Thank you for the opportunity to respond to the stakeholder consultation on the impact of the policies in the Base Erosion and Profit Shifting (BEPS) package. This response covers TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation’s views on the effort and summarizes some pieces of the academic literature that have explored these issues.

In the mid-2010s, the Organisation for Economic Co-operation and Development (OECD) led a collaborative effort among countries that fostered many ideas for simplifying international taxes, preventing abuse, and facilitating multilateral standards or agreements. Several of these ideas were converted into a 15-point action plan. In some cases, these actions became viable policy recommendations, and several of those policy recommendations became law in participating countries.

Overall, OECD tax efforts of the 2010s have generated some genuine successes, and it is important to take away the right lessons from those successes both from clear examples in a US policy context and from academic studies.

Multilateralism Has a Significant but Limited Role in Tax Policy

The most important lesson is that large-scale international cooperation has significant merit, even if not all international tax policy ideas become or should become law. Countries should remain at the negotiating table to help distinguish between the ideas that should and should not be realized in policy.

In many cases, multilateral forums are the best avenue for establishing certain processes or definitions. For example, standardized processes can improve fairness and reduce costs in dispute resolution, especially for smaller countries.[1] Furthermore, consistency in a process is often a hallmark of fairness.

Multilateralism is also valuable for certain key definitions of terms, especially where misaligned definitions might otherwise result in undue double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. or non-taxation. The OECD’s efforts on hybrid-mismatch arrangements helped the EU establish common definitions through directives,[2] and they helped the US move closer to EU definitions through administrative action by the US Treasury.[3] Fixing straightforward flaws like these allows tax authorities to spread the tax burden more proportionally among firms, rather than unduly privileging those able to take advantage of mismatched definitions to pay less tax.

However, a too-rigid approach to standardization on too many elements has costs of its own: one-size-fits-all policy leaves little room for experimentation and can be hard to unwind once adopted. And the more universal a policy choice, the more strategies may be designed specifically to exploit that policy’s downsides.

Note that multilateral implementation of international tax rules does not always need to be coerced. Some provisions prove their merit as win-wins for most jurisdictions and achieve broad voluntary adoption.

Two Strong Systems for Controlled Foreign Corporation (CFC) Rules Were Created in the Last Decade

Perhaps the most significant innovation in international taxation of the last decade was an overhaul of CFC rules, a goal of BEPS Action 3. At the onset of the BEPS project, many systems of international tax needed reform. This was especially true of the US, whose combination of worldwide taxation, deferral, and high rates was disastrous, resulting in troves of “overseas profits” that would hold out for repatriationRepatriation is the process by which multinational companies bring overseas earnings back to the home country. Prior to the 2017 Tax Cuts and Jobs Act (TCJA), the US tax code created major disincentives for US companies to repatriate their earnings. Changes from the TCJA eliminate these disincentives. holidays to be realized.

The OECD was among several forums for discussing potential improvements. And ultimately, many of the insights generated in the OECD Action 3 report became critical to the design of future CFC rules: most importantly, the US global intangible low-taxed income (GILTI) system and the income inclusion rule (IIR).

Both regimes therefore operationalize three core Action 3 insights. First, they make low-taxed foreign income immediately taxable in the residence jurisdiction, avoiding the bizarre incentives that deferral created. Second, they exclude some returns to substance, resembling the “excess profits analysis” approach to defining CFC income described in the Action 3 report. Third, they use foreign tax crediting to reduce double taxation and apply higher taxes to multinational enterprises (MNEs) that take greater advantage of low-tax jurisdictions.

Of these two systems, Tax Foundation modeling shown below illustrates that the system designed for the US in 2017 is less taxpayer-friendly than a minimum IIR despite its lower rate; in many cases, these taxpayer-unfriendly features are poor choices, and the US may be better served by eliminating them, even if higher rates are needed to recoup the revenue.

Table 1. Revenue Impact of Conversion of US 2017 Reform to Income Inclusion Rule (Billions)

| Policy Change | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 | 2026-2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Pillar Two Excess Returns Approach | 1.08 | 1.12 | 1.11 | 1.13 | 1.18 | 1.22 | 1.28 | 1.34 | 1.36 | 1.42 | 12.24 |

| Direct Expense Allocation | -14.73 | -14.87 | -15.04 | -15.28 | -15.71 | -16.29 | -16.98 | -17.66 | -18.32 | -19.1 | -163.98 |

| Full Carryforwards | -8.77 | -11.93 | -14.11 | -15.81 | -17.27 | -18.45 | -19.68 | -20.88 | -22.07 | -23.15 | -172.12 |

| Raise Top Rate to 15 Percent | 10.77 | 10.66 | 10.05 | 10.45 | 10.97 | 11.45 | 12.43 | 13.01 | 13.54 | 14.21 | 117.54 |

| Full Foreign Tax Crediting | -9.48 | -10.65 | -11.61 | -12.54 | -13.54 | -14.56 | -15.66 | -16.7 | -17.76 | -18.76 | -141.26 |

| Country-by-Country | 9.36 | 9.65 | 9.16 | 9.35 | 9.52 | 9.7 | 10.22 | 10.48 | 10.75 | 11.09 | 99.28 |

| Total | -11.76 | -16.02 | -20.44 | -22.7 | -24.85 | -26.93 | -28.38 | -30.41 | -32.49 | -34.27 | -248.25 |

Modeling provisions of this complexity comes with considerable uncertainty, but at least some provisions, such as foreign tax crediting, are sufficiently clear for us to remain certain that the US system raises more revenue than a minimum IIR does.

We believe that this general finding for the US rules will hold true even after the 2025 tax legislation makes changes to GILTI.

The US Experience Shows Success in Curbing Profit Shifting

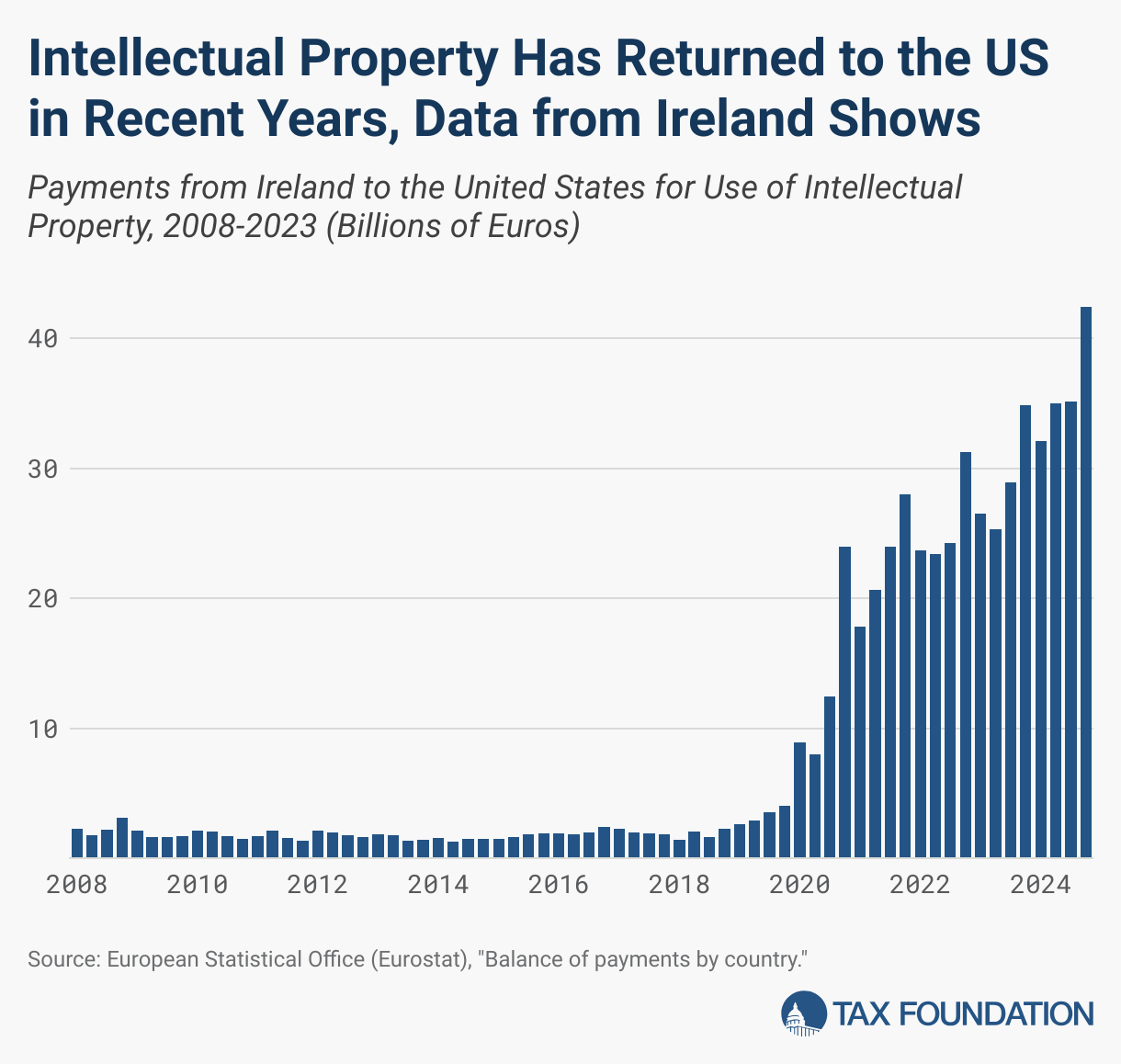

One measure of the success of recent US and OECD reforms can be found in Irish trade data with the US. Ireland is a small, open economy, and its trade data is often a proxy for the behavior of extremely large corporations that route significant payments through it.

Irish economist Seamus Coffey first noted in 2021 a dramatic change in intellectual property payments in Irish trade data. The payments to the US for intellectual property were greatly increasing. Coffey further showed that the change was not from an overall increase in Irish intellectual property imports. Rather, the source of the imports changed: the US increase came at the expense of offshore financial centers.

“A case study of US MNCs in the information and communication technology (ICT) sector shows that under the revised structures the use of technology in international markets is no longer licensed from jurisdictions such as Bermuda and the Cayman Islands but instead is licensed directly from the United States,” Coffey wrote. “This is in line with the economic footprint of these companies and aligns the reporting of their profits with the location of their substance.”[4]

The trend has continued, even more dramatically, since 2021. Payments to the US have increased by 2,227 percent from the last quarter of 2017 to the last quarter of 2024. An extension of Coffey’s data series is shown below.

Compliance Costs Should Be a Consideration in Global Policymaking

The BEPS project’s 15 actions were decisive responses to real problems in cross-border taxation, offering real benefits but also real costs. A decade of implementation experience has revealed a critical side effect: sharply higher compliance costs for both tax administrations and the business community. Assembling data in multiple formats for multiple jurisdictions is not an easy job. While these requirements undoubtedly expand the information set available to authorities, they have also required the labor of intelligent professionals who undoubtedly could have contributed to their companies or their national economies in other ways. Every requirement comes with an opportunity cost.

Surveys show international tax policy has an outsized role in driving compliance costs. For example, a Tax Foundation survey of compliance costs for large US companies revealed that the majority of both headcount and non-personnel costs in their tax departments were for international income taxes, even though domestic taxes comprise most taxes paid.[5] In some cases, OECD actions may reduce compliance costs, which is a worthwhile goal. But requiring too many data points on a country-by-country basis can quickly become a runaway multiplication problem for a multinational enterprise with many subsidiaries in many jurisdictions.

As new initiatives enter into force, the cumulative compliance stack threatens to become unsustainably thick. The solution is not perpetual expansion but disciplined pruning. After the most impactful “low-hanging fruit” has been harvested, additional layers of anti-avoidance protection may incur the same kinds of compliance costs but deliver diminishing returns.

A periodic “garden-weeding” exercise would help keep the international tax system coherent. Rules that have proven duplicative, ineffective, or overly burdensome should be eliminated.

Measured and Steady Progress Is Ideal

Many successful US and OECD reforms in the 2010s were long-considered changes to address longstanding and well-understood flaws of the international tax system. It takes time to generate insights about what reforms should be accomplished next.

In turn, future international efforts may also need time. Many of the actions of the 2010s will still take time to evaluate. There was, in many cases, a lag between the finalization of OECD ideas and implementation. And furthermore, profit shifting or other tax avoidance behaviors are not immediate. Some tax provisions may take years or decades for their effects to be fully felt; for example, even in 2025, many US companies still retain some vestigial structures designed to optimize for the pre-2017 US tax code. Many of the best reforms of the 2010s are not yet done bearing fruit.

Another reason to take one’s time in designing new tax measures is that stability in tax policy is a virtue in itself. Companies can plan investments better if they know what kind of tax code will be in effect for the life of their investment. And tax professionals are more efficient when they work with well-known and long-standing systems.

Findings in the Academic Literature

In 2021, Tax Foundation’s Elke Asen produced a broad summary of academic efforts to understand profit shifting and the impact of the OECD BEPS 1.0 initiative.[6] While this work comes soon after broad implementation of these guidelines, it still gives helpful insight into the early effects of such policy changes. She uses the available literature to answer three questions in particular: what is the magnitude of global tax revenue lost due to corporate avoidance, which means are MNEs using to shift their profits, and how effective have implemented countermeasures been thus far. An important reference point in this exercise is the reality that there is a trade-off between countering corporate tax avoidance, and fostering a robust business environment inclined towards investment and employment.

By the point of Asen’s 2021 review, nearly all OECD countries had transfer pricing regulations, thin capitalization rules, CFC rules, and nexus requirements. While a lack of a track record made thorough assessment of these efforts difficult, there were still discernible trends in the economic data.

A 2018 working paper by researchers at the International Monetary Fund found that transfer pricing regulations harm real investment in the country that implements them. De Mooij and Liu found, using a dataset of 27 countries between 2006 and 2014, that such measures decrease multinational corporations’ domestic investment in excess of 11 percent.[7] Transfer pricing regulations (TPRs) increase the cost of capital for a firm, leading to a 23 percent higher “TPR-adjusted” corporate tax rate for multinationals. However, while such regulations tend to decrease real investment domestically, De Mooij and Liu found that they do not lead to a decrease in total investment by the multinational group.

Other research on transfer pricing enforcement mechanisms have explored a different angle of their impact. Recent working papers by members of the National Bureau of Economic Research have shed light on some of the effects of the OECD’s transfer pricing directives. Specifically, Bustos et al. analyzed the effect of Chile’s implementation of these standards while Pomeranz and Serrato did the same for Chile in addition to Columbia, Spain, and Uruguay. [8] Bustos et al. found, by using national labor and taxation data, that Chile’s tightening of transfer pricing standards resulted in minimal revenue generated while significantly increasing the number of tax planning professionals employed by multinational enterprises in Chile. Pomeranz and Suárez Serrato supported these findings, and then through their comparative analysis of all four countries, found that the magnitude of this effect was correlated with the severity of the standards implemented.

Recent research by Koch and Scheider gives helpful insight into the evolution of the tax avoidance landscape in recent years.[9] The key finding of their analysis, conducted using IFRS financial statements of European multinationals, is that there has been a significant decline in MNE tax avoidance in the period after 2017. They also show that the trend of decreasing tax avoidance remains even when disregarding firms with many US affiliates. Specifically, Koch and Scheider find that from 2011-2017, the companies in their sample averaged a 4.7-7.8 percent reduction in their effective tax rates through intragroup profit differences. This figure is significantly lower from 2018 onwards, where they found that such corporations were only able to lower their effective tax rates by 2.2-2.7 percent.

[1] OECD, 16 September 2024, OECD/G20 Inclusive Framework on BEPS shows progress in making dispute resolution more effective and in improving tax transparency through country-by-country reporting.

[2] European Union, “Council Directive 2016/1164, laying down rules against tax avoidance practices that directly affect the functioning of the internal market,” Jul. 12, 2016, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32016L1164; European Union, “Council Directive 2017/952, amending Directive (EU) 2016/1164 as regards hybrid mismatches with third countries,” May 29, 2017, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2017.144.01.0001.01.ENG.

[3] Federal Register, “Rules Regarding Certain Hybrid Arrangements,” Apr. 8, 2020, https://www.federalregister.gov/documents/2020/04/08/2020-05924/rules-regarding-certain-hybrid-arrangements.

[4] Seamus Coffey, “The changing nature of outbound royalties from Ireland and their impact on the taxation of the profits of US multinationals – May 2021,” Ireland Department of Finance, Jun. 14, 2021, https://www.gov.ie/en/publication/fbe28-the-changing-nature-of-outbound-royalties-from-ireland-and-their-impact-on-the-taxation-of-the-profits-of-us-multinationals-may-2021/.

[5] William McBride, “Results of a Survey Measuring Business Tax Compliance Costs,” Tax Foundation, Sep. 4, 2024, https://taxfoundation.org/research/all/federal/us-business-tax-compliance-costs-survey/.

[6] Elke Asen, “What We Know: Reviewing the Academic Literature on Profit Shifting,” Tax Notes Federal, May 24, 2021, https://www.taxnotes.com/tax-notes-today-federal/base-erosion-and-profit-shifting-beps/what-we-know-reviewing-academic-literature-profit-shifting/2021/06/10/60lz1.

[7] Ruud De Mooij and Li Liu, “At a Cost: The Real Effects of Transfer Pricing Regulations,” International Monetary Fund (2018).

[8] Sebastián Bustos et al., “The Race Between Tax Enforcement and Tax Planning: Evidence from a Natural Experiment in Chile,” National Bureau of Economic Research Working Paper, April 2025, https://www.nber.org/system/files/working_papers/w30114/w30114.pdf; Dina Pomeranz, Juan Carlos Suárez Serrato, “Do Transfer Pricing Reforms Lead to a Boom in Tax Consultants?,” National Bureau of Economic Research Working Paper, May 2025, https://www.nber.org/system/files/working_papers/w33736/w33736.pdf.

[9] Reinold Koch and Till Scheider, “The Known Unknown: Tax Avoidance by European Multinationals” Steur und Wirtschaft, Jun. 25, 2025, S68-S77, https://steuerrecht.uni-koeln.de/sites/steuerrecht/StuW/Jahrgaenge/StuW_2025_-_Sonderheft_NeSt.pdf.