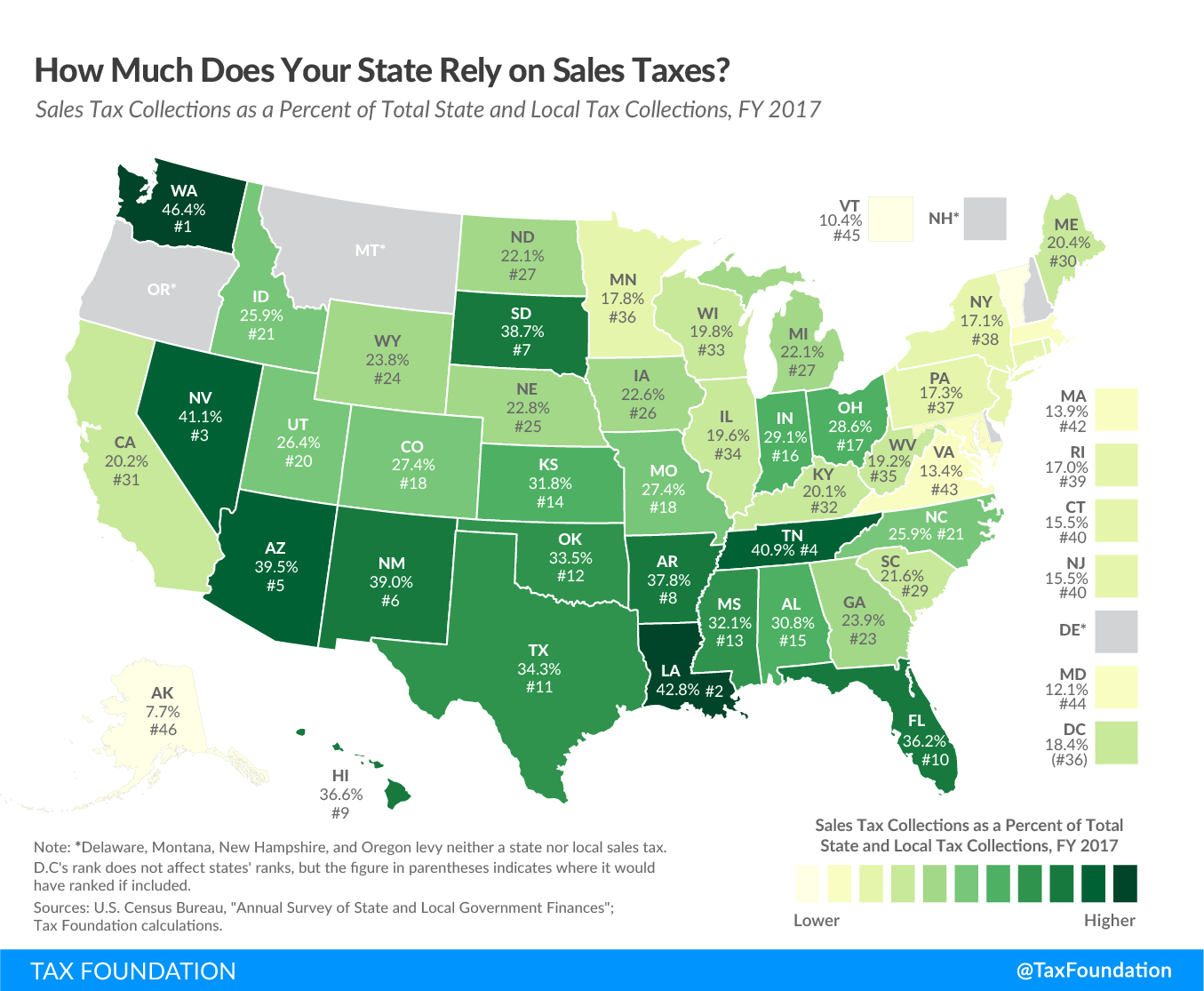

This week’s map continues our look at state revenue sources, this time focusing on revenue collected through the general sales tax.

Sales taxes are the second largest source of state and local taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue, accounting for 23.6 percent of total U.S. state and local tax collections in fiscal year 2017 (the latest data available; see Facts & Figures Table 8). Only property taxes make up a greater share of state and local tax revenue.

Consumption taxes, like sales taxes, are more economically neutral than taxes on capital and income because they target only current consumption. Income taxes fall on both present and future consumption, thus partially acting as a tax on investment by capturing savings.

Consumption taxes are generally more stable than income taxes in economic downturns as well, although the current coronavirus outbreak differs from other crises in that consumption has dropped dramatically due to the nature of pandemics.

While 45 states levy a statewide sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. and 38 allow localities to collect separate sales taxes, four states levy neither a state nor a local sales tax: Delaware, Montana, New Hampshire, and Oregon (see Facts & Figures Table 19). Eight states levy a sales tax at the state, but not the local, level: Connecticut, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, and Rhode Island. Alaska is the only state that permits local sales taxes without imposing a state sales tax.

Today’s map compares the extent to which sales taxes are responsible for tax revenue generation in each state. Washington State—which has neither a corporate nor an individual income tax but levies a harmful gross receipts tax on businesses—relies the most on sales tax revenue, which accounts for 46.4 percent of its total tax collections. Louisiana is the second-most reliant on sales tax revenue, with 42.8 percent of tax collections attributable to sales taxes. Nevada, which does not have an income tax, comes in third with 41.1 percent of state and local tax collections. Tennessee, which does not tax wage income and will fully repeal its tax on investment income by next year, is next with 40.9 percent.

Although Washington, Nevada, Tennessee, and South Dakota (38.7 percent) all rely heavily on the sales tax, they are not high-tax states. All four states forgo an individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source and choose to raise a large portion of their revenue through the sales tax instead. South Dakota additionally forgoes corporate income taxes. Wyoming does not levy individual or corporate income taxes either but manages to land near the middle of the pack (23.8 percent) in terms of sales tax reliance due to its heavy reliance on severance tax collections. This trade-off between income and sales can be a good thing, as it allows states to avoid relying on the less economically neutral individual income tax.

Many factors can affect sales tax reliance. States and localities that border low-sales tax or no-sales tax jurisdictions often struggle to levy sales taxes with high rates, as these could prompt consumers to shop across the border.

Another consideration is the tax base, the transactions that are subject to the sales tax. The most neutral form of sales tax would fall on final consumption of both goods and services at a low rate, while exempting business inputs. In practice, though, many states fall short of this ideal due to historical accident or policy decisions to exempt certain classes of goods.

Note: This is part of a map series in which we examine the primary sources of state and local tax collections

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe