Countries face twin economic challenges with the COVID-19 pandemic: maintain fiscal support to businesses that have been affected by the pandemic and prepare for an uneven and uncertain economic recovery, and work towards budgetary stability and reduce the risks associated with growing public debt. However, moving too fast towards budgetary stability either through tax hikes or spending cuts might undermine the economic recovery. What countries should focus on is implementing reforms that stimulate economic growth.

To help countries face the pandemic-related financing needs while reducing inequality, the International Monetary Fund (IMF) has released a series of policy recommendations based on a temporary COVID-19 taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities., levied on high incomes or wealth. Policymakers are encouraged to choose from a number of tax reforms to raise additional revenue from income, property, corporate, and consumption taxes.

However, not all the recommendations are equally suited to those goals. One of the taxes that the IMF identifies for reform is the corporate tax and suggests introducing an “excess profits tax.” This would translate into a windfall corporate tax to be applied on excess profits above a certain average and on top of the existing corporate tax payment. Such a tax could either target all companies or specific sectors that have been profitable during the COVID-19 crisis. In any case, a windfall tax would add complexity to the tax system, making it difficult to administer and comply with while deterring innovation and impacting economic growth. Also, once deciding to reform the corporate business tax, countries should instead consider full expensing as a means to increase private investment and accelerate economic recovery.

The IMF also calls for raising top marginal income tax rates, introducing a temporary surcharge, and/or tightening regulations on inheritance and gift taxes. Taxing the rich has gained support during the COVID-19 crisis in many countries and especially in low-income ones. Argentina, Bolivia, Colombia, Chile, Peru, and Mexico have either proposed or implemented levies on net wealth. However, Argentina only collected 2 percent of what was projected to be collected with its version of a one-time wealth tax.

New York State also plans to temporarily increase the income tax even though state tax revenue was actually up year-over-year. This will expand the gap with other U.S. states. The proposal pushes for a combined state and federal top income tax rate to more than 51 percent. But New York is not alone—many EU and OECD countries have top tax rates that reach to more than 50 percent. At a time when workers are increasingly mobile, policymakers should focus on making their countries more attractive for taxpayers to work, raise families, invest, and prosper.

Other measures the IMF recommends includes raising the property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. and “updating the property values to current market prices.” Such OECD countries as the United Kingdom, United States, Canada, Israel, France, New Zealand, and Greece already rely significantly on the property tax. Having a property tax that is levied on up-to-date and accurate property values could increase revenues.

However, such property tax reform should also ensure that businesses do not face a tax hike when they improve their properties through renovations or new constructions. Therefore, buildings, plant, and machinery should be excluded from the property tax base; otherwise, property tax can become a direct tax on capital.

The property tax index in our 2020 International Tax Competitiveness Index (ITCI) shows that Estonia, Australia, and New Zealand apply property taxes only to the value of the land itself. A complete reform of the property tax where buildings, plant, and machinery are excluded from the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. would directly improve the tax treatment of property in those countries that currently tax more than just land.

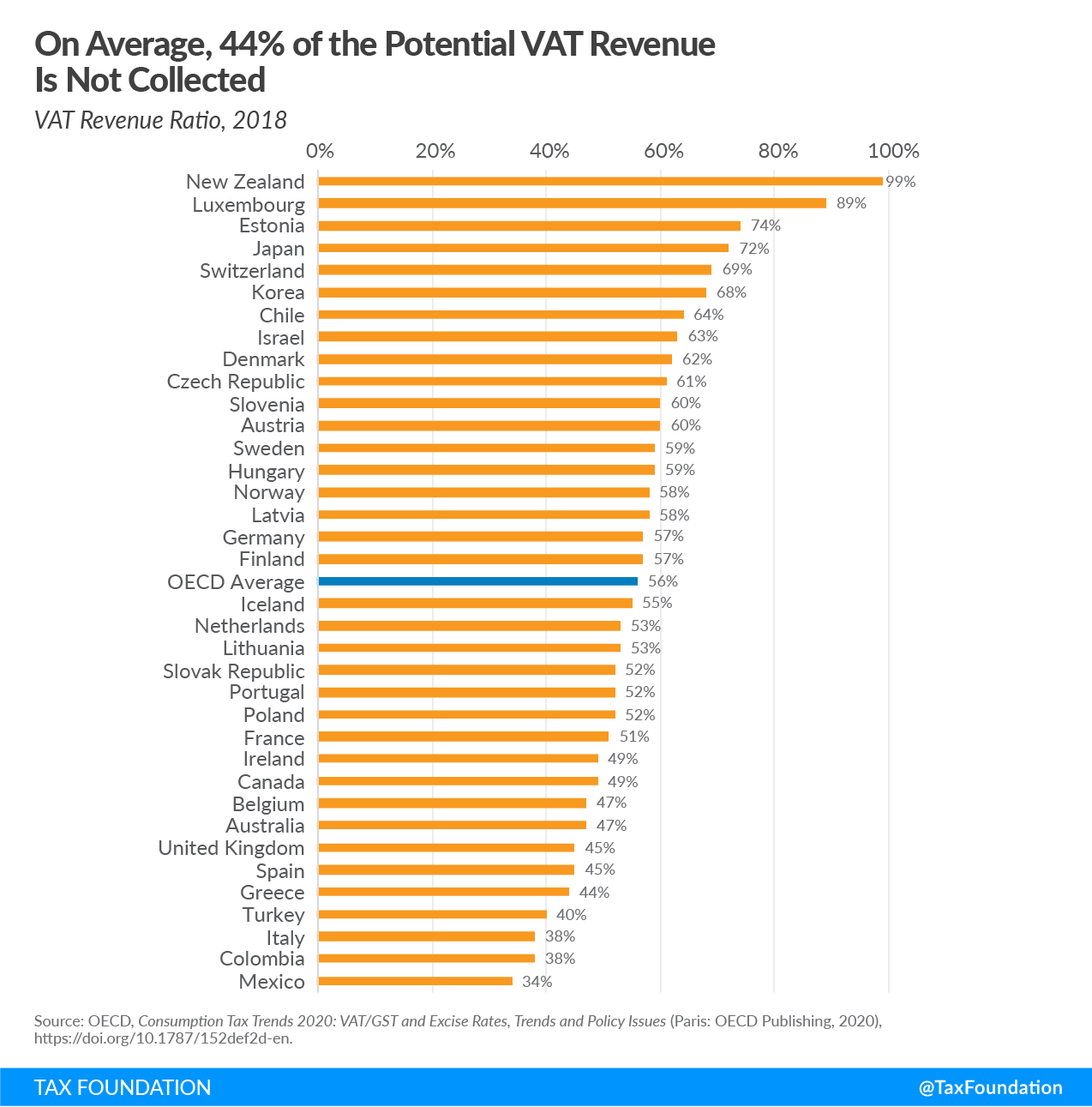

Regarding consumption taxes, the IMF recommends to “reduce the number of goods and services that are either exempt from or face special rates under Value-Added Tax (VAT) systems.” Many countries might benefit from reforming VAT as its revenues are less sensitive to economic downturns than income or corporate taxes. Countries have the opportunity to increase tax revenues by broadening their VAT base. Half of the OECD countries register VAT Revenue Ratios that are below the OECD’s average, indicating there is room to improve tax performance. When looking at the EU countries’ actionable VAT gap, VAT collection could increase on average by as much as 15.85 percentage points if reduced rates and exemptions are eliminated.

The IMF should encourage countries to shift their tax mix from harmful corporate and individual taxes to less harmful consumption and property taxes. Tax hikes implemented in the near term might undermine the desirable rapid economic recovery. Countries should focus on implementing tax reforms that have the potential to stimulate economic growth by supporting private investment and employment.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up

{kind=link}