FAQ: The One Big Beautiful Bill, Explained

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.

24 min readThe 2017 Trump Tax Cuts, known as the Tax Cuts and Jobs Act (TCJA), reduced average tax burdens for taxpayers across the income spectrum and temporarily simplified the tax filing process through structural reforms. It also boosted capital investment by reforming the corporate tax system and significantly improved the international tax system.

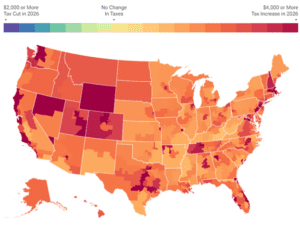

At the end of 2025, the individual portions of the Tax Cuts and Jobs Act expire all at once. Without congressional action, 62 percent of filers could soon face a tax increase relative to current policy in 2026. At the same time, the price tag for extending the 2017 Trump tax cuts is in the trillions.

Explore our related resources below, including our tariff tracker, our budget reconciliation tracker, our latest analysis and reform options regarding TCJA permanence, our interactive tax calculator and congressional districts map, and how 2026 brackets would change if the TCJA expires.

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.

24 min read

Several major new tax breaks are scheduled to expire at the end of 2028, setting the stage for another tax fight to either extend them or allow them to expire.

5 min read

The One Big Beautiful Bill Act makes many of the individual tax cuts and reforms of the TCJA permanent. It improves upon the TCJA by making expensing for R&D and equipment permanent. However, for the most part, it does not include further structural reforms, and instead introduces many new, narrow tax breaks to the code, adding complexity and raising revenue costs.

7 min readPresident Trump signed the One Big Beautiful Bill Act into law on July 4, 2025.

18 min read

Permanently extending the Tax Cuts and Jobs Act would boost long-run economic output by 1.1 percent, the capital stock by 0.7 percent, wages by 0.5 percent, and hours worked by 847,000 full-time equivalent jobs.

6 min read

Unless Congress acts, Americans are in for a tax hike in 2026.

3 min read

At the end of 2025, the individual tax provisions in the Tax Cuts and Jobs Act (TCJA) expire all at once. Without congressional action, most taxpayers will see a notable tax increase relative to current policy in 2026.

4 min read

Policymakers should have two priorities in the upcoming economic policy debates: a larger economy and fiscal responsibility. Principled, pro-growth tax policy can help accomplish both.

21 min read

If Congress allows the Tax Cuts and Jobs Act (TCJA) to expire as scheduled, most aspects of the individual income tax would undergo substantial changes, resulting in more than 62 percent of tax filers experiencing tax increases in 2026.

3 min read

Lawmakers should see 2025 as an opportunity to consider more fundamental tax reforms. While the TCJA addressed some of the deficiencies of the tax code, it by no means addressed them all.

8 min read

Given that U.S. debt is roughly the size of our annual economic output, policymakers will face many tough fiscal choices in the coming years. The good news is there are policies that both support a larger economy and avoid adding to the debt.

6 min read

While federal tax collections—especially corporate taxes—have reached historically high levels, these gains have not kept pace with escalating spending, particularly on debt interest, leading to a substantial and concerning budget deficit in FY24.

6 min read

The TCJA improved the U.S. tax code, but the meandering voyage of its passing and the compromises made to get it into law show the challenges of the legislative process.

6 min read

The Tax Cuts and Jobs Act’s changes to family tax policy serve as a reminder to avoid looking at tax reform provisions in a vacuum.

5 min read

The Tax Cuts and Jobs Act (TCJA) significantly lowered the effective tax rates on business income, but the impact was not the same for C corporations and pass-through businesses.

6 min read

As lawmakers consider which policies to prioritize in the upcoming tax policy debates, better cost recovery for all investment should be top of mind.

7 min read

Pro-growth tax reform that does not add to the deficit will require tough choices, but whether to raise the corporate tax rate is not one of them. If lawmakers want to craft fiscally responsible and pro-growth tax reform, a higher corporate tax rate simply does not fit into the puzzle.

3 min read

The 2017 Tax Cuts and Jobs Act (TCJA) was the largest corporate tax reform in a generation, lowering the corporate tax rate from 35 percent to 21 percent, temporarily allowing full expensing for short-lived assets (referred to as bonus depreciation), and overhauling the international tax code.

6 min read

As members of Congress prepare to address the expiration of the TCJA, they should appreciate how revenues have evolved since 2017.

4 min read

While the approaches differ, they share a reliance on similar linkages: new capital investment drives productivity growth, which grows the economy and raises wages for workers.

37 min read

The Tax Cuts and Jobs Act of 2017 (TCJA) reformed the U.S. system for taxing international corporate income. Understanding the impact of TCJA’s international provisions thus far can help lawmakers consider how to approach international tax policy in the coming years.

30 min read

The OBBBA made substantial improvements to cost recovery, but more opportunities remain for policymakers looking to improve the investment climate in the US.

48 min read

Rather than adopt temporary policies that phase out and expire, policymakers should focus their efforts on long-term reforms to support investment.

7 min read

The Tax Foundation uses and maintains a General Equilibrium Model, known as our Taxes and Growth (TAG) Model to simulate the effects of government tax and spending policies on the economy and on government revenues and budgets.

9 min read

The 12-year history of Tax Foundation’s ITCI shows that tax policy is constantly in flux around the world and that tax policy design choices matter for economic growth.

5 min read

Foreign R&D generally complements domestic innovation rather than substituting for it, so penalizing foreign R&D weakens US firms in cross-border mergers and acquisitions and in domestic production that depends on global scale.

7 min read

Just as many parts of American life have transformed over the past 250 years, so too has the federal tax system. While most taxes levied in the 18th century are still levied in some form today, the federal government’s reliance on them, the complexity of the tax code, and Americans’ overall tax burdens have shifted considerably.

5 min read

Revenue-neutral proposals, like many things in politics, have become a relic of the past.

This study simulates several large tax increases and consistently finds that even tax increases large enough to close the primary deficit in the near term will lose ground over time and fail to put the debt on a sustainable course.

41 min read

In 2022, incomes for the bottom 80 percent of earners were slightly lower after taxes and transfers compared to 2020 and 2021, driven by expiring pandemic-era policies.

6 min read

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).

6 min read

Policymakers should broaden and make permanent full expensing for additional asset classes and pursue structural reforms that reduce distortions in how businesses are taxed. A more consistent and predictable policy environment, paired with targeted improvements to loss treatment, R&D incentives, and compliance burdens, would give small business owners greater confidence to invest, hire, and grow.

The US, as the world’s largest services exporter, has a stronger interest in combating discriminatory services taxation than in pursuing tariffs.

44 min read

The past decade’s record suggests that countries have reliable legislative methods to improve their tax systems through ordinary tax reforms.

22 min read

Smaller corporate tax bills after the OBBBA are not evidence of new giveaways or loopholes. They are evidence the tax code is finally treating investment the way it should.

Ohio’s SB 9 will boost economic growth by conforming Ohio’s tax code to the domestic research and experimentation (R&E) immediate cost recovery provision in the One Big Beautiful Bill Act.

8 min read

What is a border adjustment? Is it a new idea? How would it work in practice?

11 min read

The tariffs now in effect threaten to offset much of the GDP growth from the tax cuts, while falling short of paying for them.

3 min read

Notably, the OBBBA makes permanent the individual tax changes first put in place by the TCJA, which avoids a tax hike on an estimated 62 percent of tax filers in 2026.

4 min read

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections. How do income taxes compare in your state?

9 min readOur analysis of the major tax provisions included in the OBBBA finds it will increase long-run GDP by 0.7 percent. The major tax provisions will reduce federal tax revenue by nearly $5.2 trillion between 2025 and 2034, on a conventional basis.

12 min read