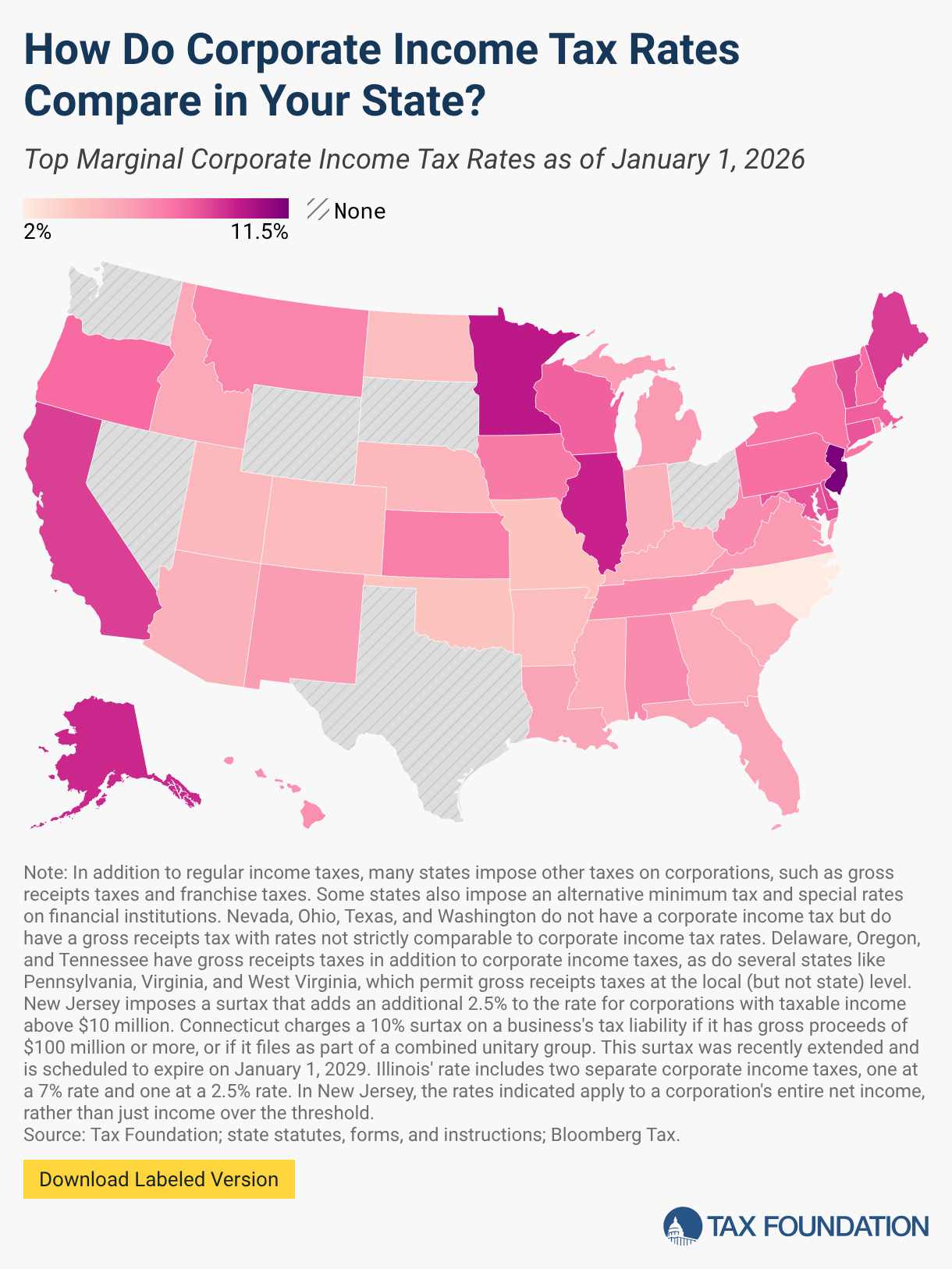

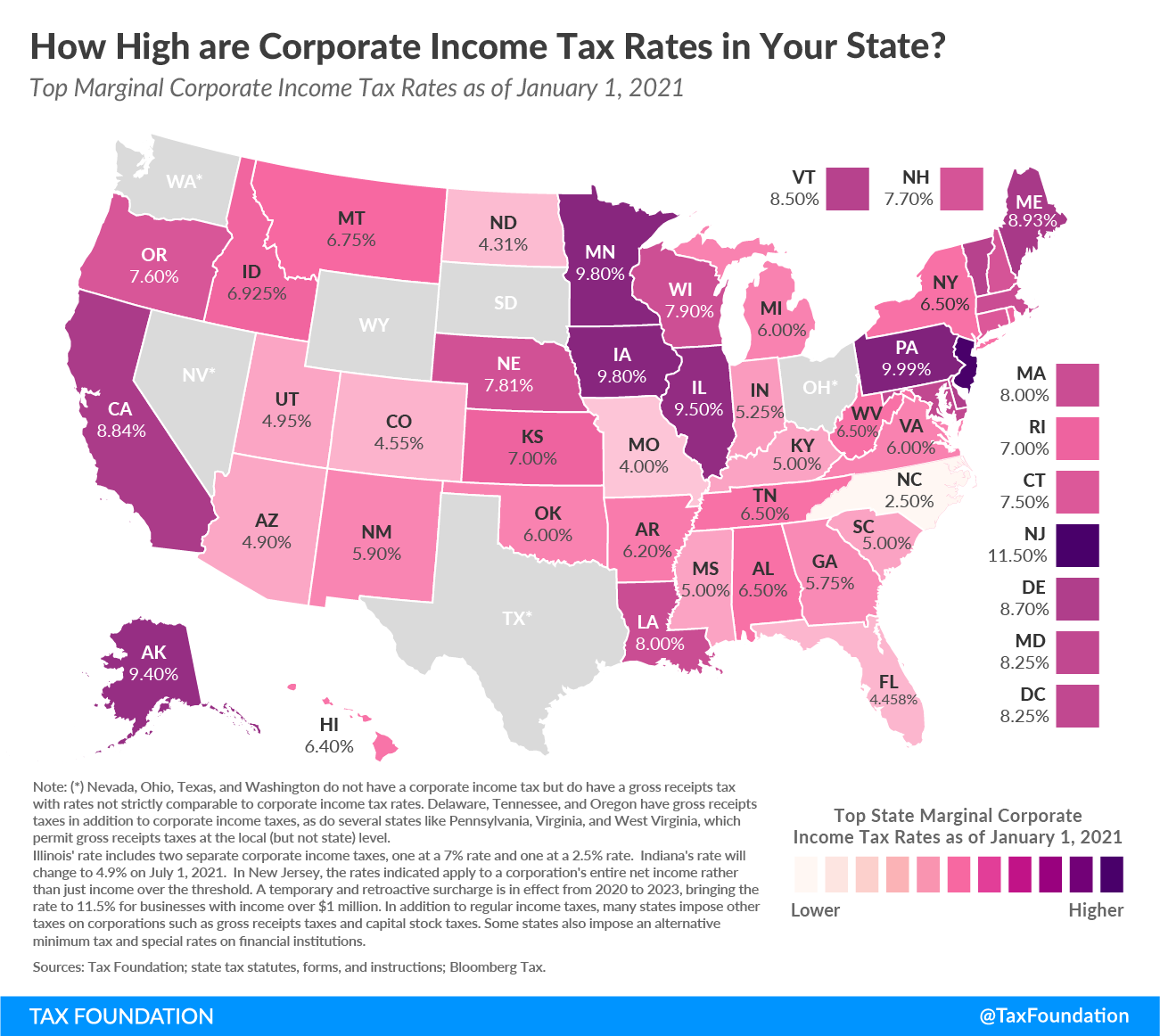

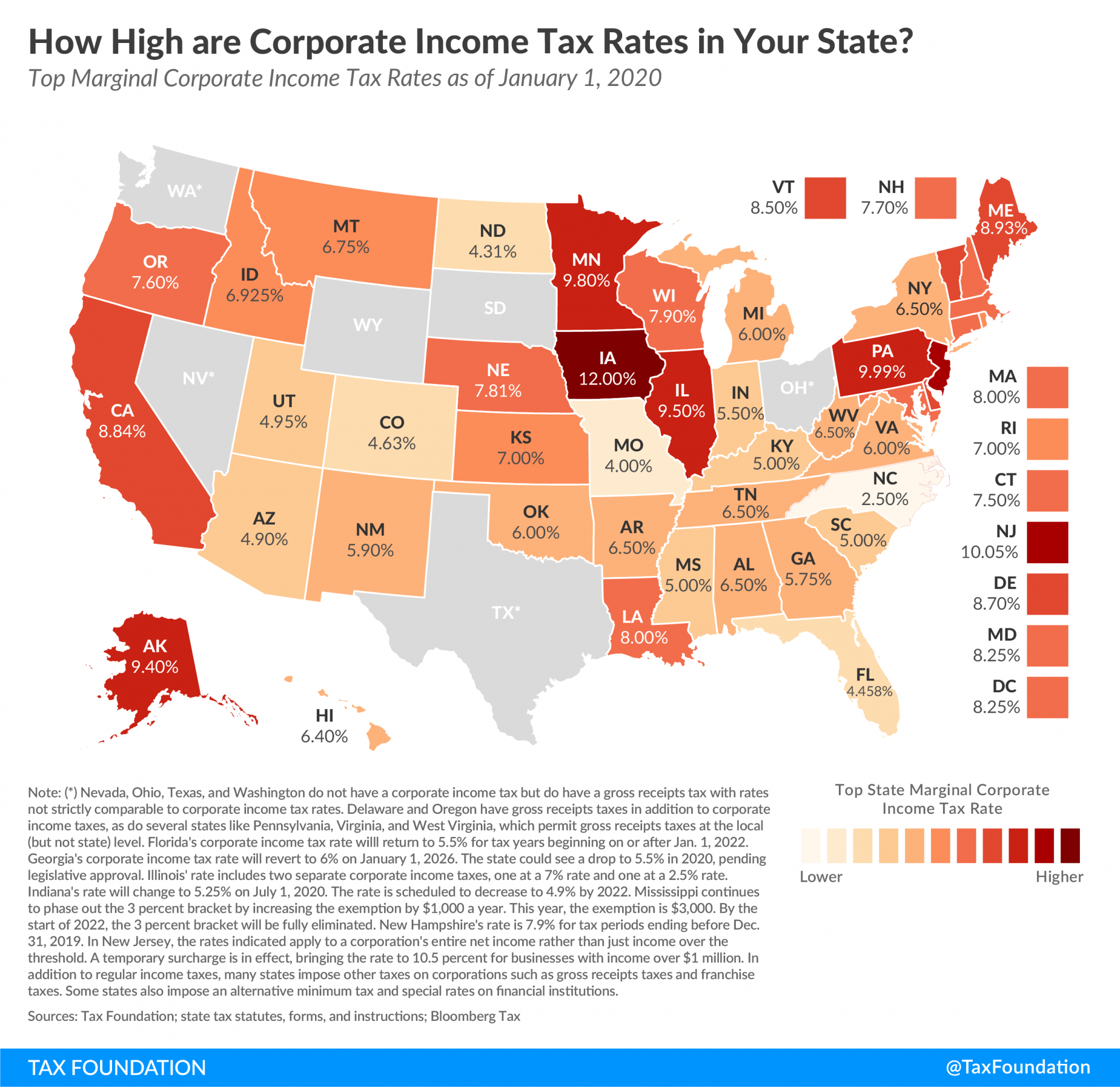

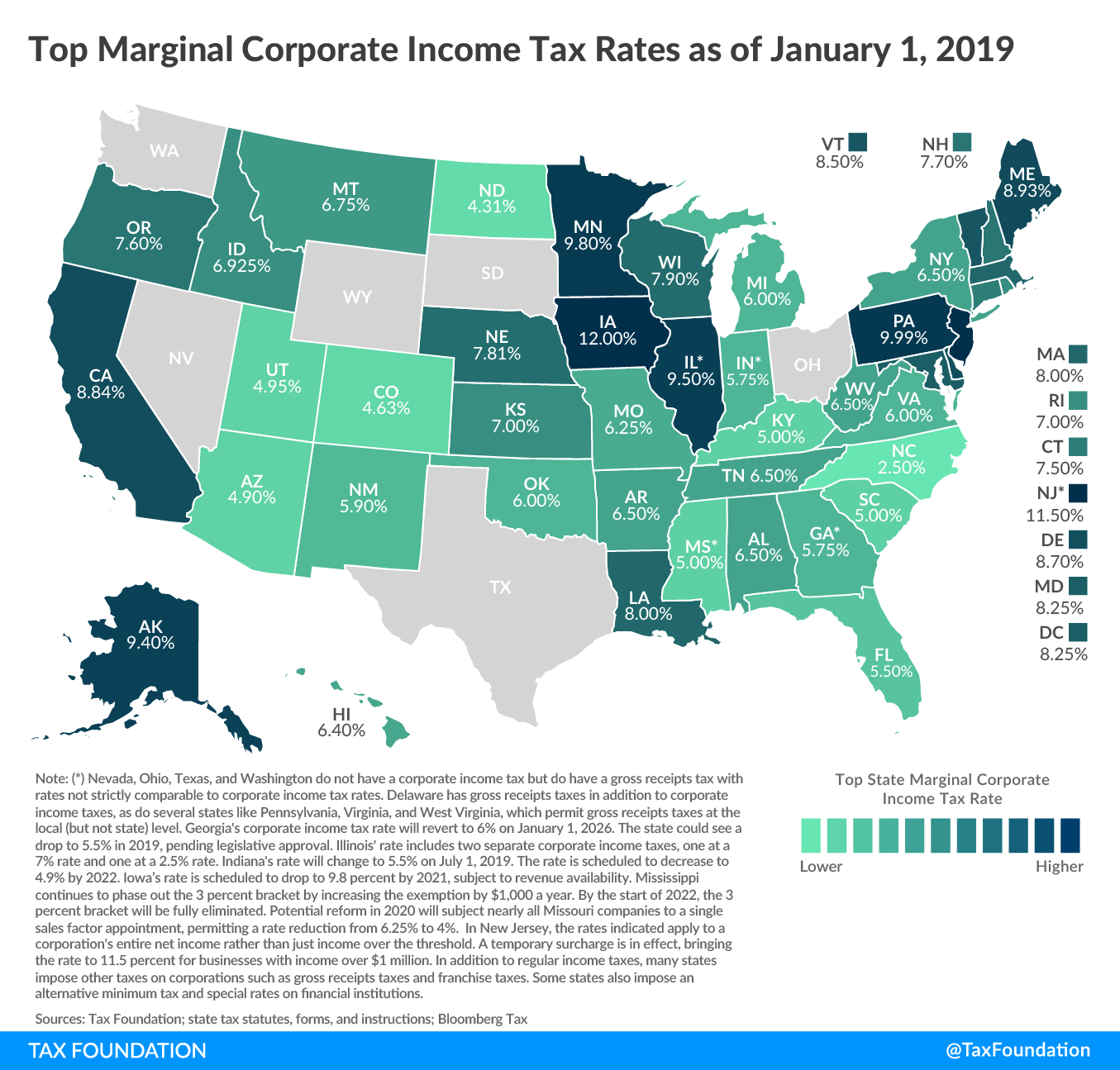

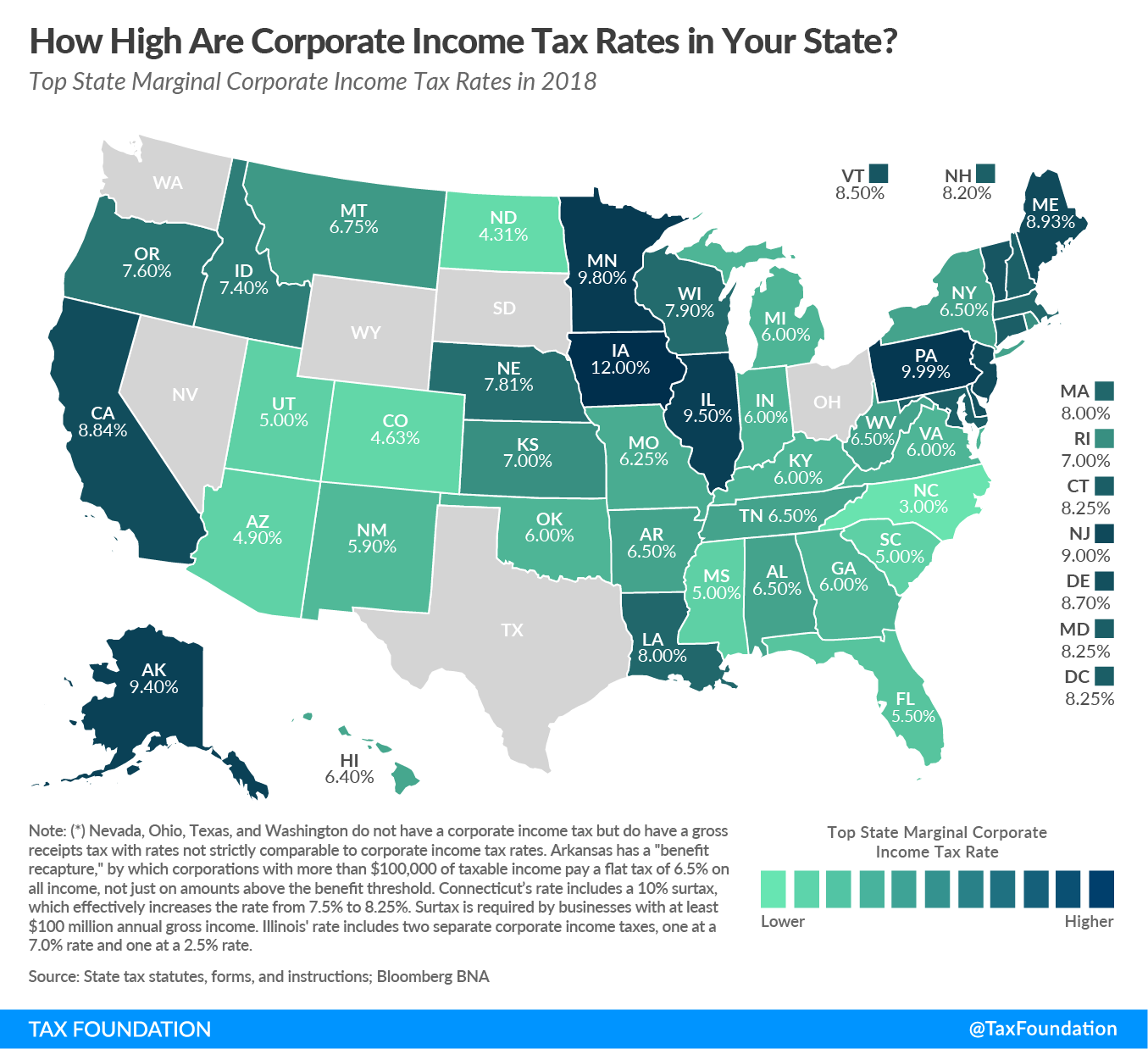

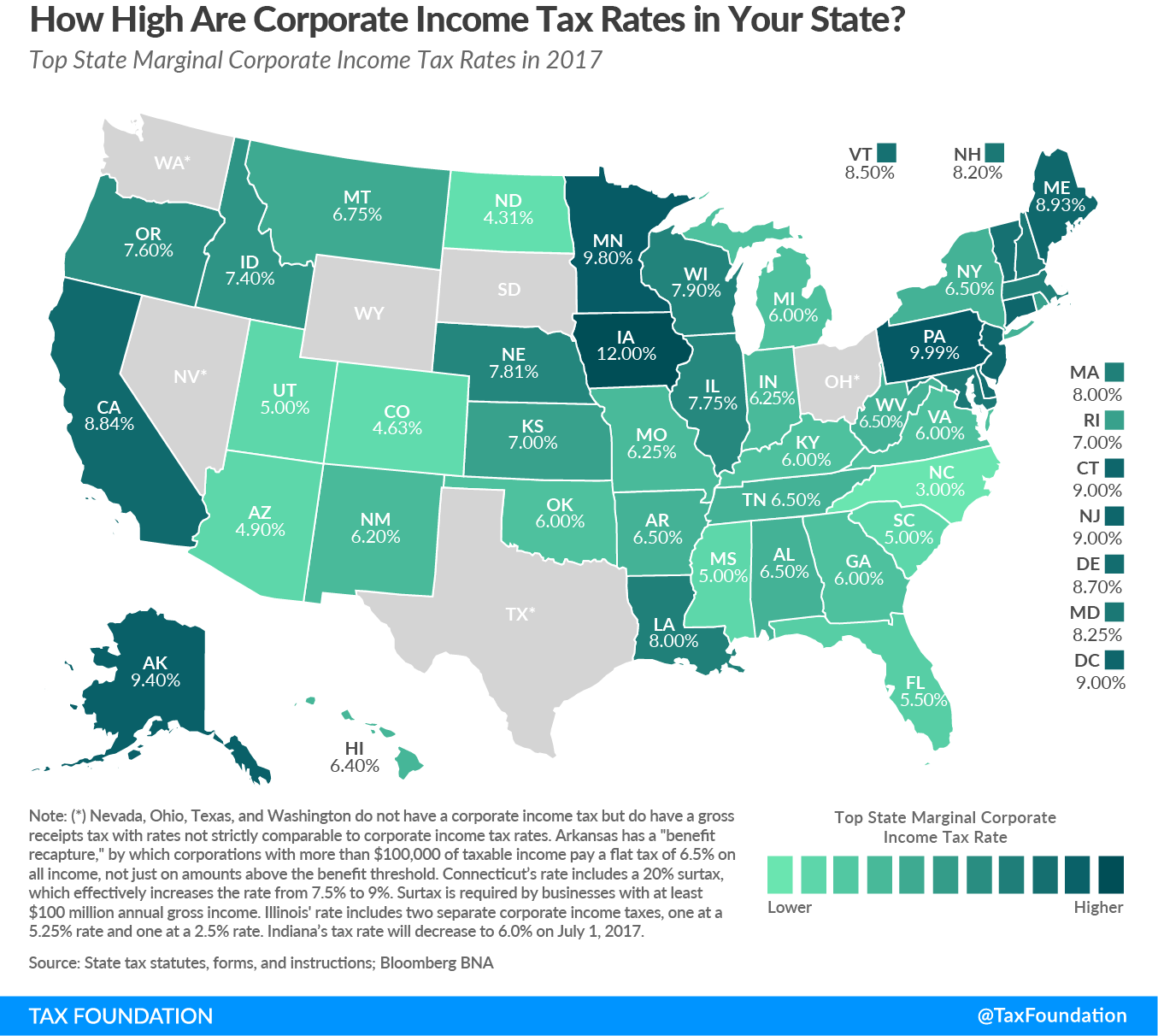

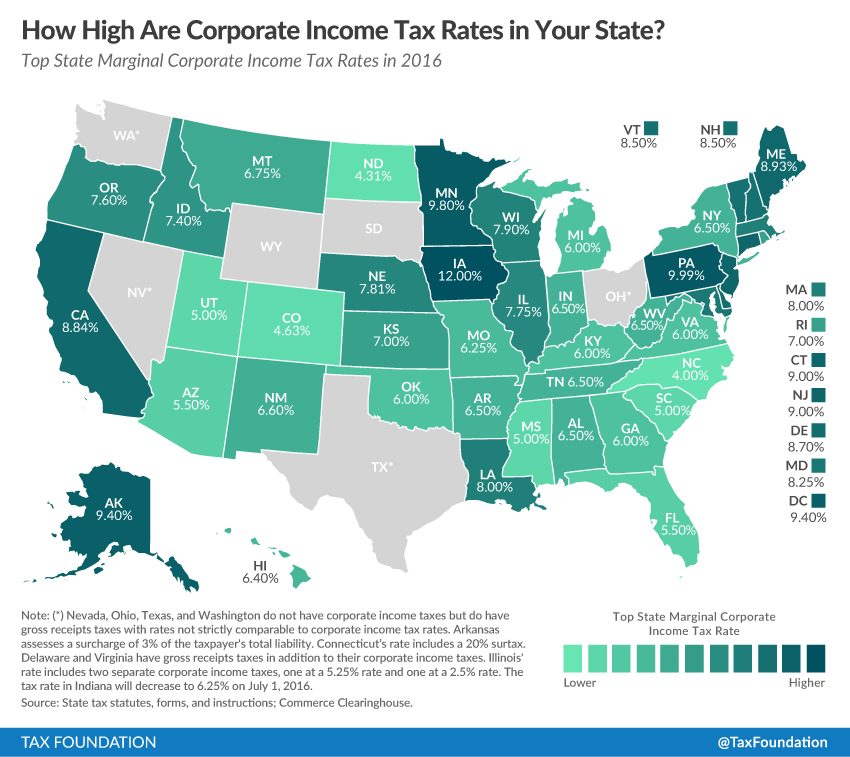

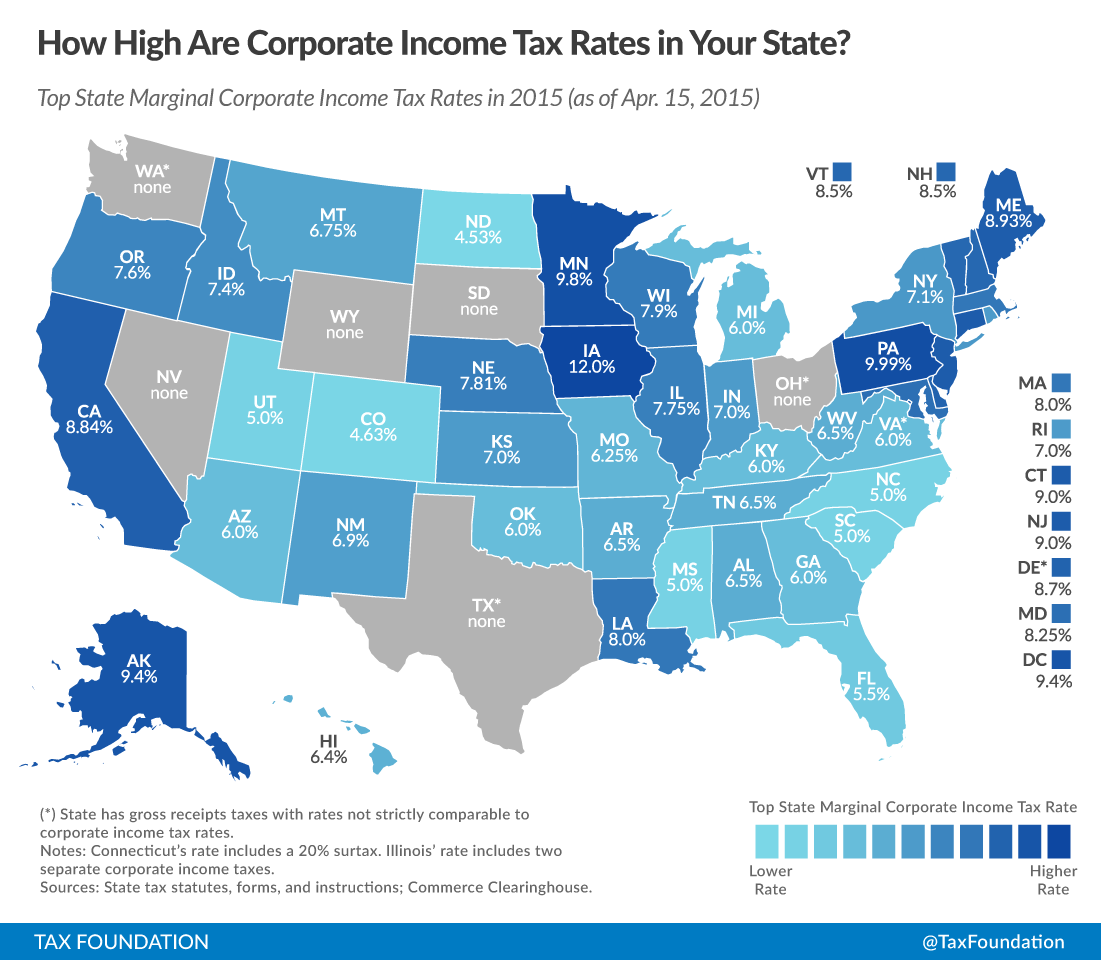

Forty-four states levy a corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.. Top rates range from a 2.0 percent flat rate in North Carolina to an 11.5 percent top marginal rate in New Jersey. Three states—Nebraska, North Carolina, and Pennsylvania—reduced their corporate income tax rates effective January 1, 2026, while no states increased their corporate income tax rates.

Among states that impose a corporate income tax, the average top marginal rate is approximately 6.57 percent, while the median top marginal rate is 6.5 percent.

Four states—Alaska, Illinois, Minnesota, and New Jersey—levy top marginal corporate income tax rates of 9 percent or higher. Maine (8.93 percent) and California (8.84 percent) are not far behind.

Thirteen states—Arizona, Arkansas, Colorado, Indiana, Kentucky, Mississippi, Missouri, North Carolina, North Dakota, Oklahoma, South Carolina, Nebraska, and Utah—have top rates at or below 5 percent.

Nevada, Ohio, Texas, and Washington impose gross receipts taxes instead of corporate income taxes. Delaware, Oregon, and Tennessee impose gross receipts taxes in addition to their corporate income taxes. Some localities in Pennsylvania, Virginia, and West Virginia likewise impose gross receipts taxes at the local, but not state, level. Gross receipts taxes are generally considered more economically harmful than corporate income taxes.

South Dakota and Wyoming are the only states that levy neither a corporate income tax nor a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding..

2026 State Corporate Income Tax Rates & Brackets

| State | Rates | Brackets | |

|---|---|---|---|

| Alabama | 6.50% | > | $0 |

| Alaska | 0.00% | > | $0 |

| Alaska | 2.00% | > | $25,000 |

| Alaska | 3.00% | > | $49,000 |

| Alaska | 4.00% | > | $74,000 |

| Alaska | 5.00% | > | $99,000 |

| Alaska | 6.00% | > | $124,000 |

| Alaska | 7.00% | > | $148,000 |

| Alaska | 8.00% | > | $173,000 |

| Alaska | 9.00% | > | $198,000 |

| Alaska | 9.40% | > | $222,000 |

| Arizona | 4.90% | > | $0 |

| Arkansas | 1.00% | > | $0 |

| Arkansas | 2.00% | > | $3,000 |

| Arkansas | 3.00% | > | $5,000 |

| Arkansas | 4.30% | > | $11,000 |

| California | 8.84% | > | $0 |

| Colorado (a) | 4.40% | > | $0 |

| Connecticut (b) | 7.50% | > | $0 |

| Connecticut (b) | 8.25% | > | $100,000,000 |

| Delaware (c) | 8.70% | > | $0 |

| Florida | 5.50% | > | $50,000 |

| Georgia | 5.19% | > | $0 |

| Hawaii | 4.40% | > | $0 |

| Hawaii | 5.40% | > | $25,000 |

| Hawaii | 6.40% | > | $100,000 |

| Idaho | 5.30% | > | $0 |

| Illinois (d) | 9.50% | > | $0 |

| Indiana | 4.90% | > | $0 |

| Iowa | 5.50% | > | $0 |

| Iowa | 7.10% | > | $100,000 |

| Kansas | 4.00% | > | $0 |

| Kansas | 7.00% | > | $50,000 |

| Kentucky | 5.00% | > | $0 |

| Louisiana | 5.50% | > | $0 |

| Maine | 3.50% | > | $0 |

| Maine | 7.93% | > | $350,000 |

| Maine | 8.33% | > | $1,050,000 |

| Maine | 8.93% | > | $3,500,000 |

| Maryland | 8.25% | > | $0 |

| Massachusetts | 8.00% | > | $0 |

| Michigan | 6.00% | > | $0 |

| Minnesota | 9.80% | > | $0 |

| Mississippi | 4.00% | > | $5,000 |

| Mississippi | 5.00% | > | $10,000 |

| Missouri | 4.00% | > | $0 |

| Montana | 6.75% | > | $0 |

| Nebraska | 4.55% | > | $0 |

| Nevada | (c) | ||

| New Hampshire | 7.50% | > | $0 |

| New Jersey (e) | 6.50% | > | $0 |

| New Jersey (e) | 7.50% | > | $50,000 |

| New Jersey (e) | 9.00% | > | $100,000 |

| New Jersey (e) | 11.50% | > | $10,000,000 |

| New Mexico | 5.90% | > | $0 |

| New York | 6.50% | > | $0 |

| New York | 7.25% | > | $5,000,000 |

| North Carolina | 2.00% | > | $0 |

| North Dakota | 1.41% | > | $0 |

| North Dakota | 3.55% | > | $25,000 |

| North Dakota | 4.31% | > | $50,000 |

| Ohio | (c) | ||

| Oklahoma | 4.00% | > | $0 |

| Oregon (c) | 6.60% | > | $0 |

| Oregon (c) | 7.60% | > | $1,000,000 |

| Pennsylvania | 7.49% | > | $0 |

| Rhode Island | 7.00% | > | $0 |

| South Carolina | 5.00% | > | $0 |

| South Dakota | None | ||

| Tennessee (c) | 6.50% | > | $0 |

| Texas | (c) | ||

| Utah | 4.50% | > | $0 |

| Vermont | 6.00% | > | $0 |

| Vermont | 7.00% | > | $10,000 |

| Vermont | 8.50% | > | $25,000 |

| Virginia | 6.00% | > | $0 |

| Washington | (c) | ||

| West Virginia | 6.50% | > | $0 |

| Wisconsin | 7.90% | > | $0 |

| Wyoming | None | ||

| Washington, D.C. | 8.25% | > | $0 |

(a) Colorado's 4.4% rate may be reduced midyear subject to revenue availability.

(b) Connecticut charges a 10% surtax on a business's tax liability if it has gross proceeds of $100 million or more, or if it files as part of a combined unitary group. This surtax was recently extended and is scheduled to expire on January 1, 2029.

(c) Nevada, Ohio, Texas, and Washington do not have a corporate income tax but do have a gross receipts tax with rates not strictly comparable to corporate income tax rates. Delaware, Oregon, and Tennessee have gross receipts taxes in addition to corporate income taxes, as do several states like Pennsylvania, Virginia, and West Virginia, which permit gross receipts taxes at the local (but not state) level.

(d) Illinois' rate includes two separate corporate income taxes, one at a 7% rate and one at a 2.5% rate.

(e) In New Jersey, the rates indicated apply to a corporation's entire net income rather than just income over the threshold.

In addition to regular income taxes, many states impose other taxes on corporations such as gross receipts taxes and capital stock taxes. Some states also impose an alternative minimum tax and special rates on financial institutions.

Source: Tax Foundation; state statutes, forms, and instructions; Bloomberg Tax.

Data compiled by Abir Mandal

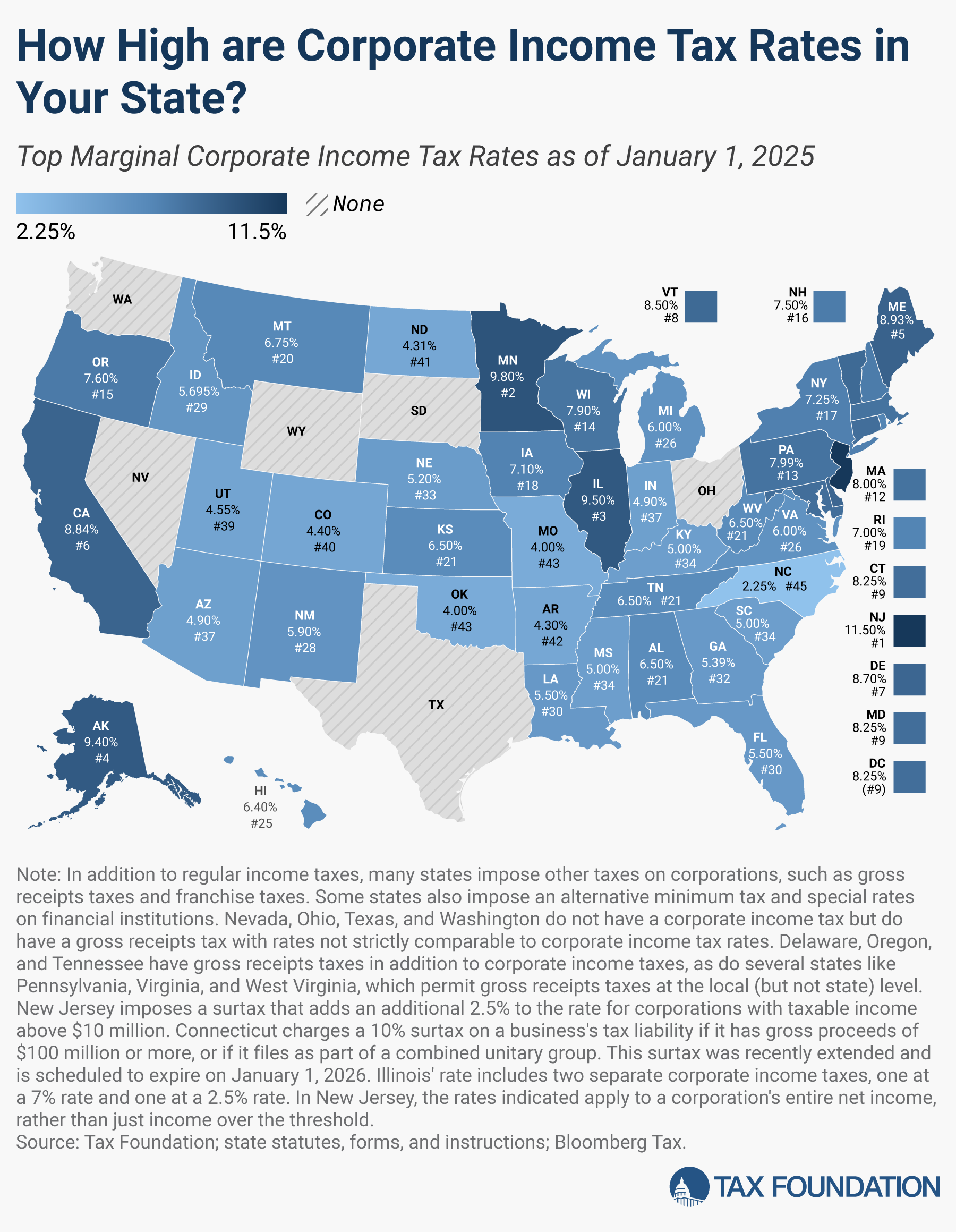

2025 State Corporate Income Tax Rates & Brackets

| State | Rates | Brackets | |

|---|---|---|---|

| Alabama | 6.50% | > | $0 |

| Alaska | 0.00% | > | $0 |

| Alaska | 2.00% | > | $25,000 |

| Alaska | 3.00% | > | $49,000 |

| Alaska | 4.00% | > | $74,000 |

| Alaska | 5.00% | > | $99,000 |

| Alaska | 6.00% | > | $124,000 |

| Alaska | 7.00% | > | $148,000 |

| Alaska | 8.00% | > | $173,000 |

| Alaska | 9.00% | > | $198,000 |

| Alaska | 9.40% | > | $222,000 |

| Arizona | 4.90% | > | $0 |

| Arkansas | 1.00% | > | $0 |

| Arkansas | 2.00% | > | $3,000 |

| Arkansas | 3.00% | > | $5,000 |

| Arkansas | 4.30% | > | $11,000 |

| California | 8.84% | > | $0 |

| Colorado (a) | 4.40% | > | $0 |

| Connecticut (b) | 7.50% | > | $0 |

| Connecticut (b) | 8.25% | > | $100,000,000 |

| Delaware (c) | 8.70% | > | $0 |

| Florida | 5.50% | > | $50,000 |

| Georgia (d) | 5.39% | > | $0 |

| Hawaii | 4.40% | > | $0 |

| Hawaii | 5.40% | > | $25,000 |

| Hawaii | 6.40% | > | $100,000 |

| Idaho | 5.695% | > | $0 |

| Illinois (e) | 9.50% | > | $0 |

| Indiana | 4.90% | > | $0 |

| Iowa | 5.50% | > | $0 |

| Iowa | 7.10% | > | $100,000 |

| Kansas | 3.50% | > | $0 |

| Kansas | 6.50% | > | $50,000 |

| Kentucky | 5.00% | > | $0 |

| Louisiana | 5.50% | > | $0 |

| Maine | 3.50% | > | $0 |

| Maine | 7.93% | > | $350,000 |

| Maine | 8.33% | > | $1,050,000 |

| Maine | 8.93% | > | $3,500,000 |

| Maryland | 8.25% | > | $0 |

| Massachusetts | 8.00% | > | $0 |

| Michigan | 6.00% | > | $0 |

| Minnesota | 9.80% | > | $0 |

| Mississippi | 4.00% | > | $5,000 |

| Mississippi | 5.00% | > | $10,000 |

| Missouri | 4.00% | > | $0 |

| Montana | 6.75% | > | $0 |

| Nebraska | 5.20% | > | $0 |

| Nevada | (c) | ||

| New Hampshire | 7.50% | > | $0 |

| New Jersey (f) | 6.50% | > | $0 |

| New Jersey (f) | 7.50% | > | $50,000 |

| New Jersey (f) | 9.00% | > | $100,000 |

| New Jersey (f) | 11.5% | > | $10,000,000 |

| New Mexico | 5.90% | > | $0 |

| New York | 6.50% | > | $0 |

| New York | 7.25% | > | $5,000,000 |

| North Carolina | 2.25% | > | $0 |

| North Dakota | 1.41% | > | $0 |

| North Dakota | 3.55% | > | $25,000 |

| North Dakota | 4.31% | > | $50,000 |

| Ohio | (c) | ||

| Oklahoma | 4.00% | > | $0 |

| Oregon (c) | 6.60% | > | $0 |

| Oregon (c) | 7.60% | > | $1,000,000 |

| Pennsylvania | 7.99% | > | $0 |

| Rhode Island | 7.00% | > | $0 |

| South Carolina | 5.00% | > | $0 |

| South Dakota | None | ||

| Tennessee (c) | 6.50% | > | $0 |

| Texas | (c) | ||

| Utah | 4.55% | > | $0 |

| Vermont | 6.00% | > | $0 |

| Vermont | 7.00% | > | $10,000 |

| Vermont | 8.50% | > | $25,000 |

| Virginia | 6.00% | > | $0 |

| Washington | (c) | ||

| West Virginia | 6.50% | > | $0 |

| Wisconsin | 7.90% | > | $0 |

| Wyoming | None | ||

| Washington, D.C. | 8.25% | > | $0 |

(a) Colorado's 4.4% rate may be reduced midyear subject to revenue availability.

(b) Connecticut charges a 10% surtax on a business's tax liability if it has gross proceeds of $100 million or more, or if it files as part of a combined unitary group. This surtax was recently extended and is scheduled to expire on January 1, 2026.

(c) Nevada, Ohio, Texas, and Washington do not have a corporate income tax but do have a gross receipts tax with rates not strictly comparable to corporate income tax rates. Delaware, Oregon, and Tennessee have gross receipts taxes in addition to corporate income taxes, as do several states like Pennsylvania, Virginia, and West Virginia, which permit gross receipts taxes at the local (but not state) level.

(d) Georgia's corporate income tax rate is scheduled to revert to 6% on January 1, 2026.

(e) Illinois' rate includes two separate corporate income taxes, one at a 7% rate and one at a 2.5% rate.

(f) In New Jersey, the rates indicated apply to a corporation's entire net income rather than just income over the threshold.

In addition to regular income taxes, many states impose other taxes on corporations such as gross receipts taxes and capital stock taxes. Some states also impose an alternative minimum tax and special rates on financial institutions.

Sources: Tax Foundation; state tax statutes, forms, and instructions; Bloomberg Tax.

Data compiled by Abir Mandal

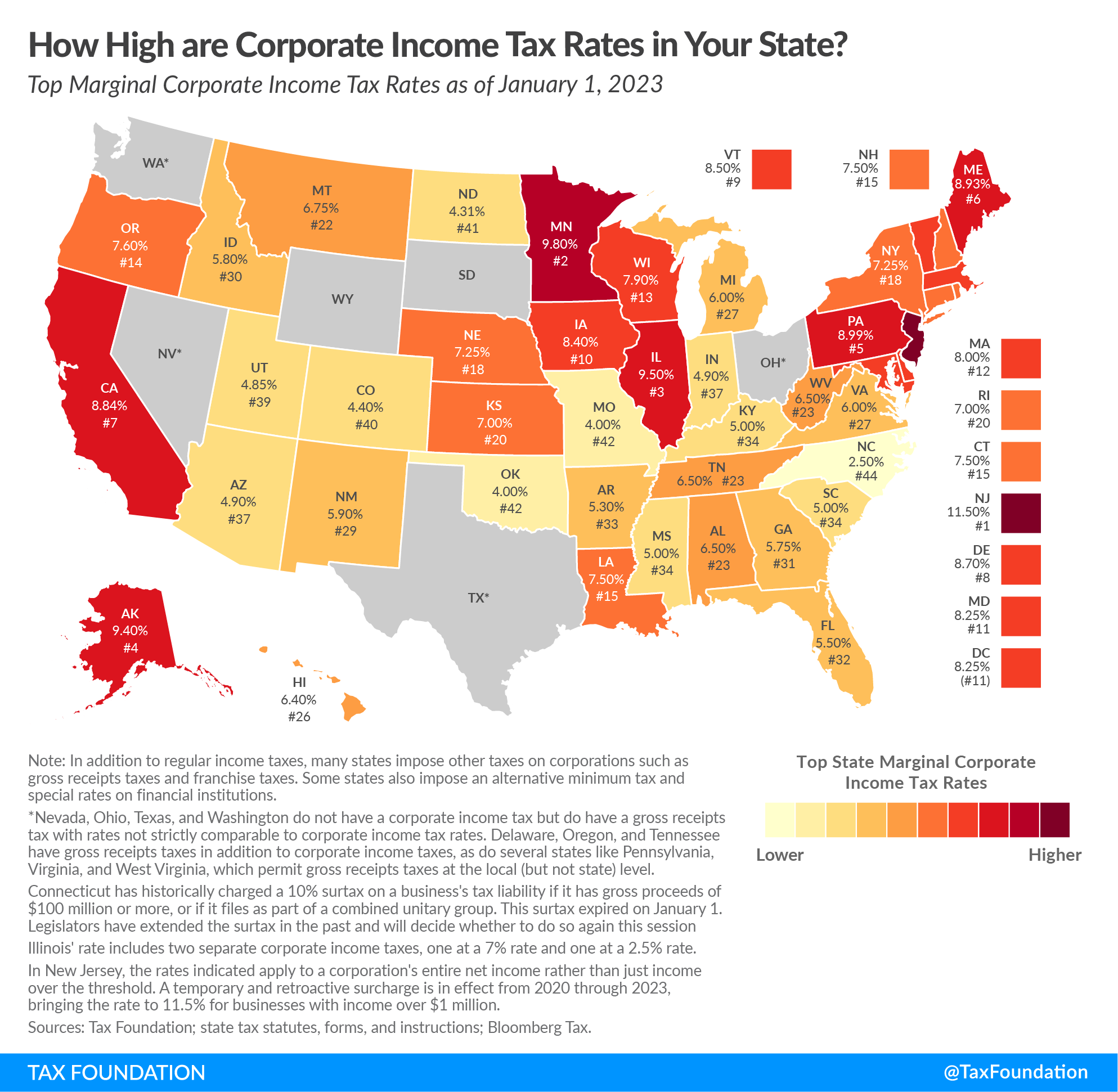

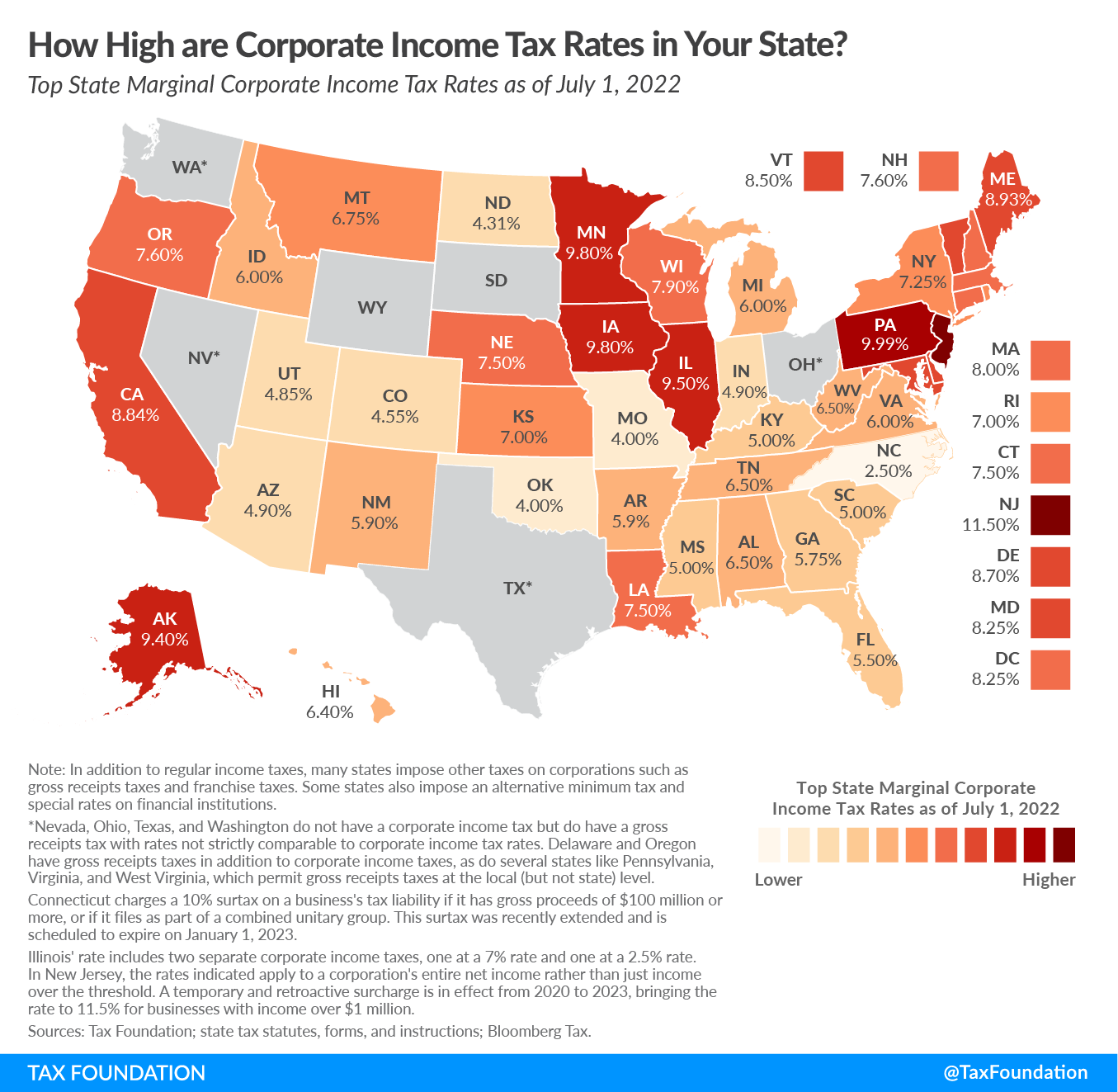

Notable State Corporate Income Tax Changes for 2026

Nebraska

Nebraska lowered its flat corporate income tax rate to 4.55 percent, down from 5.2 percent. This rate will be reduced to 3.99 percent for taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. years beginning on or after January 1, 2027, subject to revenue availability.

North Carolina

In 2021, North Carolina enacted legislation that would eliminate the corporate income tax by 2030, with gradual phasedowns occurring over several years. In 2025, the flat corporate income tax rate was 2.25 percent. In 2026, the rate was reduced to 2 percent.

Pennsylvania

In 2021, Pennsylvania lawmakers enacted HB 1342, a multi-year phasedown of the corporate net income tax rate. Beginning in tax year 2023, the law reduced Pennsylvania’s corporate net income tax rate from 9.99 percent to 8.99 percent, with additional 0.5 percentage point reductions scheduled for each year until 2031, when the rate is scheduled to reach 4.99 percent. Consequently, for 2026, corporations will face a flat 7.49 percent income tax in Pennsylvania, down from 7.99 percent in 2025.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeErrata: A previous edition of this post mistakenly referenced a corporate income tax rate reduction in Georgia, but a rate reduction was not triggered for 2026. It has been corrected.