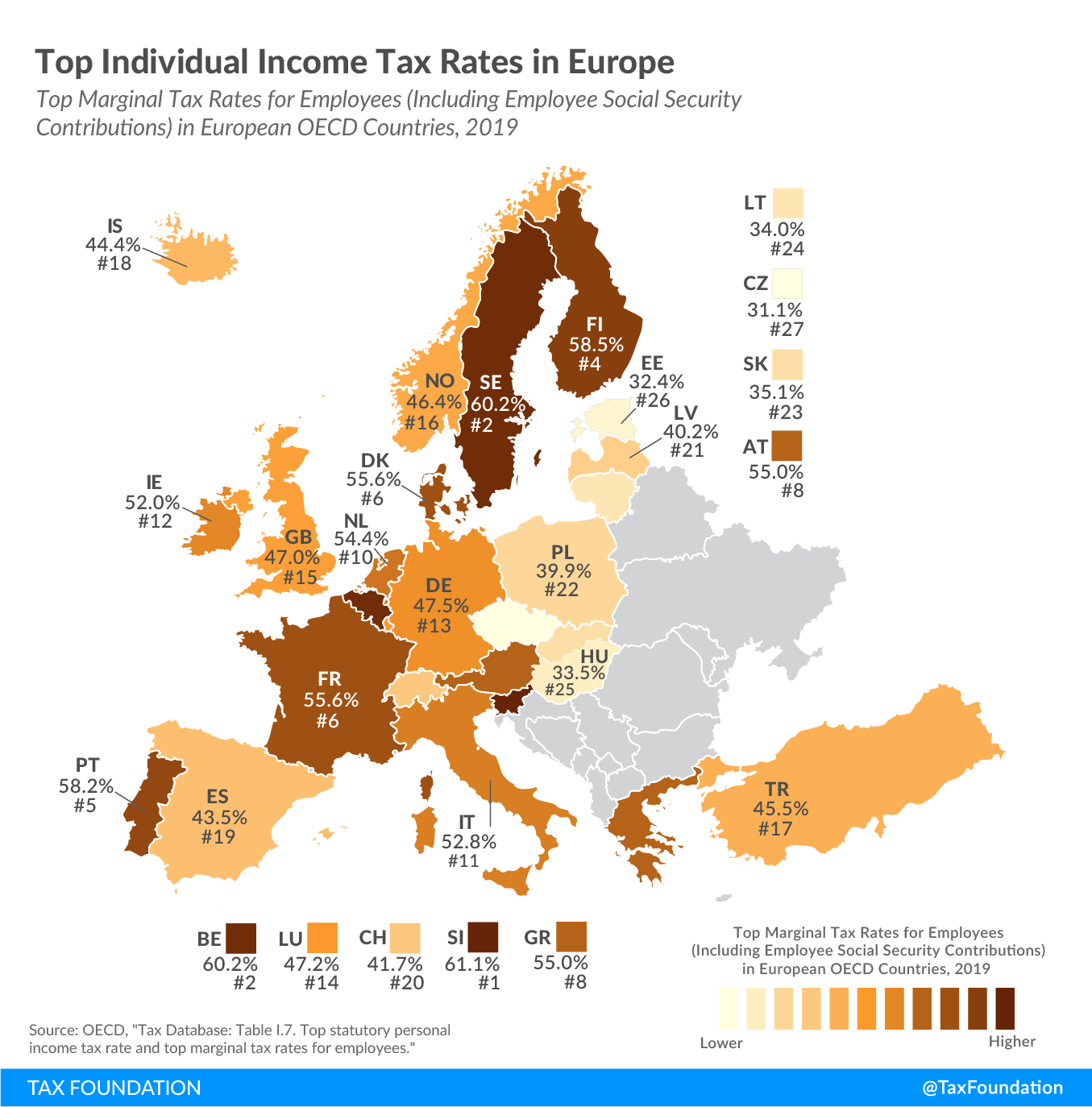

Top Personal Income Tax Rates in Europe, 2020

4 min readBy:Most countries’ individual income taxes have a progressive structure, meaning that the tax rate paid by individuals increases as they earn higher wages. The highest taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate individuals pay differs significantly across European OECD countries—as shown in today’s map.

The top individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source rate applies to the share of income that falls into the highest tax bracket. For instance, if a country has five tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat., and the top income tax rate of 50 percent has a threshold of €1 million, each additional euro of income over €1 million would be taxed at 50 percent.

The map reflects the marginal tax rate a single person without dependents faces at the earnings level at which the top statutory personal income tax rate first applies—in our example at the €1 million threshold. The marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. also includes employee-side social security contributions—in the U.S. commonly referred to as payroll taxes—and takes into account tax deductions and credits. In other words, it shows what share of that first euro over the top threshold earned in wages is paid in taxes.

Slovenia (61.1 percent), Belgium (60.2 percent), and Sweden (60.2 percent) had the highest top marginal income tax rates among European OECD countries in 2019. The Czech Republic (31.1 percent), Estonia (32.4 percent), and Hungary (33.5 percent) had the lowest rates.

The income level at which the statutory personal income tax rates apply—and at which the marginal rate shown in the map is measured—also varies significantly across the countries covered. Expressed as a multiple of a country’s average wage, the threshold ranges from 0 in Hungary to 22.7 in Austria. Hungary applies its flat 15 percent statutory personal income tax on all income earned. In contrast, Austria’s top statutory rate of 55 percent only applies to income above €1 million.

| Country | Top Marginal Income Tax Rate (Including Employee Social Security Contributions) | Top Statutory Personal Income Tax Rate | Threshold of the Top Statutory Personal Income Tax Rate | |||

|---|---|---|---|---|---|---|

| As a Multiple of the Average Wage | In National Currency* | In Euros* | In USD (PPP)* | |||

| Austria (AT) | 55.0% | 55.0% | 22.7 | EUR 1,096,663 | € 1,096,663 | $1,431,738 |

| Belgium (BE) | 60.2% | 52.9% | 1.1 | EUR 52,100 | € 52,100 | $67,804 |

| Czech Republic (CZ) | 31.1% | 15.0% | 0.3 | CZK 123,768 | € 4,821 | $9,850 |

| Denmark (DK) | 55.6% | 55.9% | 1.3 | DKK 558,044 | € 74,744 | $82,716 |

| Estonia (EE) | 32.4% | 20.0% | 0.8 | EUR 14,400 | € 14,400 | $26,172 |

| Finland (FI) | 58.5% | 51.1% | 1.9 | EUR 85,191 | € 85,191 | $99,012 |

| France (FR) | 55.6% | 55.4% | 16.1 | EUR 587,145 | € 587,145 | $778,601 |

| Germany (DE) | 47.5% | 47.5% | 5.3 | EUR 277,063 | € 277,063 | $373,533 |

| Greece (GR) | 55.0% | 55.0% | 11.0 | EUR 234,326 | € 234,326 | $417,388 |

| Hungary (HU) | 33.5% | 15.0% | 0.0 | HUF 0 | € 0 | $0 |

| Iceland (IS) | 44.4% | 46.2% | 1.2 | ISK 11,588,590 | € 84,416 | $82,389 |

| Ireland (IE) | 52.0% | 48.0% | 1.4 | EUR 70,044 | € 70,044 | $89,597 |

| Italy (IT) | 52.8% | 47.2% | 2.6 | EUR 83,263 | € 83,263 | $123,420 |

| Latvia (LV) | 40.2% | 31.4% | 4.8 | EUR 62,801 | € 62,801 | $126,554 |

| Lithuania (LT) | 34.0% | 27.0% | 9.5 | EUR 136,344 | € 136,344 | $300,694 |

| Luxembourg (LU) | 47.2% | 45.8% | 3.5 | EUR 214,756 | € 214,756 | $251,267 |

| Netherlands (NL) | 54.4% | 51.8% | 1.4 | EUR 71,886 | € 71,886 | $91,237 |

| Norway (NO) | 46.4% | 38.2% | 1.6 | NOK 964,800 | € 97,938 | $100,552 |

| Poland (PL) | 39.9% | 32.0% | 1.7 | PLN 101,147 | € 23,536 | $57,010 |

| Portugal (PT) | 58.2% | 53.0% | 15.0 | EUR 280,899 | € 280,899 | $488,964 |

| Slovakia (SK) | 35.1% | 25.0% | 3.2 | EUR 41,867 | € 41,867 | $82,234 |

| Slovenia (SI) | 61.1% | 50.0% | 4.6 | EUR 95,264 | € 95,264 | $165,883 |

| Spain (ES) | 43.5% | 43.5% | 2.4 | EUR 65,102 | € 65,102 | $102,819 |

| Sweden (SE) | 60.2% | 57.2% | 1.5 | SEK 702,925 | € 66,382 | $78,821 |

| Switzerland (CH) | 41.7% | 41.7% | 3.3 | CHF 301,123 | € 270,697 | $260,607 |

| Turkey (TR) | 45.5% | 35.8% | 3.0 | TRY 174,119 | € 27,387 | $95,045 |

| United Kingdom (GB) | 47.0% | 45.0% | 3.7 | GBP 150,000 | € 170,888 | $217,673 |

|

Source: OECD, “Tax Database: Table I.7. Top statutory personal income tax rate and top marginal tax rates for employees,” April 2020, https://stats.oecd.org/index.aspx?DataSetCode=TABLE_I7. Note: *These thresholds have been calculated by multiplying the threshold expressed as a multiple of the average wage with the average wage expressed in the national currency and in US$ Purchasing Power Parity (PPP). Thus, they are approximations of the statutory thresholds. For non-Euro countries, the threshold was converted into euros using the average 2019 exchange rates provided by the European Central Bank (ECB). |

||||||

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Elke Asen

Policy Analyst

Elke Asen was a Policy Analyst with the Tax Foundation’s Center for Global Tax Policy, focusing on international tax issues and tax policy in Europe. Prior to joining the Tax Foundation, Elke interned with the EU Delegation in Washington, D.C., the German Development Agency, and a social startup in Munich, Germany. She holds a BS in Economics from Ludwig Maximilian University of Munich.