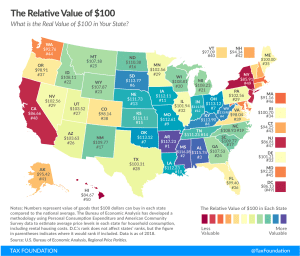

Real Value of $100 by Metropolitan Area, 2018

California is home to 7 of the 10 most expensive metro areas in America. See what’s the real value of $100 in your metro area with our new purchasing power map.

4 min read

California is home to 7 of the 10 most expensive metro areas in America. See what’s the real value of $100 in your metro area with our new purchasing power map.

4 min read

The fiscal response to the COVID-19 pandemic will require policymakers to consider what revenue resources should be used to fill budget gaps. Tax policy experts have proposed wealth taxes, (global) corporate minimum taxes, excess profits taxes, and digital taxes as opportunities for governments to raise new revenues.

20 min read

The LIHTC has subsidized over 3 million housing units since it was established in 1986, the largest source of affordable housing financing.

24 min read

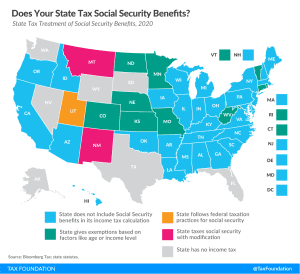

The question, “Does my state tax Social Security benefits?” may be simple enough, but the answer includes a lot of nuance. Many states have unique and specific provisions regarding the taxation of Social Security benefits, which can be broken into a few broad categories.

3 min read

Housing affordability was a major issue even before the COVID-19 crisis, but the current economic situation has made it more salient. Immediate support for people struggling makes sense now, but lawmakers should also consider long-term solutions to the problem of high rents, namely by expanding the supply of housing.

5 min read

First, the introduction of the wealth tax would significantly impact international capital flows and cause large economic dislocations in the short term. Second, provinces that are looking at raising their corporate tax rates might hinder capital attraction, growth, and economic recovery.

4 min read

According to news reports, the Vermont legislature is ready to advance S54 this month or next, to legalize cultivation and sales of marijuana in the state beginning in 2022.

6 min read

Individuals respond to taxes by changing their behavior. Hence, when there are tax differences between countries, some might respond by moving to a lower-tax area. For higher-income individuals, the benefits of moving as a result of higher taxes are greater because they have more income or wealth at stake.

4 min read

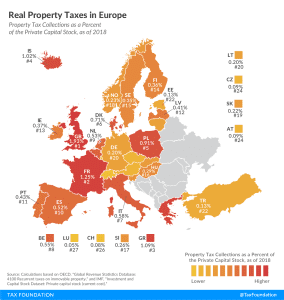

High property taxes levied not only on land but also on buildings and structures can discourage investment because they disincentivise investing in infrastructure, which businesses would have to pay additional tax on. For this reason, it may also influence business location decisions away from places with high property tax.

3 min read

When developing tax policy, lawmakers often ignore the incidence of a tax, or who actually pays the tax. Many times, this is different from who is legally required to pay the tax. Just because a 2 percent revenue tax applies to large digital companies does not mean that the companies will bear the entire cost of the tax.

1 min read

Aside from public health concerns, a ban on flavored tobacco, especially when including cigarettes, has significant tax implications and could result in unintended consequences such as increased smuggling. In Massachusetts, more than 20 percent of cigarettes smoked are purchased out of state.

5 min read

On Thursday, U.S. Senators Marco Rubio (R-FL), Bill Cassidy (R-LA), Steve Daines (R-MT), and Mitt Romney (R-UT) released the Coronavirus Assistance for American Families Act (CAAF), which would provide payments of $1,000 to adults and children with Social Security numbers, subject to income limits used in the original round of rebates. Among other modifications, it would be more generous to households and families with children when compared to the original rebates distributed under the CARES Act.

5 min read

Brazil has one of the world’s most complex tax systems. Brazil has the opportunity to implement a simple consumption tax and foster tax progressivity at the same time.

5 min read

Today marked the release of second-quarter GDP data and provides a new glimpse into early changes in state and local revenues and spending. All told, second-quarter state and local tax receipts came in about 3.8 percent lower than they did in the same quarter a year ago. Income and sales taxes fell considerably while property and excise tax collections remained stable.

3 min read

Senators Ted Cruz and Martha McSally introduced the CREATE JOBS Act that would make two significant changes to incentivize investment in the United States.

3 min read

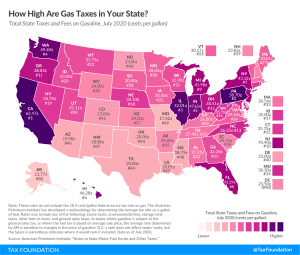

California pumps out the highest tax rate of 62.47 cents per gallon, followed by Pennsylvania (58.7 cpg), Illinois (52.01 cpg), and Washington (49.4 cpg).

2 min read

New data sheds light on what share of new business investment was eligible for bonus depreciation as it existed before 2017 tax reform, and what share of new investment was excluded from improved cost recovery. This matters because the income tax is biased against investment in capital assets to the extent that it makes the investor wait years or decades to claim the cost of machines, equipment, or factories on their tax returns.

3 min read

A resurgence in coronavirus cases and receding economic activity in many states threaten the nascent economic recovery. To address the ongoing crisis, the Senate Republican Phase 4 proposal builds on the CARES Act provisions while modifying others, including a scaled down federal UI benefit.

8 min read