Table of Contents

- Executive Summary

- Introduction

- Overview of Current Proposals

- — Governor Justice’s Proposal

- — House Republican Proposal

- — Senate Republican Proposal

- Income Tax Reductions

- — Economic Overview

- — Impact on Pass-Through Businesses

- — Impact on Migration and Remote Work

- — The Role of Reciprocal Agreements

- Sales Tax Changes

- — The Sales Tax Consensus

- — Rate Increase

- — Taxation of Professional Services

- Luxury Tax

- Excise and Severance Taxes

- Tax Cuts and the American Rescue Plan Act

- Designing for Growth

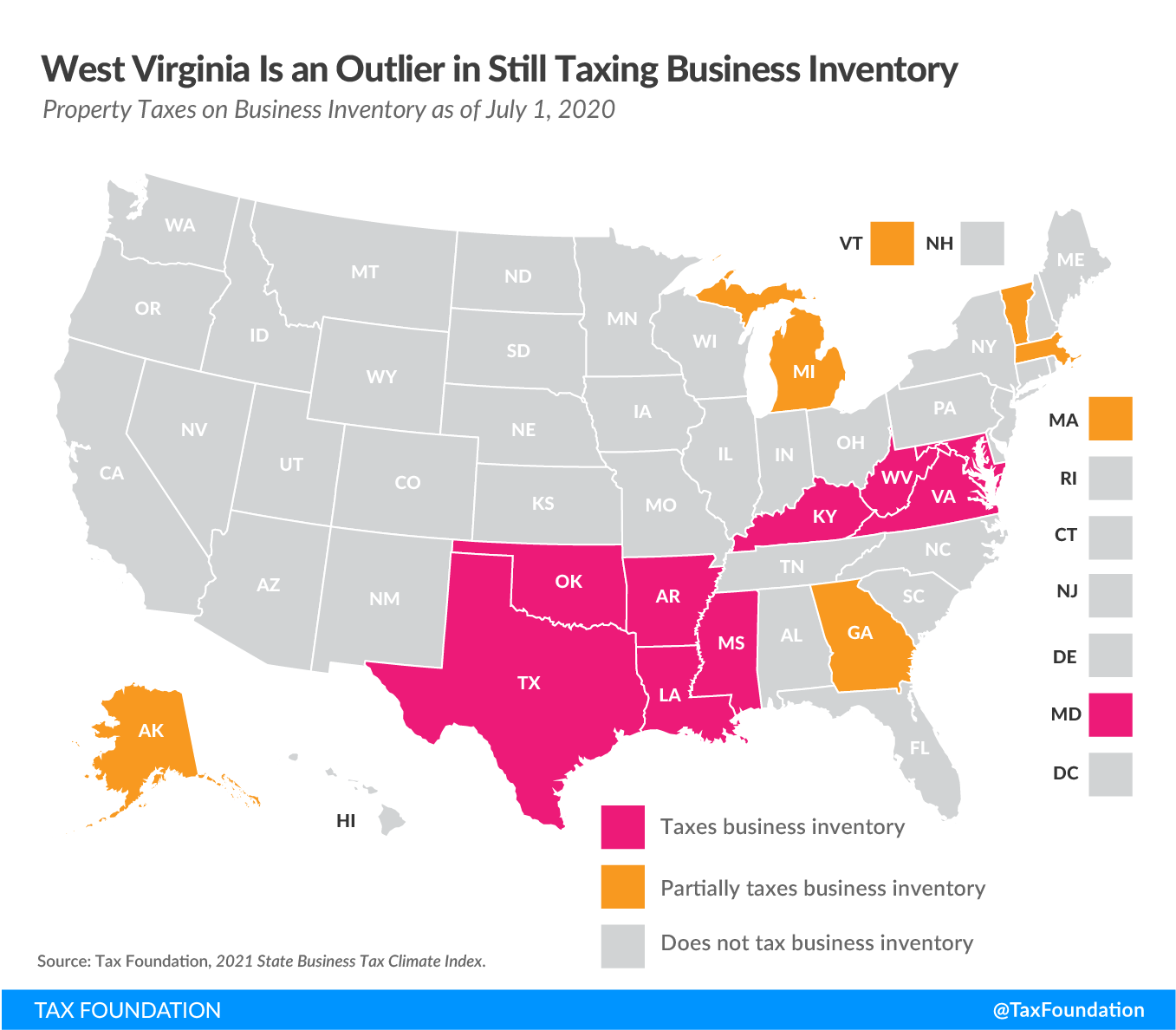

- — Inventory and Business Tangible Property Taxes

- — Corporate Nexus, Apportionment, and Sourcing Rules

- Conclusion

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign UpExecutive Summary

Income taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. repeal is on the agenda in West Virginia, with Governor Jim Justice (R) and Republicans in both the House and Senate releasing plans for dramatically lowering or eliminating the state’s individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source. Despite their shared aims, these plans represent vastly different approaches. They are not even aligned on which income should benefit from rate reductions. House Republicans propose a straightforward reduction in income tax rates, while their Senate counterparts initially exclude investment income, and the governor excludes pass-through business income as well as investment income.

Both the governor’s proposal and the plan offered by Senate Republicans would raise the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. rate, broaden the sales tax base (including to business inputs), and raise certain excise taxes, to which the governor would also add the creation of a “luxury tax” on certain purchases. The House Republican plan phases in income tax annual rate reductions without revenue offsets. The governor would offset rate reductions with a tax shift and the Senate adopts a hybrid of the two approaches, shifting burdens away from income taxes and onto consumption taxes while using future revenue gains to phase in subsequent reductions.

State policymakers are right to recognize the benefits of lower—or no—income taxes. States which forgo income taxes have seen population and economic growth vastly outstripping their peers, and a post-pandemic culture that is friendlier to remote work will greatly enhance tax competition. Details matter, however. If growth and opportunity are the goals, it is important to identify the appropriate revenue offsets for any shift from income taxation. Approaches which increase tax burdens on job creators are inconsistent with the goal of economic growth.

This publication outlines each of the three proposals, then analyzes their major components. It also highlights several other parts of the West Virginia tax code that are ripe for reform, then offers some recommendations for policymakers interested in improving the state’s tax competitiveness by designing for growth. Lawmakers have begun an important conversation, and they now have an opportunity to improve the state’s tax code and enhance the state’s competitiveness. This analysis is intended to help further those deliberations.

Introduction

The Mountain State is placing a bet on a remote work-friendly future. A state that has long attracted outdoor enthusiasts and thrill seekers hopes to turn weekend warriors into new residents, enticed by the state’s natural wonders, its proximity to large employment hubs in other states, and—policymakers hope—by a low-rate income tax, or perhaps none at all. As Governor Jim Justice (R) pointedly observes, over the past 70 years, West Virginia is the only state in the nation to lose population. At a time when the leaders of major metropolitan areas are fearful of net outmigration with the rise of telework and work flexibility, West Virginia lawmakers see an opportunity: becoming a low tax Mid-Atlantic destination for teleworking employees with a case of cabin fever and an allergy to traffic congestion and the grind of big city life.

State officials just launched an Outdoor Economic Development Collaborative effort to attract remote workers who might relocate to take advantage of the state’s hiking, climbing, rafting, and skiing,[2] but the bigger play—the game-changing play, some lawmakers hope—is to turn the Mountain State into a low-tax destination for people who work in the D.C. Metro Area, or Pittsburgh, or somewhere else within driving distance of West Virginia’s country—and city—roads.

It is not a new idea; West Virginia legislators have looked to lower income taxes in the past as well. It is, however, an idea with renewed focus: a dramatic reduction in income tax rates, and perhaps eventual income tax repeal, to create economic opportunity and drive population growth in a state that badly needs a boost.

But every hiker is familiar with the phenomenon of the false summit, the peak that can become the object of all your efforts but which, when reached, proves not to be the summit at all. Income tax reductions are an instrumental goal—a worthy one, to be sure, but subordinate to the ultimate goal of developing a tax code which promotes job creation and economic growth. Reducing reliance on the individual income tax often works in service of that aim, but when the goal is competitiveness and not just income tax relief, the importance of evaluating trade-offs comes more fully into view.

Overview of Current Proposals

With the legislature on the other side of Crossover Day (the day by which legislation must pass its chamber of origin to remain alive), Governor Justice, House Republicans, and Senate Republicans have all unveiled plans to reduce and ultimately repeal the individual income tax, with the Senate plan only recently unveiled, following the House’s passage of its own plan. None of these proposals is likely to be the final plan, and it is quite possible that the legislation will evolve dramatically, bearing only a faint resemblance to these precursors. Nevertheless, it is helpful to begin by outlining these proposals as a starting point for further analysis.

Governor Justice’s Proposal

Governor Justice’s income tax repeal plan does many things—but, at least for now, repealing the income tax is not one of them. That does not mean, however, that the plan is not big or bold; it is both. Any plan which would immediately reduce state income tax rates by 60 percent across the board deserves that label. What immediately stands out, however, is that the tax cuts are for most but not all income. Rate reductions for wage, retirement, and unemployment income do not extend to business income, investment income, rental income, or other forms of non-wage and non-retirement income. (Most businesses are pass-through businesses and pay through the individual income tax code. This is discussed at greater length later.) Excluding small businesses, farms, and investors from the reductions—especially when they are subject to the offsetting tax increases elsewhere—undercuts the growth expectations normally associated with lower income taxes.

The governor’s bill would result in a net tax cut of $185 million a year, but that represents about $477 million in tax cuts for individuals and a $292 million tax increase for businesses.[3]

In broad outlines, the governor proposes to reduce wage income taxes dramatically by raising the sales tax rate, expanding the sales tax base to business purchases, implementing a luxury tax, substantially raising excise taxes, and hiking severance taxes.[4] Specifically, the plan includes:

- An across-the-board rate cut on wage, retirement, and unemployment income yielding a top marginal rate of 2.6 percent, down from 6.5 percent (-$1.04 billion);

- Annual rebate checks to low-income households (-$52 million);

- Expansion of the sales tax base to include professional services (legal, accounting, advertising, data processing, etc.) and select other transactions, including computer hardware and software, health and fitness memberships, and the sale of lottery tickets (+$180 million);

- An increase in the state sales tax rate from 6.0 to 7.9 percent (+475 million);

- A $1.05 per pack increase in the cigarette tax and higher taxes on e-cigarettes and other tobacco products (+$86 million);

- Increases in beer and wine taxes and liquor markup (+$37 million);

- A substantially higher beverage tax (+$63 million);

- A “luxury tax,” a tiered excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on certain costly purchases (+$20 million); and

- The overhaul of the state’s severance taxes (+$42 million).

All told, revenue offsets would bring in a projected $902.6 million while tax reductions total $1.09 billion, making the bill a $185 million net tax cut.[5] Tax rates would be as follows, with business and investment income still subject to current rates.

| Single Filer Rates and Brackets by Income Category | ||

|---|---|---|

| Income Range | Wage and Retirement | Business and Investment |

| $0 – $10,000 | 1.20% | 3.00% |

| $10,001 – $25,000 | 1.60% | 4.00% |

| $25,001 – $40,000 | 1.80% | 4.50% |

| $40,001 – $60,000 | 2.40% | 6.00% |

| $60,001+ | 2.60% | 6.50% |

| Source: Governor Justice’s Tax Bill. | ||

While the proposal is a net tax cut, it is predominantly a tax shift. That is not itself a problem; reducing reliance on nonneutral, volatile, and economically inefficient sources of tax revenue in favor of revenue streams that are more neutral, stable, and pro-growth is the essence of sound tax policy and plays an important part in any package of comprehensive tax reform. When over $900 million—about 20 percent of state tax revenue—is shifted to new sources, however, the nature of those offsets is extremely important. The bill, as noted, carries an estimated $292 million tax increase for West Virginia businesses.

Much of that comes from a broadening of the sales tax base to include many business inputs that are almost never taxed elsewhere. An ideal sales tax base would include all final consumption—no real-world sales tax quite achieves this—while excluding all business-to-business transactions. The exclusion of these intermediate business transactions is not a benefit to businesses but the avoidance of what is known as tax pyramiding, where the same final transaction has the sales tax embedded in it multiple times over.

Overall, individuals do well under the plan—neglecting the indirect effects of reduced tax competitiveness—but the tax savings will be less for heavy consumers of soft drinks, alcohol, and tobacco, who would see excise taxes on those purchases increase by $186 million per year. Business owners take the largest hit.

| Changes in Overall Tax Liability for Individuals and Businesses (in millions) | |

|---|---|

| Individuals | ($477) |

| Income Taxes | ($1,036) |

| Rebate Checks | ($52) |

| Sales and Luxury Taxes | $425 |

| Excise Taxes | $186 |

| Businesses | $292 |

| Sales and Luxury Taxes | $250 |

| Severance Taxes | $42 |

| Source: Tax Foundation estimates. | |

Nothing in the governor’s plan as currently formulated expressly provides for future reductions in the income tax, either to repeal the tax on wage, retirement, and unemployment income or to reduce burdens on pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. and investment income. Full repeal would require offsetting another $1 billion in tax revenue.

House Republican Proposal

House Republicans have, perhaps chiefly as a placeholder bill, passed legislation (H.B. 3300) which adopts an immediate across-the-board rate reduction at a cost of about $75 million in tax revenue, followed by annual rate reductions calculated to be sufficient to reduce each year’s collections by $150 million, continuing until the income tax is fully phased out.[6] The legislation also establishes an Income Tax Reduction Fund, into which select existing and newly available revenues are to be deposited, along with 50 percent of all general fund surpluses. Any time the fund balance exceeds $400 million, a deposit of $100 million is to be made into the General Fund and income tax reductions are to be reduced by an additional $150 million—notably, an amount larger than the transfer.

Assuming income tax revenues would otherwise grow by 2 percent per year, full elimination of the income tax would be achieved in fiscal year 2039. The Income Tax Reduction Fund might accelerate that phasedown. Adopting the state’s assumption of an average annual deposit of $69.4 million into the fund,[7] complete repeal of the income tax might be achieved in fiscal year 2033. Table 3 shows anticipated income tax receipts under current policy, under an annual reduction with no acceleration, and under a system of annual reductions with accelerations when the Income Tax Reduction Fund balance is projected to exceed $400 million.

| Estimated Income Tax Revenues Under Multiple Scenarios | |||

|---|---|---|---|

| Income Tax Phase-Out | |||

| Year | Current Policy | Regular | Accelerated |

| 2022 | $2,041,300,000 | $2,041,300,000 | $2,041,300,000 |

| 2023 | $2,082,126,000 | $1,932,126,000 | $1,932,126,000 |

| 2024 | $2,123,768,520 | $1,820,768,520 | $1,820,768,520 |

| 2025 | $2,166,243,890 | $1,707,183,890 | $1,707,183,890 |

| 2026 | $2,209,568,768 | $1,591,327,568 | $1,591,327,568 |

| 2027 | $2,253,760,144 | $1,473,154,120 | $1,473,154,120 |

| 2028 | $2,298,835,346 | $1,352,617,202 | $1,202,617,202 |

| 2029 | $2,344,812,053 | $1,229,669,546 | $1,076,669,546 |

| 2030 | $2,391,708,294 | $1,104,262,937 | $798,202,937 |

| 2031 | $2,439,542,460 | $976,348,196 | $514,166,996 |

| 2032 | $2,488,333,310 | $845,875,160 | $224,450,336 |

| 2033 | $2,538,099,976 | $712,792,663 | — |

| 2034 | $2,588,861,975 | $577,048,516 | — |

| 2035 | $2,640,639,215 | $438,589,486 | — |

| 2036 | $2,693,451,999 | $297,361,276 | — |

| 2037 | $2,747,321,039 | $153,308,502 | — |

| 2038 | $2,802,267,460 | $6,374,672 | — |

| 2039 | $2,858,312,809 | — | — |

| Notes: Follows state revenue officials in assuming a 2 percent annual increase in income tax collections. Further assumes a 1 percent annual increase in all other revenues, based on recent trends. Accelerated phase-out assumes that $69.4 million a year (increasing by 2 percent each year) is deposited into the Income Tax Reduction Fund. | |||

| Sources: West Virginia State Budget Office; West Virginia Division of Regulatory and Fiscal Affairs; Tax Foundation calculations. | |||

Under accelerated phaseout, state tax revenues would be an estimated $2.7 billion (in nominal dollars) in fiscal year 2033, whereas they would have grown to $5.3 billion absent the policy change—these tax cuts yielding 49 percent less revenue than the state would have otherwise anticipated that year. Such calculations are made on a static basis, meaning that they assume that no economic activity increases because of the tax reduction.

For a tax cut of this magnitude, that assumption is surely untrue: all else being equal, lower taxes yield net in-migration and greater economic growth, and tax cuts of this size would certainly have a meaningful effect. That growth would increase revenues over static assumptions, since there would be more economic activity to tax under remaining taxes, but dynamic growth would be nowhere near sufficient to cover a static revenue loss of nearly 50 percent. The spending cuts this dramatic revenue decline would necessitate, moreover, would likely make the state far less attractive to individuals and businesses alike.

Lawmakers wishing to be able to adopt tax reform this year had to get some bill through the chamber of origin before what is known as Crossover Day, the day on which a bill dies if it has not reached the second chamber. Therefore, it may be a mistake to assume that H.B. 3300 as currently drafted reflects the true policy aims of House Republicans. Its phased approach holds promise, particularly if rate reductions are made contingent on revenue triggers, and if they are at least partially offset by pay-fors elsewhere in the tax code.

The bill can, therefore, be viewed as the skeleton of a later plan, a gradual approach in contrast to the governor’s immediate tax swap. The specific provisions of the bill, however, are impractical. It is exceedingly unlikely that policymakers could—or would want to—identify spending reductions to pair with such large revenue cuts, and the structure of the Income Tax Reduction Fund leads to double counting as routine revenues are diverted each year to accelerate cuts even if they do not reflect any underlying revenue growth.

Senate Republican Proposal

Following passage of H.B. 3300, Senate leaders unveiled a substitute bill (“strike and insert” language) with their own plan for tax reform.[8] Like Governor Justice, Senate Republicans rely substantially on consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or income taxes where all savings are tax-deductible. increases to offset reductions in the individual income tax, though the Senate plan differs from the governor’s plan in many particulars. It also relies on a dedicated fund to facilitate tax reductions, somewhat similar to what House Republicans propose, but unlike the House plan, it does not feature automatic annual cuts or only use the fund for accelerated reductions. Instead, the Senate would implement rate reductions (after the initial offsets) when the fund reaches set levels.

The Senate plan proceeds in multiple steps, with an immediate tax swap followed by a subsequent phasedown that includes additional tax offsets. The plan includes:

- An immediate reduction of rates on earned income—including pass-through business income, but not investment income—by more than 50 percent (-$1.09 billion);

- Expansion of the sales tax base to include computer hardware and software, digital goods, advertising, electronic data processing, and health and fitness memberships at ordinary rates; legal, accounting, architectural, and engineering services at a 3 percent rate; and groceries at a 2.5 percent rate while repealing the now-duplicative soft drink tax (+181 million);

- Increasing the general sales tax rate from 6 to 8.5 percent (+$643 million);

- Imposing a 4.3 percent state occupancy tax on short-term lodging (+$25 million);

- Taxing contingency-based legal settlements at 8.5 percent (+$21 million);

- Reducing certain existing tax credits (+$20 million);

- Creating a new trust fund to facilitate the further phasedown of the individual income tax, which would benefit from a $1 increase in the tobacco tax, raising the vapor tax from 7.5 to 35 cents per ml, and a 7.5 percentage-point increase in the tax on other tobacco products and any future similar tax increases (+$73 million); and

- Dedicating future unappropriated balances and revenue growth to further tax reductions.[9]

This yields $890 million in offsetting revenue (not counting the $73 million in excise tax increases dedicated to the fund) for an initial $1.09 billion in tax cuts, which the Senate apparently intends to further support by dedicating expected revenue growth to the initial round of tax reductions and trimming the state budget.

Subsequently, any state investment income and new revenue from excise tax increases would be deposited into a new fund, the Stabilization and Future Economic Reform (SAFER) Fund.[10] Whenever its balance exceeds $100 million, deposits are to be made to the general fund in $50 million increments until its balance is again below $100 million, with each transfer reducing rates by 12.5 basis points across the board.

Additionally, further rate reductions are to be made using future unappropriated revenues and any revenue increases, essentially plowing all state revenue growth into income tax rate reductions. Notably, there is no growth factor or inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin adjustment, which would make this a net reduction in revenue in real terms over the years in which the income tax is subject to a phasedown. Unlike the governor’s plan, the Senate would include pass-through income in the rate reductions, but still excludes investment income, delaying reductions to rates on unearned income until income taxes on earned income are fully eliminated.

The Senate plan shares some of the economically uncompetitive features of the governor’s plan, like the expanded taxation of business inputs and some unusually high excise taxes, but overall, the plan is more balanced, generating more revenue from broad-based consumption taxes. Unlike the House plan, moreover, it does not commit the state to large annual revenue reductions. Nevertheless, because it begins with a substantial tax swap, it would attempt full repeal of the income tax in a fraction of the time allotted by the House.

Income Tax Reductions

Cutting—or repealing—the individual income tax is the centerpiece of all plans released by the governor and the legislature. West Virginia lawmakers recognize an opportunity to enhance the state’s tax competitiveness by shifting from a less economically efficient tax toward sources of revenue that are better suited for growth. For these plans to work, however, those offsetting revenues must be aligned with that goal. This section examines the economic case for income tax reform, then analyzes income tax reduction options in the context of West Virginia’s competitive landscape.

Economic Overview

Nine states forgo broad-based individual income taxes. (One, New Hampshire, taxes interest and dividend income only, and Tennessee taxed income from those narrow sources until this year.) Some of these states, like Alaska and Wyoming, can lean heavily on severance tax revenues from oil and gas, an option not available to all states. But in states like Florida, New Hampshire, Tennessee, and Texas (where severance tax revenues are meaningful, but not a full explanation), different strategies have worked—and worked well.

Over the past decade, states which forgo income taxes have seen their populations grow at twice the national rate,[11] and gross state product grew 56 percent faster in states without an income tax than it did in those with one over that period.[12] In 2018 (the most recent year for which data are available), the 41 income tax states lost a net of 285,000 residents to the nine states without an income tax.[13]

The ongoing migration from high- to low-tax states, and particularly states with low income taxes, is likely to accelerate with the growing viability of telework post-pandemic.[14] Increasingly, many people will be able to live wherever they wish. Those who are highly sensitive to taxes will find it easier than ever to relocate to jurisdictions with lower tax burdens, regardless of where their employer may be located. And employers themselves will have more location flexibility as geography becomes less of a constraint on their workforces.

All taxes are not created equal. Any tax creates a certain amount of economic drag; this is unavoidable. There is truth to the adage that “whatever you tax, you get less of”—so it makes sense for policymakers to think carefully about what they choose to tax, and how. Individual income taxes fall on labor; on the margin, they lower the payoff to work, decreasing the supply of labor while increasing its cost.

An income tax can be conceptualized as a tax on consumption plus the change in savings, while a well-structured sales tax is a tax on income less the change in savings. An income tax reduces capacity for future consumption; economically, it acts like a sales tax that increases the cost of future consumption, with each additional hour of labor producing fewer goods in the future. Consumption taxes are much more economically neutral by comparison, and the economic literature consistently finds that sales taxes are less of an impediment to economic growth or location decisions than are income taxes.[15]

Consumption taxes do fall on suppliers of labor and capital, like income taxes, but they do so neutrally and—at least when well-designed—avoid double-taxing these factors. Sales taxes are typically destination-sourced, meaning that they are taxed where a good or service is consumed, not where it is produced. Thus, unlike income taxes, they do not discourage investment or job creation.[16] This is, however, only true insofar as the tax falls on final consumption; when the tax falls on business inputs, it increases the cost of investing in-state.

Evidence of the adverse impact of individual income taxes has been documented at the local, state, federal, and even international level. In a series of Organisation for Economic Co-operation and Development (OECD) working papers, OECD-affiliated economists concluded that corporate income taxes are the most harmful to growth, followed by individual income taxes, while consumption and property taxes are less economically damaging. They found that a 1 percent shift of tax revenues from income taxes to consumption and property taxes would increase gross domestic product (GDP) per capita by as much as 1 percent in the long run, and that income taxes were more strongly associated with lower incomes than were sales or consumption taxes.[17] A Canadian study, meanwhile, found that increases in sales taxes are generally associated with increases in economic growth, because they often replace income taxes and other taxes on investment.[18]

One interesting local tax study concluded that a 1 percentage-point increase in a state individual income tax rate reduces annual population growth rates by 0.81 percentage points, while a similar 1 percentage-point increase in local sales tax rates actually increases the annual growth rate by 0.83 percent,[19] evidently because residents favor the services provided by sales taxes more than they dislike the tax, whereas the opposite is true for local income taxes. The study’s authors also speculated that residents considered the sales tax to be more exportable,[20] though the degree to which this is true may be greater for a locality than it is for a state.

Because a well-structured sales tax is more efficient than income taxes, using revenue from sales tax rate increases to pay down income tax rate reductions is economically competitive, as is generating revenue for the same purpose from sales tax base broadening, provided that the base is broadened to previously untaxed final consumption and not to intermediate transactions.

Impact on Pass-Through Businesses

Over 95 percent of all West Virginia businesses are what is known as pass-through businesses, meaning that business income is taxed on (“passes through to”) the individual income tax returns of the owner or owners, rather than being taxed at the entity level like a traditional C corporation. Pass-through businesses are often thought of as small businesses, but this is not entirely true. Most pass-through businesses are small businesses, but for that matter, most C corporations are as well. In West Virginia, nearly 99 percent of businesses meet the U.S. Small Business Administration’s definition of a small business, which includes nearly all the state’s pass-through businesses and three-quarters of C Corporations. S Corporations, partnerships, limited liability corporations (LLCs), farms, and sole proprietorships are all pass-through businesses, and together they employ nearly half of the West Virginia workforce.[22]

The individual income tax is therefore extremely important to businesses, because it is the tax that most businesses pay. And while the roughly 6,000 C Corporations subject to the state’s corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.[23] are also exceedingly important to the state’s economy, and punch substantially above their weight in share of the workforce, many of their suppliers and clients are subject to the individual income tax, so they too have a stake in lower individual income taxes.

| Business Returns by Entity Type, Tax Year 2018 | ||

|---|---|---|

| Entity | Number | Share |

| C Corporations (pay CIT) | 6,183 | 4.50% |

| Pass-Through Businesses (pay PIT) | 131,040 | 95.50% |

| S Corporations and Partnerships | 26,510 | 19.30% |

| LLCs and Sole Proprietorships | 89,740 | 65.40% |

| Farms | 14,790 | 10.80% |

| Sources: IRS Statistics of Income; Tax Foundation calculations. | ||

Unfortunately, these businesses are left out of the governor’s proposed income tax relief. Reducing tax burdens on small businesses is typically an explicit aim of individual income tax rate reductions, since lower taxes on entrepreneurship, investment, and job creation are all key to the economic growth sought after by proponents of income tax cuts. Anomalously, Governor Justice’s proposal exempts small business owners from any income tax relief whatsoever, maintaining current rates on pass-through business income, along with investment income, while dramatically reducing rates on wages and retirement income.

The federal government actually provides preferential treatment of pass-through business income under a 20 percent deduction for qualified pass-through income under Section 199A, a provision adopted in the Tax Cuts and Jobs Act of 2017. Five states partially or fully incorporate this deduction into their own tax codes,[24] and one other state—South Carolina—provides standalone preferential treatment of pass-through income. In South Carolina, active trade or business income from pass-through businesses is taxed at a flat rate of 3 percent, while other forms of income are taxed at marginal rates of up to 7 percent.[25]

If West Virginia adopted Governor Justice’s proposal to bifurcate wage and business income to the detriment of businesses, the Mountain State would join Illinois as the only states to discriminate against pass-throughs in the individual income tax code. In Illinois, this disparate treatment comes in the form of a 1.5 percentage-point surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. atop the ordinary rate of 4.95 percent, leading to a pass-through business rate of 6.45 percent.[26] In West Virginia, it would mean two separate tax tables, with pass-through business income subject to the current top marginal rate of 6.5 percent while other income is taxed at a top rate of 2.6 percent, a 3.9 percentage-point differential. Marginal income from businesses would be taxed at two and a half times the rate on wage income.

There is no good justification for the preferential treatment of pass-through income as provided for in the federal tax code,[27] nor in states’ efforts to provide targeted relief just to businesses. Kansas learned this lesson the hard way, when a large and already structurally unbalanced tax cut fully excluded pass-through business income while continuing to tax wage income. This was innately unfair: a cashier pays income tax on his wages, but the shop owner pays no income tax on his earnings; attorneys are untaxed but their assistants get no such relief; subcontractors paid no tax when doing much the same work that a taxed employee might. But it also changed behavior: the prospect of legal tax avoidance led some individuals to restructure their employment, working as independent contractors (untaxed) rather than employees (taxed).

Yet there is likewise no good justification for the discriminatory treatment of pass-through income, as proposed in the governor’s tax plan, and this too would change economic decision-making in undesirable ways—arguably much worse ways, as here the tax would fall uniquely on entrepreneurial risk-taking. Leaving regular employment to start one’s own business already comes with risks and costs, but that risk-taking is crucial to a dynamic economy. If, however, leaving a salaried position for work as a sole proprietor or small business owner meant a 150 percent increase in the marginal tax rate—or, perhaps eventually, the difference between a 6.5 percent tax and no income tax at all—an already risky bet becomes even less economically attractive.

Even if small businesses did not pay a cent more under this plan than they did previously, the large delta between the taxation of wage earners and small business owners would change economic decision-making for the worse, and the new tax plan would do nothing to attract entrepreneurs to the state or encourage more West Virginians to become job creators.

The reality, however, is even bleaker for entrepreneurs: much of the new revenue to offset the tax cuts for wage earners and retirees in the governor’s plan would come from businesses by taxing their business-to-business transactions, raising the cost of doing business in West Virginia. Furthermore, C Corporations, which are inherently ineligible for relief provided only through the individual income tax, would also bear these additional tax costs. The proposal represents a substantial net tax increase for West Virginia employers, which undercuts the competitive advantage an income tax cut is intended to confer.

The House plan, by contrast, phases down income taxes for all payers, and thus avoids sacrificing much of the economic benefit of rate reductions. To be viable, however, that plan requires some sort of offset, or it could be scaled down to phase in much more modest rate reductions subject to revenue availability. The Senate plan also provides relief to pass-through businesses, though, like the governor’s plan, it does exclude unearned income from relief, at least initially.

Impact on Migration and Remote Work

Notably, some advocates of income tax relief in West Virginia have focused on population growth more than economic growth, though the two are interrelated. Instead of focusing on expanding economic opportunity within Virginia by growing jobs and businesses in-state, an emphasis is placed on making West Virginia an attractive destination for those who are employed by out-of-state businesses and can either telework or commute to an employer’s location across state lines. The latter might be newly attractive for those whose employers adopt flexible work options short of full telework, where an employee might only need to be in the office a day or two a week. States without an income tax already see population growth twice that of their peers; how much more significant might that growth be if many individuals were no longer tied to a particular workplace?

West Virginia shares a border with Kentucky (79 miles of border), Maryland (174 miles), Ohio (244 miles), Pennsylvania (119 miles), and Virginia (381 miles).[28] Pittsburgh is only about 60 miles from Wheeling and 75 miles from Morgantown, and Youngstown is 50 miles from the Northern Panhandle. Hagerstown and Frederick are just a short drive from the West Virginia border, and even Harpers Ferry to Washington, D.C., while a long commute during rush hour, may be attractive to more people if the commute did not need to be made every day. It is easy to imagine West Virginia gaining population from workers whose jobs are not fully remote but enjoy newfound flexibility that expands their commuting radius. And for those with the option of exclusive telework post-pandemic, the Mountain State could be a Mid-Atlantic remote work paradise. A low income tax burden—or none at all—could vastly enhance the state’s existing appeal to those who can suddenly work anywhere.

Traditionally, employees have been tied to specific geographies. When almost all work is performed in physical offices, an employer engaged in locational decision-making must find an equilibrium representing the optimal balance of a variety of often competing factors. They must balance costs of doing business (tax burdens, operating costs, regulatory costs, and labor costs) with access to a qualified workforce and quality of life considerations (schools, research universities, transportation systems, housing markets, cultural amenities) that are important to both executives and the workforce they want to attract. Depending on their business model, they may also need to be located close to clients, suppliers, or their customer base.

Simplify the decision, for a moment, to a question of attracting a qualified workforce. Certainly, a technology company could locate in Morgantown, taking advantage of the amenities, culture, and employee pipeline offered by a university town. West Virginia officials would love to attract more businesses to Morgantown and other business corridors, and tax policy is one way to promote that aim. But for every business that is located elsewhere, there may still be some employees who would prefer to live in Morgantown. Previously, that option was not available to them. The workforce balance that is optimal overall is never optimal for each individual. Some employees will gladly pay a premium for what Philadelphia has to offer, while others take little or no advantage of its amenities—even though they are paying for them through taxes and a high cost of living—and would far prefer a different arrangement. Traditionally, however, individual preferences are in tension with each other: a person may not appreciate any of the amenities they are paying for but appreciate working in a field which recruits heavily from people who do.

The rise of remote work changes the equation. To the extent that teams can operate virtually, employees can decide for themselves which bundle of amenities—priced in both cost of living and tax burdens—contribute to their quality of life and which do not, and choose where to live accordingly, knowing that their job will follow them there. Not everyone who takes advantage of this flexibility will do so in pursuit of financial savings. A highly compensated employee might abandon one high-cost, high-tax jurisdiction for another similarly costly locale because she prefers living in a resort destination to a major metropolitan area. Others, however, will move for lower taxes, a lower cost of living, or a higher (to them) quality of life—things that will often go together. West Virginia officials hope that the state can capitalize on both motivations, combining low taxes and a low cost of living with natural beauty and outdoor activities that may appeal to many workers ready to leave their metropolitan lifestyles behind.

The Role of Reciprocal Agreements

Of the 41 states with broad-based income taxes, 16 have entered reciprocal agreements with some or all of their neighboring states to simplify tax liability for individuals who live in one state but work in another.[29] West Virginia is among them—as are all of its neighbors. Consequently, a West Virginia resident who earns income in Kentucky, Maryland, Ohio, Pennsylvania, or Virginia pays West Virginia income tax, and does not owe taxes in the neighboring state in which they worked.

This not only simplifies tax filing but reverses the way income taxes typically operate. Income taxes are ordinarily imposed where the filer both lives and works. The home (domiciliary) state can tax all income from all sources, while other states tax income when it is earned there. To avoid double taxation, domiciliary states provide a credit for taxes paid to another state. That means that if a West Virginia resident commuted to the District of Columbia, with which the state does not have tax reciprocity, that resident would pay Washington, D.C. income taxes on their salary, then receive a credit against their West Virginia tax liability equal to the amount of tax they would have paid West Virginia on that income. But if a West Virginian instead commuted into Maryland, they would only pay taxes to West Virginia—not Maryland.

The following table illustrates this concept using the example of a single worker who earns $80,000. When a West Virginia resident works in-state, naturally they pay all income taxes on that work income to West Virginia, a $3,945 tax bill. When they work in a state like Maryland, with which West Virginia has reciprocity, the situation is identical: that income is taxed as if it were earned in West Virginia. But when that resident commutes to a job in the District of Columbia, ordinary rules apply. The federal district taxes the income, resulting in a $4,133 tax bill. Since West Virginia would have imposed $3,945 in taxes on that income, there is a credit for that amount, zeroing out liability. (It is important that the credit is for $3,945, not $4,133, as the taxpayer may have other income, taxable only in West Virginia, resulting in additional liability.)

Finally, Indiana is offered as a somewhat far-fetched example, since no one would reasonably commute from West Virginia to Indiana, and no one is likely to earn their entire salary working in Indiana while remaining a resident of West Virginia. But Indiana stands in here as an example of a state with lower income tax burdens than West Virginia but no reciprocity. Tax is paid to Indiana, resulting in a credit which reduces West Virginia tax liability, but the difference ($1,361) is still paid to West Virginia.

| West Virginia and Out-of-State Income Tax Liability on $80,000 in Salary Income | ||||

|---|---|---|---|---|

| Lives In West Virginia and Works In… | ||||

| WV | DC | IN | MD | |

| West Virginia Liability | $3,945 | $0 | $1,361 | $3,945 |

| Out-of-State Liability | $0 | $4,133 | $2,584 | $0 |

| Sources: State statutes; Tax Foundation calculations. | ||||

Reciprocity matters because those agreements would be rendered null should West Virginia ever repeal its individual income tax. A Maryland resident earning $80,000 in Maryland would owe $3,486 to Maryland; a West Virginia resident earning the same amount there would owe $3,945 to West Virginia but nothing to Maryland. If the lower rate schedule in Governor Justice’s proposal went into effect, the West Virginia resident’s tax bill would plummet to $1,578, and still nothing would be owed to Maryland. If, however, the state’s individual income tax was eliminated, the West Virginian commuting to Maryland would pay Maryland income taxes on that income. Their tax bill would shoot back up to $3,486—and be paid to Maryland, not West Virginia.

It is a different story, however, with remote workers, as they would both live and work in West Virginia, regardless of where their business is located. Seven states impose so-called convenience rules which complicate matters by taxing individuals where their office is located regardless of their physical work location, a legally dubious income sourcing rule currently subject to litigation,[30] but in most scenarios, someone working remotely in West Virginia would only be subject to West Virginia income taxes and would enjoy the benefit of the tax’s full repeal.

The issues arising from the end of reciprocity with border states, however, underscores the importance not just of attracting commuting workers but of bringing employment opportunities across the border as well. If West Virginia’s income tax were repealed, this would do nothing to attract workers who intend a daily commute to their existing office across state lines, though—provided the repeal applied to business income as well—it could do a great deal not only to attract truly remote workers but also to bring businesses and jobs across the border.

Sales Tax Changes

The governor’s plan relies on the sales tax to generate $655 million in offsetting revenue, representing nearly three-quarters of all new revenue in the proposal. The Senate Republicans’ plan, with its higher 8.5 percent rate, would generate $823 million from sales tax changes. The House Republicans’ plan does not include any tax swaps. Implemented properly, using sales tax expansion to reduce income taxes can be good policy, because a well-designed consumption tax has less of an adverse economic impact than does an income tax. A poorly designed sales tax base, however, reduces tax competitiveness.

The Sales Tax Consensus

Public finance scholars and tax policy researchers have their fair share of disagreements on taxation, but the sales tax is an area of surprising consensus. Decades ago, scholar John Due wrote that “sales tax structure should produce a uniform distribution in consumption, should be neutral regarding methods of production and distribution, and should be collected at a reasonable cost.”[31] Another leading tax scholar, Charles McLure, identified the ideal sales tax as a destination-based tax on all final consumption (but only final consumption).[32] These standards are broadly accepted, as are several related precepts and observations:

- An ideal sales tax is imposed on all final consumption, both goods and services;

- An ideal sales tax exempts all intermediate transactions (business inputs) to avoid tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.;

- Sales taxes should be destination-based, meaning that tax is owed in the state and jurisdiction where the good or service is consumed;

- The sales tax is more economically efficient than many competing forms of taxation, including the income tax, because it only falls on present consumption, not saving or investment;

- Because lower-income individuals have lower savings rates and consume a greater share of their income, the sales tax can be regressive, though broadening the base to include additional consumer services (much more heavily consumed by higher-income individuals) represents a progressive change;

- The sales tax scales well with ability to pay, because it grows with consumption and is therefore more discretionary than many other forms of taxation; and

- Consumption is a more stable tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. than income, though the failure to tax most consumer services is leading to a gradual erosion of sales tax revenues as services become an ever-larger share of consumption.

Taxes should apply to all final consumption in service of economic neutrality, the idea that taxes should not interfere with economic decision-making any more than is strictly necessary, nor should they pick winners and losers. It is not the role of the tax code to favor piano lessons over baseball bats or e-books over hardcovers. It makes little sense to tax the purchase of a lawnmower but not tax the purchase of lawn care services that obviate the need to own a mower.

The sales tax should also be broad-based in service of tax equity.[33] Sales taxes have two potential sources of regressivity: one, the propensity of lower-income individuals to consume a greater share of their income, and two, a scope of taxable consumption that is more likely to fall on the sorts of transactions which dominate the consumption of lower- and middle-income individuals.

Policymakers often exempt or lower rates on certain classes of consumption as a progressive reform. The exemption of groceries, in West Virginia and many other states, is one such example—though there is reason to believe it may not be terribly effective. Prepared foods are taxed at the standard rate and most of the progressivity of taxing unprepared foods is addressed by the exemption for SNAP (food stamps) and WIC purchases, while the exemption is enjoyed by high-income earners as well—who often spend considerably more on groceries.

In fact, while not enough work has been undertaken to establish a consensus, there is research finding that lower-income taxpayers would actually be better off if groceries were fully included in sales tax bases (while retaining the federally-indicated exemption of SNAP and WIC purchases) and revenue-neutral adjustments were made to the tax rate. The lower grocery rate is designed to create progressivity but largely fails to do so. Yet, at the same time, policymakers have largely neglected a much more straightforward way to promote equity within the sales tax.

Consumption of personal services tends to be more discretionary than consumption of goods. Consequently, higher-income individuals tend to spend a greater share of income on services, which are frequently untaxed. Expanding the sales tax base to additional services rights an accidental wrong in the sales tax as currently formulated, one that presently favors wealthier individuals.

While ideal sales tax bases are broad, however, they should not be so broad as to cover intermediate transactions, often called business inputs. To varying degrees, these business-to-business transactions are taxed in every state with a sales tax, meaning that the sales tax is often embedded in the final price of a good or service several times over. This is not an ineluctable law of consumption taxes, but it has, unfortunately, been the reality in the United States.

In Europe, value-added taxes (VATs) are structurally designed to avoid such double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income.; while each stage of production is taxed, the tax only falls on the incremental increase in value, such that, when the product is finally sold to a consumer, the VAT is imposed on 100 percent of its value—no more, no less. Theoretically, a retail sales tax could also exempt business inputs altogether, either by adopting a sufficiently robust set of exemptions or by tying the exemption to the identity of the purchaser rather than the nature of the product. In practice, though, no state has succeeded in eliminating all business inputs from the sales tax base, even though state revenue offices frequently cite it as an important principle of sales taxation.

A well-structured sales tax is imposed on all final consumer goods and services while exempting all purchases made by businesses that will be used as inputs in the production process. This is not because businesses deserve special treatment under the tax code, but because applying the sales tax to business inputs results in multiple layers of taxation embedded in the price of goods once they reach final consumers—tax pyramiding. The result is higher and inequitable effective tax rates for different industries and products, which is both nonneutral and nontransparent, hiding actual tax costs from consumers and putting in-state businesses at a competitive disadvantage.

Rate Increase

Increasing the sales tax rate is one option to pay down income tax rate reductions, and it is an option favored by both Governor Justice and Senate Republicans. Under the governor’s plan, the state sales tax rate would increase from 6 to 7.9 percent. Under the Senate plan, it would rise to 8.5 percent. Critics have noted that either rate would be the highest state rate in the country, but in many states, local option sales taxes are much more substantial than they are in West Virginia, where many—but not all—jurisdictions impose a 1 percent local option sales tax rate.

Because many West Virginia municipalities do not have a local sales tax, the state’s average local rate is almost exactly 0.5 percent. Thus, the Mountain State’s combined state and local rate would be tied with Arizona for 11th-highest nationwide.[35] Were the income tax rate reduced to 2.6 percent or something near it—the omission of business and investment income in the governor’s plan notwithstanding—that would represent the third-lowest income taxes among these 11 states, after Tennessee and Washington, which forgo individual income taxes altogether.

| State and Average Local Combined Sales Tax Rates, Including Proposed 7.9 and 8.5% Rates | ||||

|---|---|---|---|---|

| State | State Rate | Avg. Local Rate | Combined Rate | Rank |

| Tennessee | 7.00% | 2.55% | 9.55% | 1 |

| Louisiana | 4.45% | 5.07% | 9.52% | 2 |

| Arkansas | 6.50% | 3.01% | 9.51% | 3 |

| Washington | 6.50% | 2.73% | 9.23% | 4 |

| Alabama | 4.00% | 5.22% | 9.22% | 5 |

| West Virginia (Senate) | 8.50% | 0.50% | 9.00% | -6 |

| Oklahoma | 4.50% | 4.45% | 8.95% | 6 |

| Illinois | 6.25% | 2.57% | 8.82% | 7 |

| Kansas | 6.50% | 2.19% | 8.69% | 8 |

| California | 7.25% | 1.43% | 8.68% | 9 |

| New York | 4.00% | 4.52% | 8.52% | 10 |

| Arizona | 5.60% | 2.80% | 8.40% | 11 |

| West Virginia (Governor) | 7.90% | 0.50% | 8.40% | -11 |

| Source: Tax Foundation research. | ||||

In practice, however, the combined rate would either be 7.9 or 8.9 percent under the governor’s plan, and 8.5 or 9.5 percent under the Senate’s. Charlestown, Moorefield, White Hall, and Wheeling all raised their municipal rates from 0.5 to 1 percent between 2015 and 2020, bringing all West Virginia municipalities to a rate of either 0 or 1 percent,[36] with the latter also representing the maximum allowable rate. That maximum allowable combined rate would be tied with Georgia for 19th nationwide under the governor’s plan.

Because sales taxes are more neutral and pro-growth than income taxes, it is better to have a moderately high sales tax with a low (or no) income tax than vice versa, with Tennessee a model of a state that has thrived with high sales taxes but no individual income tax. Particularly in a state in which much of the population lives near a state border, however, lawmakers must bear in mind that unusually large tax differentials can drive cross-border shopping, especially for larger purchases.

West Virginia has at various times exempted, reimposed, and again exempted groceries from the sales tax, which creates a natural experiment regarding the effects of large rate differentials on cross-border shopping. When groceries were briefly taxed at 6 percent from 1988-1991, while neighboring states exempted grocery purchases from their own sales tax or (in the case of Virginia) taxed it at a reduced rate, per capita food sales in West Virginia border counties decreased by 1.38 percent for every percentage-point increase in the cross-border tax differential.[37] Curiously, the only statistically significant border effect was with Virginia, which underscores that these effects are modest and that consumers’ time preferences impose natural limits on willingness to engage in cross-border shopping.

Separately, a study in Nebraska found that a one percentage-point increase in a local sales tax induced a 4.81 percent reduction in demand due to cross-border shopping when another city was immediately adjacent, dropping to 1.87 percent with a 20-minute drive.[38] These findings, and others like them, indicate that the effect of a 1.9 to 2.5 percentage-point increase in the sales tax rate would be modest but not nonexistent. More significant than the rate increase, however, is the proposed inclusion of intermediate transactions, which would cause the tax to pyramid.

Taxation of Professional Services

Both the Senate plan and the proposal offered by Governor Justice lean heavily on the taxation of professional services, though the Senate plan taxes them at a lower rate and includes more consumer base broadeningBase broadening is the expansion of the amount of economic activity subject to tax, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. Narrow tax bases are non-neutral, favoring one product or industry over another, and can undermine revenue stability. as well. West Virginia already taxes more services than most of its peers, taxing 115 of the 176 services tracked by the Federation of Tax Administrators (FTA) in its decennial survey of sales taxes on services. West Virginia taxed 27 of the 34 “business services” listed by the FTA, a category that includes things like maintenance, marketing, packing and crating, telemarketing, and testing, but only one of a possible nine professional services that FTA tracks, a category that includes accounting, architecture, legal services, engineering, and medical services.[39] Both plans would change that, with the governor’s plan taxing all professional services except those of a medical nature while the Senate plan establishes a default presumption that services are taxed, with certain exceptions.

Including business inputs in the sales tax base increases business costs and does so proportionally to the length of the production chain. A large corporation might be vertically integrated, with its own programmers, in-house counsel, an advertising department, accounting and human resources offices, and the like. Smaller businesses, however, might contract for many of these services, or might outsource product engineering—and pay sales tax on the transaction. Indeed, the final consumer good may have a production chain that includes multiple companies that paid sales tax on all these business services and more. This puts West Virginia companies at a competitive disadvantage against out-of-state competitors who did not pay sales tax on those inputs. In a competitive multistate market, their margins will be lower than their rivals’. In a more geographically closed market, West Virginia consumers will bear much of the additional burden in the form of higher prices.

Taxation of professional services is rare, and were West Virginia to expand its base to include them, it would likely tax more such services than any other state. If paired with the governor’s proposed rate increase (contrasted with the Senate’s lower rate on professional services), West Virginia would impose the highest rate on them anywhere in the country. Only Hawaii, New Mexico, and South Dakota tax a wide range of professional services under their sales tax, with sales taxes in Hawaii and New Mexico in some ways better resembling gross receipts taxes.

West Virginia, meanwhile, would become the only state to tax professional services under its sales tax and impose a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding.—the local Business & Occupation (B&O) tax—on those services. Seven states impose gross receipts taxes at the state level, often in lieu of a corporate income tax, and another three (Pennsylvania, Virginia, and West Virginia) have locally-levied gross receipts taxes. Were West Virginia to expand its sales tax base to professional services, it would be the only state to impose income, sales, and gross receipts taxes on them.

| States Taxing Services Proposed for Inclusion in West Virginia’s Tax Base | ||

|---|---|---|

| Professional Service | Number | List |

| Accounting and Bookkeeping | 3 | HI, NM, SD |

| Advertising (Digital) | 0 | — |

| Advertising (TV/Radio/Print) | 2 | HI, NM |

| Architecture | 3 | HI, NM, SD |

| Attorneys | 3 | HI, NM, SD |

| Data Processing (a) | 4 | CT, HI, NM, SD |

| Engineers | 3 | HI, NM, SD |

| Metal and Coal Mining Services | 4 | CT, HI, NM, SD |

| Real Estate Management | 3 | HI, NM, SD |

| (a) Connecticut taxes data processing at a reduced 1% rate. | ||

| Sources: Federation of Tax Administrators; Tax Foundation research. | ||

All West Virginia businesses face higher tax costs under the taxation of such services. It is important to note, however, that the taxation of professional services does not uniquely disadvantage the providers of those services. Sales taxes in West Virginia and most other states are destination-sourced, meaning that sales and use taxes are imposed where a good or service is used or consumed, not where it is sold. West Virginia’s destination sourcing covers services, not just tangible goods. This means that a business would pay sales tax on a professional service when it uses or benefits from that service in West Virginia, not when the service provider is located in West Virginia.

Consequently, a West Virginia company cannot avoid paying the sales tax on professional services by contracting with an out-of-state firm. Similarly, a West Virginia-based professional services corporation is not at a competitive disadvantage against its rivals when competing for out-of-state business, since clients based in other states would not be subject to West Virginia sales tax. These firms may, however, suffer if their overall sales volume is reduced due to higher taxation, which may happen because West Virginia-based companies cut back, shift more activities to out-of-state affiliated companies, or bring more of these services in-house.

The sale tax is ill-suited to the taxation of business inputs, a fact that becomes readily apparent with its expansion to certain industries. A sales tax on advertising, for instance, would be levied on advertising run in Pennsylvania by a West Virginia-based company, but not on advertisements served in West Virginia by a Pennsylvania-based company.

Given the adverse economic impact of taxing business-to-business transactions, policymakers could instead consider broadening the sales tax base to include a wider range of final consumption. This could include currently untaxed personal services as well as goods that are excluded from the sales tax base, particularly groceries (as the Senate plan proposes, at a reduced rate) and gasoline. While motor fuel is already subject to an excise tax to fund roads, that user-pays systems is separate from the consumption itself, which could reasonably be taxed, just like cigarettes are subject both to an excise tax and the state sales tax.

Groceries, meanwhile, are exempted to make the sales tax more progressive. But as noted previously, evidence suggests that the exemption does not enhance progressivity once it is extended beyond the exclusion of SNAP and WIC purchases, and if lawmakers wished, they could combine the re-inclusion of groceries in the sales tax base with additional tax offsets for low-income households. Alternatively, lawmakers could tax food at a reduced rate, as the Senate plan does, in line with the 2.5 percent rate imposed on groceries in neighboring Virginia.[40]

Luxury Tax

These days, the luxury tax is mainly the bane of those playing the Monopoly board game, but Governor Justice proposes situating the tax somewhere between Beckley and Parkersburg rather than Boardwalk and Park Place. The governor’s plan would raise an estimated $20 million from a tiered excise tax on so-called luxury items, defined to include furniture, electronic equipment, appliances, recreational and luxury vehicles (boats, planes, snowmobiles, and ATVs), artwork and collectors’ items, and personal accoutrements (jewelry, watches, clothing, furs, etc.) which cost more than $5,000 in aggregate. The luxury tax is in addition to ordinary sales taxes on these goods.

Luxury purchases would face different rates depending on sale price, though the rates are for the entire purchase price, not the marginal amount, and rates decline as prices rise. The rate on a purchase running $5,000 to $10,000 is 3 percent (above any sales tax liability), with rates declining to 1 percent for purchases in excess of $1 million.[41] A homeowner furnishing a new house and a business upgrading its electronics could both face the luxury tax—though, if sufficiently motivated, they might find ways to legally avoid it.

No state currently imposes a luxury tax, though the federal government did so briefly in the early 1990s, imposing a 10 percent tax on luxury boats, cars, aircraft, jewelry, and furs for personal use above certain price points.[42] The tax, adopted during the administration of President George H. W. Bush, went into effect in 1991 but was repealed in 1993 under the Clinton administration. Policymakers quickly soured on the new tax, which they blamed for significant job losses in affected industries, and which proved an administrative nightmare.

“What went wrong with the luxury tax,” wrote journalist James Glassman at the time, “was that, in trying to go after the rich guys’ toys, Congress put the toymakers out of business. The rich guys, meanwhile, bought other toys (including foreign-made ones) not covered by the tax; or they bought used toys and refurbished them; or they simply saved the money, waiting to spend it another day.”[43] And tax administrators quickly found themselves tangled up in controversies over definitions, use, repairs, and secondhand markets. The tax lived on, for a while, as a surtax on luxury automobiles, but that too was ultimately phased out.[44]

A West Virginia luxury tax would run into similar problems—and some unique to a state-level tax. The tax is, by definition, arbitrary: a $6,000 engagement ring would be taxed, but a $100,000 Porsche would not. A high-end gaming PC would come in below the threshold, but a warehouse’s security system might be taxed as a “luxury.” Many things not generally seen as luxuriant—like furnishing a new home—could be taxed, while more conspicuous consumption goes untaxed if it falls under the $5,000 threshold.

Whereas the federal tax attempted—at great administrative difficulty—to exempts business purchases, the West Virginia proposal does no such thing. Business electronics, for instance, which can carry a high price tag, would appear to be captured by the luxury tax. Furnishing an office would trigger the luxury tax as well, and a vaguely drawn provision about consolidating purchases would make compliance difficult at best.

The proposal attempts to capture remote sales of luxury goods by establishing remote seller and marketplace facilitator provisions similar to those adopted for out-of-state sellers under the sales tax in the aftermath of South Dakota v. WayfairSouth Dakota v. Wayfair was a 2018 U.S. Supreme Court decision eliminating the requirement that a seller have physical presence in the taxing state to be able to collect and remit sales taxes to that state. It expanded states’ abilities to collect sales taxes from e-commerce and other remote transactions. (2018).[45] This approach significantly burdens interstate commerce, since West Virginia would be alone in imposing a luxury tax, and it is unreasonable and constitutionally dubious to require all out-of-state sellers of potentially qualifying goods to comply with West Virginia’s proposed luxury tax law.

As an excise tax, moreover, the luxury tax does not contain any obvious use tax component. Whereas sales and use taxes are typically sourced to the destination where a good or service is used, excise taxes are imposed on the transaction itself. While West Virginia could impose the luxury tax on goods delivered into the state by a remote seller, the proposal may not permit the state to collect tax if the purchaser traveled to another state to make the purchase, even if they did so with the intent of transporting it back to West Virginia. For sufficiently large purchases, cross-border purchases could become quite attractive, to the detriment of in-state sellers.

Luxury taxes may change behavior in other ways as well, for instance by favoring repair of used high-end goods over the purchase of new ones, and it is likely to hurt employment in certain sectors, much like the federal tax did. No other state imposes such a tax, and such a novel tax is ill-suited for West Virginia.

Excise and Severance Taxes

West Virginia imposes excise taxes on beer and wine, soft drinks, tobacco, solid waste disposal, and health care,[46] and severance taxes on the extraction of coal, natural gas, oil, timber, and other natural resources.[47] Coal mining in what is now West Virginia began in the early 19th century and has been a mainstay of the state’s natural resource economy ever since,[48] but West Virginia’s preeminence in natural gas production owes to the more recent development of the Marcellus Shale. Mining, quarrying, and oil and gas extraction employs 3.2 percent of West Virginia’s workforce, almost six times the national average.[49]

West Virginia also has the nation’s highest incidence of smoking[50] and is among the highest in soft drink consumption,[51] which makes higher taxation of these products potentially lucrative, but also portends a significant burden on low-income households. While the class of excise taxes often called “sin taxes” is sometimes imposed to reduce consumption, the purpose of proposed tax increases here is primarily revenue generation, not public health benefits.

The governor’s plan proposes $186 million in increased revenue from existing excise taxes, plus $20 million from the luxury tax, which is an excise tax but is treated separately here due to its unique characteristics. Another $42 million would come from higher severance taxes. Senate Republicans would capture $73 million from tax increases on tobacco and vapor products, but do not propose any changes to severance taxes or any alcohol tax increases. The Senate plan also repeals the soft drink tax, instead generating revenue from the low-rate sales tax on groceries, including beverages.

Excise taxes have their place when internalizing social costs, called externalities, or when functioning as a user-pays system. The motor fuel tax provides a good example of both purposes. The tax is primarily levied to fund road construction and maintenance, with gasoline used as a proxy for contribution to road wear-and-tear. It is, therefore, chiefly a user-pays system. However, by increasing the cost of driving, the tax also helps to capture externalities like a driver’s contribution to traffic congestion and pollution. These are part of the cost of driving, but absent the tax, those costs are borne by society at large, not the drivers themselves. In practice, motor fuel taxes tend to be lower than necessary just to fund road projects, but conceptually, the tax has both functions.

Whereas the motor fuel tax is largely a user-pays system, excise taxes on many products are largely about capturing negative externalities, like covering the additional health-care costs associated with tobacco use or funding efforts to reduce problem gaming or combat drunk driving. Frequently, however, these taxes come to be seen as sources of general revenue, completely divorced from the externalities they are intended to capture.

Excise taxes are poorly suited to generate operating revenues. By definition, such taxes are narrow and selective, and they lack revenue stability, especially when imposed on declining markets. Tobacco tax revenue, for instance, which is projected to raise an additional $86 million in the plan, has been declining for decades. Every year more people quit and fewer people take up smoking, so while an increase could raise more revenue in the short term, it should not be relied upon as a long-term mechanism for general fund revenue.[52] A similar trend can be observed in soda consumption, which has also been declining for years.[53]

In addition to the decline in consumption of taxed products, a narrow base is also vulnerable to regulatory or technological disruption. For example, if new tobacco regulation is adopted at the state or federal level, West Virginia could find themselves without the revenue needed to fund essential services.

The Senate plan nods to this revenue uncertainty by depositing increased revenues from excise taxes into a fund rather than using them directly to pay down rate reductions, but since fund excess balances are used to pay down permanent rate reductions, it is not clear that this provides much protection against volatility beyond the $50 million to $100 million reserve balance in the fund.

Increased reliance on severance taxes also introduces volatility into tax revenues, especially since the governor’s proposal is to introduce a graduated rate based on the commodity price. West Virginia has seen disappointing severance tax collections in recent years due to lower production and delays to pipeline projects,[54] and while higher taxes can boost revenues in the short run, the new design may introduce greater uncertainty over a longer time horizon. Furthermore, higher taxes on a highly price-sensitive industry could shift production elsewhere, particularly given the proven reserves in neighboring states with far lower severance (or, in Pennsylvania, environmental impact) taxes.

Luxury tax proposal notwithstanding, excise taxes tend to be regressive, but some more so than others. For several of the categories targeted for tax increases, consumption increases as income declines, which result in higher consumption among young people, low-income earners, racial and ethnic minorities, and those without a college education.

In 2013, about 47 percent of West Virginians with a high school education or less consumed soda at least once per day, compared to 26 percent of West Virginians with a college degree. Nearly 64 percent of 18- to 24-year-olds drink soda at least once a day; the same can be said about 57 percent of those aged 25 to 34, and 48 percent of those 35 to 54. Eighty percent of all West Virginians consume soda, and 45 percent consume soft drinks more than once a day, compared to 31 percent nationwide.[55]

In 2019, 37.9 percent of West Virginia adults over 25 with incomes below $25,000 a year smoked, compared to just 13 percent of those with incomes over $75,000. The discrepancies are even higher in educational attainment: 40.3 percent of those with less than a high school education reported smoking, whereas only 10.4 percent of college graduates smoked that year.[56]

By itself, the fact that some excise taxes have regressive effects is not an argument against levying them, as a user-pays system or the internalization of meaningful externalities can be good policy, but the effect does underscore the importance of not relying on regressive excise taxes to generate significant tax revenue above and beyond the legitimate aims of excise taxation.

The governor’s proposal would yield some of the nation’s highest taxes, with high rates on cigarettes and extremely high rates on beer, wine, vapor products, and soft drinks. At 75 cents per milliliter, West Virginia’s proposed tax would be significantly higher than the retail price of many vapor products. The Senate would set the tax rate at 35 cents per milliliter. Currently, the nation’s highest volume-based vapor tax on open systems is 10 cents per milliliter.

In the governor’s plan, a wine tax of $4 per gallon would be the nation’s highest, and over four times the median. The higher beer tax ($29.25 per barrel, up from $5.50) would be the third-highest nationwide, imposed at over 3.6 times the median rate. And soft drink taxes of any sort are rare, but West Virginia’s would become quite high at 6 cents per can or bottle (of 16.9 fluid ounces or less).

West Virginia’s existing tax on soft drinks is unusual because it has a much broader base than beverage taxes imposed elsewhere in the country. In West Virginia, almost all beverages are included in the base—including unsweetened beverages. This removes any consumer incentive to substitute unsweetened beverages for sugary drinks and makes little sense if the tax is intended to internalize externalities associated with sugar consumption. Historically, however, this tax has primarily existed for revenue generation, and that would be even more true under the sixfold increase in the governor’s plan.