Today’s taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. map focuses on one of the guardrails implemented under the 2017 Tax Cuts and Jobs Act (TCJA) to prevent corporate tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. erosion and foreign profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens. by US corporations. Global intangible low-taxed income (GILTI) is a category of foreign income taxed by the federal government but at a rate lower than the US corporate income tax rate. GILTI was designed as a proxy for the profits of US multinationals from foreign-held intangible assets, including patents, software, trademarks, copyrights, and other forms of IP held by their foreign subsidiaries.

Crucially, it is only a proxy; it does not directly tax income derived from intangibles but instead taxes high rates of return, which the law’s drafters associated with royalty income from intangible assets. Similarly, the determination of whether such income is only subject to low foreign taxes—a possible sign of profit-shifting—is complex and does not always align with genuinely low foreign tax burdens.

GILTI is meant to ensure that, regardless of where a US company does business in the world, its foreign subsidiaries pay at least a minimum rate of income tax, if not to other countries, then to the United States. When a US company’s controlled foreign corporations (CFCs) owe less than the specified minimum rate to other countries, then they owe taxes on GILTI as a form of “top-up tax” to the US.

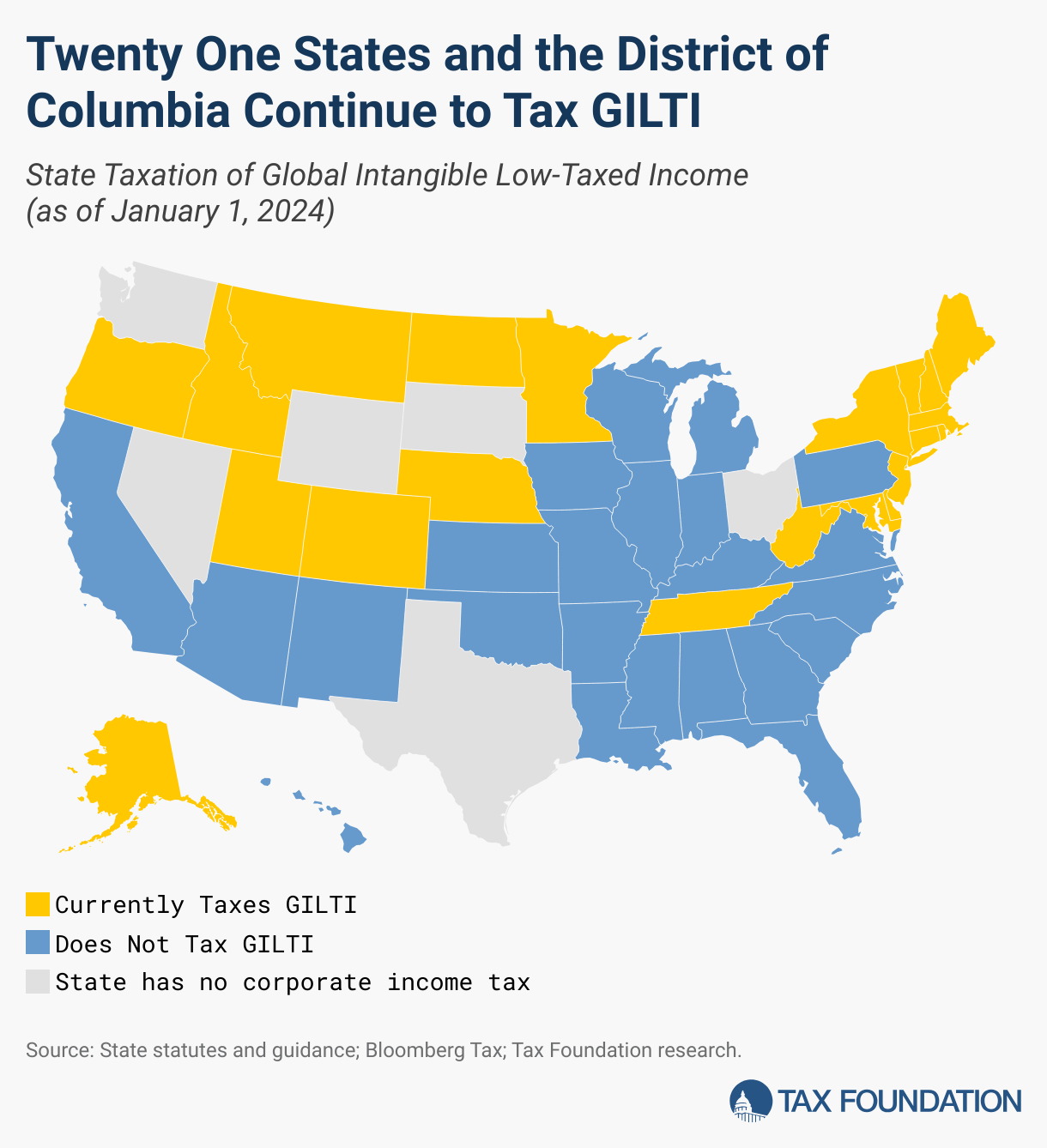

21 States and DC Continue to Tax GILTI

State Taxation of Global Intangible Low-Taxed Income (as of October 1, 2024)

| State | GILTI State Taxation |

|---|---|

| Alabama | 0% |

| Alaska | 20% |

| Arizona | 0% |

| Arkansas | 0% |

| California | 0% |

| Colorado | 50% |

| Connecticut | 5% |

| Delaware | 50% |

| District Of Columbia | 50% |

| Florida | 0% |

| Georgia | 0% |

| Hawaii | 0% |

| Idaho | 15% |

| Illinois | 0% |

| Indiana | 0% |

| Iowa | 0% |

| Kansas | 0% |

| Kentucky | 0% |

| Louisiana | 0% |

| Maine | 50% |

| Maryland | 50% |

| Massachusetts | 5% |

| Michigan | 0% |

| Minnesota | 50% |

| Mississippi | 0% |

| Missouri | 0% |

| Montana | 20% |

| Nebraska | 50% |

| Nevada | State has no corporate income tax |

| New Hampshire | 50% |

| New Jersey | 5% |

| New Mexico | 0% |

| New York | 5% |

| North Carolina | 0% |

| North Dakota | 30% |

| Ohio | State has no corporate income tax |

| Oklahoma | 0% |

| Oregon | 20% |

| Pennsylvania | 0% |

| Rhode Island | 50% |

| South Carolina | 0% |

| South Dakota | State has no corporate income tax |

| Tennessee | 5% |

| Texas | State has no corporate income tax |

| Utah | 50% |

| Vermont | 50% |

| Virginia | 0% |

| Washington | State has no corporate income tax |

| West Virginia | 50% |

| Wisconsin | 0% |

| Wyoming | State has no corporate income tax |

Recent Changes to State GILTI Tax Base Treatment

States’ treatment of GILTI has not changed significantly in recent years. Since our last map update on May 20, 2021, only two states, New Jersey and Minnesota, amended their state tax codes or provided supplementary regulatory guidance that invokes GILTI tax base changes:

- New Jersey decreased its GILTI tax base from 50 percent to 5 percent by asserting that GILTI was classified as a deemed dividend. The Garden State’s Dividend Received Deduction allows corporations to deduct as much as 100 percent of dividends and deemed dividends from state corporate taxation, except that, in the case of GILTI, a 5 percent inclusion is added back.

- Minnesota passed F. 1938 in 2023, which repealed the 100 percent subtraction of GILTI income that previously allowed Minnesota corporations to exclude GILTI from their Minnesota state corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. burdens. Minnesota now taxes 50 percent of GILTI, effective tax year 2023 onward.

Concerns Surrounding GILTI in State Tax Codes

The inclusion of GILTI in state corporate tax codes has sparked significant debate. GILTI was introduced to target multinational corporations (MNCs) with operations in low-tax jurisdictions by ensuring that US companies pay a minimum level of tax on foreign profits, with the specific goal of addressing profit shifting—i.e., when companies locate valuable intellectual property in low-tax jurisdictions abroad and allocate royalty revenue to those foreign subsidiaries. However, allowing states to incorporate GILTI into their corporate tax regimes raises several concerns, including possible violations of the Dormant Commerce Clause, the undue complexity imposed on MNCs’ tax filings, and the artificial inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. of tax liabilities due to inconsistent apportionmentApportionment is the determination of the percentage of a business’ profits subject to a given jurisdiction’s corporate income or other business taxes. U.S. states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. rules when states include GILTI in their apportionment formulas. These issues not only strain compliance efforts but also create disparities between states, ultimately complicating the business environment for MNCs and consumers who could be adversely affected when firms pass the cost of GILTI tax compliance onto their goods and services in the form of higher prices.

The Dormant Commerce Clause of the US Constitution restricts states from enacting legislation that discriminates against or unduly burdens interstate commerce. Thus far, states’ GILTI policies have not been successfully challenged on these grounds, but there is a good argument to be made that these laws run afoul of the Constitution for several reasons.

First, states taxing GILTI effectively impose a higher tax on foreign income than on domestic income, which directly affects interstate and international business activities. MNCs that earn profits in foreign countries must grapple with a patchwork of state-level tax regulations that impose an inconsistent burden on their global income. Some states allow total offsets or subtractions. Minnesota recently passed SF 1938, which repealed the state’s 100 percent subtraction of GILTI and imposed a tax on 50 percent of all MNCs’ foreign GILTI. This taxation of foreign income disproportionately affects companies headquartered in states that have adopted GILTI, forcing them to pay additional taxes that may not be levied on US-domiciled businesses. Notably, it also makes states’ corporate income tax rates far more relevant to US-based businesses—and Minnesota has a particularly high rate. Second, the inclusion of GILTI at the state level leads to double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. . When taxed at the state level, GILTI lacks the adjustments present at the federal level, such as foreign tax credits or deductions. This duplication of tax liability unfairly penalizes MNCs and could be interpreted as a violation of the prohibition on discriminatory taxation against interstate or international commerce.

State-level inclusion of GILTI adds significant complexity to the already challenging tax compliance landscape for MNCs. Each state operates its own unique corporate tax regime, and differences in how states apply GILTI further exacerbate the compliance burden.

The lack of uniformity in state tax codes means that MNCs must navigate a maze of different filing requirements, apportionment formulas, and rules regarding the inclusion or exclusion of GILTI in taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income. . Some states conform to the federal treatment of GILTI, while others partially or fully decouple from federal rules. This fragmentation forces MNCs to allocate considerable resources toward understanding and complying with each state’s specific requirements, adding layers of complexity to their tax filings.

Furthermore, the inclusion of GILTI often requires sophisticated and costly tax planning strategies to mitigate the risk of overpayment or penalties. Multinational businesses must continuously track state-level tax law changes to adjust their tax reporting processes, which can be resource-intensive and prone to error. Small to mid-sized MNCs, in particular, may lack the internal resources to cope with these complexities, making them more susceptible to tax compliance risks. In contrast, large corporations with greater resources may leverage complex tax avoidance strategies, creating an uneven playing field.

Perhaps one of the most significant effects of including GILTI in state tax codes is the artificial inflation of corporate tax liabilities for MNCs. GILTI was designed as a federal anti-base erosion measure, targeting income that would otherwise escape US taxation. However, when states tax GILTI, it often results in an overreach of their taxing authority, particularly given the use of inflexible apportionment formulas that fail to accurately reflect where economic activity occurs.

States use apportionment formulas to allocate income to the state based on factors such as property, payroll, and sales. These formulas were not designed with GILTI in mind, and as a result, they often fail to appropriately apportion foreign income to the states in a fair and consistent manner. For example, a state might tax GILTI as if it were purely domestic income, even though the income is derived from the economic activity associated with a company’s controlled foreign corporations. This creates a disconnect between the location of the income generation and the state’s claim to tax it.

States that tax GILTI increase filing complexity, drive up the cost of tax compliance, and introduce unnecessary economic uncertainty and legal risk. The following 21 states and the District of Columbia continue to tax GILTI despite these challenges.