Key Findings

- In theory, the carbon taxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them. is the most efficient approach to address climate change.

- In practice, however, the policymaking process can interfere and weaken the policy.

- We consider several theoretical arguments for carbon taxes and the evidence from carbon taxes implemented around the world related to emissions, economic growth, distribution and revenue recycling options, other environmental taxes, green subsidies, and environmental regulations.

- Most of the major arguments hold up well: the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. is not a significant drag on economic growth, it reduces emissions, and the revenue is usually returned to taxpayers by reducing other taxes.

- One argument in particular falls short: the tax is rarely accompanied by complementary efforts to streamline environmental policymaking.

- When looking at carbon taxes around the world, the United States can find some aspects to emulate and others to avoid.

- While it might be difficult to transfer the exact theoretical carbon tax into practice, a next-best, real-world carbon tax is certainly achievable.

Introduction

Among economists, the carbon tax is a popular solution to climate change.[1]

The case for the carbon tax is clear in the abstract. Find out the social cost of carbon emissions, then tax carbon emissions at that rate. The approach has numerous benefits: for one, it allows the market to determine the most efficient ways to reduce emissions. Additionally, it is one all-encompassing climate policy, simplifying the tax and regulatory environment by replacing numerous interlocking sector- and industry-level subsidies, regulations, and narrow excise taxes. Unlike other climate policies, carbon taxes also produce revenue, creating opportunities for reducing other, more economically harmful taxes—meaning the policy can have twin environmental and economic benefits.

But carbon taxes (and their cousin, cap and trade) are not purely theoretical exercises.[2] As of April 2022, 70 carbon pricing initiatives at regional, national, and subnational levels around the world cover more than 23 percent of all global CO2 emissions combined.[3] The 36 existing carbon taxes alone cover 5.7 percent of global CO2 emissions.

Translating an idea from basic economic theory into policy can be difficult. While it may be easy to object on the grounds that “a carbon tax may be sound in theory, in practice it would not deliver on these benefits,” it is a legitimate concern. However, with dozens of carbon taxes enacted around the world, we can assess how those theoretical arguments have translated in practice—we do not need to theorize about administrative challenges.

On broad economic questions, the evidence is favorable. Carbon taxes have helped reduce carbon emissions, with comparatively low costs. Most revenue has either been used to reduce existing taxes or substitute for other potential tax increases, thus often improving economic growth on net. However, fewer examples show the carbon tax cutting the Gordian Knot of climate policy. Many carbon taxes only cover a portion of emissions and coexist with regulatory regimes and subsidy schemes, rather than acting as a totalizing policy.

Emissions

Emissions: In Theory

Carbon taxes will reduce emissions. However, the extent of the reduction depends on elasticity, or how responsive people are to changes in prices. If the price elasticity of emissions is high, a carbon tax will result in significant emissions reductions as people stop polluting to avoid bearing the tax. If the price elasticity of emissions is low, then polluters will mostly choose to bear the tax’s burden instead of changing their behavior.

The Energy Modeling Forum (EMF) recently composed a meta-analysis of 11 different models of four different carbon tax scenarios: a $25 carbon tax, rising 1 percent per year; a $25 carbon tax, rising 5 percent per year; a $50 carbon tax, rising 1 percent per year; and a $50 carbon tax, rising 5 percent per year.[4] These constitute large reductions in carbon emissions.

| Scenario | Range of Emissions Reductions after 5 Years | Range of Emissions Reductions after 15 Years |

|---|---|---|

| $25 per ton, rising 1% per year | 16-28% | 17-38% |

| $50 per ton, rising 5% per year | 21-35% | 26-47%* |

|

Source: Alexander R. Barron, Allen A. Fawcett, Marc A. Hafstead, James R. McFarland, and Adele C. Morris, “Policy Insights from the EMF 32 Study on U.S. Carbon Tax Scenarios,” Climate Change Economics 9:1 (2018), https://www.worldscientific.com/doi/10.1142/S2010007818400031. *One model with more aggressive assumptions about the impact of carbon taxes on carbon emissions did not run a $50 per ton carbon tax rising at 5 percent per year, meaning there may be larger higher-end scenarios. |

||

One consensus finding across all the EMF models is that the electricity sector would be the most responsive to the carbon tax, driving a majority of the total emissions reduction.

The EMF project also notes some shortcomings of the model. Part of the theoretical case for carbon taxes is that they will increase incentives for the development of new, low-emission or no-emission technologies, but modeling technological leaps is a challenge. While models can assess how people would respond to a carbon tax with the technology we have today, they are less effective in predicting technological advancement. For instance, a model can predict that rising gas prices from a carbon tax would not significantly reduce miles driven because driving tends to be relatively nonresponsive to price changes, but it cannot accurately predict a change in demand for and technological development of electric cars.

Nonetheless, well-documented evidence shows increases in energy prices drive energy innovation.[5] More recent modeling applies the induced innovation concept to carbon taxes and finds a 19 percent more effective reduction in emissions.[6]

Another source of uncertainty about a carbon tax’s impact on emissions is international markets. One concern about a carbon tax (and many other environmental policies) is the offshoring of pollution, also known as carbon leakage.[7] The idea here is simple: by raising the cost of pollution in the taxed jurisdiction, polluters will simply move their operations to an untaxed jurisdiction and continue to sell their products to consumers in the taxed jurisdiction. Under this scenario, while domestic emissions go down, global carbon emissions are unchanged, and the domestic economy suffers as polluting industries move abroad.

One causal channel, however, suggests carbon taxes in one jurisdiction could lower emissions in other jurisdictions as well: innovation.[8] When a major jurisdiction adopts a carbon price that induces green technological change and development, that technology can become economical for other untaxed jurisdictions to adopt over time.

Effects on Emissions: In Practice

Existing evidence suggests carbon taxes do reduce emissions, as basic economic theory indicates. The impact on emissions varies greatly with the rate and the scope of the tax.

Most of the long-lived examples of carbon taxes fall short of the idealized policy in several ways. For the purposes of discussing relatively established carbon taxes and their impacts on emissions, the most relevant departure from idealized policy is the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. . Many carbon taxes exclude a significant portion of the tax base, and, as such, the “carbon tax” reduces emissions less than a true tax on all carbon emissions would. Below includes a brief discussion of carbon taxes that have been around for several years, covering reasonably large economic areas, with rates of at least $5 per ton of carbon, and a tax base of at least 20 percent of domestic carbon emissions.[9]

Of the many existing carbon taxes, the carbon taxes of Sweden, British Columbia, and the United Kingdom are useful examples for a few reasons. The policies have been around for a long time, providing ample opportunity for economic actors to respond and for economists to study the effects.[10] The carbon taxes are all levied at an economically significant rate on a non-trivial share of the carbon emissions in the country, so we can realistically expect them to have an effect on emissions.[11] The economies are all relatively large, increasing the likelihood that a larger body of research exists and removing some possible idiosyncrasies associated with being a small nation.[12]

Sweden, British Columbia, and the United Kingdom are not the only jurisdictions to fit these criteria—Switzerland and the three other Nordic countries, Finland, Norway, and Denmark, could have all also qualified. But Sweden is the largest economy of the four Nordics, and Sweden, British Columbia, and the United Kingdom provide a broad variety of examples: a Nordic country, a North American province, and a Western European country. Additionally, this paper is not limited to these three carbon taxes: we will discuss carbon taxes in other jurisdictions, including Australia’s canceled carbon tax, in the context of other variables of interest.

Sweden

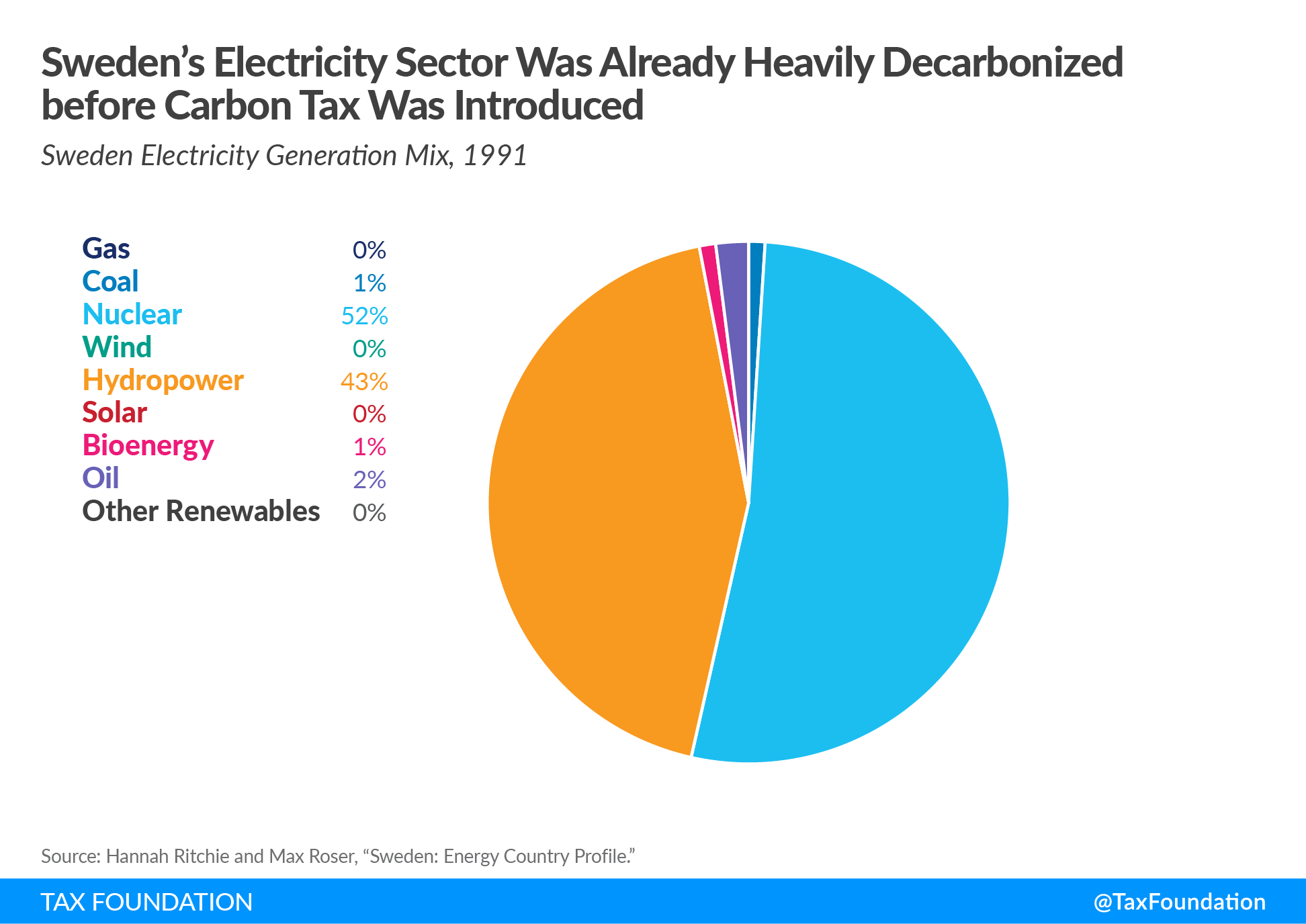

Sweden enacted a carbon tax in 1991. Initially, the carbon tax was levied at $26 per ton (converted to U.S. dollars), before rising to around $95 per ton by 2004 and $130 per ton today. It applies to roughly 40 percent of Sweden’s carbon emissions, as it excludes industrial sector emissions covered by the EU’s emissions trading system (ETS)—an EU-level cap and trade carbon pricing scheme—among other emissions. The tax mostly falls on fossil fuels used for transportation and heating.[13] The carbon tax, however, was only one of several Swedish environmental policies enacted since the 1990s.[14]

When the Swedish carbon tax was introduced, policymakers reduced, but still maintained, a separate, significant tax on energy use. As a result, the net effect of introducing a carbon tax on the total tax rate on electricity was not as large as one might expect based on the high carbon tax rate.[15] Furthermore, the Swedish electricity sector was already heavily decarbonized, with 95 percent of Swedish electricity in 1991 coming from either nuclear or hydroelectric power.[16] Nevertheless, between 1991 and 2021, Sweden’s carbon dioxide emissions fell by more than 37 percent.[17] An empirical analysis of Sweden’s carbon tax found it reduced transportation emissions by 6 percent.[18] While it is a reduction in emissions, it seems relatively modest when contrasted with the more substantial emissions reduction potential of a carbon tax modeled in the EMF studies. However, after considering that Sweden’s electricity sector was already largely decarbonized, the more modest reduction makes more sense.

British Columbia

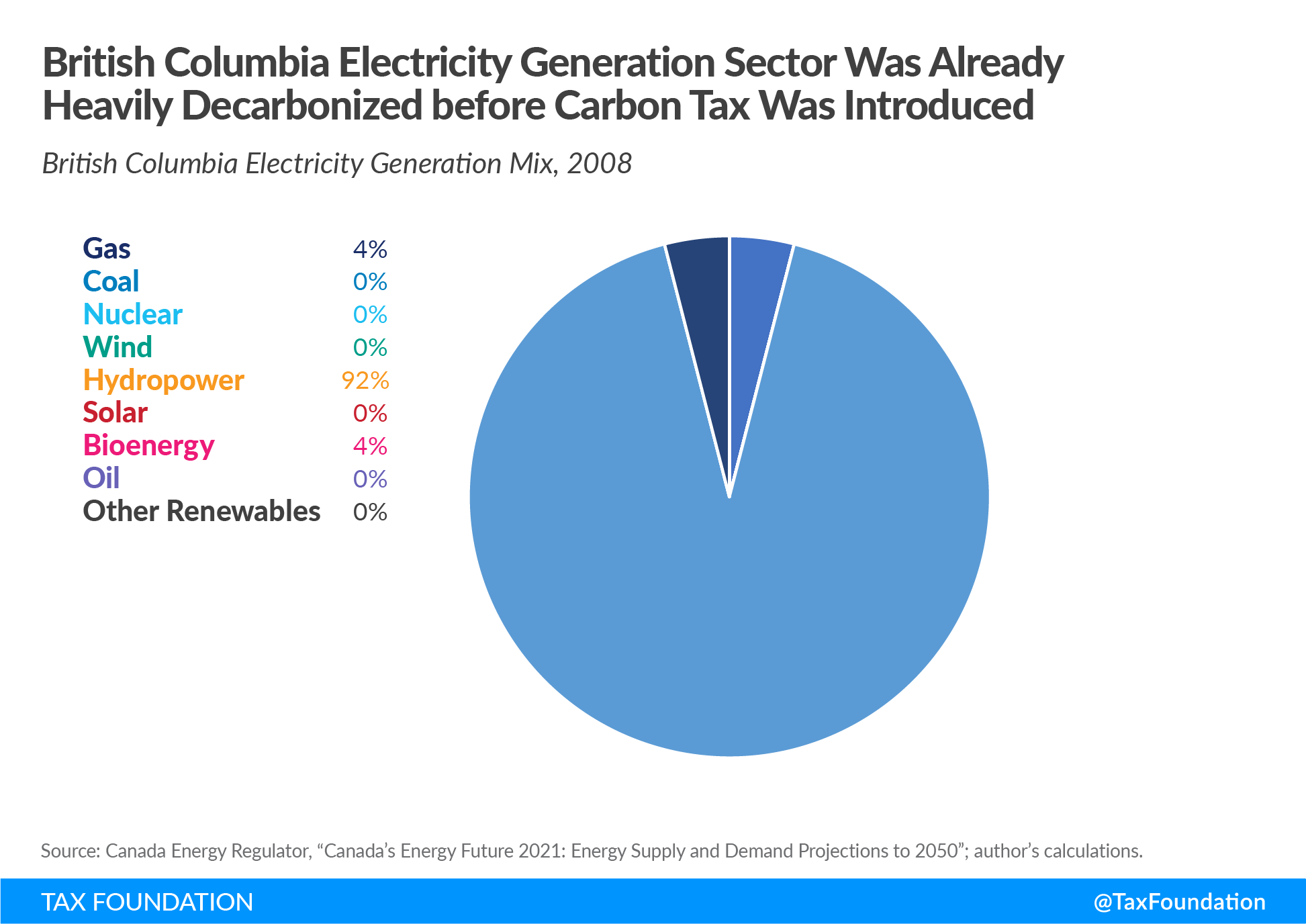

The Canadian province of British Columbia enacted a carbon tax in 2008.

British Columbia provides a more promising example than Sweden. Instead of a high tax applied to a narrow base, the British Columbia tax applied a low-to-moderate tax to a broad base. The existing evidence suggests the tax has lowered emissions. In the first few years of the tax’s introduction, it reduced aggregate emissions by between 5 and 15 percent.[19] That includes an estimated 4 percent reduction in emissions from manufacturing and an estimated 8 percent reduction in emissions from gasoline for private vehicles, while primarily commercial diesel emissions fell by less.[20]

The successful emissions reduction comes even with some idiosyncrasies related to British Columbia’s baseline, which somewhat mutes a carbon tax’s potential. As discussed previously, most modeling suggests carbon taxes have the largest effect on emissions in the power generation sector, incentivizing producers to switch from coal to natural gas or renewables. But when British Columbia introduced the carbon tax, it already got most of its electricity from hydroelectric power.[21]

United Kingdom

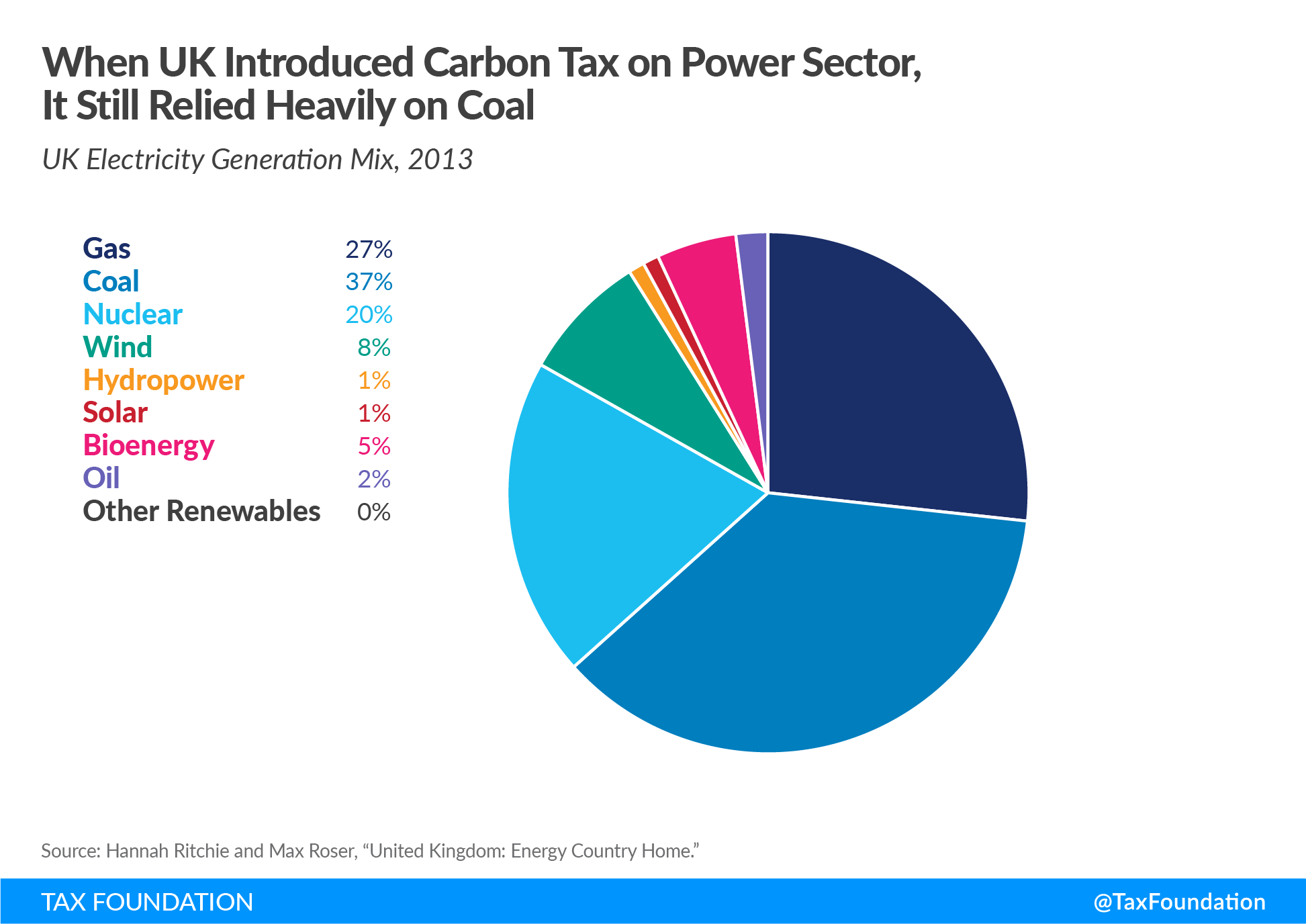

The United Kingdom adopted a carbon tax in 2013. The UK carbon tax provides a contrast to the Scandinavian and British Columbian examples. While the UK tax rate is relatively low (around $23 per ton) and the tax base is relatively narrow (only covering 21 percent of emissions), the UK carbon tax’s base falls on the power generation sector, which is much more responsive to taxation.

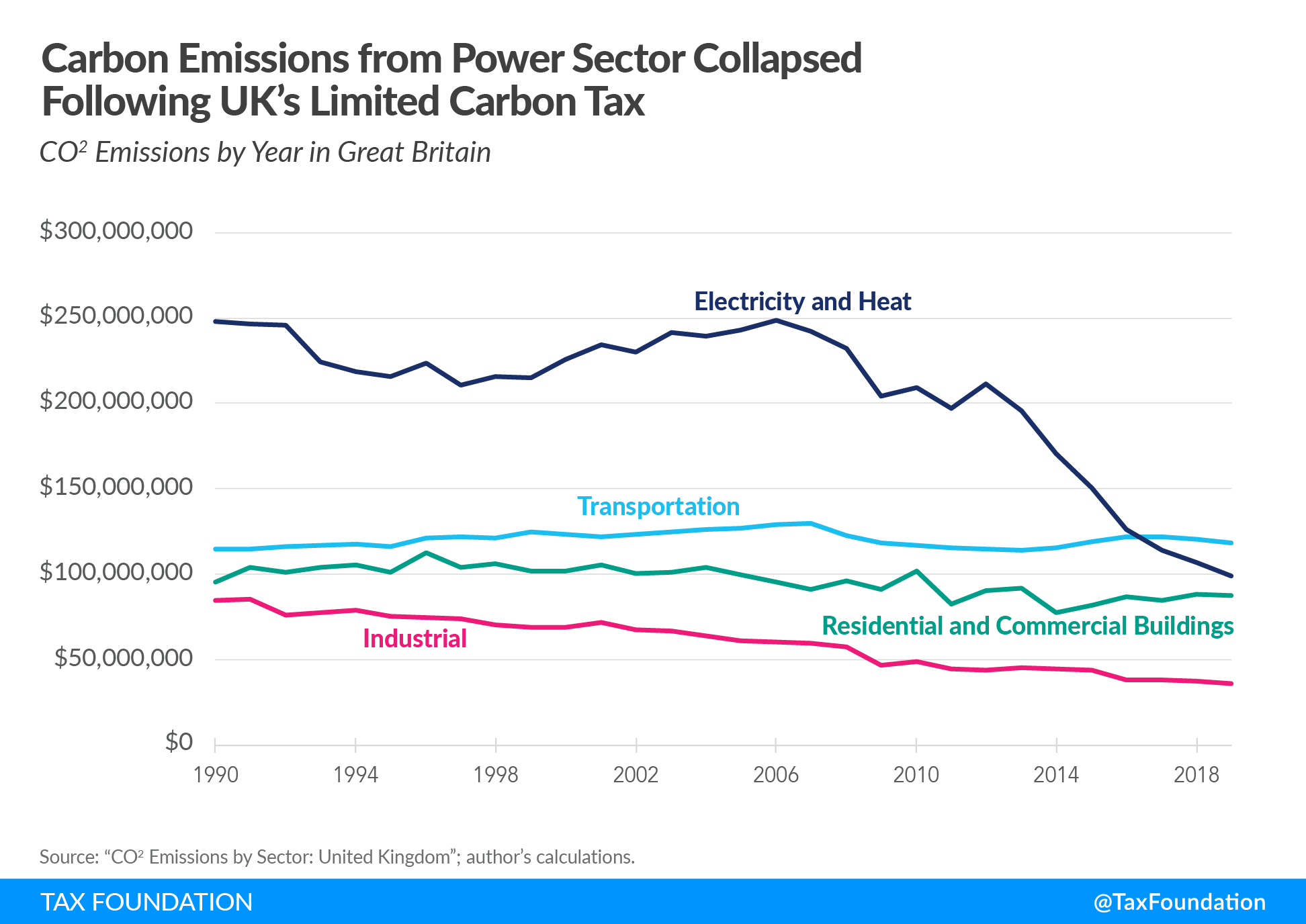

Between 2013 and 2016, the UK saw a significant decline in emissions.[22] The relatively modest carbon tax reduced carbon emissions from the power sector by between 20 and 26 percent, and reduced aggregate emissions by 6.2 percent, despite only applying to a narrow slice of aggregate emissions.[23] The impact of the UK’s carbon tax is clearly visible in UK emissions data by sector, as the power sector was consistently the largest source of emissions before the tax was introduced. The tax was not the only driving factor, but it was a major contributor to the decrease. Within the power sector, the primary driver of the emissions reduction was a shift away from coal as a fuel source: in 2012, coal made up almost 40 percent of the electricity generation in the UK; by 2021, coal generated less than 2 percent.[24]

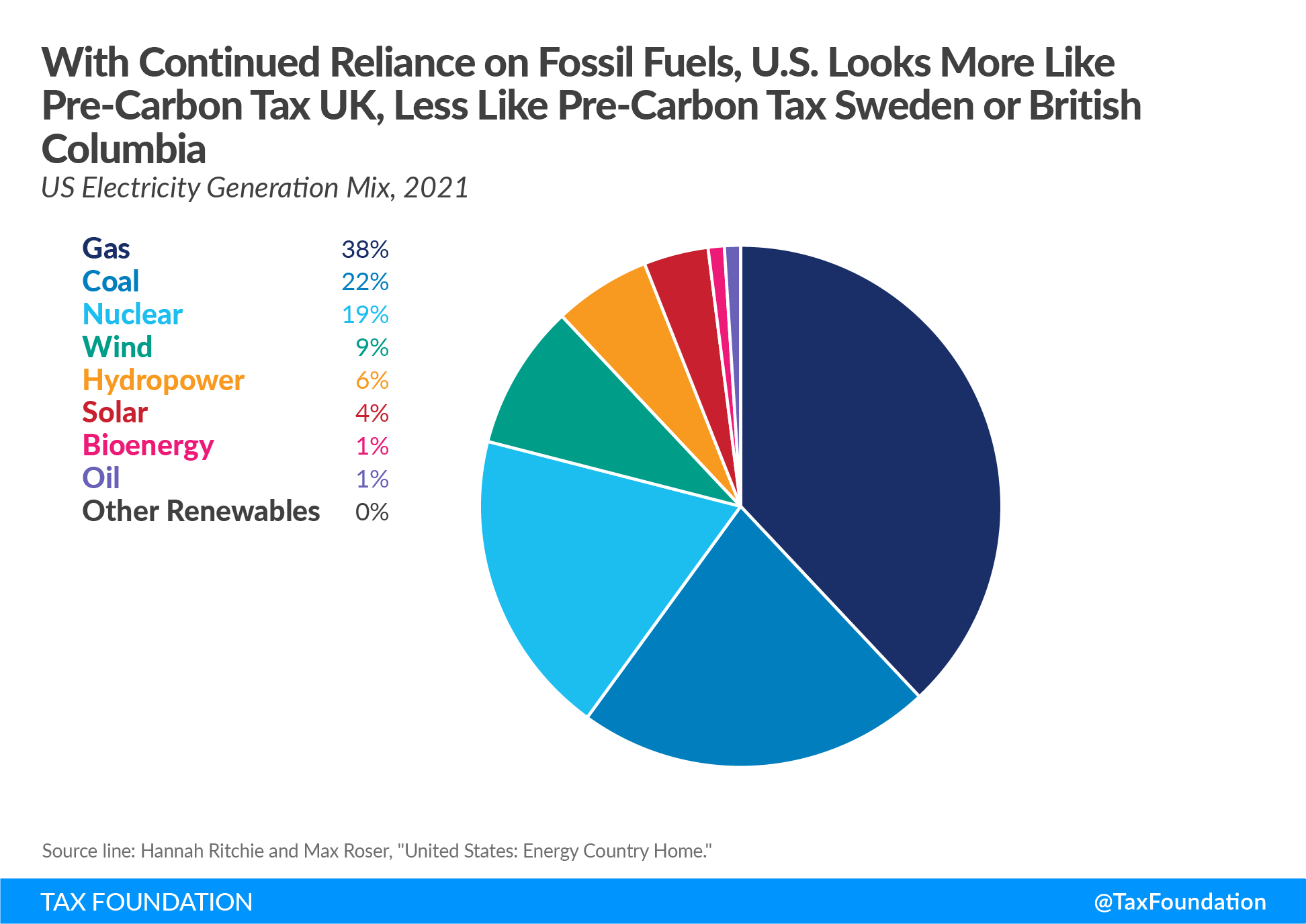

So, in Sweden and British Columbia, carbon taxes led to modest reductions in carbon emissions, but in the United Kingdom, a narrow carbon tax focused on the power sector produced comparatively large emissions reductions. How should the experiences of Sweden, British Columbia, and the United Kingdom inform our view of how effective a U.S. carbon tax would be in reducing emissions? Given that the most powerful response to the carbon tax occurs in the power sector, it’s worth considering what the U.S. electricity generation mix looks like, and how it compares to the electricity mixes at the point of carbon tax introduction in Sweden, British Columbia, and the United Kingdom. The United States still relies primarily on fossil fuels for electricity, unlike pre-carbon-tax Sweden and pre-carbon-tax British Columbia, but similar to pre-carbon-tax United Kingdom, which saw a rapid decline in emissions once a carbon tax was introduced.

Setting aside the sector-by-sector issue, if the United States introduced a carbon tax, it could lead to additional emissions reductions in non-power generation sectors above what existing carbon taxes have done, thanks to induced innovation. Sweden and British Columbia are relatively small markets, and even pre-carbon tax made up a vanishingly small share of global emissions. As a result, we would not expect additional incentives for new, low-emission technology there to dramatically change technological development paths around the world. In contrast, the U.S. is both a large economy and a large emitter. As mentioned earlier, around 5.7 percent of global emissions are subject to carbon taxes. Introducing a carbon tax in the United States would bring the share of global emissions coverage from 5.7 percent to 19.3 percent.[25]

As an example, the transportation sector is relatively unresponsive to carbon pricing, because people do not substantially reduce their driving in response to higher fuel prices.[26] That means consumers are not responsive at the intensive margin: choosing how much to drive in their gas-powered car. A carbon tax, particularly in a large market like the U.S., could have a bigger effect on the extensive margin, so when consumers choose which car to purchase, they will be more likely to choose an electric car, which could, in turn, accelerate electric car adoption elsewhere.

Macroeconomic Effects

A carbon tax has potentially significant consequences for the economy in aggregate. In the United States, for instance, a broad-based carbon tax levied at a relatively modest rate of $25 per ton would raise around $1 trillion in tax revenue over a decade.[27] There are a few major areas of concern: the tax’s impact on economic growth, the distribution of the tax burden, and (related to both growth and distribution) the actual use of the tax revenue.

Effects on Economic Growth: Theory

Two opposing ideas define the debate over a carbon tax’s impact on economic growth.

The first, which views the carbon tax more favorably, is the double dividend effect: that a carbon tax can both provide environmental benefits and economic benefits, the latter by generating revenue to allow for pro-growth tax reforms. The validity of a double dividend cannot be settled as a general matter. The potential benefits of a tax swap, where some other tax is reduced alongside the introduction of a carbon tax, depends on what taxes currently exist in a jurisdiction.

If the existing tax system is poorly designed, then there would be plenty of improvements available to pair with a carbon tax that could produce a net increase in economic growth. But if the existing tax system is close to optimal, then constructing a net pro-growth package would be more difficult. Generally, taxes on capital hurt growth more than taxes on labor and consumption.[28] A carbon tax can be modeled like a slightly more distortionary version of a consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible. .[29] As a result, packages that pair carbon taxes with reductions in corporate or personal income taxes are more likely to produce net positive economic growth.

The second, popular among carbon tax opponents, is the tax interaction effect.[30] The tax interaction effect suggests that, in a tax policy status quo that features significant distortionary policies, a carbon tax (even if paired with reductions in tax rates) could prove net harmful economically, as carbon taxes could further distort factor prices when combined with existing (albeit lower) distortionary taxes.[31] This view also suggests a carbon tax ought to be modeled as a tax on intermediate inputs, rather than a narrow-based consumption tax.

The conclusion of the interaction effect is not necessarily that any carbon tax introduced will be net harmful economically (setting aside the long-term environmental benefits), but that the existence of the interaction effect means the optimal carbon tax rate may be lower than the theoretical Pigouvian tax rate, and that the established existence of other distortionary taxes could weaken, rather than strengthen, the case for a carbon tax and a double dividend.

Several studies compare the net economic impact of different revenue recycling packages. The vast majority agree carbon taxes paired with reductions in capital taxation produce net positive economic growth. However, there is more disagreement regarding the use of carbon tax revenue to reduce other taxes, such as taxes on labor.[32]

Tax Foundation has put together several analyses to this effect. Initially, we modeled pairing a carbon tax with discreet options for revenue recycling: a carbon tax with a payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. cut, a carbon tax with a universal cash payment, and a carbon tax with capital tax cuts.[33] Tax Foundation found the capital tax cut package produced the largest increase in growth, although it still raised taxes on lower-income households on net. Meanwhile, the universal cash payment model provided a large boost to low-income households while reducing growth, and the payroll tax cut package moderately increased both growth and low-income households’ after-tax income.

More recent Tax Foundation research has considered mixed revenue recycling packages, where some revenue is used for lump-sum cash payments and some revenue is used for capital tax cuts (specifically, improvements to the cost recoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages. of capital investments). The modeling results showed that a balance between the two could yield both distributionally progressive and pro-growth results.[34]

| Carbon Tax Package | Percent Change in GDP |

|---|---|

| $50 Carbon Tax | -0.4% |

| $50 Carbon Tax, Dividend of $1,057 | -0.4% |

| $50 Carbon Tax, Reduce Payroll Tax 2.24% | +0.1% |

| $50 Carbon Tax, Expensing for R&D, Permanence for Bonus Depreciation, 11% Corporate Tax Rate | +0.8% |

| $60 Carbon Tax Paired with Permanence for TCJA Individual Provisions | +1.0%* |

| $50 Carbon Tax, Expensing for Capital Investment, $100 Dividend | +1.8% |

| $50 Carbon Tax, Expensing for R&D, Permanence for Bonus Depreciation, $445 Dividend | +0.2% |

|

Note: *Long-run economic growth score of pairing a carbon tax with TCJA permanence is somewhat overstated, as for the first few years of the budget window in that analysis, TCJA individual permanence has no cost because most provisions do not expire until 2025. Sources: Kyle Pomerleau and Elke Asen, “Carbon Tax and Revenue Recycling: Revenue, Economic, and Distributional Implications,” Tax Foundation, Nov. 6, 2019, https://taxfoundation.org/carbon-tax/; Elke Asen, “A Carbon Tax to Make the Individual Provisions of the TCJA Permanent,” Tax Foundation, Sep. 30, 2020, https://taxfoundation.org/carbon-tax-to-make-the-tcja-individual-provisions-permanent/; Alex Muresianu and Huaqun Li, “Carbon Taxes and the Future of Green Tax Reform,” Tax Foundation, Jun. 21, 2022, https://taxfoundation.org/carbon-taxes-green-tax-reforms/. |

|

Effects on Economic Growth: In Practice

Most of the work on the economic impact of carbon taxes shows they do not significantly reduce growth and, if anything, are often associated with higher growth.

A recent study of European countries with and without carbon taxes found a slightly positive connection between carbon taxes and higher economic growth.[35] Now, that is not evidence that carbon taxes on their own cause growth, but it supports the idea that carbon taxes can replace tax revenue from other, more distortionary sources and generate net economic growth.

Strong post facto analyses of the economic impact of individual carbon taxes are sparse compared to theoretical analyses. In the case of British Columbia, economic costs of the policy have been negligible, with one study suggesting the revenue-recycling package had increased growth.[36] Other studies of British Columbia’s carbon tax reform found positive impacts on other economic indicators, such as employment and manufacturing productivity.[37] Sweden’s carbon tax was enacted amidst a massive package of reforms, making isolating the effects of the carbon tax alone even more difficult. Meanwhile, Australia’s carbon tax is often cited as a cautionary tale, but the policy was repealed soon after it was enacted, making it difficult to assess the economic impact beyond projections and short-term impacts on employment.[38]

Differences in revenue recycling choices can help explain the distinction between British Columbia and Australia. British Columbia’s carbon tax was paired with significant reductions in corporate and individual marginal tax rates: the corporate tax rate was reduced from 12 percent to 10 percent, the small business tax rate from 4.5 percent to 2.5 percent, and the bottom two personal income tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. from 5.35 and 8.15 percent to 5.06 and 7.7 percent, respectively.[39] Initially, marginal rate reductions, along with a credit for low-income households to offset distributional concerns, accounted for almost all of the revenue used, although over time some additional revenue has been directed toward more targeted subsidies.[40] Conversely, in Australia, a significant portion of the revenue was directed towards targeted subsidy programs from the outset. The Australian carbon tax also included transfer payments and reductions in the bottom income tax brackets, but it did not substantially improve the business tax environment with broader structural reforms.[41]

Another notable difference between Australia and British Columbia is that Australia’s carbon tax was introduced immediately at $23 per ton, while British Columbia’s was phased in slowly, starting at $10 per ton in 2008 and incrementally increasing by $5 per ton per year until it reached $30 per ton in 2012.[42] By phasing the tax in, consumers and businesses had time to adjust their behavior to prepare for the tax’s impact in British Columbia, while in Australia, the immediate introduction of the tax (coupled with the subpar revenue recycling scheme) meant there was little economic actors could do except eat the tax’s costs.[43]

Ultimately, it is difficult to isolate the impact of a carbon tax change on aggregate GDP growth, and the variation of carbon tax rates and bases pose challenges for cross-country comparisons, as do variations in revenue recycling schemes. Nonetheless, the existing evidence suggests a minimal effect on GDP in either direction.

Distribution and Revenue Recycling: In Theory

Distributional factors also play into the carbon tax debate. Typically, the more harmful taxes, like corporate and personal income taxes, are also more progressive, while a carbon tax is at least slightly regressive. As a result, a major concern about swapping a carbon tax for a corporate tax cut is that it would be very regressive, amounting to a tax increase on lower-income households and a tax cut for the rich.[44] These distributional concerns have led some carbon tax advocates to abandon the idea of the pro-growth tax swap, and instead advocate for the revenue to entirely be used for universal cash payments—raising after-tax incomes for poorer households, but not increasing long-run growth.[45] It is possible to balance growth and distributional concerns by splitting the revenue between different uses.

Different assumptions about a carbon tax have implications for modeling its distributional impact. Some model a carbon tax as a consumption tax while others model it as a tax on intermediate inputs. The consumption tax option leads to a smaller estimated impact on economic growth but a more regressive distribution of the tax burden, while the intermediate input option leads to a larger estimated impact on economic growth but a more proportional distribution of the tax burden.

Additionally, when modeling the carbon tax’s distributional impact, one must decide whether to measure the burden relative to annual income or lifetime income.[46] Measuring the tax’s distribution based on lifetime income leads to a flatter measured distribution of the tax burden, as there are many groups of taxpayers who may have a low annual income in a particular year, but a high income over their lifetime, such as retirees and college students. In many ways, lifetime income is a better measure than annual income of whether a tax disproportionately impacts certain taxpayers, but annual income is a more standard metric.

Revenue recycling also makes a major difference in the tax’s distribution. Generally, relative to the existing U.S. tax system, a carbon tax paired with lump-sum rebates is highly progressive, while a carbon tax paired with corporate tax reductions is regressive, and a carbon tax paired with reductions in payroll taxes ends up roughly neutral. When Tax Foundation modeled a strict carbon tax for payroll tax cut swap, we found moderate net tax cuts for the bottom 90 percent of taxpayers and a tax increase for high-income households. When the Tax Policy Center modeled a strict carbon tax for payroll tax swap, they found moderate net tax increases for lower-income households, a moderate net tax cut for middle- to upper-middle-income households, and effectively no change in net tax liability for high-income households.[47] Some research suggests that allocating around 11 percent of the revenue from a carbon tax toward the bottom 20 percent of earners should fully balance out the costs.[48]

A common objection to the promises of a revenue-neutral carbon tax is that while a pure tax swap that returns all revenue to taxpayers may work on paper, it is inevitable that politicians will squirrel away revenue over time to finance pet projects and grow government.[49] On a similar note, some argue that the introduction of a new tax would ultimately lead to tax increases even if initially offset with reductions to existing taxes, as a carbon tax would be an additional lever on which the government could pull.[50]

Distribution and Revenue Recycling: In Practice

Modeling the distribution of existing carbon taxes faces the same question that modeling theoretical carbon taxes does: whether to measure distribution against lifetime incomes or annual incomes. Both options provide useful information.

In Sweden’s case, one study found that the burden of the carbon tax was regressive when measured against annual incomes, but progressive when measured against lifetime incomes.[51] Meanwhile, an analysis of British Columbia’s carbon tax estimated that the tax was slightly progressive even before considering revenue recycling, owing to the tax falling on the returns to labor and capital while not impacting taxpayers reliant on government transfer payments.[52]

British Columbia is also cited as a good example of carbon tax revenue recycling. Initially, the plan was near textbook: allocating most of the revenue to reducing personal and corporate rates and including a credit for low-income households to offset the distributional impact.[53] However, some of that luster has faded since the tax’s introduction.[54] The personal income and small business tax reductions have stayed, but the corporate tax rate has inched back up from 10 percent to 12 percent.

Measuring exactly how carbon tax revenues are used is difficult, given that government revenue is fungible. A survey conducted in 2016 estimated that roughly 44 percent of carbon tax revenue gets used for revenue recycling, 28 percent for general government funding, and 15 percent for earmarked green spending.[55] However, generating such approximations runs into many challenges that overall suggest the share of revenue used to reduce or substitute for other taxes is substantially higher than 44 percent.

Sweden is one prominent example of how it can be difficult to isolate exactly where carbon tax revenues go. When Sweden introduced its carbon tax in 1991, it also executed a major tax reform to lower its once-infamous high marginal tax rates. The reform reduced the corporate tax rate from 57 percent to 30 percent and the top marginal personal tax rate from 80 percent to 50 percent.[56] It also created a 30 percent tax rate for capital income and reduced tax benefits for capital investment, among other changes.

The long-term legacy of Sweden’s tax reform, when considering tax rates, is clear. Sweden was infamous for its high marginal tax rates in the 1970s and 1980s.[57] Since Swedish tax reform, individual and corporate rates have fluctuated slightly, but nowhere near their old pre-reform highs. As of 2022, the top marginal personal income tax rate has risen from 50 percent to 52 percent, while the corporate tax rate has fallen even further, to 20.6 percent.[58] Moreover, Sweden has continued to cut back on capital taxation in other areas since the reform, as they have eliminated both their wealth taxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary. and their inheritance taxAn inheritance tax is levied upon the value of inherited assets received by a beneficiary after a decedent’s death. Not to be confused with estate taxes, which are paid by the decedent’s estate based on the size of the total estate before assets are distributed, inheritance taxes are paid by the recipient or heir based on the value of the bequest received. in the mid-2000s.[59]

The additional revenue generated by the carbon tax allowed Sweden to bring its other taxes closer to sound tax principles, but the reform did not include explicit links between carbon tax revenue generated and other taxes reduced. Given that the carbon tax was merely one revenue raiser in a larger package, and with some of the other revenue raisers putting an unfortunate burden on investment, it is difficult to isolate the carbon tax’s exact impact on other taxes or the economy at large.[60] Generally, though, the carbon tax’s introduction was paired with other tax cuts and those tax cuts have proved resilient. The 2016 survey roughly assigned 50 percent of Sweden’s carbon tax revenue to revenue recycling, but given the long-term continuation of tax rate reductions, that share could be much higher.

Ireland produces another example of the challenges of determining the exact impact a carbon tax has on other taxes. Ireland introduced a carbon tax in 2010. On paper, none of the revenue was used to reduce other taxes, a small portion was earmarked for energy-efficiency retrofits in residential houses, and the rest was directed towards general funds. In the 2016 survey of carbon tax uses, the authors assessed that one-eighth of the money went to green subsidies and the rest went to general funds, with none allocated to revenue recycling.[61]

However, the carbon tax was enacted in the context of a massive fiscal crisis in Ireland following the global financial crisis of 2008. The Irish government entered an agreement with the European Central Bank, the European Commission, and the International Monetary Fund for support, provided that the Irish government increase tax revenue and reduce expenditures. One of those tax increases was the carbon tax. So, while the revenue was not used to reduce other taxes relative to the status quo, it meant smaller increases in other (more harmful) taxes such as personal and corporate taxes as part of the deal.[62]

A similar scenario played out in Iceland in 2010.[63] In that case, policymakers introduced a carbon tax as a fiscal solution, ultimately preventing other tax increases. There may not be a double dividend, where the revenue goes towards a reduction in other taxes, but there may be a double dividend relative to the counterfactual, where other taxes that would have been increased would have reduced growth more relative to the carbon tax.

Poor uses of the tax revenue raised can make carbon taxes politically perilous, and we can see examples of that dynamic in both Australia and France. In Australia, the government allocated a significant amount of the revenue toward targeted social programs, including relief for specific sectors of the economy as well as new clean energy subsidies, but did not substantially improve the business tax environment.[64] Australia’s carbon tax is one of the only examples of a carbon tax to be introduced and subsequently repealed.

France introduced a carbon tax in 2014, and initially earmarked all revenue for environmental and climate spending.[65] Later, the French government planned to raise the carbon tax (along with the gas taxA gas tax is commonly used to describe the variety of taxes levied on gasoline at both the federal and state levels, to provide funds for highway repair and maintenance, as well as for other government infrastructure projects. These taxes are levied in a few ways, including per-gallon excise taxes, excise taxes imposed on wholesalers, and general sales taxes that apply to the purchase of gasoline. ) to address budgetary woes, and these increases helped drive the well-publicized “Yellow Vest” protests.[66] The French carbon tax stuck around, but the increases were canceled.

Clearly, not all the revenue generated by carbon taxes enacted around the world has gone toward reducing other taxes. But revenue recycling is not a phantom promise either: plenty of examples show carbon taxes either being paired with sustained reductions in marginal tax rates or serving as an alternative to other tax increases when some form of tax hike is a foregone conclusion.

Environmental Taxes

Environmental Taxes: In Theory

The gas tax is the biggest environmental tax in the United States. It is not a tax to lower carbon emissions; it is instead a user feeA user fee is a charge imposed by the government for the primary purpose of covering the cost of providing a service, directly raising funds from the people who benefit from the particular public good or service being provided. A user fee is not a tax, though some taxes may be labeled as user fees or closely resemble them. for road usage. However, it changes the relative price of no- or low-emission cars, creating a marginal incentive for green technology.[67]

When constructing ideal policy in a vacuum, it would make sense to replace the gas tax with something like a vehicle miles traveled (VMT) tax, and then apply a carbon tax. This way, one policy serves as a dedicated user fee that applies equally to electric and gas-powered vehicles, and one policy serves as a marginal incentive for reducing carbon emissions. Because a VMT tax faces some administrative challenges, it may be more feasible in the U.S. to keep the gas tax and layer a carbon tax on top of it. Given that the current gas tax is too low to fully finance road costs, combining it with a carbon tax would not create excess burdens on road transportation.[68]

Beyond the gas tax, the U.S. has only minimal environmental taxes, and, in general, it would make sense to scrap them in favor of a broad carbon tax. In some cases, the other environmental taxes are not targeted at the externalities of carbon emissions. The excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on coal sales is not aimed at the externalities of the emissions of coal-fired power plants, but at the costs of black lung contracted by coal miners.[69] Similarly, the Superfund tax on several chemicals is aimed at mitigating the localized environmental costs of possible leaks and spills.[70] On one hand, it makes sense to have separate taxes that address separate environmental costs; on the other hand, these environmental taxes have very low revenue for their administrative costs.[71]

Environmental Taxes: In Practice

Unfortunately, Europe does not present a clear comparison to the United States, given that excise taxes on fuel are much higher than in the United States. Under the Energy Tax Directive, European Union countries must levy a minimum of a €0.33 per liter tax on gasoline (or around $1.33 per gallon), and most European countries levy additional taxes on top of that minimum rate.[72] For comparison, the state that imposes the highest gas taxes in the U.S. is California, with an average gas tax rate of around $.67 per gallon. Even when adding in the federal gas tax of $.184 a gallon, to reach $.85 per gallon, it is still substantially lower than the minimum tax levied in Europe.[73]

Other European excise taxes can also clash with a carbon tax. Take the example of Sweden— where the carbon tax is primarily levied on emissions from transportation.[74] When Sweden imposed its carbon tax, it already had an energy tax on electricity usage in law, as well as a tax on aviation and a tax on vehicles that scales according to a vehicle’s emissions. Even further, Sweden is part of the EU’s Emissions Trading System, which largely applies to the industrial sector.[75] Some emissions are subject to more than one of these taxes, but the carbon tax is limited in scope, excluding many emissions to attempt to avoid double taxation. The introduction of a carbon tax has not been a sword through the Gordian Knot of energy taxation.

Ultimately, European carbon taxes have not replaced or simplified broad networks of different taxes that serve similar, though not identical, purposes. In the United States, implementing a carbon tax would not run the same risk, given that the U.S. does not have a broad framework of high excise taxes on energy products like European countries do.

The most relevant exception in the United States is the handful of states that have adopted cap-and-trade measures of their own.[76] To maintain a fully neutral carbon tax, policymakers would have two options: repeal the state-level carbon pricing upon the introduction of a federal policy or provide a credit to firms for the carbon price paid at the state level.

Green Subsidies

Green Subsidies: In Theory

Tax credits for renewable energy have a similar goal to the carbon tax: change the relative prices of high- and low-emissions behavior to reduce the former and increase the latter. These subsidies are usually less efficient than a carbon tax for several reasons.

For one, green subsidies require revenue, often raised through economically distortionary taxes, while carbon taxes create space to lower economically distortionary taxes.[77] But setting aside the revenue needed for green subsidies, determining the right base for a subsidy has more challenges than for a tax.

The power generation sector is perhaps the best place to illustrate the challenge. Imagine an energy company that is considering upgrading or replacing a coal power plant. Current law provides subsidies for wind and solar power, but those technologies may not be viable where the power plant is located. If the energy company effectively faces a choice between upgrading its existing coal plant or replacing it with a natural gas plant, tax subsidies for wind and solar do not help make the greener natural gas plant cheaper. The carbon tax, on the other hand, would provide a marginal incentive for the firm to choose the natural gas plant over the coal plant.[78]

Presuming the carbon tax is set at the socially optimal level, the continued existence of tax subsidies for green investment in production is redundant, even distortionary—at least from the perspective of addressing the negative externalities associated with carbon emissions. One could make the case that government support for green energy should continue as part of a broader policy of support for R&D investment across the economy.[79] R&D support could be better achieved through broad R&D policies rather than specific environmental policies.[80]

Additionally, while some policymakers shy away from carbon taxes due to distributional concerns, green subsidies have similar problems. The evidence on the environmental credits is clear. Using IRS data, economists Severin Borenstein and Lucas Davis found that since 2006, the top 20 percent of earners have received more than 60 percent of the benefits of environmental tax credits, while the bottom 60 percent have received only 10 percent of the benefits. Tax credits for electric vehicles look particularly extreme, with 90 percent of the benefits going to the top 20 percent of earners.[81] Initial analysis of the recently enacted InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. Reduction Act tax credits could look similar.[82]

Green Subsidies: In Practice

It is easy to point out the shortcomings of existing green subsidy regimes, particularly in the United States, and the benefits of replacing the existing set of green subsidies with a single carbon tax. Unfortunately, the broader use of carbon pricing in the European Union has not proved an impediment to ever-growing subsidies. However, given a level of policymaker interest in addressing climate change, carbon taxes and green subsidies are competing policy options.

European Union Member States spent €73 billion on renewable energy subsidies in 2018, as well as €15 billion for energy efficiency initiatives.[83] For comparison, the EU’s GDP in 2018 was around €13.5 trillion, meaning the EU spent roughly 0.7 percent of its GDP on environmental subsidies.[84] More recent data from 2020 suggests around 1 percent of the EU area’s GDP is devoted to public, environmental investment.[85]

Contrast that with the United States, which has a negligible level of carbon pricing. In 2016, the United States spent $6.8 billion on renewable energy subsidies and just under $1 billion in subsidies for energy efficiency, compared to its $19 trillion GDP in 2016, meaning the U.S. spent 0.04 percent of GDP on environmental subsidies.[86] Even going back to earlier years, when green energy subsidies enacted as part of the stimulus response to the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. were still on the books, U.S. subsidies as a share of GDP still fell short of the EU. In 2010, the U.S. spent $15.8 billion on renewable energy subsidies and $7.4 billion on energy conservation efforts, for a total of $23.2 billion, or 0.15 percent of GDP.[87] However, with the Inflation Reduction Act’s large tax credits for green energy, that ratio could look much different going forward, particularly given how initial estimates of those credits’ cost may have been low.[88]

In Europe’s case too, just because they have historically had large green subsidies and more expansive carbon pricing than the U.S. does not necessarily mean that carbon pricing schemes and green energy subsidies cannot act as substitutes. European countries have been more politically focused on climate change than the United States, so it is unsurprising that they have traditionally had more of both subsidies and carbon pricing.

EU policymakers think in terms of emissions targets. The European Green Deal, for example, aims to reduce 2030 carbon emissions by at least 55 percent relative to 1990 levels.[89] The European Green Deal includes numerous different policies to achieve this goal, including expansions to the EU’s Emissions Trading System and the introduction of a carbon border adjustment mechanism (CBAM), as well as new regulatory measures and subsidies designed to spur green technology adoption in Member States.[90] More recently, the EU Commission has put forward a green industrial policy plan to further subsidize green or green-adjacent technology.[91] If there was no carbon pricing in the European Green Deal, that would necessitate more expansive subsidies, at least from the perspectives of European environmentalist policymakers.

Meanwhile, in the United States, the Inflation Reduction Act has been a case study of how carbon pricing and green subsidies can be direct political substitutes. In 2010, a proposal for cap and trade petered out in Congress.[92] Since then, many environmentalist groups turned away from carbon pricing in favor of more “transformative” ideas like the Green New Deal.[93] Politicians followed suit: during the first two years of the Biden administration, the carbon tax idea was pushed aside in favor of the subsidy approach that culminated in the Inflation Reduction Act.[94]

In short, while there are few examples of a carbon tax replacing an existing set of subsidies for green energy, the Inflation Reduction Act is a great example of a complicated subsidy regime being enacted after carbon pricing had been taken off the table.

Regulation

Regulation: In Theory

The relative simplicity and directness of the carbon tax as a price signal is generally considered a more cost-effective way to reduce carbon emissions than various forms of top-down regulation.

The American Action Forum estimated that the economic burden per ton of reduced carbon emissions was twice as high for Obama-era regulations as it would have been for a $25 per ton carbon tax.[95] The gap between the two policies would further widen when considering the possible benefits of revenue recycling in the case of the carbon tax. The advantage of carbon pricing over regulation comes from how they treat different emissions. The carbon tax allows individual polluters to weigh the costs of reducing emissions against the tax owed, while regulations punish polluters even when the costs of reducing emissions exceed the cost of emissions.[96]

These analyses contrast relatively well-designed carbon regulation with a carbon tax. However, some regulations have been counterproductive thanks to design problems. For example, Corporate Average Fuel Economy (CAFE) standards regulate automobile fuel efficiency according to vehicle size, with looser standards for light trucks than for passenger cars. This divergence incentivizes producers to increase vehicle size to be subject to the looser standards, thus undermining the reduction in emissions.[97]

Additionally, much like green subsidies, environmental regulations face distributional challenges.[98]

Regulation: In Practice

Similar to subsidies, it is less likely that carbon taxes replace current environmental regulations and more likely that they substitute for new expansions of climate regulations.

With the European Green Deal today, tightening regulations go hand in hand with expansions to carbon pricing. The proposal includes expansions to the EU’s Emissions Trading System, as well as more emissions regulations on numerous sectors of the economy. It expands the EU’s directive on renewable fuels in the power sector, strengthens emissions standards for cars and vans, and introduces new limits on pollution from maritime fuel, among other top-down policies.[99] In terms of Member States with their own carbon taxes, Sweden also has a comprehensive set of emissions and climate regulations along with their carbon tax.[100]

One issue with parsing through the trade-offs between environmental regulations and carbon taxes is that many environmental regulations are aimed at non-climate change harms, often localized. For instance, the Clean Air Act of 1970 was aimed at localized harms of air pollution, rather than planet-wide climate change. Climate change only developed into a significant political concern in the 1980s, with 1988 being a major turning point.[101] Finland provides a relatively rare example of carbon taxes replacing some existing environmental regulations.[102]

One area of significant deregulation in indirect connection with carbon taxes is energy market deregulation. In the United States, energy market deregulation moved power generation, transmission, and distribution away from regulated monopolies with effectively fixed prices, and toward competitive markets with multiple firms and more variable prices.[103] In the European Union, energy market deregulation followed the same loose framework, with additional privatization efforts.[104] While the overall costs and benefits of energy market deregulation are debatable,[105] there is some evidence that deregulation of energy markets has accelerated the environmental benefits of carbon pricing schemes.[106]

External Validity and Conclusions

The theoretical case for the carbon tax is strong, yet critics argue that the benefits do not materialize when carbon taxes are enacted. While existing carbon taxes may not be as good as the abstract ideal carbon tax, they still deliver on several core promises: reducing emissions at a relatively low economic cost, with a substantial portion (likely a majority) of revenue being returned to taxpayers or replacing other tax increases. Critics are correct that existing carbon taxes have not served as all-encompassing replacements for complex webs of other environmental and climate policies.

The experience abroad indicates that some carbon taxes have been paired with sustained reductions in other taxes while few have been paired with the repeal of substantial pre-existing environmental regulations. The prospects of a carbon tax in the United States are in policymakers’ hands, and they should learn from theoretical as well as practical cases of how to best design a carbon tax system.

[1] “Economists’ Statement on Carbon Dividends,” The Wall Street Journal, Jan. 16, 2019, https://www.wsj.com/articles/economists-statement-on-carbon-dividends-11547682910.

[2] The difference between carbon taxes and cap and trade is whether price or quantity is set by the market. Under a carbon tax, government sets a price on carbon emissions, and companies can choose how much to reduce their emissions in response (in other words, allowing the market to choose the quantity). Under a cap-and-trade system, government sets a cap on the permissible amount of carbon emissions and auctions off allowances for pollution, effectively allowing the market to choose the price.

[3] World Bank, “Carbon Pricing Dashboard,” last updated Apr. 1, 2022, https://carbonpricingdashboard.worldbank.org/map_data.

[4] James R. McFarland, Allen A. Fawcett, Adele C. Morris, John M. Reilly, and Peter J. Wilcoxen, “Overview of the EMF 32 Study on U.S. Carbon Tax Scenarios,” Climate Change Economics 9:1 (2018), https://www.worldscientific.com/doi/suppl/10.1142/S201000781840002X; see also Alexander R. Barron, Allen A. Fawcett, Marc A. Hafstead, James R. McFarland, and Adele C. Morris, “Policy Insights from the EMF 32 Study on U.S. Carbon Tax Scenarios,” Climate Change Economics 9:1 (2018), https://www.worldscientific.com/doi/10.1142/S2010007818400031.

[5] David Popp, “Induced Innovation and Energy Prices,” American Economic Review 92:1 (March 2002), https://www.aeaweb.org/articles?id=10.1257/000282802760015658.

[6] Stephie Fried, “Climate Policy and Innovation: A Quantitative Macroeconomic Analysis,” American Economic Journal: Macroeconomics 10:1 (2018), https://pubs.aeaweb.org/doi/pdfplus/10.1257/mac.20150289.

[7] See, for instance, Alex Muresianu and Sean Bray, “Carbon Taxes, Trade, and American Competitiveness,” Tax Foundation, Nov. 3, 2022, https://taxfoundation.org/border-adjusted-carbon-tax-revenue/.

[8] Joshua Meltzer, “A Carbon Tax As a Driver of Green Technology Innovation and the Implications for International Trade,” Energy Law Journal 35:45 (2014), https://www.eba-net.org/wp-content/uploads/2023/02/4-14-45-Meltzer_Final-5.13.14.pdf; see also Aaron Cosbey, Susanne Droege, Carolyn Fischer, and Clayton Munnings, “Developing Guidance for Implementing Border Carbon Adjustments: Lessons, Cautions, and Research Needs from the Literature,” Review of Environmental Economics and Policy 13:1 (Winter 2019), https://www.journals.uchicago.edu/doi/full/10.1093/reep/rey020.

[9] World Bank, “GDP (current US$),” World Bank National Accounts Data, and OECD National Accounts data files, accessed Feb. 28, 2023, https://data.worldbank.org/indicator/NY.GDP.MKTP.CD; see also World Bank, “Carbon Pricing Dashboard,” last updated Apr. 1, 2022, https://carbonpricingdashboard.worldbank.org/. These criteria were chosen to exclude carbon taxes with little external validity for a U.S. policy conversation. For example, Estonia’s carbon tax only covers 5.6 percent of its emissions; Poland and Ukraine have effective carbon tax rates around or below $1 per ton; and a microstate like Lichtenstein provides few policy lessons for the United States.

[10] This excludes the many carbon taxes that have been introduced in the past 10 years, in countries like France, Spain, Portugal, Mexico, Chile, and Canada (at a national level), as well as carbon taxes that were introduced but then quickly repealed, such as Australia’s.

[11] This excludes both countries like Estonia, Latvia, and Poland, which all have carbon taxes that cover less than 10 percent of emissions, as well as countries like Japan and Ukraine, which have broad carbon taxes set at low rates.

[12] This excludes countries like Liechtenstein, Iceland, and Slovenia.

[13] Samuel Jonsson, Anders Ydstedt, and Elke Asen, “Looking Back on 30 Years of Carbon Taxes in Sweden,” Tax Foundation, Sep. 23, 2020, https://taxfoundation.org/sweden-carbon-tax-revenue-greenhouse-gas-emissions/.

[14] Samuel Jonsson, Anders Ydstedt, and Elke Asen, “Looking Back on 30 Years of Carbon Taxes in Sweden.”

[15] Ibid.

[16] Hannah Ritchie and Max Roser, “Electricity Production by Source, Sweden,” Our World in Data, accessed Mar. 24, 2023, https://ourworldindata.org/energy/country/sweden#what-sources-does-the-country-get-its-energy-from.

[17] Hannah Ritchie, Max Roser, and Pablo Rosado “CO2 and Greenhouse Gas Emissions,” Our World in Data, accessed Feb. 28, 2023, https://ourworldindata.org/co2/country/sweden.

[18] Julius J. Andersson, “Carbon Taxes and CO2 Emissions: Sweden as a Case Study,” Economic Policy 11:4 (2019), https://pubs.aeaweb.org/doi/pdfplus/10.1257/pol.20170144.

[19] Brian Murray and Nicholas Rivers, “British Columbia’s Revenue-Neutral Carbon Tax: A Review of the Latest Grand Experiment in Environmental Policy,” Energy Policy 86 (November 2015), https://www.sciencedirect.com/science/article/abs/pii/S0301421515300550.

[20] Younes Ahmadi, Akio Yamazaki, and Philippe Kabore, “How Do Carbon Taxes Affect Emissions? Plant-Level Evidence from Manufacturing,” Environmental and Resource Economics 82 (2022), https://link.springer.com/article/10.1007/s10640-022-00678-x; see also Chad Lawley and Vincent Thivierge, “Refining the Evidence: British Columbia’s Carbon Tax and Household Gasoline Consumption,” The Energy Journal 39:2 (November 2016), https://www.iaee.org/en/publications/init2.aspx?id=0; Jean-Thomas Barnard and Maral Kichian, “The Long and Short Run Effects of British Columbia’s Carbon Tax on Diesel Demand,” Energy Policy 131 (August 2019), https://www.sciencedirect.com/science/article/abs/pii/S0301421519302708.

[21] See British Columbia, “Provincial Inventory of Greenhouse Gas Emissions,” Ministry of Environment and Climate Change Strategy (September 2022), https://www2.gov.bc.ca/gov/content/environment/climate-change/data/provincial-inventory, see also John Nyboer and Maximilian Kniewasser, “Energy and GHG Emissions in British Columbia, 1990-2010,” Canadian Industrial End-use Data and Analysis Centre (June 2012), https://pics.uvic.ca/sites/default/files/uploads/publications/Energy_Data_Report_2010_1.pdf.

[22] Jan Abrell, Miriam Kosch, and Sebastian Rausch, “How Effective Was the U.K. Carbon Tax? A Machine Learning Approach to Policy Evaluation,” USAEE Working Paper No. 19-396, Apr. 17, 2019 https://www.econstor.eu/bitstream/10419/207139/1/1663457328.pdf.

[23] Marion Leroutier, “Carbon Pricing and Power Sector Decarbonization: Evidence from the UK,” Journal of Environmental Economics and Management 111 (January 2022), https://www.sciencedirect.com/science/article/pii/S0095069621001285.

[24] Hannah Ritchie and Max Roser, “United Kingdom: Energy Country Profile,” Our World in Data, accessed Mar. 8, 2023, https://ourworldindata.org/energy/country/united-kingdom.

[25] Hannah Ritchie and Max Roser, “United States: CO2 Country Profile,” Our World in Data, accessed Apr. 4, 2023, https://ourworldindata.org/energy/country/united-states.

[26] Kristin Hayes and Marc Hafstead, “Carbon Pricing 103: Effects Across Sectors,” Resources for the Future, Apr. 27, 2020, https://www.rff.org/publications/explainers/carbon-pricing-103-effects-across-sectors/.

[27] Tax Foundation, “Option 50: Institute a Carbon Tax” in Options for Reforming America’s Tax Code 2.0, Apr. 19, 2021, https://taxfoundation.org/tax-reform-options/?option=50.

[28] See for instance, Asa Johansson, Christopher Heady, Jens Matthias Arnold, Bert Brys, and Laura Vartia, “Taxation and Economic Growth,” OECD Economics Department Working Papers No. 620 (July 2008), https://www.oecd-ilibrary.org/economics/taxation-and-economic-growth_241216205486.

[29] Kyle Pomerleau and Elke Asen, “Carbon Taxes and Revenue Recycling: Revenue, Economic, and Distributional Implications,” Tax Foundation, Nov. 6, 2019, https://taxfoundation.org/carbon-tax/.

[30] Robert P. Murphy, “Carbon Taxes and the ‘Tax Interaction Effect,’” Econlib, Oct. 1, 2012, https://www.econlib.org/library/Columns/y2012/Murphycarbon.html.

[31] A. Lans Bovenberg and Lawrence H. Goulder, “Optimal Environmental Taxation in the Presence of Other Taxes: General Equilibrium Analysis,” The American Economic Review 86:4 (September 1996), https://www.jstor.org/stable/2118315.

[32] Jaume Freire-Gonzalez, “Environmental Taxation and the Double Dividend Hypothesis in CGE Modelling Literature: A Critical Review,” Journal of Policy Modeling 40:1 (January-February 2018), https://www.sciencedirect.com/science/article/pii/S0161893817301205?via%3Dihub; see also Lawrence H. Goulder and Marc A. Hafstead, “Tax Reform and Environmental Policy: Options for Recycling Revenue from a Tax on Carbon Dioxide,” Resources for the Future, Discussion Paper 13-31 (October 2013), https://media.rff.org/documents/RFF-DP-13-31.pdf.

[33] Kyle Pomerleau and Elke Asen, “Carbon Taxes and Revenue Recycling: Revenue, Economic, and Distributional Implications.”

[34] Alex Muresianu and Huaqun Li, “Carbon Taxes and the Future of Green Tax Reform,” Tax Foundation, Jun. 21, 2022, https://taxfoundation.org/carbon-taxes-green-tax-reforms/.

[35] Gilbert Metcalf and James Stock, “Measuring the Macroeconomic Impact of Carbon Taxes,” AEA Papers and Proceedings 110 (May 2020), https://www.aeaweb.org/articles?id=10.1257/pandp.20201081.

[36] Brian Murray and Nicholas Rivers, “British Columbia’s Revenue-Neutral Carbon Tax: A Review of the Latest Grand Experiment in Environmental Policy”; see also Gilbert E. Metcalf, “On the Economics of a Carbon Tax for the United States,” Brookings Institution, March 2019, https://www.brookings.edu/wp-content/uploads/2019/03/metcalf_web.pdf.

[37] Akio Yamazaki, “Jobs and Climate Policy: Evidence from British Columbia’s Revenue-Neutral Carbon Tax,” Journal of Environmental Economics and Management 83 (May 2017), https://www.sciencedirect.com/science/article/abs/pii/S0095069617301870; see also Younes Ahmadi, Akio Yamazaki, and Philippe Kabore, “How Do Carbon Taxes Affect Emissions? Plant-Level Evidence from Manufacturing.”

[38] Alex Robson, “Australia’s Carbon Tax: An Economic Evaluation,” Institute for Energy Research, September 2013, https://www.instituteforenergyresearch.org/wp-content/uploads/2013/09/IER_AustraliaCarbonTaxStudy.pdf.

[39] Malcolm Fairbropther and Ekaterina Rhodes, “Climate Policy in British Columbia: An Unexpected Journey,” Frontiers in Climate 4 (2022), https://www.frontiersin.org/articles/10.3389/fclim.2022.1043672/full.

[40] Brian Murray and Nicholas Rivers, “British Columbia’s Revenue-Neutral Carbon Tax: A Review of the Latest Grand Experiment in Environmental Policy.”

[41] Jeremy Carl and David Fedor, “Tracking Global Carbon Revenues: A Survey of Carbon Taxes Versus Cap-and-Trade in the Real World,” Energy Policy 96 (September 2016), https://www.sciencedirect.com/science/article/pii/S0301421516302531.

[42] Malcolm Fairbropther and Ekaterina Rhodes, “Climate Policy in British Columbia: An Unexpected Journey.”

[43] Alex Robson, “Australia’s Carbon Tax: An Economic Evaluation.”

[44] John Horowitz, Julie-Anne Cronin, Hannah Hawkins, Laura Konda, and Alex Yuskavage, “Methodology for Analyzing a Carbon Tax,” Office of Tax Analysis Working Paper 115, January 2017, https://home.treasury.gov/system/files/131/WP-115.pdf.

[45] See for instance, Climate Leadership Council, “The Four Pillars of the Carbon Dividends Program,” https://clcouncil.org/our-solution/.

[46] Kevin A. Hassett, Aparna Mathur, and Gilbert E. Metcalf, “The Lifetime of a U.S. Carbon Tax: A Lifetime and Regional Analysis,” The Energy Journal 30:2 (2009), https://www.jstor.org/stable/41323238; see also Aparna Mathur and Adele C. Morris, “Distributional Effects of a Carbon Tax in Broader U.S. Fiscal Reform,” The Brookings Institution, Dec. 14, 2012, https://www.brookings.edu/wp-content/uploads/2016/06/14-carbon-tax-fiscal-reform-morris.pdf.

[47] Kyle Pomerleau and Elke Asen, “Carbon Taxes and Revenue Recycling: Revenue, Economic, and Distributional Implications”; see also Joseph Rosenberg, Eric Toder, and Chenxi Lu, “Distributional Implications of a Carbon Tax,” Tax Policy Center, July 2018, https://www.taxpolicycenter.org/sites/default/files/publication/155473/distributional_implications_of_a_carbon_tax_5.pdf.

[48] Mathur and Morris, “Distributional Effects of a Carbon Tax in Broader U.S. Fiscal Reform.”

[49] Jordan McGillis, “The Case Against a Carbon Tax,” Institute for Energy Research, April 2019, https://www.instituteforenergyresearch.org/wp-content/uploads/2019/04/Carbon-Tax-Policy-BriefFinalText-1.pdf, see also David Kreutzer and Nicolas Loris, “Carbon Tax Would Raise Unemployment, Not Swap Revenue,” The Heritage Foundation, Jan. 8, 2013, https://www.heritage.org/environment/report/carbon-tax-would-raise-unemployment-not-swap-revenue.

[50] Chris Prandoni, “Americans for Tax Reform Opposes a Carbon Tax,” Americans for Tax Reform, Nov. 13, 2012, https://www.atr.org/americans-tax-reform-opposes-carbon-a7346/.

[51] Julius Andersson and Giles Atkinson, “The Distributional Effects of a Carbon Tax on Gasoline: The Role of Income Inequality,” Stockholm Institute of Transition Economics Working Paper (February 2022), https://www.juliusandersson.com/The_Distributional_Effects_of_a_Carbon_Tax_February_2022.pdf.

[52] Marisa Beck, Nicholas Rivers, Randall Wigle, and Hidemichi Yonezawa, “Carbon Tax and Revenue Recycling: Impacts on Households in British Columbia,” Resource and Energy Economics 41 (August 2015), https://www.sciencedirect.com/science/article/abs/pii/S0928765515000317.

[53] Brian Murray and Nicholas Rivers, “British Columbia’s Revenue-Neutral Carbon Tax: A Review of the Latest Grand Experiment in Environmental Policy.”

[54] Charles Lammam and Taylor Jackson, “Examining the Revenue Neutrality of British Columbia’s Carbon Tax,” Fraser Institute, Feb. 1, 2017, https://www.fraserinstitute.org/sites/default/files/examining-the-revenue-neutrality-of-bcs-carbon-tax.pdf.

[55] Jeremy Carl and David Fedor, “Tracking Global Carbon Revenues: A Survey of Carbon Taxes Versus Cap-and-Trade in the Real World.” Categories do not sum to 100 percent as these categories are not comprehensive, and in some years, revenue from carbon taxes may not exactly match revenue recycling uses.

[56] Samuel Jonsson, Anders Ydstedt, and Elke Asen, “Looking Back on 30 Years of Carbon Taxes in Sweden.”

[57] Daniel J. Mitchell, “ABBA and the Most-Inane-Ever Tax Controversy,” Cato Institute, Feb. 18, 2014, https://www.cato.org/blog/abba-story-most-inane-ever-tax-controversy.

[58] Cristina Enache, “Corporate Tax Rates Around the World, 2022,” Tax Foundation, Dec. 13, 2022, https://taxfoundation.org/publications/corporate-tax-rates-around-the-world/; see also PwC, “Sweden: Individual – Taxes on Personal Income,” last reviewed Jan. 30, 2023, https://taxsummaries.pwc.com/sweden/individual/taxes-on-personal-income.

[59] Samuel Jonsson, Anders Ydstedt, and Elke Asen, “Looking Back on 30 Years of Carbon Taxes in Sweden.”

[60] Ibid; see also Alan J. Auerbach, Kevin Hassett, and Jan Sodersten, “Taxation and Corporate Investment: the Impact of the 1991 Swedish Tax Reform,” Swedish Economic Policy Review 2 (1995), https://web.archive.org/web/20200709190922id_/https://www.regeringen.se/contentassets/da1b0124255849ddaa1b2c9c9ad7c14f/alan-j.-auerbach-kevin-hassett–jan-sodersten-taxation-and-corporate-investment-the-impact-of-the-1991-swedish-tax-reform.

[61] Jeremy Carl and David Fedor, “Tracking Global Carbon Revenues: A Survey of Carbon Taxes Versus Cap-and-Trade in the Real World.”

[62] Frank Convery, Louise Dunne, and Deirdre Joyce, “Ireland’s Carbon Tax and the Fiscal Crisis: Issues in Fiscal Adjustment, Environmental Effectiveness, Competitiveness, Leakage, and Equity Concerns,” OECD Environmental Working Papers 59 (October 2013), https://www.oecd-ilibrary.org/environment-and-sustainable-development/ireland-s-carbon-tax-and-the-fiscal-crisis_5k3z11j3w0bw-en.

[63] Jeremy Carl and David Fedor, “Tracking Global Carbon Revenues: A Survey of Carbon Taxes Versus Cap-and-Trade in the Real World.”

[64] Alex Robson, “Australia’s Carbon Tax: An Economic Evaluation.”

[65] Jeremy Carl and David Fedor, “Tracking Global Carbon Revenues: A Survey of Carbon Taxes Versus Cap-and-Trade in the Real World.”

[66] Patrick Criqui, Mark Jaccard, and Thomas Sterner, “Carbon Taxation: A Tale of Three Countries,” Sustainability 11:22 (2019), https://www.mdpi.com/2071-1050/11/22/6280.

[67] Ulrik Boesen, “Who Will Pay for the Roads,” Tax Foundation, Aug. 25, 2020, https://taxfoundation.org/road-funding-vehicle-miles-traveled-tax.

[68] Ibid., see also Joseph Kile, “Testimony: Options for Funding and Financing Highway Spending,” Congressional Budget Office, May 18, 2021, https://www.cbo.gov/publication/57222; Ulrik Boesen, “How Are Your State’s Roads Funded,” Tax Foundation, Apr. 21, 2021, https://taxfoundation.org/state-infrastructure-spending/.

[69] Scott D. Szymendera, “The Black Lung Program, the Black Lung Disability Trust Fund, and the Excise Tax on Coal,” Congressional Research Service, Feb. 7, 2023, https://crsreports.congress.gov/product/pdf/R/R45261.

[70] Thomas A. Barthold, “Issues in the Design of Environmental Taxes,” Journal of Economic Perspectives 8:1 (Winter 1994), https://pubs.aeaweb.org/doi/pdf/10.1257/jep.8.1.133.

[71] Ibid; see also Don Fullerton, “Why Have Separate Environmental Taxes” in Tax Policy and the Economy 10 (January 1996), https://www.nber.org/system/files/chapters/c10898/c10898.pdf.

[72] Adam Hoffer, “Gas Taxes in Europe, 2022,” Tax Foundation, Jul. 12, 2022, https://taxfoundation.org/gas-taxes-in-europe-2022/.

[73] Janelle Fritts, “How High are Gas Taxes in Your State,” Tax Foundation, Jul. 28, 2021, https://taxfoundation.org/state-gas-tax-rates-2021/.

[74] Julius J. Andersson, “Carbon Taxes and CO2 Emissions: Sweden as a Case Study.”

[75] Samuel Jonsson, Anders Ydstedt, and Elke Asen, “Looking Back on 30 Years of Carbon Taxes in Sweden.” Notably, the EU hopes to expand the existing ETS to cover emissions from more sectors in the coming years.

[76] Gilbert Metcalf, “Implementing a Carbon Tax,” Resources for the Future, May 2017, https://media.rff.org/documents/RFF-Rpt-Metcalf_carbontax.pdf.

[77] Charles L. Ballard and Steven G. Medema, “The Marginal Efficiency Effects of Tax and Subsidies in the Presence of Externalities,” Journal of Public Economics 52 (1993), http://econ.msu.edu/faculty/ballard/docs/Marginal%20Efficiency%20Effects%20of%20Taxes%20and%20Subsidies,%20Journal%20of%20Public%20Economics%201993.pdf.

[78] International Energy Administration, “The Role of Gas in Today’s Energy Transitions,” World Energy Outlook Special Report, July 2019, https://iea.blob.core.windows.net/assets/cc35f20f-7a94-44dc-a750-41c117517e93/TheRoleofGas.pdf.

[79] Joseph E. Aldy, Timothy J. Brennan, Dallas Burtraw, Carolyn Fischer, Raymond J. Kopp, Molly K. Macauley, Richard D. Morgenstern, Karen L. Palmer, Anthony Paul, Nathan Richardson, and Roberton C. Williams III, “Considering a Carbon Tax: Frequently Asked Questions,” Resources for the Future, Nov. 2, 2012, https://www.resources.org/common-resources/considering-a-carbon-tax-frequently-asked-questions/.

[80] See for instance, Alex Muresianu and Garrett Watson, “Reviewing the Federal Tax Treatment of Research and Development Expenses,” Tax Foundation, Apr. 13, 2021, https://taxfoundation.org/research-and-development-tax/.

[81] Severin Borenstein and Lucas W. Davis, “The Distributional Effects of U.S. Clean Energy Tax Credits,” Tax Policy and the Economy 30:1 (2016), https://www.journals.uchicago.edu/doi/full/10.1086/685597.

[82] John Bistline, Neil R. Mehrotra, and Catherine Wolfram, “Economic Implications of the Climate Provisions of the Inflation Reduction Act,” Brookings Papers on Economic Activity BPEA Conference Draft, Mar. 30-31, 2023, https://www.brookings.edu/wp-content/uploads/2023/03/BPEA_Spring2023_Bistline-et-al_unembargoedUpdated.pdf; see also William McBride and Daniel Bunn, “Repealing Inflation Reduction Act’s Green Energy Credits Would Raise $570 Billion, JCT Projects,” Tax Foundation, Apr. 26, 2023, https://taxfoundation.org/inflation-reduction-act-green-energy-tax-credits-analysis/.

[83] Directorate-General for Energy, “Energy Costs, Taxes, and the Impact of Government Interventions on Investment,” European Commission, Oct. 23, 2020, https://op.europa.eu/en/publication-detail/-/publication/76c57f2f-174c-11eb-b57e-01aa75ed71a1/language-en.

[84] Statista, “Gross Domestic Product of the European Union (EU27) from 1995 to 2021,” Statista Research Department, Feb. 28. 2023, https://www.statista.com/statistics/279447/gross-domestic-product-gdp-in-the-european-union-eu/.

[85] Mar Delgado-Tellez, Marien Ferdinandusse, and Carolin Nerlich, “Fiscal Policies to Mitigate Climate Change in the Euro Area,” European Central Bank Economic Bulletin, 2022, https://www.ecb.europa.eu/pub/economic-bulletin/articles/2022/html/ecb.ebart202206_01~8324008da7.en.html.

[86] EIA, “Direct Federal Financial Interventions and Subsidies in Energy in Fiscal Year 2016,” U.S. Energy Information Administration, April 2018, https://www.eia.gov/analysis/requests/subsidy/pdf/subsidy.pdf.

[87] Ibid.

[88] William McBride and Daniel Bunn, “Repealing Inflation Reduction Act’s Green Energy Credits Would Raise $570 Billion, JCT Projects.”

[89] EU Commission, “European Green Deal,” accessed Mar. 23, 2023, https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal_en.

[90] Ibid, see also Robert C. Pietzcker, Sebastian Osorio, and Renato Rodrigues, “Tightening EU ETS Targets in Line with the European Green Deal: Impacts on the Decarbonization of the EU Power Sector,” Applied Energy 293 (July 2021), https://www.sciencedirect.com/science/article/pii/S0306261921003962.

[91] EU Commission, “A Green Deal Industrial Plan for the Net-Zero Age,” Feb. 1, 2023, https://commission.europa.eu/system/files/2023-02/COM_2023_62_2_EN_ACT_A%20Green%20Deal%20Industrial%20Plan%20for%20the%20Net-Zero%20Age.pdf.

[92] John M. Broder, “Cap and Trade Loses Its Standing as Energy Policy of Choice,” The New York Times, Mar. 25, 2010, https://www.nytimes.com/2010/03/26/science/earth/26climate.html.

[93] Zack Colman and Eric Wolff, “Why Greens Are Turning Away From a Carbon Tax,” Politico, Dec. 9, 2018, https://www.politico.com/story/2018/12/09/carbon-tax-climate-change-environmentalists-1052210.

[94] Amy Harder, “Joe Biden Unlikely to Push Carbon Tax as Part of Climate Change Plan,” Axios, Aug. 20, 2020, https://www.axios.com/2020/08/20/joe-biden-carbon-tax-climate-change-plan.

[95] Phillip Rossetti, Dan Bosch, and Dan Goldbeck, “Comparing Effectiveness of Climate Regulations and a Carbon Tax,” American Action Forum, Jul. 2, 2018, https://www.americanactionforum.org/research/comparing-effectiveness-climate-regulations-carbon-tax-123/.

[96] Shuting Pomerleau and Ed Dolan, “Carbon Pricing and Regulations Compared: An Economic Explainer,” Niskanen Center, September 2021, https://www.niskanencenter.org/wp-content/uploads/2021/09/Niskanen2-2.pdf.

[97] Kate A. Whitefoot and Steven J. Skerlos, “Design Incentives to Increase Vehicle Size Created From the U.S. Footprint-Based Fuel Economy Standards,” Energy Policy (2011), https://www.meche.engineering.cmu.edu/_files/images/research-groups/whitefoot-group/WS-FootprintFuelEconomy-EP.pdf.

[98] Lucas W. Davis and Christopher R. Knittel, “Are Fuel Economy Standards Regressive,” Journal of the Association of Environmental and Resource Economists 6:51 (March 2019), https://www.journals.uchicago.edu/doi/full/10.1086/701187; see also Arik Levinson, “Energy Efficiency Standards Are More Regressive than Energy Taxes: Theory and Evidence,” Journal of the Association of Environmental and Resource Economists 6:51 (March 2019), https://www.journals.uchicago.edu/doi/epdf/10.1086/701186.

[99] EU Commission, “‘Fit for 55’: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality,” Jul. 14, 2021, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52021DC0550&from=EN.

[100] Swedish Ministry of Infrastructure, “Sweden’s Integrated National Energy and Climate Plan,” Jan. 16, 2020, https://energy.ec.europa.eu/system/files/2020-03/se_final_necp_main_en_0.pdf.

[101] Robinson Meyer, “History’s Greatest Obstacle to Climate Progress Has Finally Fallen,” The Atlantic, Aug. 7, 2022, https://www.theatlantic.com/science/archive/2022/08/senate-climate-inflation-reduction-bill-passed/671073/.

[102] Rauno Sairinen, “Regulatory Reform and Development of Environmental Taxation: The Case of Carbon Taxation and Ecological Tax Reform in Finland” in Handbook of Research on Environmental Taxation, ed. Janet E. Milne and Mikael Skou Andersen, https://books.google.com/books?id=1ouS7zPW9T0C&printsec=frontcover&source=gbs_ge_summary_r&cad=0#v=onepage&q&f=false.