Table of Contents

- Key Findings

- Introduction

- A Brief Overview of GILTI

- Calculating GILTI Tax Liability

- State Taxation of GILTI Is Complex and Uncompetitive

- State Taxation of GILTI Raises Constitutional Issues

- Current Status of States’ Taxation of GILTI

- The Impact on States of the Biden Administration’s Proposed Federal Changes to GILTI

- A Brief Overview of FDII

- Current State Treatment of the FDII Deduction and the Impact of the Biden Administration’s Proposed Changes

- Recent Changes in States’ Tax Treatment of GILTI and FDII

- State Legislative Proposals Related to GILTI

- Conclusion

Launch Resource Center: U.S. International Tax Reform

Key Findings

- Twenty states and the District of Columbia tax some portion of Global Intangible Low-Taxed Income (GILTI), although only 16 of those states have issued guidance on the matter more than three years after the federal law went into effect.

- States that have not yet issued guidance on their treatment of GILTI should act quickly to provide clarity to taxpayers, and states that currently tax GILTI should exclude it from their tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates..

- As part of the American Jobs Plan Act, President Joe Biden has proposed several major changes to GILTI, including reducing the value of the § 250 deduction, eliminating the 10 percent exemption for deemed returns to Qualified Business Asset Investment (QBAI), and taxing GILTI on a country-by-country basis.

- If the proposed federal changes to GILTI are adopted, more U.S. companies will be exposed to taxes on GILTI, and more income will be taxed as GILTI by the federal government and by states.

- Several states have legislation pending this year that would change their tax treatment of GILTI. In California, Illinois, and Minnesota, proposals are circulating to tax GILTI for the first time, while a Massachusetts bill would tax GILTI to a much greater degree. Alabama, Iowa, and Kansas exempted GILTI from taxation over the past year, while Nebraska policymakers considered but did not adopt such legislation.

- Twenty-two states conform to the federal deduction for Foreign-Derived Intangible Income (FDII), which would be eliminated under the Biden proposal.

Introduction

Unless states act, tax changes proposed by the Biden administration will increase the amount of foreign income taxed in some states, undermining their competitive standing and imposing a tax increase that was never agreed upon by state lawmakers. A provision of the Tax Cuts and Jobs Act (TCJA) of 2017 which was part of a shift to quasi-territorial taxation at the federal level had the opposite effect in some states, and President Joe Biden’s American Jobs Plan Act would further increase state taxation of activity that historically fell outside states’ purview.

While the TCJA represented a broader shift of the U.S. government away from taxing income earned outside the U.S., certain anti-base erosion guardrails were put in place, including Global Intangible Low-Taxed Income (GILTI), to return some foreign income to the U.S. tax base under certain circumstances. At the same time, the TCJA also created an incentive for situating intangible assets in the U.S., the deduction for Foreign-Derived Intangible Income (FDII).

GILTI was designed to deter companies from parking their intangible assets in low-tax countries, while FDII was designed to encourage domestic investment in intangible assets. In both cases, they were adjustments to a new regime which, overall, had shifted away from worldwide taxation. When GILTI and FDII were created, however, many states automatically brought these provisions into their own tax bases due to the way in which states conform with the federal tax code, even though states had historically taxed very little foreign income, turning GILTI from a guardrail at the federal level into an expansion of the tax base at the state level. There is little justification for states to bring international income into their tax bases.

State taxation of GILTI increases tax burdens on U.S. multinationals for reasons having nothing to do with their activities in the state. States were never intended to tax international income, and doing so raises serious constitutional issues in many states. State taxation of GILTI is unconventional and economically uncompetitive and will become even more so if the federal government adopts a more aggressive approach to taxing GILTI, as outlined in the American Jobs Plan Act. Under the Biden administration’s proposal, the definition of GILTI would be expanded while a deduction would be reduced, both of which would flow through to some states.

Just as many states conform to the federal treatment of GILTI, many likewise remain conformed to the FDII deduction, which would be eliminated under the federal proposal. Continued conformity on both provisions would lead, simultaneously, to greater taxation of GILTI while eliminating the benefit of FDII. This paper shows how states currently tax GILTI and FDII and how they would be impacted by President Biden’s proposed federal tax changes. It also provides an overview of recent and pending state legislative actions related to GILTI.

A Brief Overview of GILTI

Prior to the TCJA, the U.S. corporate income tax applied to a resident corporation’s entire worldwide income but provided credits for taxes paid to other countries. With enactment of the TCJA in 2017, however, the U.S. shifted to a quasi-territorial system of taxation, whereby the U.S. government largely retreated from taxing foreign income, with the exception of certain anti-base erosion provisions that were put in place to discourage profit shifting and the offshoring of intellectual property (IP) into low-tax countries.

One of those guardrails is GILTI, a distinct category of foreign income that is taxed by the U.S. government but at a rate lower than the U.S. corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate. Established by the TCJA in § 951A of the Internal Revenue Code (IRC), GILTI was designed as a proxy for the profits of U.S. multinationals from foreign-held intangible assets, including patents, software, trademarks, copyrights, and other forms of IP held by their foreign subsidiaries. Crucially, it is only a proxy: it does not directly tax income derived from intangibles but instead taxes high rates of return, which the law’s drafters associated with royalty income from intangible assets. Similarly, the determination of whether such income is only subject to low foreign taxes—a possible sign of profit-shifting—is complex and does not always align with actually low foreign tax burdens.

In essence, GILTI is a new category of foreign income of U.S. multinational companies from which a minimum tax is collected and sent to the U.S. Treasury, despite the TCJA’s broader shift away from taxing international income. GILTI is meant to ensure that, regardless of where a U.S. company does business in the world, its foreign subsidiaries pay at least a minimum rate of income tax, if not to other countries, then to the United States. When a U.S. company’s controlled foreign corporations (CFCs) owe less than the specified minimum rate to other countries, then they owe taxes on GILTI as a form of “top-up tax” to the U.S.[1]

Calculating GILTI Tax Liability

The GILTI calculation is highly complex, but in its simplest form, GILTI is calculated by taking 10 percent of a CFC’s qualified business asset investment (QBAI)—or investments in machinery, equipment, and buildings—and subtracting interest expenses. That amount is then subtracted from the company’s “net tested income,” or the net income of the U.S. company’s foreign affiliates. Any profits exceeding that amount are deemed “supernormal returns.” (It is important to note that, under current law, the net tested income of all CFCs is blended together when calculating GILTI liability, rather than the income and tax liability of each CFC being calculated separately or on a country-by-country basis.)

The justification for the GILTI formula is that, over time, earnings attributable to investments in tangible property do not often exceed 10 percent of the depreciable value of the assets used to produce said earnings. This formula therefore assumes that if a CFC has foreign profits exceeding 10 percent of QBAI less interest expenses, those profits are more likely attributable to investments in intangible rather than tangible assets. (This, however, is not always the case, so the GILTI formula is a rough approximation at best.)

After supernormal returns are calculated, the amount of GILTI that is subject to taxation by the U.S. government is calculated by first applying a deduction (the § 250 deduction) designed to tax GILTI at a lower rate than U.S.-sourced income, as well as a credit for foreign taxes paid, known as the foreign tax credit (FTC).

The § 250 deduction—named after the section of the tax code in which it is located—excludes 50 percent of a company’s GILTI from taxation each year through 2025. This deduction is set to become less generous beginning in 2026, when it will exclude only 37.5 percent of GILTI from the U.S. corporate income tax base. As such, under the current U.S. corporate income tax rate of 21 percent, the 50 percent deduction yields an effective rate on GILTI of 10.5 percent. Absent further changes to current law, when the deduction drops to 37.5 percent starting in 2026, the effective rate on GILTI will increase to 13.125 percent, since 62.5 percent of a company’s foreign supernormal returns will be taxed at the current 21 percent corporate income tax rate.

After the § 250 deduction is applied, a credit for foreign taxes paid is granted, offsetting up to 80 percent of the company’s non-U.S. income tax liability. The value of the credit is limited to U.S. tax liability multiplied by the company’s foreign profits divided by its worldwide profits, a formula which can sometimes generate taxable GILTI income even when the foreign income in question is subject to high tax rates abroad. In general, however, the higher a company’s foreign tax liability is, the lower its residual U.S. liability will be.

When acting as intended, GILTI prevents base erosion by collecting a minimum tax on foreign profits held in low-tax jurisdictions. It is important to note, however, that there are many cases in which GILTI’s reach extends far beyond its intent, acting as an added layer of U.S. taxes on top of the taxes CFCs pay abroad, even when those earnings are not attributable to intangible assets in low-tax jurisdictions.[2]

For example, some U.S. multinational companies have significant domestic research or interest expenses, and current U.S. FTC expense allocation rules typically require the attribution of some of a company’s domestic expenses to its foreign income. This can limit the amount of FTCs available to the company and increase its GILTI liability.[3] This unintended consequence of current FTC expense allocation rules is just one example of how some U.S. multinational companies have supernormal returns—and therefore owe taxes on GILTI—even if those so-called supernormal returns have nothing to do with the offshoring of intellectual property.

State Taxation of GILTI Is Complex and Uncompetitive

After the TCJA was enacted, many states automatically included GILTI in their tax base due to the way in which corporate tax codes conform with the IRC. In general, states that conform to a post-TCJA version of the IRC can be assumed to include GILTI in their tax base unless the state has expressly decoupled from GILTI or determined that GILTI constitutes foreign dividend income subject to a 100 percent dividends received deduction (DRD). (Often, even where GILTI is treated as foreign dividend income, state DRDs are less than 100 percent.)

Some states conform to the federal corporate tax code before credits or deductions (line 28 of Form 1120), which implies inclusion of GILTI under § 951A without the § 250 deduction. The § 250 deduction is structurally necessary to produce the lower rate which is intended to be imposed on GILTI, since it is structured as a minimum tax. Without the § 250 deduction or an FTC, these states were on track to tax all of a company’s so-called supernormal returns, not just the portion of GILTI that is taxed by the federal government. Importantly, all the states that otherwise presumably would have been on track to tax 100 percent of GILTI—including Connecticut, Montana, and Utah, to name a few—have either decoupled from GILTI, legislatively conformed to the § 250 deduction, or fully or mostly excluded GILTI by classifying it as a foreign dividend eligible for the state’s DRD.

However, even states that bring in the § 250 deduction—often by using line 30 of the corporate income tax form as their income starting point—tax an outsized share of it compared to the federal government since states, by default, do not have credits for foreign taxes paid. States do not offer such credits because state tax codes were not designed to account for international income, as they follow the long-held standard that state taxation stops at the “water’s edge,” applying only to income earned domestically. Without the 80 percent credit for foreign taxes paid, state taxation of GILTI tends to be far more aggressive than federal taxation of GILTI, potentially rivaling or even exceeding the federal rate.

State taxation is further complicated by the difficulty in determining how much of GILTI is attributable to a particular state, and how it should be included for apportionment purposes. Some states provide “factor relief” for GILTI—apportioning it as they would apportion income earned domestically—but apportionmentApportionment is the determination of the percentage of a business’s profits subject to a given jurisdiction’s corporate income tax or other business tax. US states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. of GILTI has proven highly complex. Some states deny factor representation for GILTI, including GILTI in the numerator while excluding it from the denominator or only including a narrow definition of net rather than gross GILTI in the denominator, which inflates the state’s share and discriminates against GILTI compared to other forms of income.

Even with the § 250 deduction and attempts at apportionment, state taxation of GILTI is highly uncompetitive, as it increases in-state tax burdens for multinational businesses for reasons having nothing to do with the company’s activities in the state (or even in the U.S.). As such, the most competitive and economically neutral approach is for states to avoid taxing GILTI altogether, either by offering a subtraction for GILTI, or, for states that offer a 100 percent DRD, by classifying GILTI as dividends income.

In many cases, states relied on administrative determinations—at least initially—to interpret whether or how much GILTI they tax. For example, some states—including Kentucky, Louisiana, and Missouri, to name a few—issued guidance saying GILTI is excluded from taxation because it is classified as a dividend or deemed dividend and is therefore eligible for the state’s DRD. Other states, including Nebraska and Maryland, have issued guidance saying GILTI is not considered a dividend or deemed dividend and is therefore not eligible for the DRD.

There is good justification for states to classify GILTI as a foreign dividend or deemed foreign dividend. States have long offered DRDs as a way of excluding from their tax base any foreign income that might otherwise incidentally flow through to the state. For instance, Subpart F income—a category of foreign income that was created by the federal government long before the TCJA and includes passive earnings from dividends, royalties, rents, or interest—is deductible under states’ DRDs. While GILTI is distinct from Subpart F income, these categories of foreign intangible income are found in the same portion of the tax code—IRC sections 951 and 952, respectively—and both types of income are attributable (or deemed attributable) to foreign investments in intangible assets. As such, states that extend their DRD to Subpart F income have good reason to do the same for GILTI, a newly conceived category of income that did not exist until the TCJA.

State Taxation of GILTI Raises Constitutional Issues

Not only is state taxation of GILTI highly unusual and uncompetitive, but it also raises serious constitutional issues in states that treat GILTI less favorably than they treat income earned domestically, in violation of the U.S. Constitution’s Dormant Commerce Clause, which prohibits states from discriminating against foreign (both out-of-state and international) commerce.

States that use separate rather than combined reporting face a particularly precarious situation, as such states include CFCs—but not U.S.-based subsidiaries—in a consolidated group for purposes of taxation. This treats international income less favorably than U.S.-sourced income. Under the Foreign Commerce Clause, Congress, not states, has the sole authority to regulate international commerce, so a state’s decision to tax international income more heavily than domestic income is presumptively unconstitutional and in conflict with the precedent established in Kraft Gen. Foods, Inc. v. Iowa Department of Revenue & Finance (1992). In this case, the U.S. Supreme Court struck down a state business tax that offered domestic but not foreign subsidiaries a deduction for dividends received. Given this precedent, it is especially prudent for separate reporting states to remove GILTI from their tax bases.

Another way in which states’ taxation of GILTI can run afoul of the U.S. Constitution is when GILTI is apportioned less favorably than other forms of income. Each state with a corporate income tax has a system in place to determine the amount of a company’s corporate income that is deemed attributable to that state. Apportionment formulas vary, but they take into account either the company’s sales into that state as a percentage of total sales or some weighted combination of factors (including sales, property, and payroll) in the state as a percentage of the U.S. total.

Importantly, under a typical state’s apportionment formula for U.S.-sourced income, a multistate company’s presence in that state (measured using single sales factor or multi-factor apportionment) is included in both the numerator and the denominator of the formula, such that the denominator shows the company’s total presence in all states. For purposes of GILTI taxation, however, some states are taxing GILTI without proper apportionment, either by including GILTI in the numerator but excluding it from the denominator or by including only net—rather than gross—GILTI in the denominator. (Net GILTI is the amount subject to tax, not the amount of international income yielding that tax liability, even though the U.S.-sourced sales factor is based on gross sales.) This inflates the share of GILTI—compared to the share of domestic income—that is taxed by the state. This unequal treatment could likewise be found to violate the Commerce Clause.

Current Status of States’ Taxation of GILTI

Despite many states’ decisions to move away from taxing GILTI, some states remain intent on taxing it, while uncertainty persists elsewhere—even though, in many cases, companies are already paying it.

Even more than three years after enactment of the TCJA, a handful of states are conformed to the sections of the federal tax code that include GILTI but have never issued guidance officially setting out the state’s approach to its taxation. As a result, some companies could be accruing GILTI liability in a state without their knowledge, while others are remitting in the absence of clear guidance regarding their tax obligations. Such ambiguity, years after the enactment of the TCJA, is unjustifiable. States that have not yet issued guidance should act quickly to provide clarity to taxpayers and ultimately codify legislative language excluding GILTI from taxation.

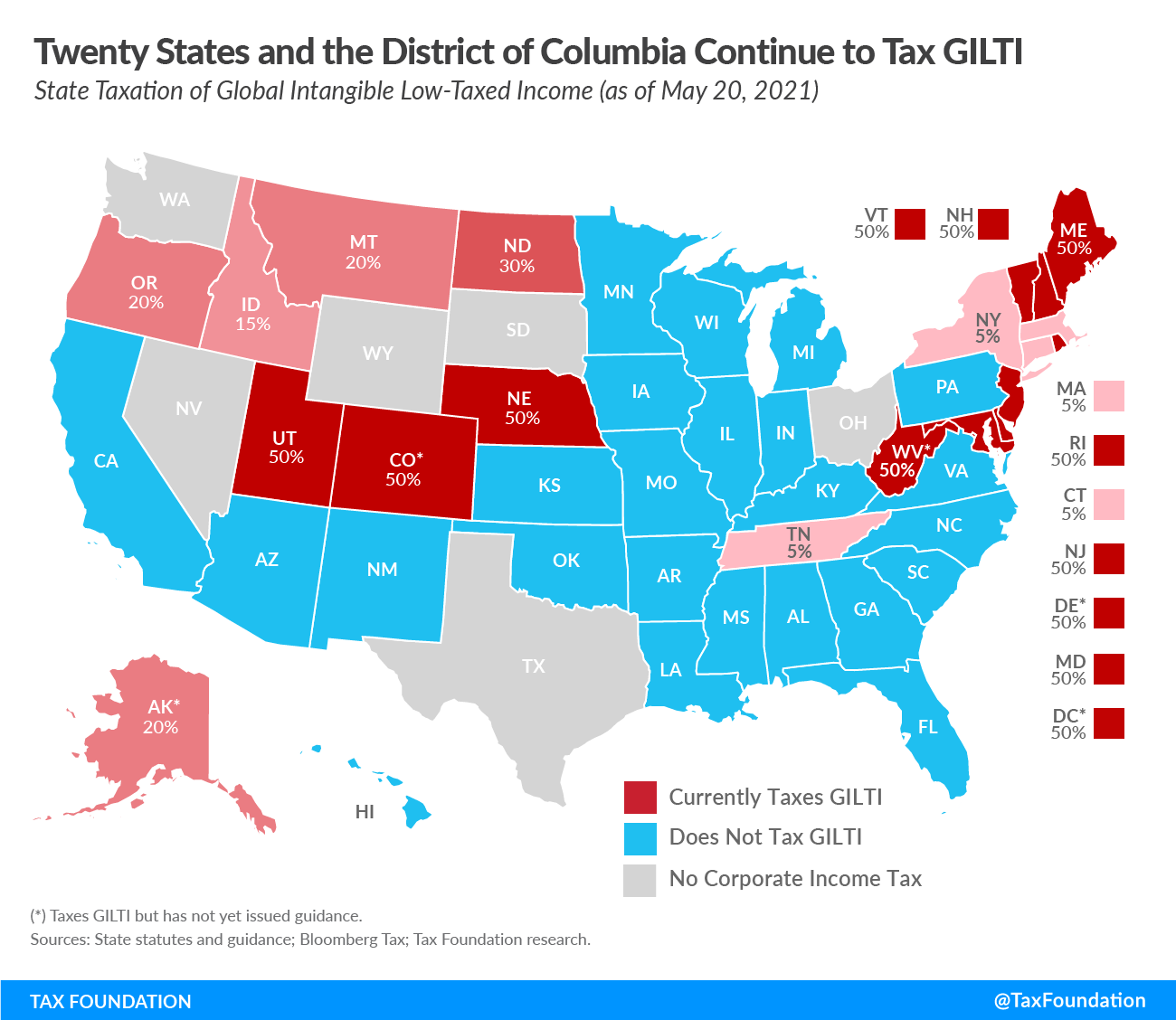

Figure 1 shows the current status of states’ taxation of GILTI, as well as whether each state has issued guidance outlining its approach. For states that tax GILTI, the map shows the percentage of apportionable GILTI that is taxed after applying the § 250 deduction or DRD, where applicable. The calculation does not take into account, however, how a state apportions GILTI. Businesses can be subject to significantly higher tax liability in states that do not provide factor relief for GILTI.

To date, 20 states and the District of Columbia tax GILTI, but only 16 of those states have issued guidance on the topic. Currently, 11 states and the District of Columbia tax 50 percent of GILTI, while other states tax less, including four states that tax only 5 percent of it.

The Impact on States of the Biden Administration’s Proposed Federal Changes to GILTI

In April 2021, President Biden unveiled the basic outline of the tax provisions of his proposed American Jobs Plan Act, called the “Made in America Tax Plan,” which has stated goals of “reducing profit shiftingProfit shifting is when multinational companies reduce their tax burden by moving the location of their profits from high-tax countries to low-tax jurisdictions and tax havens. and eliminating incentives to offshore investment.”[4] Among other provisions, the plan proposes several changes to the tax treatment of GILTI. These include increasing the rate on GILTI to 21 percent, eliminating the 10 percent exemption for deemed returns to QBAI, and taxing GILTI on a country-by-country basis. If adopted, these changes would not only increase GILTI tax liability for U.S. multinationals at the federal level, but they would also increase companies’ state income tax liability in the states that currently tax GILTI.

While President Biden’s draft tax plan does not specify details regarding how the rate on GILTI would be increased, it is generally understood that this would be accomplished by reducing the § 250 deduction from 50 percent to 25 percent under the plan’s proposed new corporate income tax rate of 28 percent. (Taxing 75 percent of GILTI under a higher corporate income tax rate of 28 percent would yield a 21 percent effective rate on GILTI.) It is worth noting, however, that some Senate Democrats have expressed concerns with this much of a rate increase and have since proposed a target corporate income tax rate of 25 percent.[5] Although the federal rate increase would not flow through to states, a reduced § 250 deduction would.

In addition to significantly increasing multinational companies’ federal income tax liability—as well as increasing the number of companies with income classified as GILTI—reducing the § 250 deduction would directly increase multinational companies’ tax liability in the nine states and the District of Columbia that bring that deduction into their own tax code. Several of those states—Colorado, Delaware, Maryland, Nebraska, and New Jersey, as well as the District of Columbia—conform to the federal code in such a way that changes to the deduction would be brought in automatically, thereby increasing the amount of GILTI they tax from 50 percent to 75 percent. The other four states that bring in the § 250 deduction—Idaho, New Hampshire, Vermont, and West Virginia—use static conformity and would only bring in proposed changes with the proactive adoption of legislation to update their conformity date.

President Biden’s other two proposed changes—eliminating the exemption for deemed returns to QBAI and imposing GILTI on a country-by-country basis—would automatically increase the amount of foreign earnings that flow through to all states that tax GILTI.

First, eliminating the exemption for deemed returns to QBAI would offend any sense in which GILTI operates as a proxy for intangible income parked in low-tax jurisdictions. Instead, GILTI would become a much broader and more aggressive approach to the U.S. government’s taxation of foreign income, regardless of its source. If the federal base is broadened such that additional income is classified as GILTI under § 951A, all states that conform to that section would automatically tax that additional income without taking any legislative action or even updating their conformity dates.

Second, GILTI is currently calculated based on a company’s profits, losses, and taxes in all foreign countries combined, rather than based on the company’s profits, losses, and taxes in each individual country. When net foreign income is the basis for GILTI taxation, a company’s losses in one country can offset profits in another. Calculating GILTI on a country-by-country basis would mean some companies would be taxed under GILTI for having a highly profitable operation in one country even if the company had several unprofitable operations elsewhere.[6] This would increase the amount of income that is taxed by the U.S. as GILTI, meaning more of that income would also be taxed by all states that tax GILTI.

Table 1 shows the states that currently tax GILTI and specifies which states have issued guidance to that effect. In addition to displaying whether each state offers the § 250 deduction or classifies GILTI as dividends income that is eligible for the state’s DRD, the table shows the percentage of GILTI each state taxes. The table also includes a column showing the percentage of GILTI each state would tax if President Biden’s proposal to reduce the § 250 deduction to 25 percent were adopted.

| State Taxation of GILTI Under Current Law and Biden’s Proposal | |||||

|---|---|---|---|---|---|

| State | GILTI Inclusion | § 250 | DRD | Guidance | |

| Current Law | Biden Proposal | ||||

| Alaska | 20% | 20% | No | 80% | ✗ |

| Colorado | 50% | 75% | Yes | 0% | ✗ |

| Connecticut | 5% | 5% | No | 95% | ✓ |

| Delaware (a) | 50% | 75% | Yes | 0% | ✗ |

| Idaho (b) | 15% | 15% | Yes | 85% | ✓ |

| Maine | 50% | 50% | No | 0% | ✓ |

| Maryland (a) | 50% | 75% | Yes | 0% | ✓ |

| Massachusetts | 5% | 5% | No | 95% | ✓ |

| Montana | 20% | 20% | No | 80% | ✓ |

| Nebraska | 50% | 75% | Yes | 0% | ✓ |

| New Hampshire (c) | 50% | 75% | Yes | 0% | ✓ |

| New Jersey | 50% | 75% | Yes | 0% | ✓ |

| New York | 5% | 5% | No | 0% | ✓ |

| North Dakota (d) | 30% | 30% | No | 70% | ✓ |

| Oregon | 20% | 20% | No | 80% | ✓ |

| Rhode Island | 50% | 50% | No | 0% | ✓ |

| Tennessee | 5% | 5% | No | 95% | ✓ |

| Utah | 50% | 50% | No | 50% | ✓ |

| Vermont (c) | 50% | 75% | Yes | 0% | ✓ |

| West Virginia (c) | 50% | 75% | Yes | 0% | ✗ |

| District of Columbia | 50% | 75% | Yes | 0% | ✗ |

| (a) Separate reporting state with meaningful inclusion of GILTI, raising constitutional issues under Kraft. | |||||

| (b) The deduction is reduced to 80 percent if the taxpayer elects not to submit domestic disclosure spreadsheets. | |||||

| (c) State uses static conformity, so federal changes to the § 250 deduction would not flow through automatically. | |||||

| (d) The 70 percent deduction for foreign dividends is available for companies filing returns using the water’s edge method, while GILTI is eliminated (100 percent deduction) as duplicative for companies using a worldwide combined reporting method. | |||||

| Note: “Biden Proposal” column assumes a Section 250 deduction reduced to 25 percent. California conforms to a pre-TCJA version of the IRC and therefore does not currently tax GILTI but could tax it upon updating its conformity date. | |||||

| Sources: State statutes and guidance; Bloomberg Tax; Tax Foundation research. | |||||

A Brief Overview of FDII

One of the TCJA provisions enacted in conjunction with GILTI was the introduction of a deduction for FDII. While GILTI involves the U.S. government’s taxation of domestic corporations’ foreign intangible income, the FDII deduction reduces the effective tax rate for domestic investments in intangible property that generate income from exports to foreign markets. When it comes to the interaction between these two policies, if GILTI is the stick, FDII is the carrot.[7] GILTI reduces the incentive for U.S. companies to offshore intangible property into low-tax countries, while FDII creates an incentive for situating IP in the U.S. The GILTI and FDII deductions are both found in IRC § 250, but the two deductions are distinct and should be treated as such by policymakers.

Just as there is little justification for states to tax GILTI, there is also little reason for states to offer the FDII deduction, although states should avoid the particularly aggressive approach of taxing GILTI while denying FDII. At the federal level, GILTI and FDII work in tandem to reduce the incentive for offshoring IP, but these particular incentives carry much less weight at the state level. State taxation of GILTI is unlikely to impact whether a company offshores its IP, but a state’s taxation of GILTI is likely to impact whether a company maintains a significant presence of property or employees in a particular state, as a state’s taxation of GILTI creates an incentive for businesses to avoid unnecessary exposure to that state’s income tax.

Ultimately, states should avoid becoming involved in international matters and remain agnostic to companies’ activities abroad, as a firm’s activities abroad have historically had no bearing on how that firm is taxed by a particular state. Some states have remained hesitant to exclude GILTI from taxation because the additional revenue is appealing, but of all the ways to raise a dollar of revenue, taxing GILTI is a particularly nonneutral, complex, and economically harmful approach.

Conversely, some states have been hesitant to decouple from the FDII deduction, as doing so would increase some business’ tax liability. It is important to bear in mind, however, that the revenue forgone from offering a state FDII deduction would be more efficiently spent reducing the corporate income tax rate that applies to all firms, since the FDII deduction does little to promote economic growth and is only available to some firms. Denying this deduction with no offset, however, particularly while increasing the taxation of GILTI, is simply a tax increase on multinational businesses with in-state activities.

In short, the most economically neutral position for a state to be in is to avoid taxing GILTI and to avoid conforming to the FDII deduction. For states that do not currently tax GILTI, there is little economic justification for offering the FDII deduction.

Current State Treatment of the FDII Deduction and the Impact of the Biden Administration’s Proposed Changes

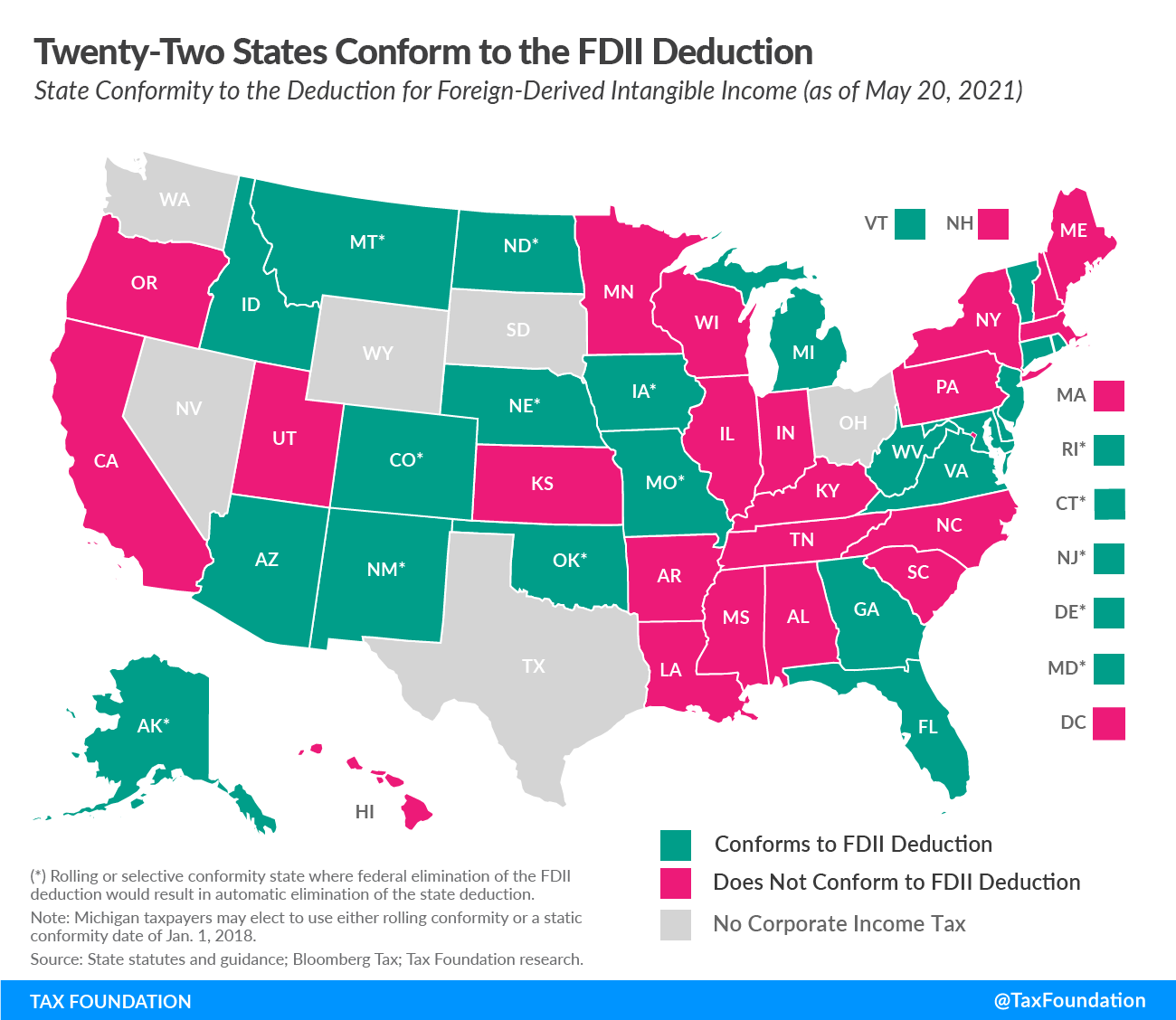

Currently, 22 states conform to the FDII deduction. Of the nine states and the District of Columbia that tax GILTI but conform to the GILTI deduction, all but New Hampshire and the District of Columbia also conform to the FDII deduction. But of all the states that tax GILTI, several take the particularly aggressive approach of taxing GILTI while denying the FDII deduction: Massachusetts, Maine, New Hampshire, New York, Oregon, Tennessee, Utah, as well as the District of Columbia. Meanwhile, nine states conform to the FDII deduction despite decoupling from GILTI.

In addition to raising taxes on GILTI, the Biden administration has proposed eliminating the FDII deduction, thereby eliminating the “carrot” incentive while intending to make the “stick” a stronger deterrent by taxing GILTI more aggressively. Fourteen of the 22 states that currently conform to the FDII deduction conform with the IRC on a rolling basis or would otherwise bring in this change automatically, so these states’ FDII deductions would be repealed automatically if the federal deduction is eliminated. Figure 2 shows the current status of states’ conformity to the FDII deduction and shows the states in which federal repeal of the GILTI deduction would automatically flow through to the state.

Recent Changes in States’ Tax Treatment of GILTI and FDII

Given the constitutional issues, complexity, and negative economic effects of taxing GILTI, several states have eliminated or reduced their taxes on GILTI over the past couple years. In January 2019, 30 states and the District of Columbia were poised to tax GILTI.[8] As of January 2020, that number had dropped to 23 states and the District of Columbia.[9] Today, only 20 states and the District of Columbia still tax GILTI.

Over the past year, three states (Iowa, Alabama, and Kansas) have newly excluded GILTI from taxation, and Utah codified its taxation of only 50 percent—rather than 100 percent—of GILTI. In Iowa, House File 2641 was signed into law in June 2020, excluding GILTI from the state’s corporate income tax base, retroactive to tax year 2019, by adopting a subtraction modification. Similar legislation (House Bill 170) was adopted in Alabama in February 2021, decoupling from GILTI retroactive to tax year 2018 by allowing a deduction for any GILTI included in the taxpayer’s federal taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. .[10] In Kansas, legislators overrode Gov. Laura Kelly’s (D) veto of Senate Bill 50, thereby allowing a subtraction from federal adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods equal to 100 percent of GILTI beginning in 2021.[11]

Utah previously theoretically taxed 100 percent of GILTI by neither conforming to the § 250 deduction nor classifying GILTI as dividends income, though state tax officials had operated under an assumption of 50 percent taxability. House Bill 39, enacted in March 2021, codified that determination by expressly classifying GILTI as dividends income, eligible for the state’s 50 percent DRD, retroactive to tax year 2018.

In Maine, L.D. 220 was adopted in March 2021, denying the FDII deduction, effective retroactively to January 1, 2020. The law does, however, direct Maine Revenue Services to conduct a study regarding the deduction to help inform whether policymakers might consider conforming to the deduction again in the future.

State Legislative Proposals Related to GILTI

During their 2020 and 2021 legislative sessions, several states that had not yet excluded GILTI from taxation debated legislation to do so, while some states that do not tax GILTI are considering newly taxing it.

California

California does not tax GILTI because the state conforms to the IRC as it existed on January 1, 2015. During the 2021 legislative session, Assembly Bill 71 was introduced, a bill that would tax GILTI for businesses that file using the state’s water’s edge election.

Specifically, beginning January 1, 2022, for businesses that do not use combined reporting in which the income of foreign affiliates is brought into the state tax base, AB-71 would bring into the state’s tax base 50 percent of any Section 951A income (not by conforming to the § 250 deduction). Further, the bill would tax 40 percent of deemed repatriated income. AB-71 is undergoing committee consideration and has not received a vote on the Assembly floor.

Illinois

Illinois excludes GILTI from its tax base by treating it as an eligible foreign dividend subject to the state’s 100 percent DRD. However, Gov. J.B. Pritzker’s (D) executive budget for fiscal year 2022 proposes denying the application of the DRD to GILTI while denying the § 250 deduction, which would result in Illinois becoming the only state to tax 100 percent of GILTI.[12]

Massachusetts

Massachusetts taxes 5 percent of GILTI, since the state treats GILTI as a dividend that is eligible for the state’s 95 percent DRD. However, legislation has been introduced to tax a larger amount. Companion bills H.2826 and S.1812 would deny the application of the state’s DRD to GILTI and would instead bring 50 percent of § 951A income into the tax base beginning January 1, 2021. This bill was referred in March 2021 to the Joint Committee on Revenue.

Minnesota

Minnesota excludes GILTI from taxation by giving it the benefits of the state’s 100 percent DRD. However, one proposal, House File 2114 (and its companion bill, Senate File 2459), would require CFCs that generate GILTI to be included in a combined filing group for purposes of apportioning income attributable to and taxed by Minnesota. Minnesota uses water’s edge filing, whereby only the income of domestic corporations is included in the state tax base.

Nebraska

LB347 was introduced and received a hearing in the Unicameral’s Revenue Committee but did not advance in its original form to the Unicameral floor. This bill would exclude GILTI from taxation by giving GILTI the benefit of the state’s 100 percent DRD both prospectively and retroactively.

In 1984, legislation was adopted in Nebraska fully excluding the dividends and deemed dividends of foreign corporations from the state’s tax base and limiting the income included in the numerator of the state’s apportionment formula to income from businesses that are subject to the IRC.[13] Despite this historical decision of the legislature that the state not tax foreign income, the Nebraska Department of Revenue issued guidance in December 2019 determining that GILTI is not considered a foreign dividend or a deemed foreign dividend and is therefore ineligible for the state’s DRD.[14] Because the state conforms to the IRC on a rolling basis, Nebraska automatically brings GILTI and the § 250 deduction into its tax base despite the lack of any proactive decision by the legislature to tax foreign income.

While LB347 as introduced did not advance to the Unicameral floor, an amendment was considered (AM774 to LB432) that would have excluded GILTI from the tax base starting in 2022, but that amendment fell just shy of the majority vote needed for adoption into the underlying bill, which was sent to the governor on May 21, 2021.

Conclusion

At the federal level, GILTI and FDII work in tandem—albeit imperfectly—to discourage the offshoring of IP into low-tax countries, but regulation of international commerce is the job of the federal government, not states. State taxation of GILTI not only raises serious constitutional issues, but it also creates an uncompetitive business climate for multinational companies. States that have not already done so should exclude GILTI from their tax base, especially in light of the Biden administration’s proposed federal changes to GILTI that would flow through to states and make state taxation of GILTI even more aggressive and uncompetitive. Additionally, while state FDII deductions provide tax relief to some firms, their economic effects are modest, and the forgone revenue would be better used in structural reforms that benefit all firms.

Most states never set out to tax international income, which is why so many state legislatures have acted to either exempt or substantially reduce the inclusion of GILTI in their tax base. Now, with the Biden administration proposing the transformation of GILTI from a poorly structured minimum tax into something closer to the reimposition of a worldwide approach to taxation, it is particularly important that states respond, lest they slide into the creation of a worldwide tax system of their own—something states were never meant to do, and for which their existing tax codes are wholly inadequate.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up[1] Daniel Bunn, “U.S. Cross-border Tax Reform and the Cautionary Tale of GILTI,” Tax Foundation, Feb. 17, 2021, 12, https://www.taxfoundation.org/gilti-us-cross-border-tax-reform/.

[2] Ibid.

[3] Richard Rubin, “New Tax on Overseas Earnings Hits Unintended Targets,” The Wall Street Journal, Mar. 26, 2018, https://www.wsj.com/articles/new-tax-on-overseas-earnings-hits-unintended-targets-1522056600.

[4] U.S. Department of the Treasury, “The Made in America Tax Plan,” April 2021, https://www.home.treasury.gov/system/files/136/MadeInAmericaTaxPlan_Report.pdf.

[5] Christina Wilkie, “Biden Open to 25% Corporate Tax Rate as Part of An Infrastructure Bill Compromise,” CNBC, May 6, 2021, https://www.cnbc.com/2021/05/06/biden-says-corporate-tax-rate-should-be-between-25percent-and-28percent.html.

[6] Daniel Bunn, “GILTI by Country Is Not as Simple as it Seems,” Tax Foundation, May 18, 2021, https://www.taxfoundation.org/gilti-by-country/.

[7] Linda Pfatteicher, Jeremy Cape, Mitch Thompson, and Matthew Cutts, “GILTI and FDII: Encouraging U.S. Ownership of Intangibles and Protecting the U.S. Tax Base,” Bloomberg Tax, Feb. 27, 2018.

[8] Jared Walczak, “Toward a State of Conformity: State Tax Codes a Year After Federal Tax Reform,” Tax Foundation, Jan. 28, 2019, 35, https://www.taxfoundation.org/state-conformity-one-year-after-tcja/.

[9] Jared Walczak and Erica York, “GILTI and Other Conformity Issues Still Loom for States in 2020,” Tax Foundation, Dec. 19, 2019, 7, https://www.taxfoundation.org/gilti-state-conformity-issues-loom-in-2020/.

[10] EY, “Alabama Modifies Its Corporate Income Tax, Exempts Certain COVID-19-Related Payments from State Tax, Extends Various Tax Credits,” Feb. 16, 2021, https://taxnews.ey.com/news/2021-0360-alabama-modifies-its-corporate-income-tax-exempts-certain-covid-19-related-payments-from-state-tax-extends-various-tax-credits.

[11] Katherine Loughead, “Outlier No More: Kansas Adopts Tax Reform with Wayfair Safe Harbor, GILTI Exclusion,” Tax Foundation, May 4, 2021, https://www.taxfoundation.org/kansas-tax-override/.

[12] Gov. JB Pritzker, Illinois State Budget Fiscal Year 2022, 49, https://www2.illinois.gov/sites/budget/Documents/Budget%20Book/FY2022-Budget-Book/Fiscal-Year-2022-Operating-Budget.pdf.

[13] EY, “Nebraska Department of Revenue Limits Application of Its Dividends Received Deduction on Subpart F Income,” Feb. 22, 2021, https://taxnews.ey.com/news/2021-0404-nebraska-department-of-revenue-limits-application-of-its-dividends-received-deduction-on-subpart-f-income.

[14] EY, “Nebraska Department of Revenue Issues Guidance on Treatment of GILTI and FDII,” Dec. 12, 2019, https://taxnews.ey.com/news/2019-2193-nebraska-department-of-revenue-issues-guidance-on-treatment-of-gilti-and-fdii.

Share this article