In the first century of state income taxation, only four states transitioned from a graduated-rate to a single-rate, or flat, individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source structure. But the past four years have brought significant focus on income taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform and relief, and with that, something of a flat tax revolution.

Between 2021 and 2025, eight states enacted laws to transition to a flat individual income tax structure while providing income tax relief to taxpayers across the income spectrum. Six of those flat taxes have already been implemented, while two others are set to take effect in the future.

Specifically, Arizona enacted a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. law in July 2021, followed by Iowa in March 2022, Mississippi and Georgia in April 2022, and Idaho in September 2022. Louisiana joined them in December 2024, followed by legislation adopted in Kansas in April 2025 and Ohio in June 2025.

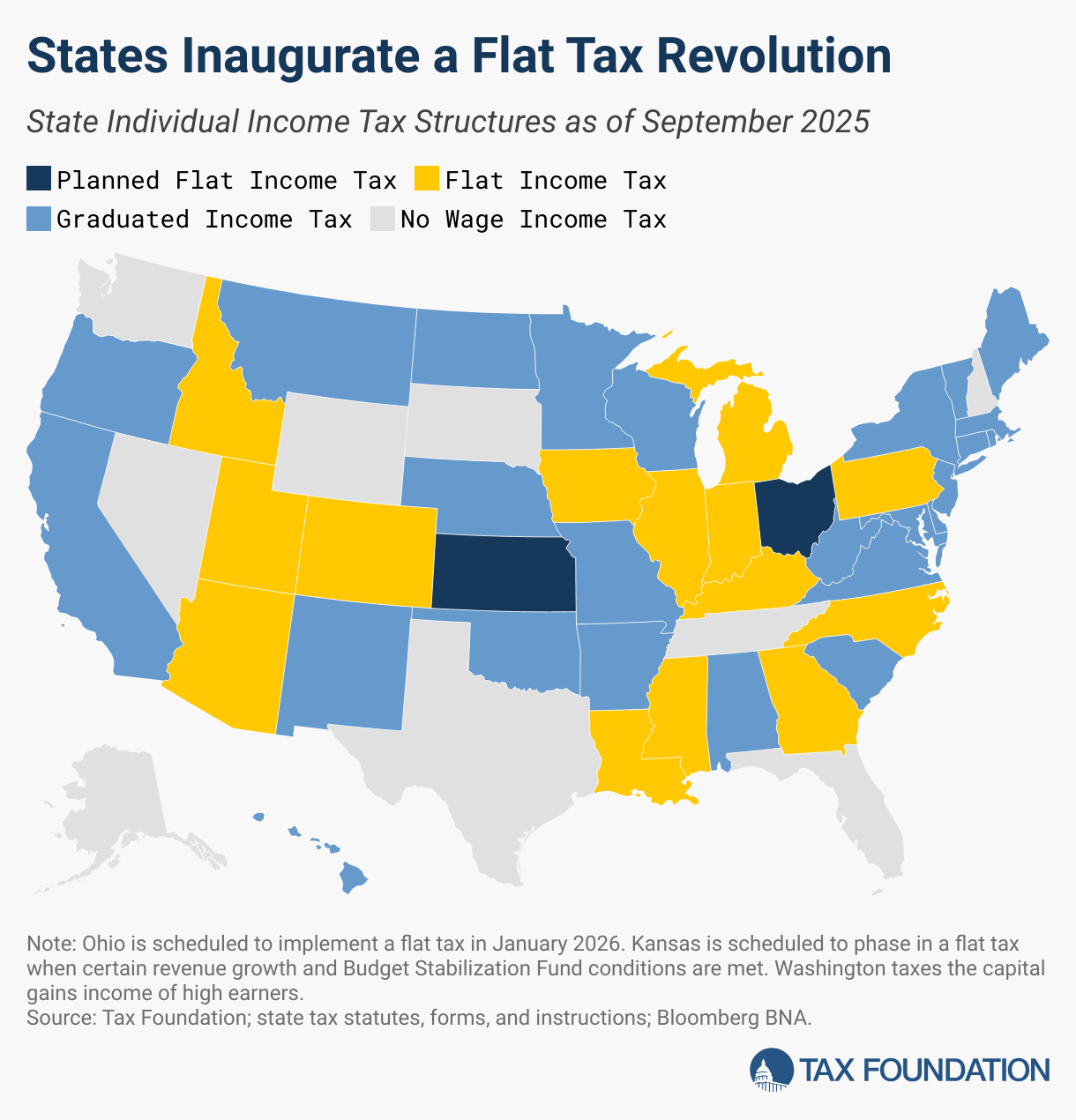

The flat taxes in Kansas and Ohio have not yet been implemented but are scheduled to take effect in future years. In Kansas, the timing of the transition to a flat rate of 4 percent is contingent upon specific revenue growth and Budget Stabilization Fund triggers. Ohio is scheduled to implement a low, flat rate of 2.75 percent in January 2026.

Recently, legislators in several additional states have seriously considered moving to a flat tax and could be on the cusp of making such a transition. In Kansas, various flat tax bills were vetoed by the governor in both 2023 and 2024, and it wasn’t until 2025 that legislators’ override attempts were successful. In Missouri and Oklahoma—two states with nearly flat bracket structures—lawmakers have recently considered the possibility of moving to a single-rate system. Flat tax deliberations continue in South Carolina as well.

Currently, 14 states have single-rate individual income tax structures, while nine states do not levy an individual income tax on wage or salary income at all. Twenty-seven states and the District of Columbia have graduated-rate structures, but two of those states (Ohio and Kansas) are on track to phase in a single-rate structure in the future.

A Brief History of State Income Tax Structure

In 1987, the 75th anniversary of state income taxation, Colorado replaced its half-century-old graduated-rate income tax with a single-rate tax. It would take another 30 years for another state to follow suit, when Utah implemented a flat tax in 2007. Next came North Carolina in 2014, as part of that state’s comprehensive reforms, followed by Kentucky in 2019. They joined five other states that already had flat taxes: Illinois, Indiana, Massachusetts, Michigan, and Pennsylvania. (Massachusetts’ flat tax has since been dismantled, with voters’ adoption in November 2022 of a constitutional amendment imposing a four percentage point surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. on income exceeding $1 million as of January 2023.)

The first state income tax, implemented in Wisconsin in 1912, had a two-rate structure. The first flat tax was Massachusetts’ tax, which went into effect in 1917. Five states had income taxes back then, with Massachusetts and Virginia both implementing them that January. Only five years passed between the first progressive income tax and the first flat income tax, but 75 years passed between the first progressive income tax and the first time one was transitioned from a graduated-rate to a single-rate structure. It took more than a century for the first four states—Colorado, Utah, North Carolina, and Kentucky—to make the transition from a graduated-rate to a single-rate structure, making it all the more notable that eight states—Arizona, Iowa, Mississippi, Georgia, Idaho, Louisiana, Kansas, and Ohio—enacted laws to make that same transition within a matter of only four years between July 2021 and June 2025.

Eight States Enacted Flat Tax Laws from 2021-2025

In July 2021, Arizona lawmakers enacted legislation to phase in a flat tax rate of 2.5 percent using tax triggers that made the timing of such a transition subject to revenue availability. This law was temporarily held up in litigation but received court clearance in 2022 to move forward, and, upon the tax triggers being met, a flat rate of 2.5 percent was implemented in January 2023.

Iowa, as part of a comprehensive tax reform law enacted in March 2022, began the process of phasing in a flat rate in 2023, with the initial goal of reaching a flat rate of 3.9 percent by 2026 to bring the state further and further away from the graduated-rate tax that not long ago topped out at 8.98 percent. In May 2024, in response to the state’s strong continued fiscal condition, Gov. Kim Reynolds (R) signed into law S.F. 2442, which accelerated the implementation of the flat tax by a year—to January 1, 2025—and reduced the rate further than initially planned, to 3.8 percent.

Mississippi’s flat tax, which took effect in 2023, was initially set at a rate of 5 percent, but that rate was reduced to 4.7 percent in 2024 and 4.4 percent in 2025 and is now scheduled to phase down to 4.0 percent in 2026, 3.75 percent in 2027, 3.5 percent in 2028, and 3.25 percent in 2029. Lawmakers have also adopted additional triggers that could yield further reductions subject to revenue availability in later years.

Georgia’s flat tax law, which was also adopted in 2022, took effect on January 1, 2024, moving the state to a single rate of 5.49 percent. Subsequent legislation adopted in 2024 retroactively reduced the rate to 5.39 percent for tax year 2024, and a law enacted in 2025 reduced the rate to 5.19 percent, retroactively effective as of tax year 2025. Subject to tax triggers that are contingent upon revenue availability, this rate could be reduced by 0.1 percentage points in future years until it reaches 4.99 percent.

In a 2022 special session, Idaho adopted a 5.8 percent flat tax, replacing the four-bracket tax structure that was previously in effect. This change was effective starting with the 2023 tax year. In 2024, the rate was retroactively reduced to 5.695 percent, and in 2025, the rate was retroactively reduced to 5.3 percent.

In December 2024, Louisiana lawmakers enacted a comprehensive tax reform law that moved the state to a single-rate individual income tax as of January 1, 2025. Specifically, this law consolidated Louisiana’s three brackets into one and reduced the rate to 3 percent, a significant reduction from the previous top marginal rate of 4.25 percent.

In April 2025, Kansas legislators overrode the governor’s veto of SB 269, setting the stage for the state’s future phase-in of a flat income tax. Specifically, this law dedicates individual and corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. collections growth above an inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin-adjusted FY 2024 baseline to be used to reduce income tax rates by a commensurate amount, beginning with the individual income tax. At the end of each fiscal year, if it is determined that real income tax revenue growth above the inflation-adjusted FY 2024 baseline has occurred and the Budget Stabilization Fund balance is at least 15 percent of the prior fiscal year’s general fund tax revenues, the state’s two marginal individual income tax rates of 5.2 percent and 5.58 percent will be reduced proportionally until a single rate of 4 percent is implemented.

Finally, in Ohio, H.B. 96, enacted in June 2025, retroactively reduced the state’s individual income tax rates for 2025 and scheduled a reduction to a flat rate of 2.75 percent to take effect on January 1, 2026.

Benefits of Moving to a Flat Tax Structure

Supporters of flat taxes often identify their simplicity as one of their salient features. This is true, but it’s important to stop and ask what is meant by this. It is not enough to merely state that a single rate is simpler than multiple rates, because, while trivially true, that tells us relatively little. It is not particularly difficult to use tax tables to ascertain one’s tax liability.

Flat taxes are meaningfully simple, however, in several ways. State revenue forecasting—as well as projecting the revenue effects of potential tax changes—is far more easily accomplished under a single-rate tax structure. Flat taxes also make it easier for taxpayers to estimate their tax liability and how it would change under different income scenarios, enhancing tax transparency and potentially improving some taxpayers’ economic decision-making.

Flat taxes also accord better with taxpayers’ impressions of tax burdens based on headline rates. Individuals and small businesses may be more attracted to a state with a relatively lower flat rate than one with a graduated-rate system, even if the two systems yield similar liabilities. Flat taxes also simplify the function by which taxpayers decide whether to work or invest more on the margin, since all marginal returns to labor and investment are exposed to the same rate.

Of greater significance for taxpayers, however, is that flat-rate income taxes tend to function as a bulwark against unnecessary tax increases, and to provide greater certainty for individual and business taxpayers. Economic decisions are made on the margin; choices about investments, labor, or relocation will be made on the basis of the effect on the next dollar of income, not the prior ones. A competitive top marginal rate matters most for economic growth, and flat income taxes—given their “all-in” nature—not only mean a lower rate on that all-important margin, but they tend to be harder to raise in the future, whereas highly graduated taxes are more susceptible to targeted, but often economically inefficient, tax hikes. Notably, all four states that transitioned from a graduated-rate to a single-rate individual income tax before 2023 now have flat rates that are between 0.6 and 1.55 percentage points lower than they were when the transition to a flat tax first occurred.

Taxpayers seem to sense this intuitively: in Illinois, for instance, voters in November 2020 lopsidedly rejected a constitutional amendment that would have permitted a graduated-rate structure even though the rates initially proposed by the General Assembly would not have increased tax liability for the vast majority of voters and would, in fact, have initially reduced tax liability for some. Illinoisans seemed to recognize that, once the principle of a graduated-rate structure is established, it would become far easier for lawmakers to raise income tax rates on more and more taxpayers in the future—even setting aside the negative implications moving away from a flat tax would have had for the state’s economic competitiveness.

This is one reason why states with nearly flat income taxes should consider finishing the job, as Georgia, Idaho, and Mississippi have recently done. In Alabama, for instance, the current three-bracket system, with the top rate kicking in at $3,000 of income for single filers, only provides $40 in tax savings compared to taxing all income at the top rate. Raising the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. would easily provide the same progressive benefits while embracing the simplicity and—more importantly—the certainty and stability of a single-rate tax. Three other states—Arkansas, Missouri, and Oklahoma—likewise have top rates that kick in at or below $10,000 for single filers, and these are all states in which continued income tax reform and relief remain a priority.

Three States Have Nearly Flat Graduated-Rate Income Taxes

| State | Brackets | Top Rate Kick-In (2025, Single Filers) | Maximum Savings |

|---|---|---|---|

| Alabama | 3 | $3,000 | $40 |

| Missouri | 7 | $9,191 | $175 |

| Oklahoma | 6 | $7,200 | $188 |

These states now present an opportunity for reform culminating in a flat tax, but they also serve as a cautionary tale about the implications of not indexing a graduated-rate income tax. When Alabama adopted its graduated-rate income tax in 1935, the majority of taxpayers were fully exempt, and few taxpayers were subject to the top marginal rate of 5 percent on income above $3,000, which is equivalent to approximately $69,000 in 2025, higher than today’s median household income in the state and a small fortune in Depression-era Alabama. Over time, the lack of inflation indexing has subjected the vast majority of taxpayers’ income to the top marginal rate, making it similar to a single-rate tax.

Of the 14 states that already have flat taxes, four enshrine that status in their state constitutions, locking in the benefit and making it harder for lawmakers to raise taxes by switching to a progressive taxA progressive tax is one where the average tax burden increases with income. High-income families pay a disproportionate share of the tax burden, while low- and middle-income taxpayers shoulder a relatively small tax burden. regime. This is a particularly important protection for small business owners, since about 95 percent of all businesses are pass-through businesses subject to individual, not corporate, income taxes, and the vast majority of pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. income is earned by companies exposed to states’ top marginal income tax rates. In Illinois, for instance, where lawmakers in 2020 championed a failed constitutional amendment to permit a graduated-rate income tax, 93 percent of pass-through business income was on returns with more than $200,000 in adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods (AGI), and over half of all pass-through business income was reported on returns showing more than $1 million in AGI. Hiking the top marginal rate is not just about the wealthy; it is about the state’s small businesses, too, and about providing a greater level of certainty for entrepreneurs making location decisions.

States that currently have flat taxes but that have not yet constitutionally protected their single-rate tax structures should consider doing so. The following table shows states that currently have a flat tax, their date of implementation, and whether a single-rate tax is constitutionally mandated. Of the four states that have had flat taxes from the start, three enshrine this status in their constitution. Of the 10 that transitioned, only one does.

Fourteen States Have Flat Income Taxes

| State | PIT Adopted | Flat As Of | Constitutional |

|---|---|---|---|

| Arizona | 1933 | 2023 | |

| Colorado | 1937 | 1987 | ✓ |

| Georgia | 1929 | 2024 | |

| Idaho | 1931 | 2023 | |

| Illinois | 1969 | Always | ✓ |

| Indiana | 1965 | Always | |

| Iowa | 1934 | 2025 | |

| Kentucky | 1936 | 2019 | |

| Louisiana | 1934 | 2025 | |

| Michigan | 1967 | Always | ✓ |

| Mississippi | 1912 | 2023 | |

| North Carolina | 1921 | 2014 | |

| Pennsylvania | 1971 | Always | ✓ |

| Utah | 1971 | 2007 |

From 2021 to 2025, within the span of four years, more states enacted laws converting graduated-rate individual income tax structures into single-rate income tax structures than did so in the whole 108-year history of state income taxation up until that point. In several additional states, lawmakers are working to see that this momentum continues. For states that want to remove barriers to upward mobility and business investment while promoting long-term economic growth and enhancing their competitive standing, moving from a graduated-rate to a single-rate individual income tax structure while reducing the top marginal rate is among the most valuable tax reforms lawmakers could adopt.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe