As Congress attempts to prevent the expiration of major TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Cuts and Jobs Act (TCJA) provisions, it needs to find ways to pay for them. Ideally, it should use the least economically harmful means possible.

Eliminating tax exclusions for fringe benefits is one of the best options for policymakers to raise revenue. The largest of such benefits is the tax exclusion for employer-sponsored health insurance. However, there is a smaller, less-discussed option: employer-provided group-term life insurance.

Two goals of a well-designed tax system should be neutral treatment between saving and consumption and neutral treatment of different types of employee compensation. A tax system that’s neutral between saving and consumption applies the same effective tax rate to income consumed immediately and income saved and consumed later. Typically, that neutrality is achieved by taxing saving only once, either when money is first invested (Roth treatment) or when money is taken out to spend (traditional IRA or 401[k] treatment). And a tax system that’s neutral between different types of employee compensation would include all types of compensation in the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. .

The US tax code violates these ideals in many ways, including under Section 79 of the Internal Revenue Code, which excludes premiums paid by an employer for the first $50,000 of life insurance coverage from an employee’s taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. . This not only erodes the neutrality of employee compensation but also introduces a second layer of tax exemptions on saving.

Life insurance is a form of saving. Money is first “invested” when the policyholder pays premiums, and money is paid out to beneficiaries in the event of death. A neutral tax system would apply to one, and only one, of these transactions. Under current law, death benefits from life insurance are paid out to beneficiaries tax-free, which ensures only one layer of taxation. Life insurance premiums are normally taxable, but premiums for employer-provided coverage worth under $50,000 are not—meaning tax exemptions on the front end and the back end.

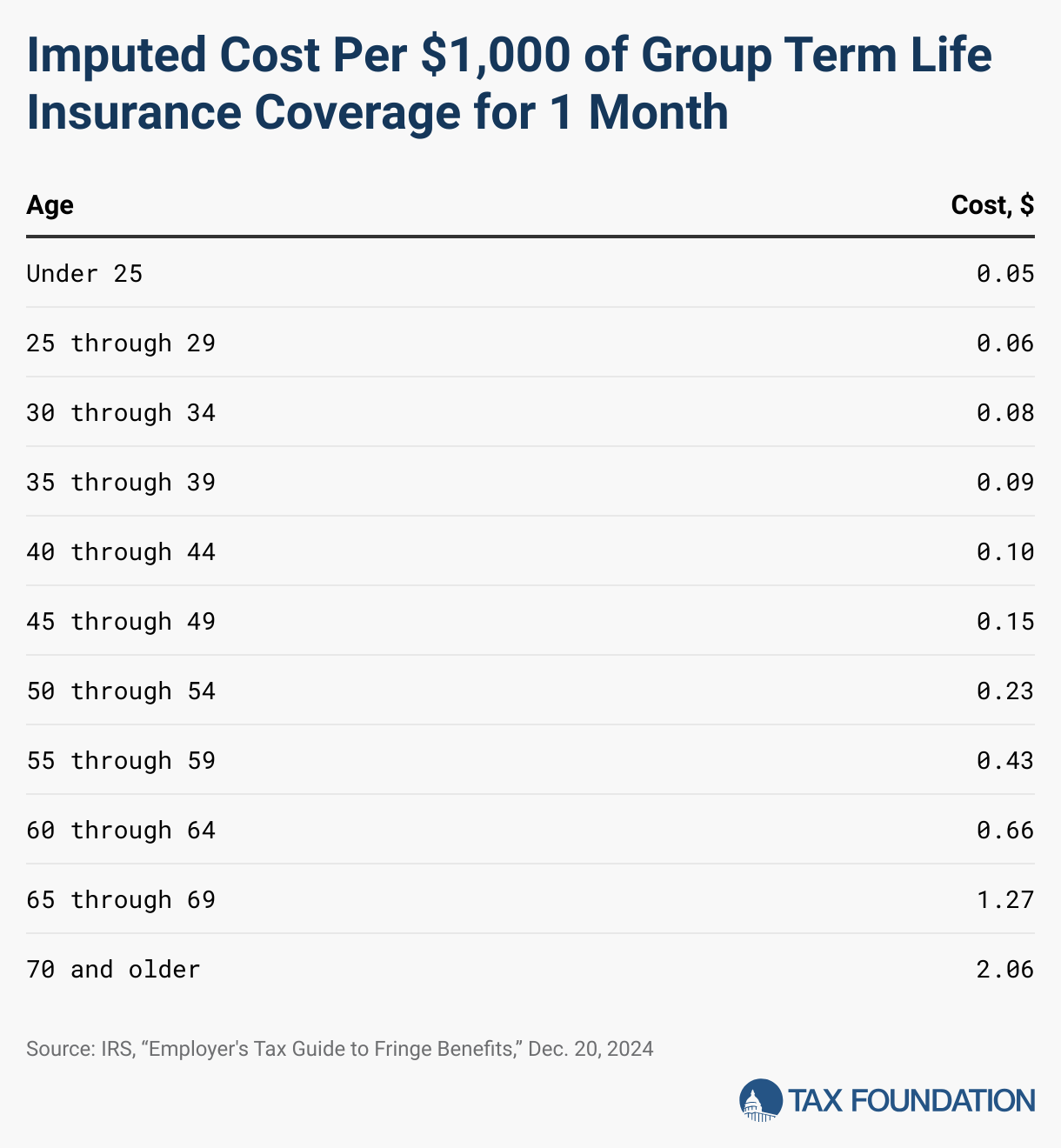

Employer-provided coverage above $50,000 shows up on an employee’s W-2 as imputed income. Imputed income isn’t based on the amount of premiums or actuarial cost (in essence, the value of the insurance coverage the employer is providing the employee), but on a predefined table determined by the IRS. For instance, based on the IRS table, $50,000 of group-term life insurance coverage over the course of a year for a 27-year-old employee would be valued at $36.

Using a predefined cost of insurance can lead to a misalignment where some taxpayers’ imputed incomes are higher or lower than the actuarial costs of coverage, which leads to either over-taxing or under-taxing. The tax exclusion also provides larger benefits to higher-income taxpayers thanks to the progressive structure of the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. . For example, a lower-income individual facing the bottom marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. of 10 percent only saves $10 in income taxes if they have $100 worth of excluded coverage, while a taxpayer facing the top marginal tax rate of 37 percent saves $37.

According to the Treasury Department, the exclusion of premiums on group-term life insurance under $50,000 of coverage will cost the Treasury almost $45 billion over the next 10 years. In an ideal system, the full value of premiums on group-term life insurance would be included in taxable income, and that value would reflect the actuarial cost of insurance.

Repealing the exclusion, along with the imputed income rules for employer-paid premiums, would raise additional revenue while improving the neutrality of the tax system.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe