Repatriation is the process by which multinational companies bring overseas earnings back to the home country. Prior to the 2017 Tax Cuts and Jobs Act (TCJA), the US tax code created major disincentives for US companies to repatriate their earnings. Changes from the TCJA eliminate these disincentives.

Repatriation under a Worldwide Tax System

Prior to the 2017 TCJA, the United States had a worldwide tax system, under which US corporations were required to include all earnings into their domestic tax base, even those that were made outside the United States.

However, income earned in foreign operations was not taxed until it was repatriated to the US parent corporation. For example, imagine a US company with a subsidiary in the UK. That subsidiary paid the UK’s 19 percent corporate tax on its earnings. When the US parent company repatriated these earnings to the United States, it would owe an additional 16 percent tax—the difference between the UK’s 19 percent and the pre-TCJA 35 percent corporate tax rate—on those earnings.

If instead the company held its earnings overseas, it would not owe this additional tax until the earnings were brought to the US. This discouraged companies from repatriating their earnings, building a large amount of earnings overseas and deferring US tax liability.

Repatriation Since TCJA

The TCJA enacted reforms that shifted from worldwide taxation toward territorial taxation, in which only income earned within the United States is subject to the US corporate income tax, removing the main tax barrier to repatriation.

To transition to this new territorial tax system and address the buildup of cash that occurred under the old worldwide tax system, the TCJA imposed a one-time tax of 15.5 percent on liquid assets like cash and 8 percent on illiquid assets, payable in installments over eight years, regardless of whether companies repatriate old overseas earnings.

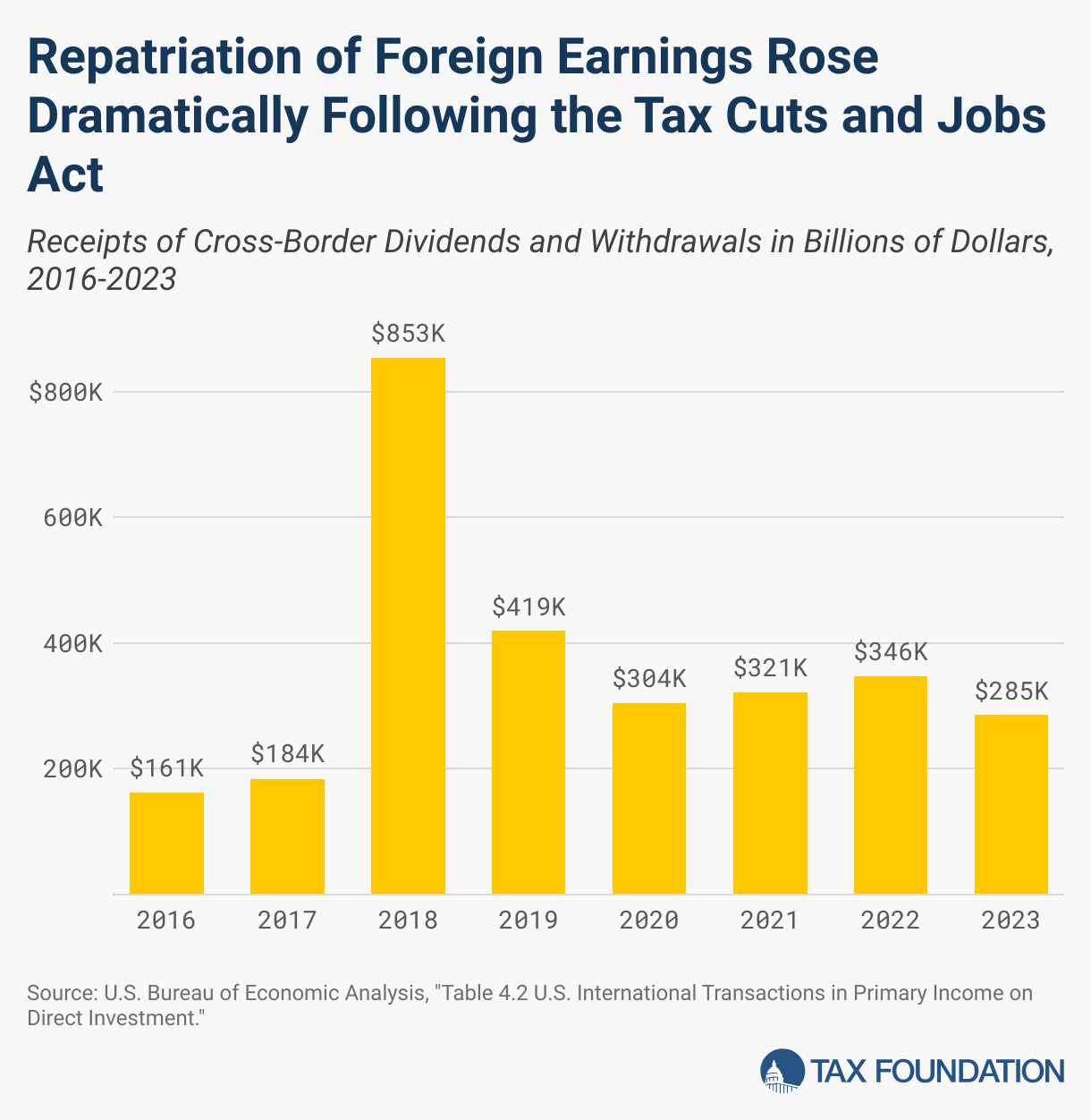

Data indicates a significant uptick in repatriation following enactment of the TCJA, though these figures include repatriation of current earnings as well as past earnings. It is also important to understand the composition of overseas earnings—earnings that have been reinvested in illiquid assets are not likely to be repatriated.

It is important to keep in mind that one-time influxes of cash do not change the incentives to invest. Thus, companies choosing to repatriate their past earnings generally does not boost investment or create jobs.

Stay updated on the latest educational resources.

Level-up your tax knowledge with free educational resources—primers, glossary terms, videos, and more—delivered monthly.

Subscribe