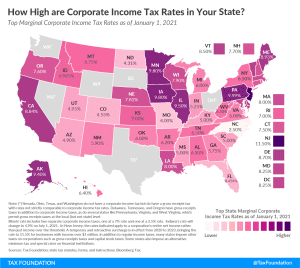

A $6 Billion Tax Increase Proposal in Pennsylvania Would Yield the Nation’s Highest Combined Flat-Rate Income Taxes

Under the budget introduced by Gov. Tom Wolf, Pennsylvania’s flat personal income tax rate would increase by 46 percent, partially offset by an outsized increase in the poverty credit, which would see a family of four eligible for partial relief due to poverty until they reached $100,000 in taxable income—four times the poverty line.

6 min read