On Thursday evening, former President Donald Trump proposed a blanket exemption from income taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. for income earned from overtime work. Exempting overtime from tax would add to Trump’s growing list of newly proposed tax cuts, including exemptions for tipped income and Social Security benefits.

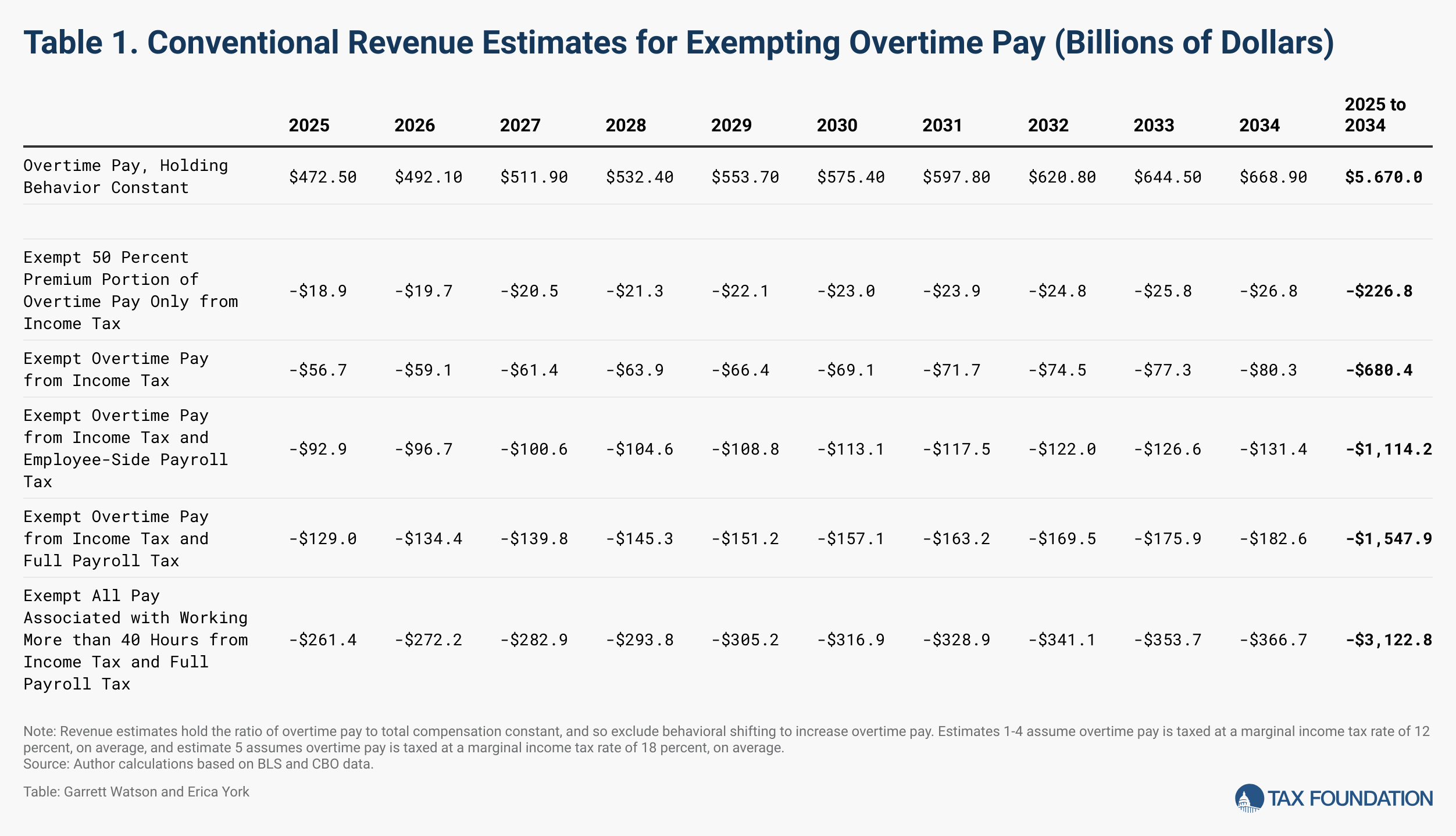

We estimate a lower-bound reduction in revenue for exempting all overtime pay from the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of $680.4 billion over 10 years on a conventional basis. This latest proposal would increase Trump’s already promised $6.1 trillion in tax cuts to $6.8 trillion and raise the total deficit increase of his entire tax and tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. plan to $2.0 trillion over 10 years. Further exempting all overtime pay from employee-side payroll taxes (6.2 percent for Social Security and 1.45 percent for Medicare) combined with the income tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. would reduce tax revenues by $1.1 trillion over 10 years.

The lack of design specificity creates uncertainty over the ultimate revenue effect. For example, if the proposal exempts overtime compensation from income tax and both sides of the payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue., the cost would exceed $1.5 trillion over 10 years. On the other hand, a narrowly tailored proposal that only exempts the 50 percent overtime premium from income tax would reduce revenue by about $227 billion over 10 years on a conventional basis.

While key details are missing from the overtime proposal, exempting overtime pay from income tax would significantly distort labor market decisions. Employees would be encouraged to take more overtime work, and hourly or salaried non-exempt jobs may become more attractive if the benefit is not extended to salaried employees who are exempt from Fair Labor Standards Act (FLSA) overtime rules.

Trump’s proposal would also affect employers as employees find ways to request more overtime work, raising employer labor costs. For some employers, the increased attractiveness of overtime work may fit well with their existing operations. For other employers, they may need to be more aggressive to contain overtime requests as total labor costs rise.

We can illustrate the potential revenue loss of gaming (excluding any increases in overtime hours worked) by looking at the Bureau of Labor Statistics estimates for 2023, which show that 34.4 million workers reported working more than 40 hours a week. Exempting all pay associated with working more than 40 hours per workweek from income taxes and both sides of the payroll tax, as opposed to overtime pay as defined by FLSA rules, could have a fiscal cost of $3.1 trillion over 10 years (not including interest costs).

Conventional Revenue Estimate for Exempting All Overtime Pay from the Individual Income Tax (Billions of Dollars)

| 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2025 to 2034 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Overtime Pay, Holding Behavior Constant | $472.5 | $492.1 | $511.9 | $532.4 | $553.7 | $575.4 | $597.8 | $620.8 | $644.5 | $668.9 | $5.670.0 |

| Exempt 50 Percent Premium Portion of Overtime Pay Only from Income Tax | -$18.9 | -$19.7 | -$20.5 | -$21.3 | -$22.1 | -$23.0 | -$23.9 | -$24.8 | -$25.8 | -$26.8 | -$226.8 |

| Exempt Overtime Pay from Income Tax | -$56.7 | -$59.1 | -$61.4 | -$63.9 | -$66.4 | -$69.1 | -$71.7 | -$74.5 | -$77.3 | -$80.3 | -$680.4 |

| Exempt Overtime Pay from Income Tax and Employee-Side Payroll Tax | -$92.9 | -$96.7 | -$100.6 | -$104.6 | -$108.8 | -$113.1 | -$117.5 | -$122.0 | -$126.6 | -$131.4 | -$1,114.2 |

| Exempt Overtime Pay from Income Tax and Full Payroll Tax | -$129.0 | -$134.4 | -$139.8 | -$145.3 | -$151.2 | -$157.1 | -$163.2 | -$169.5 | -$175.9 | -$182.6 | -$1,547.9 |

| Exempt All Pay Associated with Working More than 40 Hours from Income Tax and Full Payroll Tax | -$261.4 | -$272.2 | -$282.9 | -$293.8 | -$305.2 | -$316.9 | -$328.9 | -$341.1 | -$353.7 | -$366.7 | -$3,122.8 |

Source: Author calculations based on BLS and CBO data.

From a tax policy perspective, there is no principled reason to treat income derived from overtime work any differently than income earned from a taxpayer’s first 40 hours of work. For FLSA non-exempt and hourly employees, employers must pay 1.5 times the regular rate for any hours worked over 40 in a workweek. Overtime pay is totaled together with all other income earned for tax purposes, which results in consistent tax treatment across workers. Trump’s proposal, by contrast, levies a “zero tax rate on a completely unprincipled definition of income,” as former Congressional Budget Office director Doug Holtz-Eakin put it.

Introducing an exemption for overtime work would increase time spent on overtime decisions for employees and worker classification arrangements between employees and employers purely for tax purposes, distracting them from productive activity. While the proposed tax exemption would produce a small increase in the labor supply and long-run economic growth, there are more straightforward ways to do that, such as lowering statutory tax rates, that do not clutter up the tax code with more exemptions or lead to economically wasteful gaming.

Exempting overtime is a more complicated proposal than Trump’s other proposed exemptions for tips and Social Security, which are both already subject to some tax reporting requirements. Instead, exempting a portion of wage income, based on hours worked, introduces an entirely new distinction in the tax code, requiring additional information reporting of hours, likely from employers and employees, as well as new administrative checks.

In short, Trump’s “No Tax on Overtime Pay” proposal would unnecessarily complicate the tax code, increase compliance and administrative costs, and reduce neutrality by favoring certain work arrangements over others.

Revenue Estimating Notes

The Bureau of Labor Statistics estimates that overtime and premium pay makes up about 3.0 percent of total compensation, or about 4.2 percent of salaries and wages. Holding that ratio constant over the 10-year window, that totals to about $5.7 trillion in overtime and premium pay. By holding the ratio constant, we do not incorporate the effect of a recent Biden administration rule change to expand overtime pay to a larger segment of employees, and assume this rule is reversed under a second Trump administration.

By holding the ratio of overtime pay to total compensation constant, we exclude any behavioral shifting to increase overtime hours worked or to reclassify compensation arrangements to qualify for overtime pay—and the incentive for such behavior would be strong.

We assume that, on average, overtime pay is taxed at a marginal income tax rate of 12 percent. For our upper bound estimate, we assume that, on average, overtime pay is taxed at a marginal income tax rate of 18 percent. Both of these rate assumptions are based on current law rates, because Trump has also proposed making the 2017 tax law permanent.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe

{kind=link}