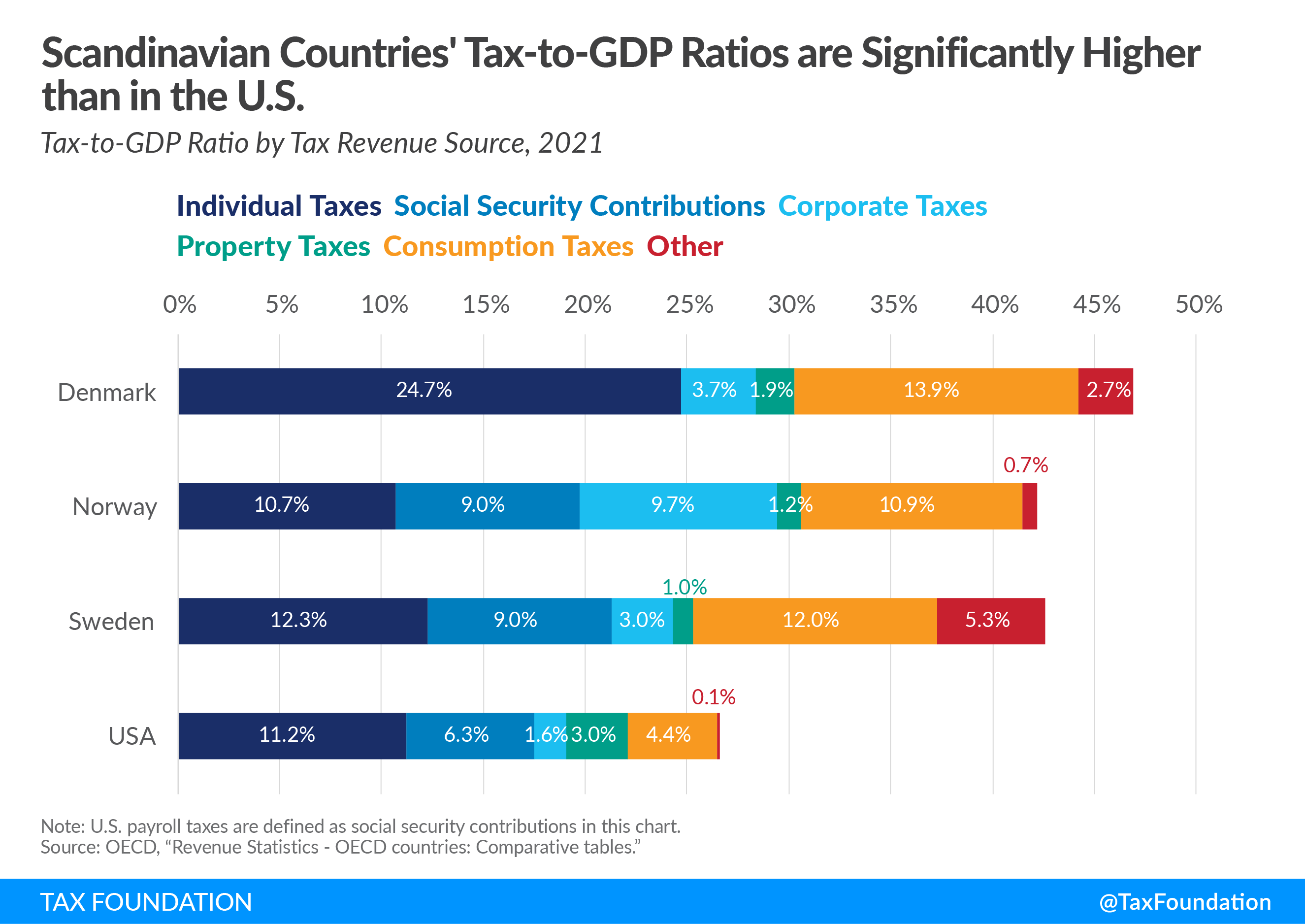

Scandinavian countries are well known for their broad social safety net and their public funding of services such as universal health care, higher education, parental leave, and child and elderly care. High levels of government spending naturally require high levels of taxation. In 2021, Denmark’s tax-to-GDP ratio was at 46.9 percent, Norway’s at 42.2 percent, and Sweden’s at 42.6 percent. This compares to a ratio of 24.5 percent in the United States.

So how do Scandinavian countries raise their tax revenues? A first breakdown shows that consumption taxes and social security contributions—both taxes with a very broad base—raise much of the additional revenue needed to fund their large-scale public programs.

Taxation of Labor Income

In 2021, Denmark (24.7 percent), Norway (19.7 percent), and Sweden (21.3 percent) all raised a high amount of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue as a percent of GDP from individual taxes, almost exclusively through personal income taxes and social security contributions. This compares to 17.5 percent of GDP in individual taxes in the United States.

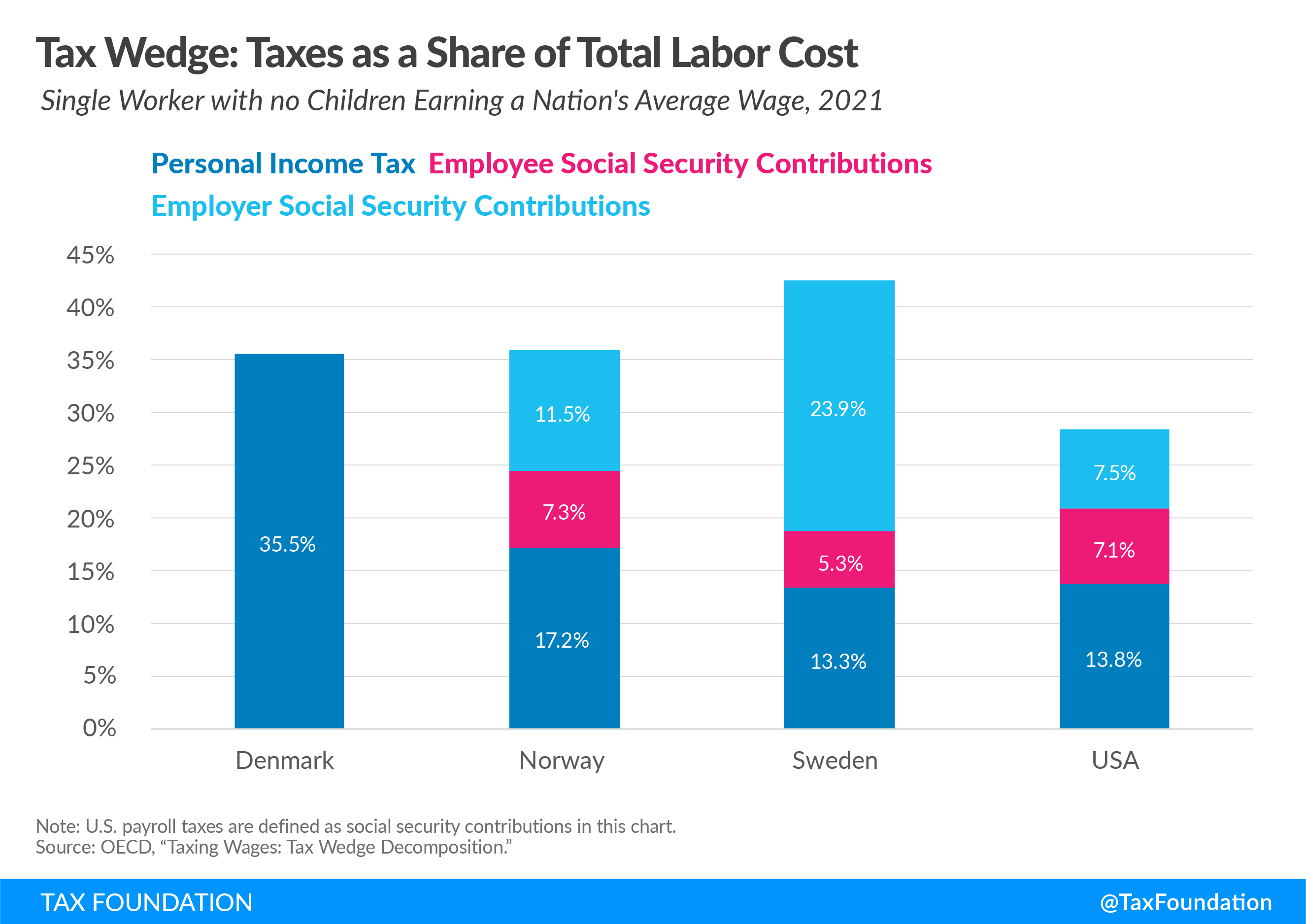

Tax WedgeBroadly speaking, a tax wedge is the difference between the pre-tax price or return and after-tax price or return. For labor income, it is the difference between the total labor costs to the employer and the corresponding net take-home pay of the employee.

One way to analyze the level of taxation on wage income is to look at the so-called “tax wedge,” which shows the difference between an employer’s cost of an employee and the employee’s net disposable income.

In 2021, the tax wedge for a single worker with no children earning a nation’s average wage was 35.4 percent in Denmark, 36.0 percent in Norway, and 42.6 percent in Sweden. The tax wedges of the Scandinavian countries are now higher than the U.S. tax wedge of 28.4 percent and the OECD average of 34.6 percent.

Social Security Contributions

Social security contributions are levied on wages to fund specific programs and confer an entitlement to receive a (contingent) future social benefit. Social security contributions are largely flat taxes and tend to be capped.

Both Norway and Sweden levy high social security contributions, raising revenue amounting to approximately 9 percent of GDP in 2021. In the United States, social security contributions (payroll taxes) raise revenue of about 6 percent of GDP.

In Norway and Sweden, social security contributions—employer and employee side combined—account for 18.8 percent and 29.2 percent of the total labor costs of a single worker with no children earning an average wage, respectively. This compares to 14.6 percent in the U.S.

Only Denmark does not impose social security contributions to fund its social programs. Instead, it uses a share of its individual income tax revenue for these programs.

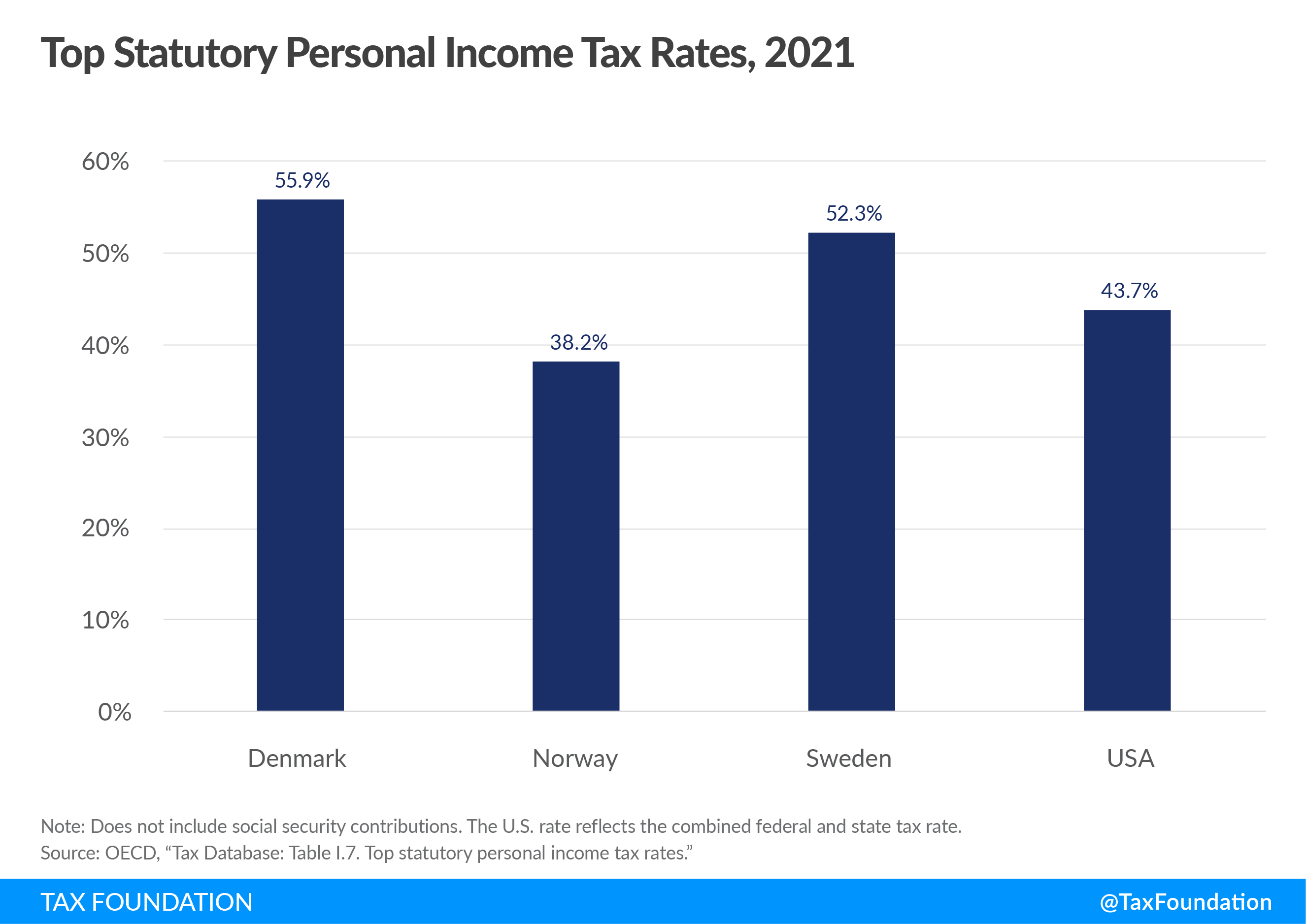

Top Personal Income Taxes

Top personal income tax rates are rather high in Scandinavian countries, except in Norway. Denmark’s top statutory personal income tax rate is 55.9 percent, Norway’s is 38.2 percent, and Sweden’s is 52.3 percent.

However, tax rates are not necessarily the most revealing feature of Scandinavian income tax systems. In fact, the United States’ top personal income tax rate is higher than Norway’s top rate, at 43.7 percent (federal and state combined).

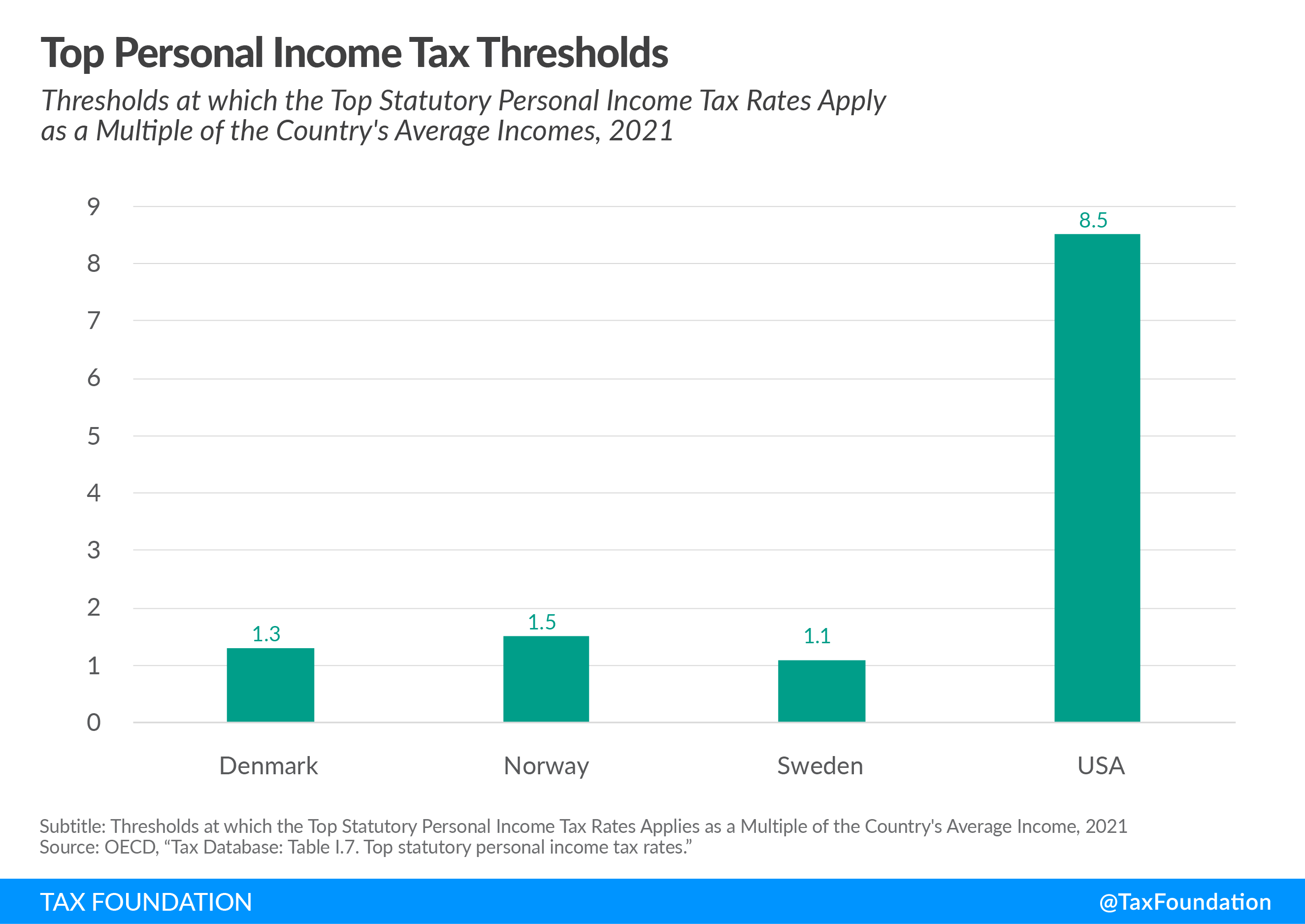

Scandinavian countries tend to levy top personal income tax rates on (upper) middle-class earners, not just high-income taxpayers. For example, Denmark’s top statutory personal income tax rate of 55.9 percent applies to all income over 1.3 times the average income. From a U.S. perspective, this means that all income over $82,000 (1.3 times the average U.S. income of about $63,000) would be taxed at 55.9 percent.

Norway and Sweden have similarly flat income tax systems. Norway’s top personal tax rate of 38.2 percent applies to all income over 1.5 times the average Norwegian income. Sweden’s top personal tax rate of 52.3 percent applies to all income over 1.1 times the average national income.

In comparison, the United States levies its top personal income tax rate of 43.7 percent (federal and state combined) at 8.5 times the average U.S. income (at around $530,000). Thus, a comparatively smaller share of taxpayers faces the top rate.

Importantly, the overall progressivity of an income tax depends on the structure of all tax brackets, exemptions, and deductions, not only on the top rate and its threshold. In addition, the amount of tax revenue raised given a certain tax system depends on the distribution of taxable income.

Value-Added Taxes (VAT)

In addition to income taxes and social security contributions, all Scandinavian countries collect a significant amount of revenue from Value-Added Taxes (VATs). VATs are similar to sales taxes in that they aim to tax consumption. However, the VAT is assessed on the value added in each production stage of a good or service rather than only on the final sales price.

As a tax on consumption, VATs are economically efficient: they can raise significant revenue with relatively little harm to the economy. However, depending on the structure, a VAT can be regressive because lower-income earners tend to consume a larger share of their incomes.

In 2021, Denmark collected about 9.6 percent of GDP through the VAT, Norway 8.2 percent, and Sweden 9.2 percent. All three countries have VAT rates of 25 percent. The United States does not have a national sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. or VAT. Instead, there are state and local sales taxes. The average tax rateThe average tax rate is the total tax paid divided by taxable income. While marginal tax rates show the amount of tax paid on the next dollar earned, average tax rates show the overall share of income paid in taxes. across the country (weighted by population) is about 7.5 percent. Due to the much lower rate, combined with a narrower base, U.S. sales taxes collect only about 2 percent of GDP in revenue.

Business Taxes

While Scandinavian countries raise significant amounts of tax revenue from individuals through the income tax, social security contributions, and the VAT, corporate income taxes—as in the United States—play a less important role in terms of revenue.

In 2021, the United States raised 1.4 percent of GDP from the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. , below the OECD average of 2.9 percent. Denmark and Sweden raised a share similar to the OECD average, at 3.7 percent and 3.0 percent of GDP, respectively. Norway is the exception with corporate revenue equal to 9.7 percent of GDP. Norway is situated on large reserves of oil and charges companies a corporate income tax rate of 78 percent on extractive activities.

All Scandinavian countries’ corporate income tax rates are lower than the United States’ rate. In 2022, both Denmark’s and Norway’s statutory corporate income tax rates were 22 percent and Sweden’s corporate income tax rate was 20.6 percent. The U.S. tax rate on corporations is slightly higher at 25.8 percent (federal and state combined).

Capital Gains and Dividend Taxes

The taxation of capital gains and dividends in Scandinavian countries is similar to the United States, with the exception of Denmark and Norway. Denmark’s top tax rate on dividends and capital gains is among the highest in the OECD, at 42 percent. Norway (35.2 percent) increased its tax on capital gains in 2022.

Sweden’s (30 percent) capital gains and dividends taxes are more in line with the United States. The United States taxes dividends and capital gains at 28.94 percent (federal and state combined).

Conclusion

Scandinavian countries provide a broader scope of public services—such as universal health care and higher education—than the United States. However, such programs necessitate higher levels of taxation, which is reflected in Scandinavia’s relatively high tax-to-GDP ratios.

Adopting such public services in the United States would naturally require higher levels of taxation. If the U.S. were to raise taxes in a way that mirrors Scandinavian countries, taxes—especially on the middle class—would increase through a new VAT and higher social security contributions. Business and capital taxes would not necessarily need to be increased if policymakers were following the Scandinavian model.

It does not come as a surprise that taxes in Scandinavian countries are structured this way. In order to raise a significant amount of revenue, the tax base needs to be broad. This means higher taxes on consumption through the VAT and higher taxes on middle-income taxpayers through higher social security contributions. Business taxes are a less reliable source of revenue (unless your country is situated on top of oil). In short, Scandinavian countries focus taxation on labor and consumption.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe