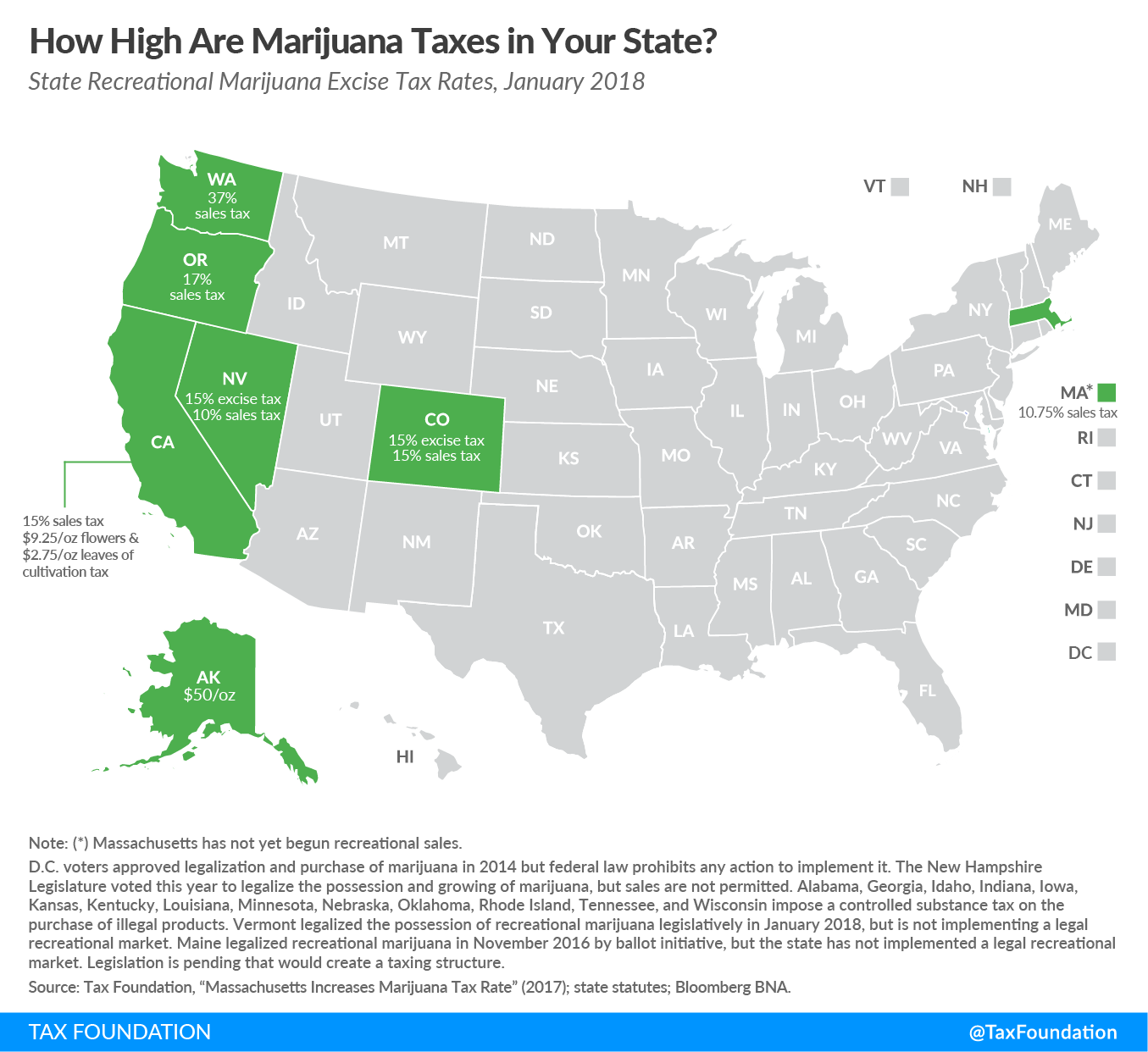

State Excise Tax Rates on Recreational Marijuana, as of September 2024

| State | Tax Rate(s) | Notes |

|---|---|---|

| Alaska | $50/oz of Mature Flowers | |

| Alaska | $25/oz of Immature Flowers and Abnormal Buds | |

| Alaska | $15/oz of Plant Trims | |

| Alaska | $1 per Clone Plant | |

| Arizona | 16% on Retail Sales | If a federal excise tax is imposed, AZ caps combined rates to 30% and automatically reduces the state rate to combine to 30%. |

| California | 15% on Retail Gross Receipts | Counties may impose additional excise taxes, which would be included in the gross receipts for the purposes of the state excise tax. |

| Colorado | 15% on Wholesale Average Market Rate | Counties and municipalities can impose additional excise taxes on wholesale transactions, up to 5%. |

| Colorado | 15% on Retail Sales | |

| Connecticut | $0.00625 per milligram of THC in plant material | |

| Connecticut | $0.0275 per milligram of THC in edible products | |

| Connecticut | $0.009 per milligram of THC in other cannabis | |

| Connecticut | $1 per THC Infused Beverage | |

| Connecticut | 3% Municipal Tax on Retail Gross Receipts | |

| Delaware | 15% on Retail Sales | The tax was imposed in April 2023, but sales have yet to actually begin. The Office of the Marijuana Commissioner only began accepting applications for licenses in August 2024. Licenses for cultivation are expected to be issued in November 2024, product manufacturing in December 2024, and retail in March 2025. |

| Illinois | 7% on Wholesale Gross Receipts | Counties and municipalities may impose additional taxes up to 3.75%. |

| Illinois | 10% on Retail Sales of Products with 35% or less THC | |

| Illinois | 20% on Retail Sales of Cannabis-Infused Products | |

| Illinois | 25% on Retail Sales of Products with more than 35% THC | |

| Maine | $335/lb of Flowers | |

| Maine | $94/lb of Plant Trim | |

| Maine | $35 per Mature Plant | |

| Maine | $1.5 per Immature Plant or Seedling | |

| Maine | $0.3 per Seed | |

| Maine | 10% on Retail Sales | |

| Maryland | 9% on Retail Sales | |

| Massachusetts | 10.75% on Retail Sales | Localities may impose additional taxes up to 3%. |

| Michigan | 10% on Retail Sales | |

| Minnesota | 10% on Retail Gross Receipts | |

| Missouri | 6% on Retail Sales | Cities and counties may impose additional taxes up to 3%, which was interpreted by Missouri courts to mean 3% each to total 6%. |

| Montana | 20% on Retail Sales | Counties may impose additional taxes up to 3%. |

| Nevada | 15% on Wholesale Fair Market Value | |

| Nevada | 10% on Retail Sales | |

| New Jersey | $1.24/oz Social Equity Excise Fee | The Social Equity Excise Fee is calculated to be 0.333% of the Average Retail Price, capped per ounce depending on the Average Retail Price up to $10/oz. The rate cap increases if the average retail price decreases. Municipalities may impose additional taxes, up to 1% on wholesale receipts or 2% on cultivator, manufacturer, and retailer receipts, totaling 7% before accounting for pyramiding effects. |

| New Mexico | 12% on Retail Sales | Beginning July 1 2025, the tax is set to increase incrementally 1% per year until reaching 18% in July 2030. |

| New York | 9% on Wholesale Sales | |

| New York | 9% on Retail Sales | |

| New York | 4% Local Tax on Retail Sales | |

| Ohio | 10% on Retail Sales | Legal retail sales began August 2024. |

| Oregon | 17% on Retail Sales | Cities and counties may impose additional taxes up to 3%. |

| Rhode Island | 10% on Retail Sales | |

| Rhode Island | 3% Local Tax on Retail Sales | |

| Vermont | 14% on Retail Sales | |

| Washington | 37% on Retail Sales |

Sources: State Statutes; Bloomberg Tax.

2024 Notable Changes

- Minnesota legalized recreational marijuana and taxes sales at 10 percent of retail gross receipts.

- Ohio legalized recreational marijuana and taxes sales at 10 percent of retail sales.

- Delaware established a 15 percent tax on retail sales, but business licensure has yet to be completed, so sales have yet to begin. Retail licenses are expected in March 2025.

- California switched its wholesale-level tax to a tax levied on retail gross receipts.

- New York swapped its specific tax by THC content for a 9 percent ad valorem wholesale tax.

- Planned legalization in Virginia was not authorized by the state legislature, and a subsequent attempt to legalize recreational sales and tax them at 11.625 percent was vetoed by the governor.

Data compiled by Adam Hoffer, Jacob Macumber-Rosin

Changes from 2025

- Maine rebalanced the taxes on recreational marijuana. The wholesale taxes per unit of product were reduced across product types, including from $335 per pound of flower to $223 per pound of flower, while the percentage tax on retail sales was raised from 10 to 14 percent.

- Maryland increased the tax on retail sales of recreational marijuana from 9 to 12 percent.

- Michigan established a new 24 percent wholesale tax on recreational marijuana in addition to the 10 percent retail tax that is still levied.

- Minnesota raised the tax on retail gross receipts of recreational marijuana from 10 to 15 percent.

- New Mexico raised the tax on retail sales of recreational marijuana from 12 to 13 percent, and has similar increases scheduled annually until 2030.

Nearly half of US states regulate and tax recreational markets, and only 10 states still lack a comprehensive medical marijuana program. A few states have decriminalized possession but have not allowed for the cultivation or sale of marijuana, sometimes due to gubernatorial vetoes or court rulings blocking legalization.

Many states that have not yet legalized marijuana seem to be moving toward legalization, but challenges clearly remain. This year is set to be another eventful year for drug policy ballot initiatives, which may shift the marijuana tax landscape further. Legislative efforts are ongoing in many states, such as Virginia, New Hampshire, and Pennsylvania. Efforts seem to be underway for federal rescheduling of marijuana, which has some tax implications, but would not change the federal prohibition of recreational marijuana. More comprehensive federal reforms like the STATES 2.0 Act would be required to actually legalize marijuana.

Under the existing federal prohibition, businesses that operate in states that have nullified the federal policy to establish quasi-legal markets remain burdened by the inability to participate in interstate commerce. These businesses also have difficulty doing business with banking institutions and face struggles associated with the unique legal framework.

Many states have been facing budget shortfalls and/or a struggling legal marijuana industry, which has prompted several changes to marijuana tax policy. The tax in California increased briefly from 15 to 19 percent before that increase was reverted and delayed to give some relief to the industry. The new Michigan wholesale tax on adult-use marijuana was prompted by transportation revenue needs, with revenues from the new tax dedicated to the neighborhood road fund. Minnesota budget woes spurred the marijuana tax increase from 10 to 15 percent before legal sales even began.

Excise taxes on recreational marijuana are ill-suited for filling gaps in general revenue or shortfalls in unrelated spending programs. Squeezing the legal marijuana industry for revenue unnecessarily burdens a growing industry and encourages consumers to stick to established illicit markets. States should not go through all the trouble of nullifying federal marijuana prohibition, administering licensure and regulations, and fostering a legal market only to overburden that market with taxes that render it unable to compete with illicit purveyors.

A significant majority of marijuana consumption already occurs via illicit markets, even as more states legalize sales. States that impose excessive taxes, require expensive or limited licensure, or otherwise hinder their legal markets may not experience significant reductions in illicit consumption. If prices in legal markets are kept higher than illicit market prices, consumers will not be incentivized to switch to safer legal products. Properly designed taxes have the potential to generate billions of dollars in revenue for the states, though it may take some time for these revenues to be realized as legal markets develop.

With interstate commerce prohibited, the disparate tax designs across states do not yet create some of the problems that occur in other legal markets. There are no multistate businesses that must comply with varied regulations, and tax arbitrage or double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. cannot legally occur. However, if interstate commerce is eventually tolerated by the federal government, the significant differences in tax designs may create negative effects and opportunities for tax avoidance. States should prepare to harmonize their tax designs once interstate marijuana business is allowed—and would be better advised to coalesce around best practices now, before systems become more difficult to reform.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe