All Related Articles

Bonus Depreciation Helps Disadvantaged Workers, Study Finds

Low-skilled workers have been the hardest hit by the pandemic-induced economic slowdown. When deciding on bonus depreciation, which is currently set to expire in 2026, policymakers should remember that disadvantaged workers would be the most likely to benefit from making it permanent.

2 min read

Ohio’s CAT Is Out of the Bag

Coming out of the pandemic, the state of Ohio is estimating significant tax revenue growth, and some lawmakers are looking to take advantage and repeal the Commercial Activity Tax (CAT), one of only a few gross receipts taxes still levied in the country.

7 min read

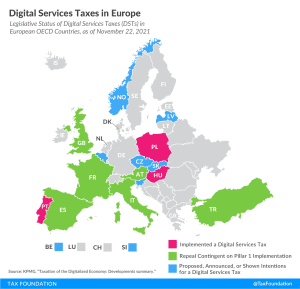

Digital Services Taxes in Europe, 2021

Despite ongoing multilateral negotiations in the OECD, about half of all European OECD countries have either announced, proposed, or implemented their own unilateral digital services tax.

7 min read

Business Tax Collections Within Historical Norm After Accounting for Pass-through Business Taxes

When looking at the tax burden on businesses over time, it is important to provide a complete picture by accounting for the different types of businesses in the U.S. and the timing effects of the 2017 tax law. Doing so provides important context on existing tax burdens and for considering the impact of raising taxes on corporations and pass-through firms.

3 min read

How Will Build Back Better Impact Inflation?

The persistently high inflation in recent months has made some lawmakers question the need for additional deficit spending, In the short term, the Build Back Better Act would likely contribute to inflation, but the magnitude of that contribution is unclear.

3 min read

Red Flags Emerge in Build Back Better Book Minimum Tax, Interest Expense Limitation

The Build Back Better Act would raise taxes to pay for social spending programs. But the design of some of the tax increases may end up hurting private pensions, among other problems.

6 min read

Norway’s New Budget Adds Unnecessary Complexity

Norway’s proposed reductions in income tax have the potential to increase disposable income for workers that can potentially raise consumption and contribute to economic growth. However, the increase of the wealth and indirect taxes is likely to step up the complexity of the tax system and create additional distortions.

3 min read

How Do Build Back Better Taxes Affect 5G Competition?

One unintended consequence of the tax proposals in the Build Back Better Act is a higher potential burden on wireless spectrum investments, which could slow the build out of 5G technology as the U.S. races to compete with other countries—moving in the opposite direction of countries like China that are actively subsidizing 5G expansion.

5 min read

Economy Loses More than Revenue Gains in the House Build Back Better Act

Due to the House Build Back Better tax plan’s economically costly and inefficient tax increases, our analysis finds that long-run GDP would drop by a little over $1 for every $1 in new tax revenue.

6 min read

Taxing Decisions, 2021: Minisode 3 Revenge of the SALT

Infrastructure has made its way across the finish line, but the tax debate is far from over on Capitol Hill. Senior policy analyst Garrett Watson joins host Jesse Solis to walk us through the latest iteration of Democrats’ trillion-dollar reconciliation package and the myriad tax changes that are being proposed to finance this deal.

2022 Tax Brackets

The IRS recently released the new inflation adjusted 2022 tax brackets and rates. Explore updated credits, deductions, and exemptions, including the standard deduction & personal exemption, Alternative Minimum Tax (AMT), Earned Income Tax Credit (EITC), Child Tax Credit (CTC), capital gains brackets, qualified business income deduction (199A), and the annual exclusion for gifts.

5 min read

Comparing Tax Provisions in Different Versions of the House Build Back Better Act

The most recent versions of President Biden’s Build Back Better plan are improvements on the original proposal, but would still reduce economic growth and average after-tax incomes for the top 80 percent of earners in the long run.

7 min read

Tax Foundation Comments on Maryland’s Digital Advertising Tax Regulations

While it is not within the purview of the Comptroller’s office to reject a legislatively-approved tax no matter how poor—or constitutionally infirm—the underlying policy, the regulations fairly to fully resolve several important issues raised by the bill, while potentially creating additional legal infirmities in the regulation’s approach to apportionment.

Despite Slip in International Tax Competitiveness Index, Germany Retains Top G7 Rank

More often than not, by looking at Germany’s tax code as an example, G7 countries can improve the stability of their revenues and the lives of those they represent.

5 min read

Spain’s 2022 Budget Unsurprisingly Comes with More Tax Hikes

While other countries in Europe are working towards introducing tax cuts or delaying the introduction of new taxes to stimulate economic recovery by supporting business investment and employment, Spain is putting more fiscal pressure on businesses.

3 min read

Pro-Growth Tax Reform for Oklahoma

Our new study identifies a number of deficiencies in Oklahoma’s tax code and outlines possible solutions for reform that would create a more neutral tax code and encourage long-term growth in the state.

6 min read

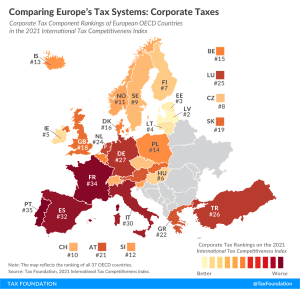

Comparing Europe’s Tax Systems: Corporate Taxes

According to the corporate tax component of the 2021 International Tax Competitiveness Index, Latvia and Estonia have the best corporate tax systems in the OECD.

3 min read

Tracking 2021 Election Results: State Tax Ballot Measures

Through 10 ballot measures across four states—Colorado, Louisiana, Texas, and Washington—voters will decide significant questions of state tax policy.

7 min read

Austria’s Budget Comes with Tax Cuts and Carbon Levies

Austria should not shy from lowering the corporate income tax rate sooner or even implementing a more ambitious tax reform to improve its tax competitiveness and contribute to greater economic growth.

3 min read