Key Findings

-

Many state and local governments impose ad valorem property taxes on tangible personal property (TPP) in addition to property taxes applied to land and structures. Tangible personal property taxes are levied on property that can be moved or touched, such as business equipment, machinery, inventory, and furniture.

-

Forty-three states include TPP in their property tax base. Of states reporting personal property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. data, state reliance on personal property in 2017 ranged from 1.79 percent to about 29 percent of state property taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. bases. For states reporting, personal property as a proportion of the average state tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. has declined from 11.27 percent to 9.98 percent from 2006 to 2017.

-

Taxes on tangible personal property are a source of tax complexity and nonneutrality, incentivizing firms to change their investment decisions and relocate to avoid the tax. Different types of TPP often receive preferential treatment depending on how the property is used or where it is invested, further distorting economic decision-making.

-

State and local governments have many options to alleviate the burden of TPP taxes. In addition to repealing them, options include enacting de minimis exemptions for firms with small amounts of property, expanding existing de minimis and universal exemptions already existing in statute, permitting localities to lower TPP taxes through lower millage rates or assessment ratios, and streamlining rules related to depreciation of TPP and the declaration of taxable TPP to tax authorities.

-

The experience of state and local governments expanding TPP tax exemptions and offering local-option tax reductions over the past decade can provide a road map for policymakers reforming TPP taxes in their jurisdictions. States should permit local-for-local tax swaps to reduce TPP tax burdens while transitioning localities from TPP taxes as a revenue source.

Introduction

Property taxes are one of the main sources of revenue for state and local governments, making up about 31.5 percent of total U.S. state and local tax collections as of fiscal year 2016.[1] Most property tax revenue flows to local governments, and localities are reliant on property taxes to fund government services such as public education, making up about 72 percent of all local tax revenue in fiscal year 2016.[2]

The property tax base is an important element of state and local tax codes, as property taxes alter business investment decisions and where people decide to live. While most people are familiar with residential property taxes on land and structures, known as real property taxes, many states also tax tangible personal property (TPP) owned by individuals and businesses.

Tangible personal property (TPP) comprises property that can be moved or touched, and commonly includes items such as business equipment, furniture, and automobiles. This is contrasted with intangible personal property, which includes stocks, bonds, and intellectual property like copyrights and patents.

Taxes on TPP make up a small share of state and local tax collections, but create high compliance costs, distort investment decisions, and are an archaic mode of taxation. This paper reviews the history and administration of tangible personal property taxation, examining how states have reformed their tax levies on TPP over the last 10 years. It will provide recommendations on how policymakers can alleviate TPP tax burdens while being conscious of how TPP taxes provide localities with needed revenue, using previous state experiences as a guide. This will give state and local governments a path forward to eliminate TPP taxes from their tax codes over the long run.

Overview of Taxes on Tangible Personal Property

In the United States, levies on personal property emerged in tandem with taxes on real property. Property taxes originally approximated a tax on wealth more than modern property taxes do, as taxes on personal property have waned.[3]

As the administrative burden of assessing personal property grew more complicated, policymakers in the 19th century sought to limit property taxes to real estate and certain types of personal property, such as inventory and machinery.[4] Individual property owned for personal use was gradually excluded from the tax base in the 20th century, with the focus shifting almost entirely to TPP owned by businesses.

Internationally, countries shifted from taxing tangible personal property: across the 36 Organisation for Economic Co-operation and Development (OECD) countries, only seven countries levy taxes on personal property: Austria, France, Germany, the Netherlands, Japan, the United Kingdom, and the United States.[5]

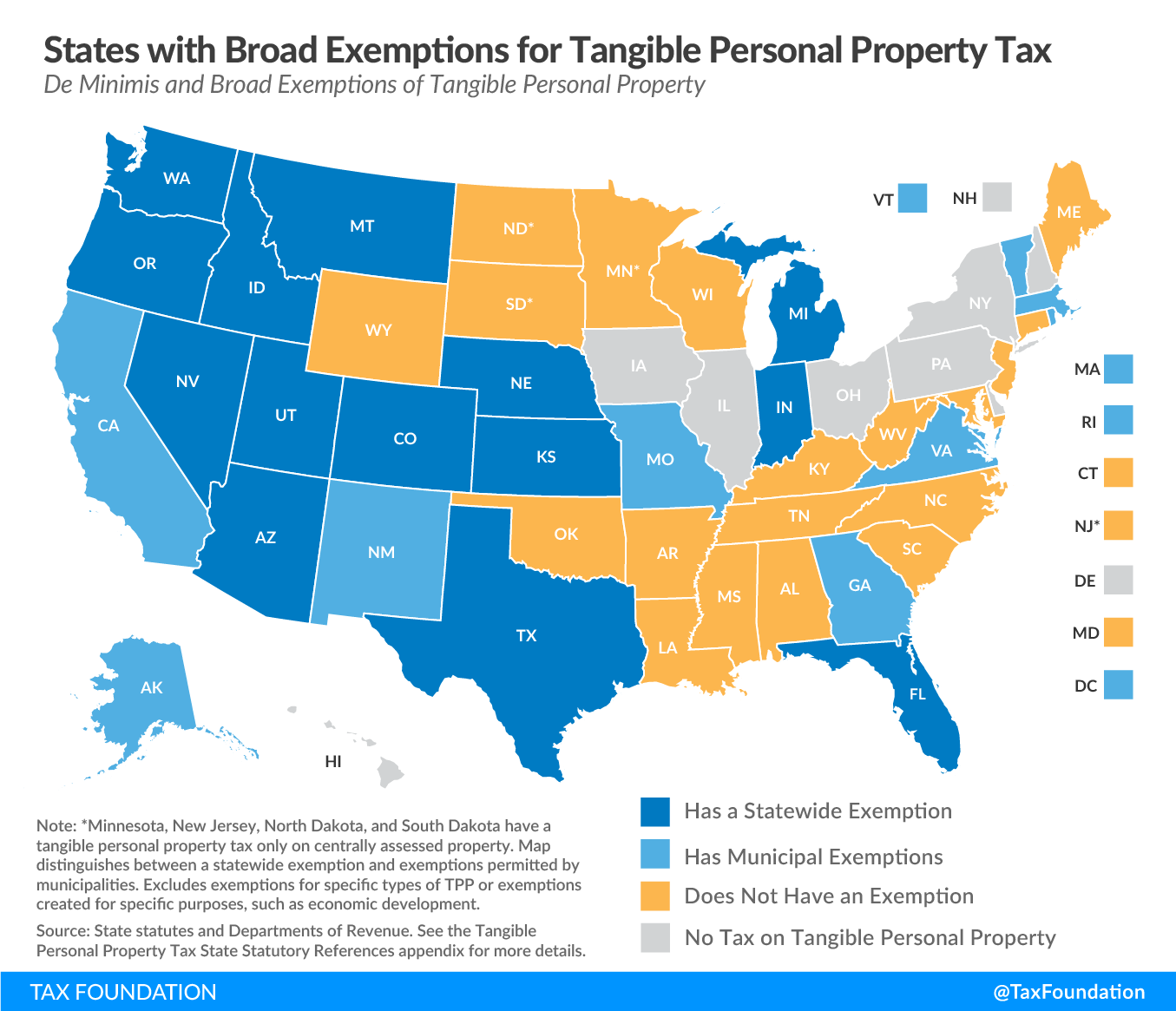

Over time, the American personal property tax base was eroded as states provided exemptions for different types of TPP. For example, agriculture, manufacturing, and renewable energy firms are often exempt from TPP levies. Many states offer exemptions for economic development if firms meet certain requirements, such as number of new jobs created or a set amount of investment in a locality.

For instance, Maryland permits local governments to provide a credit for expanding manufacturing facilities.[6] Similarly, Idaho allows counties to exempt TPP that is part of an investment of at least $500,000 in a new manufacturing plant for up to five years.[7]

Seven states (Delaware, Hawaii, Illinois, Iowa, New York, Ohio, and Pennsylvania) exempt all TPP from taxation, while another five states (Minnesota, New Hampshire, New Jersey, North Dakota, and South Dakota) exempt most TPP from taxation except for select industries that are centrally assessed, such as public utilities or oil and natural gas refineries.

How Tangible Personal Property is Taxed

Taxes on TPP are levied mostly by local governments, but they are regulated at the state level. There is much variation in how TPP is taxed. Property classifications, assessment ratios, and exemptions are often established by the state, with localities opting to tax TPP within the boundaries set by the state government. Twenty-three states permit municipalities to reduce the tax owed on TPP, while 27 states do not provide this option (see Table 2 in the Appendix).

The process for calculating and remitting TPP tax is complicated and varies depending on the state. Firms must first determine which property is eligible for taxation, which varies across states, counties, and municipalities. States usually exclude personal use property from TPP tax, instead focusing on business property.

Some states tax durable assets like motor vehicles, watercraft, and aircraft owned for personal use, as these assets have liquid secondary markets and avoid many of the administrative challenges of assessing other personal use property. For property that is not excluded or exempt from the TPP tax base, TPP tax liability is calculated by first determining the assessed value of the property and multiplying it by the assessment ratio for that class of property. Assessment ratios typically reduce the value of the property subject to tax, lowering a taxpayer’s tax liability.

Assessment ratios may also be higher for TPP than for real residential property. Fifteen states impose different assessment ratios for TPP than for real property. This means that TPP has a separate assessment ratio to determine the property value that will be subject to the property tax millage. States may also levy different assessment ratios for separate types of TPP. For example, South Carolina uses an assessment ratio of 5 percent for farm machinery and equipment, compared to 10.5 percent for most other TPP.

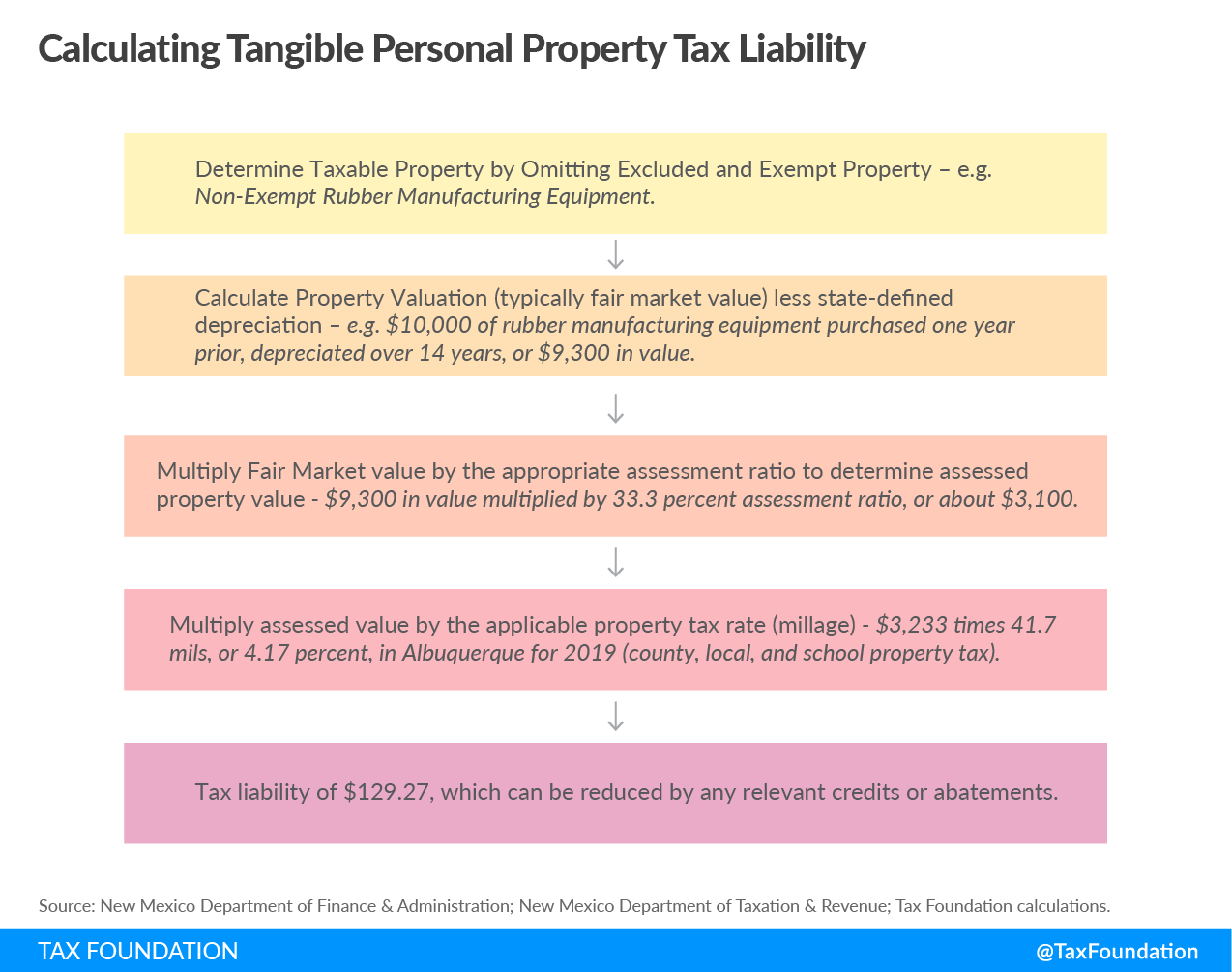

Figure 1.

Take, for example, a rubber factory in New Mexico. The business must first determine if it holds TPP subject to tax. New Mexico taxes TPP that is maintained by a business for which it took a federal tax depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. in the previous tax year. The business’ rubber manufacturing equipment may therefore be taxed, unless it is used for an exempt purpose. If the business is the lessee of a metropolitan redevelopment property project, for example, the TPP may still be exempt for up to seven years from acquisition.[9]

Once the business determines its taxable property, it must value the property. New Mexico appraises property by examining the cost of acquiring the property, the value of the property if sold, and the present value of the income generated by the property.[10] For machinery and equipment, the cost approach is most often used.[11]

The property value is then depreciated with the straight-line method using state-defined depreciation schedules.[12] The straight-line method of depreciation is calculated by dividing the value of the asset by the number of years it is expected to be used and subtracting that amount from the value of the asset each year.[13] This value is multiplied by the state’s uniform assessment ratio, which is set at 33.3 percent for all property, to arrive at the property’s taxable value.[14]

The taxable value is multiplied by the millage, which is the applicable property tax rate. States may either apply the same tax rate across real and tangible personal property or may levy different tax rates for different types of property. Levying different tax rates on TPP is one way that local governments may raise additional revenue on nonresidential property and favor specific taxpayers.[15]

Once TPP tax is calculated, taxpayers may reduce their liability through tax credits and abatements. Credits for TPP tax are commonly used to incentivize economic development. In Maryland, for example, localities may grant a tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. for new or expanding manufacturing facilities under certain conditions.[16] Abatements, which reduce tax liability after it has been assessed but before it has been paid, are another way states and municipalities may reduce TPP tax burdens. Nevada uses abatements for businesses operating in economic development zones, for instance.[17]

Tangible Personal Property Tax Limitations

Like the limitation regimes established for real property, state governments have instituted limits on the growth of personal property taxes. Property taxes may be limited through three methods: assessment limits, levy limits, and rate limits.[18]

Assessment limits cap increases in TPP tax produced through a rise in assessed value.[19] While real property often appreciates, personal property usually depreciates in value over time.[20] Assessment limits are therefore less applicable to personal property, as the property is unlikely to require a limitation in the growth in assessed value.

Personal property tax regimes may be subject to rate limits, which constrains the ability of state and local governments from raising tax rates above an absolute threshold or above a fixed growth rate. This limits revenue growth from personal property taxes through deliberate increases in tax rates. Rate limits are more common for TPP and are often defined statutorily at the state level.

Levy limits impose restrictions on the total amount of revenue collected from property taxes. Levy limits may apply to real property and personal property. In Washington, the state constitution limits tax from real and personal property to 1 percent of total property value unless voters approve a higher percentage.[21]

Economic Impact of Taxing Tangible Personal Property

Property taxes comport to the benefit principle and are economically efficient when levied on real property.[22] Real property taxes fund state and local government services, and they are a comparatively transparent method of taxation. Included in the real property tax base is land, which generates economic rents and is an efficient source of tax revenue.

Landowners cannot move their land and avoid tax liability and will fully bear a tax imposed on land. Taxes on real property are also imposed on buildings and other improvements on land, which affects the marginal decision to improve and build on the property; evidence suggests that property taxes are a significant factor in business location decisions.[23]

The relative efficiency and transparency of real property taxes can be contrasted with taxes on TPP.

Tangible Personal Property Taxes and Capital Taxation

Tangible personal property taxes are a type of stock tax on the value of a business’ tangible assets. These assets are used to generate a return, which is reduced by the TPP tax. This influences investment decisions, dissuading firms from making the marginal investment in their enterprises.

Imagine, for example, a manufacturing firm considering a new investment in machinery that faces a 0.5 percent effective TPP tax rate annually. If the machinery can be fully expensed and depreciates at 5 percent per year, the effective tax rate on the marginal investment in machinery is 6.67 percent due to the TPP tax.[24] This means that an investment that breaks even—earning a 0 percent net return and covering costs in present value—faces a 6.67 percent tax rate. In other words, 6.67 percent of the gross return from the marginal investment covers the TPP tax. A TPP tax dissuades firms from making new investments.[25]

Like other wealth taxes, TPP taxes are a poorly targeted form of capital taxation.[26] Ideally, the tax code exempts or lightly taxes a normal return–compensation for deferring consumption–and targets super-normal returns earned above that threshold. Super-normal returns generated by economic rents, innovative business models, and luck are less sensitive to taxation and are a more efficient source of tax revenue.[27]

A tax on tangible personal property, by contrast, disproportionately targets normal and low rates of return. For example, machinery producing a 4 percent return and facing a 0.5 percent effective TPP tax rate yields a 12.5 percent effective tax rate, while machinery producing a 10 percent return only yields a 5 percent effective tax rate from the same TPP tax.

TPP taxes discourage investment at the margin while poorly targeting super-normal returns, slowing economic growth, and creating a poorly targeted tax on returns to capital.

Nonneutral Tax Treatment of Tangible Personal Property

In addition to being a poor form of capital taxation, taxes on TPP are nonneutral. TPP is often treated differently from real property, with separate assessment ratios and millage rates.

As states have narrowed the TPP tax base by exempting personal-use property, expanding de minimis exemptions, or providing credits for favored activity (such as economic development), this has increased the variability of how TPP is treated in state property tax codes. Certain kinds of TPP, or TPP used in ways that make them ineligible for exemptions, credits, or abatements, are impacted more by property taxes.

Businesses attempt to avoid TPP tax by altering their investment and purchasing decisions. For example, a firm may avoid purchasing automated machinery in favor of using additional labor if the machinery is subject to a property tax. There is evidence that the elimination of TPP taxes increases investment in capital. In Ohio, policymakers exempted manufacturing equipment from the state’s TPP tax, resulting in greater capital investment and a shift from labor.[28] Increased capital investment improves labor productivity, raising wages higher than they would otherwise be for workers.

Alternatively, firms may shift their activity to take advantage of tax preferences for TPP, such as moving to municipalities where tax rates are lower for the TPP a firm owns. In some states, TPP is assessed on a specific “snapshot” date, while others may pro-rate TPP tax assessment for ownership of property owned for less than one year. For example, a piece of equipment owned for six months would have a 50 percent pro rata assessment. For states that use a “snapshot” date for assessment, firms may defer investments until after TPP tax has been levied for the tax year, with the goal of disposing of the property prior to the next time TPP taxes are levied.[29]

Compliance Costs and Lack of Transparency

Tangible personal property taxes are a type of tax on business inputs, as property such as machinery, equipment, and inventory are part of a firm’s production process. Firms may pass along the tax in the form of higher prices when goods or services are sold in the production process. This may conceal the impact of the tax on consumers, as consumers may pay higher prices as a result of a tax on TPP.

Taxes on TPP are “taxpayer active,” meaning that taxpayers must determine the tax liability that they owe, accounting for the depreciable value of their taxable property, the relevant assessment ratios and millage, and applicable credits, abatements, and refunds for which they are eligible. This increases the cost of complying with TPP taxes.

Compliance costs are higher in states that have different assessment ratios and millage rates for different types of TPP. Fifteen states use separate assessment ratios for residential property and TPP (see Table 2 in the Appendix).

Firms with different types of TPP across multiple municipalities may have to sort through dozens of different exemption requirements, assessment ratios, millage rates, TPP declaration forms, and relevant tax credits, which amplifies the cost of compliance.

Some states have made efforts to reduce the compliance burden on firms. Nevada’s Tax Commission, for example, may exempt TPP if the annual tax is less than the cost of collecting it.[30] This also helps reduce administrative costs for the state.

Twenty-seven states and the District of Columbia simplify part of the administration of TPP taxes by offering a uniform tangible personal property declaration form that can be used across the state. In the other 16 states, firms must use locality-specific declaration forms and processes to calculate and remit their TPP tax liability. For firms with TPP in many jurisdictions, this is a source of tax complexity and a high cost of compliance.

Recent Trends in Tangible Personal Property Taxation

Of the states with data available for personal property, personal property made up 11.27 percent of the average state property tax base in 2006. This fell to 10.15 percent of the average state property tax base in 2012 and to 9.98 percent of the average state property tax base in 2017 (See Table 1).[31] States are relying slightly less on personal property as part of the property tax base.[32]

|

Source: Lincoln Institute for Land Policy, “Significant Features of the Property Tax.®” |

|||

| State | 2006 Personal Property | 2012 Personal Property | 2017 Personal Property |

|---|---|---|---|

| Arkansas | 24.98% | 21.09% | 22.54% |

| California | 4.11% | 5.66% | 5.20% |

| Colorado | 12.06% | 14.61% | 6.90% |

| Connecticut | 6.09% | 10.73% | 13.28% |

| Florida | 7.43% | 7.63% | 7.00% |

| Georgia | 17.09% | 14.83% | 11.03% |

| Indiana | 15.27% | 14.03% | 15.42% |

| Kentucky | 8.52% | 8.28% | 16.74% |

| Louisiana | 29.94% | 29.94% | 28.96% |

| Maine | 7.75% | 4.90% | 3.78% |

| Maryland | 2.32% | 3.11% | 3.26% |

| Massachusetts | 2.28% | 3.00% | 3.00% |

| Michigan | 8.93% | 8.51% | 8.24% |

| Mississippi | 31.12% | 28.47% | 28.08% |

| Missouri | 20.90% | 19.45% | 18.79% |

| Montana | 7.57% | 8.98% | 7.51% |

| Nebraska | 6.35% | 6.52% | 4.92% |

| Nevada | 3.94% | 6.01% | 5.26% |

| New Mexico | N/A | 1.86% | 1.30% |

| North Carolina | 17.06% | 13.24% | 7.61% |

| Oklahoma | 17.91% | 18.75% | 22.74% |

| Oregon | 3.38% | 2.74% | 2.71% |

| Rhode Island | 4.30% | 3.36% | 4.04% |

| South Carolina | 16.05% | 12.27% | 14.52% |

| Tennessee | 7.80% | 6.71% | 6.85% |

| Texas | 12.77% | 12.19% | 11.64% |

| Utah | 14.16% | 11.19% | 10.76% |

| Virginia | 9.20% | 7.68% | 8.37% |

| Washington | 5.12% | 5.33% | 4.64% |

| Wisconsin | 2.32% | 2.33% | 2.51% |

| Wyoming | N/A | 1.12% | 1.79% |

| Average | 11.27% | 10.15% | 9.98% |

Since 2006, states like Connecticut and Kentucky have markedly increased the relative share of personal property in their property tax bases, while Colorado, Georgia, Maine, North Carolina, and Utah have markedly reduced the relative share that personal property makes up in the property tax base.

While no state has eliminated TPP outright from its property tax base over the past decade, states have expanded their use of de minimis exemptions and raised exemption thresholds for TPP tax. This reduces the number of firms subject to TPP tax or lowers tax liability for firms which owe TPP tax and may explain some of the reduced reliance on TPP in state property tax bases.

Expansion of De Minimis Exemptions

De minimis exemptions provide relief for small firms by eliminating their tax liability if they remain below a valuation threshold for their tangible personal property. These exemptions lower compliance costs for firms with a small amount of otherwise taxable TPP.

Figure 2.

Indiana, for example, recently raised its de minimis exemption from $20,000 to $40,000 in business personal property per county and prohibited counties from collecting TPP tax filing fees from businesses that file but do not have a tax liability.[33] Indiana originally implemented its $20,000 de minimis exemption in 2015, and 89,749 taxpayers took advantage of the exemption.[34] An additional 28,300 exemptions were projected by the Indiana Legislative Services Agency as a result of the increase in the exemption threshold.[35]

Since 2012, Utah, Colorado, Idaho, and Indiana have enacted or expanded their de minimis exemptions. Utah exempts individual items of TPP with an acquisition cost of $1,000 or less in addition to exempting TPP with a fair market value under $10,800.[36] In Colorado, the legislature added a state income tax credit to reimburse taxpayers’ TPP tax between $7,001 and $15,000, effectively raising the state’s $7,700 TPP exemption.[37]

As states consider de minimis exemptions for TPP, policymakers should consider making the exemption threshold also a filing threshold. This reduces compliance costs for firms, as firms under the threshold may have to file in many localities if filing requirements remain in place when firms are under the de minimis threshold. Indiana, for example, previously required taxpayers to file a TPP tax return and pay filing fees even if they qualified for exemption. In April 2019, the state prohibited counties from collecting TPP tax filing fees but kept the filing requirement for exempt taxpayers.[38]

Most state exemptions are indexed to inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. . Oregon’s de minimis exemption was originally set at $12,500 but has since risen to $17,000.[39] Indexing exemption thresholds ensures that firms are not pushed above the threshold over time due to inflation. States that have not indexed their exemption thresholds should consider doing so, which will help maintain the value of the exemption for firms over time. Texas, for instance, should index its TPP de minimis exemption of $500, after raising their de minimis exemption to cover more firms that own TPP.[40]

Broader Tangible Personal Property Tax Exemptions

In addition to de minimis exemptions, some states provide broader exemptions for a certain amount of TPP for all taxpayers. Florida, for example, provides a $25,000 exemption for all property in the county where the property is used for business purposes.[41] Universal exemptions avoid the tax cliff that de minimis exemptions face and reduce the TPP tax burden for more firms.[42]

Idaho enacted a $100,000 exemption on personal property taxes in each county per taxpayer.[43] All TPP worth less than $3,000 is also exempt, which works like Utah’s exemption for individual items of TPP costing less than $1,000. Utah and Idaho’s exemptions show that states may pair a broad de minimis or universal exemption with an exemption for individual pieces of TPP under a certain value.

For example, a firm in Idaho may have $110,000 in TPP. The first $100,000 is exempt from tax; individual items worth less than $3,000 may also be exempt even above the $100,000 threshold.[44] Washington takes a similar approach by exempting $15,000 of TPP for heads of household, corporations, and limited liability corporations while exempting personal property worth $500 or less from property tax.[45]

Nebraska also exempted the first $10,000 in personal property from taxation in 2015, and included a provision reimbursing municipalities for lost tax revenue from the exemption.[46] Montana has a limited TPP tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. for commercial and industrial TPP, which is classified as a distinct type of property. The first $100,000 of commercial and industrial TPP is exempt from TPP tax. Prior to enactment of the $100,000 exemption, Montana had a $20,000 de minimis threshold. By raising the limit and making the exemption available to all firms, Montana reduced the number of firms exposed to TPP tax liability.[47]

One approach Michigan has taken is to create two separate exemptions: one for eligible manufacturing TPP and a de minimis exemption on TPP worth less than $80,000. To replace the revenue lost from these exemptions, Michigan established an Essential Services Assessment (ESA). The ESA is a tax on the TPP using the exemption for eligible manufacturing personal property with a millage rate ranging from 0.9 mills to 2.4 mills, resulting in a lower tax burden for most taxpayers with TPP.[48]

Areas for Future Reform

States have made progress in reducing TPP tax burdens over the past decade, but there remains room for reform. The most fruitful areas of reform include exempting major business inputs such as inventory, machinery, and equipment from TPP tax, which make up a large component of TPP tax bases. Additionally, states should permit localities to reduce TPP taxes in their jurisdictions and streamline TPP depreciation rules, simplifying one aspect of TPP tax administration.

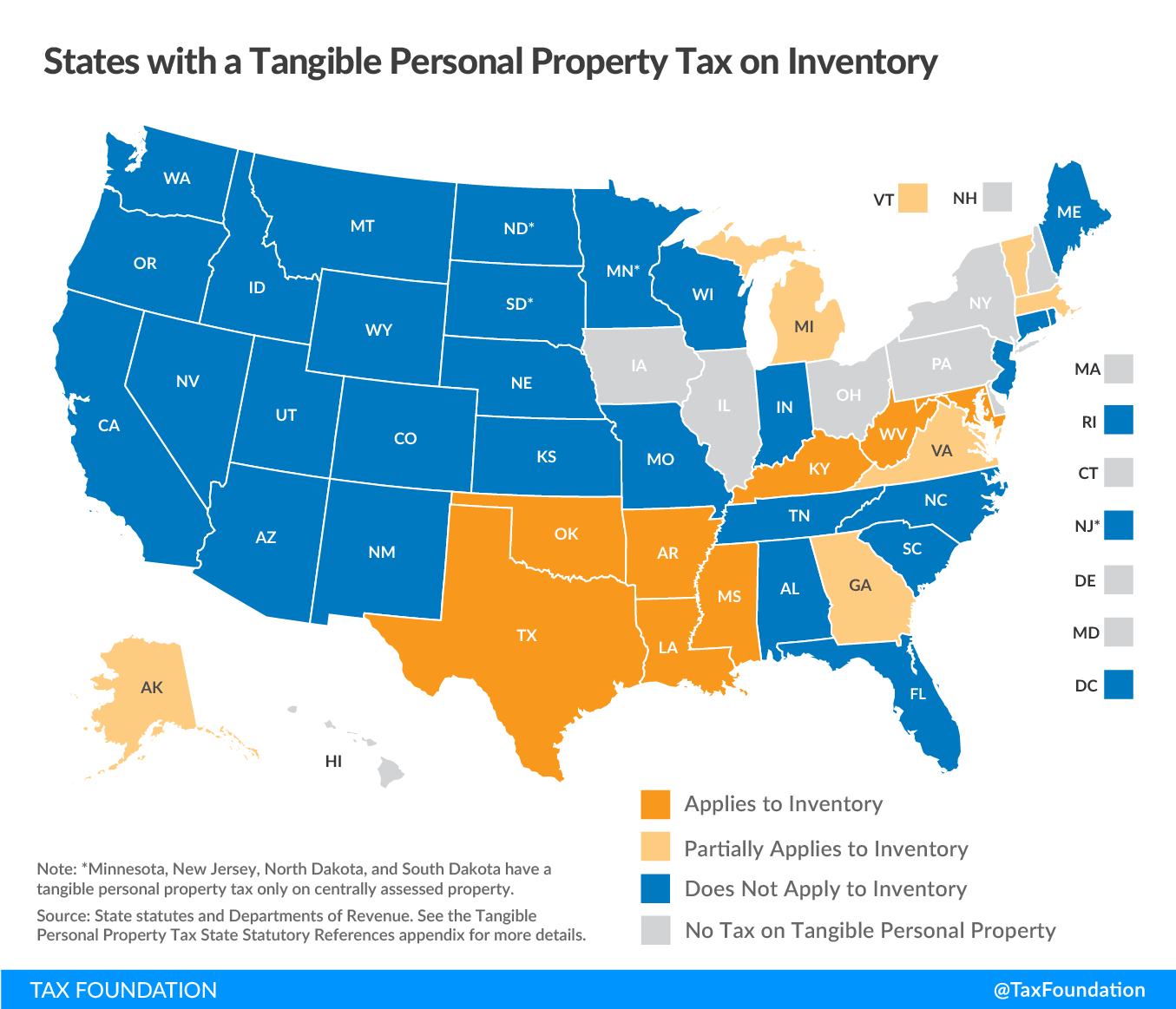

Taxation of Inventory

Fourteen states levy TPP taxes on inventory in some form. Eight states fully tax inventory, while six states tax inventory partially but exempt certain types of inventory or exempt inventory from property tax at the state level. For example, in Georgia, inventory is exempt from state property taxes, but localities may tax inventory. Ninety-three percent of counties in Georgia partially exempt inventory using a freeport exemption ranging from 20 percent to 80 percent of the value of the inventory.[49] In Michigan, inventory is exempt from property tax, except for inventory under lease.[50]

Figure 3.

Taxes on inventory are nonneutral, as businesses with larger quantities of inventory, like manufacturers, are disproportionately burdened by the tax.[51] Businesses with little to no inventory escape this form of property taxation, despite using local and state government services like firms with larger amounts of inventory.

Inventory taxes, like many other taxes on TPP, are often locally assessed and are a revenue source for localities, making it a challenge to replace the revenue when states exempt inventory from the property tax base.

States with property taxes on inventory are considering ways to eliminate the burden on firms while not depriving municipalities of the tax revenue. Kentucky, for example, enacted a state income tax credit that offsets TPP tax paid on inventory. The credit is being phased in from 2018 to 2021, with the credit amount rising by 25 percent increments every tax year.[52] Taxpayers will still need to calculate and remit their TPP tax liability but will find relief through a reduced state income tax liability. The tax credit is nonrefundable, meaning that taxpayers can only reduce state income tax liability to zero. Beyond that amount, taxpayers will not find additional relief from TPP tax on inventory.

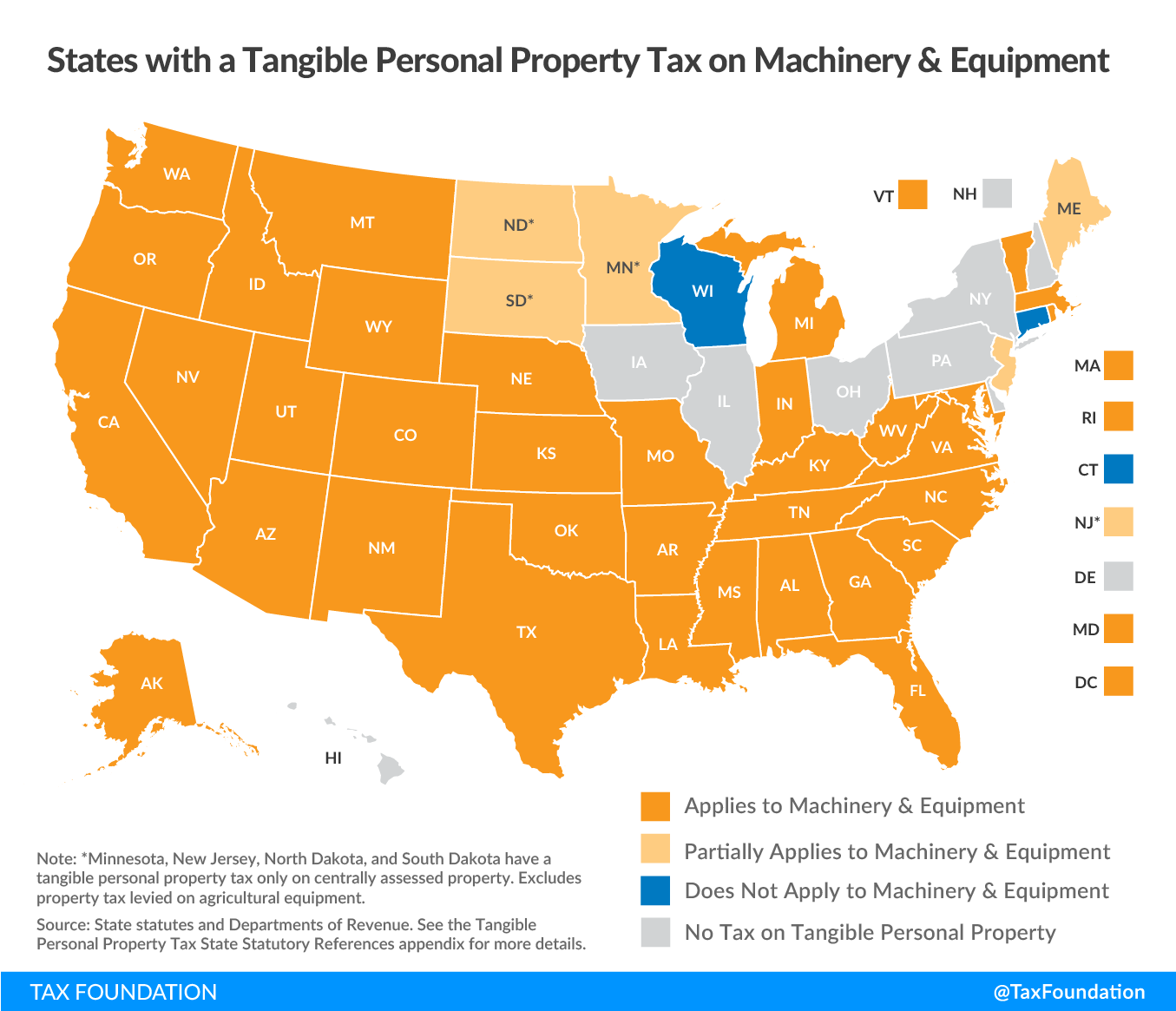

Taxation of Machinery and Equipment

Machinery and equipment make up a large portion of state TPP tax bases and are key business inputs for firms.

Figure 4.

Thirty-six states levy TPP taxes on machinery and equipment. Often, agricultural machinery and equipment will be granted lower assessment ratios or millage rates than other forms of TPP. For example, Missouri uses a 12 percent assessment ratio for farm machinery but a 33.3 percent ratio for most other TPP.[53] Similarly, South Carolina assesses farm machinery and equipment at 5 percent when most TPP is assessed at 10.5 percent of value.[54] Other states, like Utah, exempt farm machinery and equipment outright.[55]

Some states exempt all machinery and equipment from the property tax base. Like inventory, these forms of property are critical to many firms and are a large determinant of businesses’ TPP tax liability in manufacturing and related industries. To smooth out the impact of exempting machinery and equipment, some states only exempt property acquired after the exemption is enacted. Kansas, for example, did so when enacting an exemption of commercial and industrial machinery in 2006.[56]

As firms replace machinery that depreciates over time, more property becomes subject to the exemption. Tax revenue gradually declines, giving the state and localities an adjustment period to replace the lost revenue. This should be an approach that other states consider when balancing revenue stability for localities with the repeal of TPP taxes on machinery and equipment.

Local-Option Exemptions of Tangible Personal Property Tax

Another option to reduce TPP tax burdens is to authorize localities to reduce TPP tax rates or exempt types of TPP. Twenty-three states permit localities to partially or fully exempt firms from TPP taxation. This gives municipalities greater control over their property tax base while transitioning them from relying on TPP taxes for revenue.

State and local governments should carefully consider the trade-offs involved when exempting or eliminating TPP tax. While taxes on TPP violate the principles of sound tax policy and would not exist in an ideal tax system, local governments rely on the tax revenue generated by taxes on TPP. State governments have considered tax swaps to resolve this problem in other contexts, but these schemes are often difficult to implement.[57]

Both Kentucky and Louisiana have tried to resolve the problem of lost revenue by creating state income tax credits to eliminate a firm’s inventory tax liability. Local governments still receive tax revenue, with the state government refunding the levy back to businesses.[58] In 2016, the tax rebate cost Louisiana about $225 million.[59] Louisiana is exploring possible local-for-local tax swaps, given the complexity of the current rebate system.

Slow phaseouts over multiple years can help mitigate the problems associated with a loss of revenue. Vermont, for example, authorized cities and towns to exempt inventory and other TPP from local taxes, with the option of phasing in the exemption up to 10 years.[60] From 2013 to 2018, the number of municipalities taxing inventory has fallen from 34 to seven (about 3 percent of all municipalities). The same trend occurred with the taxation of machinery and equipment, with the number of municipalities levying those taxes dropping from 62 to 45 (about 18 percent of all municipalities).[61] This shows that localities can make headway eliminating taxes on inventory while finding alternative revenue sources over time.

When localities are permitted to reduces taxes on TPP, there is evidence that this increases revenue growth for other types of taxes. In Pennsylvania, counties that repealed their taxes on personal property between 1978 and 1990 experienced greater growth in revenue from their real estate taxes than counties that kept a tax on personal property.[62] Higher tax revenue from other sources may help localities as they transition from TPP taxes, but would not fully cover the decline in revenue in most cases. Instead, local governments should consider local-for-local tax swaps to maintain revenue stability.

Depreciation Rules

State and local governments provide depreciation schedules for the purposes of TPP that is usually different from the federal treatment of the property for income tax purposes. Many states use straight-line depreciation schedules when calculating TPP tax.

Navigating different depreciation schedules for income tax and property tax is a source of tax complexity for businesses, and policymakers should consider ways to simplify the process of depreciating TPP. This is especially true in states that do not conform to depreciation rules for income tax purposes with the federal income tax, as firms must calculate applicable depreciation more than once to determine income tax liability and TPP tax liability.[63]

One method some states have taken to improve the tax treatment of personal property is improving how taxable TPP is depreciated. In 2011, Arizona accelerated the depreciation provided for certain classes of taxable business property, and the legislature extended the accelerated depreciation in 2017.[64] This approach shortened the depreciation schedule, lowering tax liability on TPP.

Shortening depreciation schedules is another lever for states to lower TPP tax burdens on firms. The schedules could also be adjusted over time to give localities an opportunity to adapt to the lower revenue raised from the tax.

Conclusion

The taxation of tangible personal property by state and local governments is a blight on a relatively efficient and transparent type of tax. Property taxes, when properly structured, conform to the benefit principle by supporting government services used by property owners in a transparent manner.[65]

Taxes on tangible personal property, on the other hand, increase the complexity of state and local tax codes, discriminate against taxpayers based on their capital structure, and change economic behavior by incentivizing taxpayers to modify their property ownership to avoid the tax. Efforts by some states to exempt major types of TPP, raise de minimis exemption thresholds, and provide a local option to reduce TPP taxes show that progress is possible, despite the challenge a reduction or elimination of TPP taxes poses to state and local budgets.

To establish buy-in among municipal stakeholders, states should consider options to consider the revenue lost from eliminating TPP taxes or expanding TPP tax exemptions. State-for-local tax swaps, such as providing state income tax credits to firms that pay TPP taxes, are challenging to effectively administer and may not unanchor localities from their reliance on TPP tax revenue. Instead, states should grant localities greater authority to reduce TPP tax burdens and replace the lost revenue elsewhere. Local option tax reductions are a more promising approach and have been shown to work in states like Vermont over several years.

With some courage, states have an opportunity to rid themselves of an antiquated tax, streamlining their property tax codes and making their tax systems more consistent with the principles of sound tax policy.

Appendix

|

Source: State statutes and state departments of revenue. |

||||||

| State | Different rate or assessment ratio for personal vs. real property? | TPP applies to inventory? | TP applies to non-ag equipment and machinery? | State Uniform Personal Property Declaration Form? | Local Option to reduce TPP tax? | Economic Development Exemption? |

|---|---|---|---|---|---|---|

| Alabama | No | No | Yes | Yes | Yes | Yes |

| Alaska | No | Partial | Yes | No | Yes | Yes |

| Arizona | Yes | No | Yes | No | No | No |

| Arkansas | No | Yes | Yes | Yes | No | No |

| California | No | No | Yes | No | Yes | Yes |

| Colorado | Yes | No | Yes | Yes | No | No |

| Connecticut | No | No | No | Yes | Yes | Yes |

| Delaware | – | – | – | – | – | – |

| Florida | No | No | Yes | Yes | Yes | Yes |

| Georgia | No | Partial | Yes | Yes | Yes | Yes |

| Hawaii | – | – | – | – | – | – |

| Idaho | No | No | Yes | Yes | Yes | Yes |

| Illinois | – | – | – | – | – | – |

| Indiana | No | No | Yes | Yes | Yes | Yes |

| Iowa | – | – | – | – | – | – |

| Kansas | Yes | No | Yes | Yes | Yes | Yes |

| Kentucky | Yes | Yes | Yes | Yes | Yes | Yes |

| Louisiana | Yes | Yes | Yes | Yes | Yes | Yes |

| Maine | No | No | Partial | No | No | Yes |

| Maryland | Yes | Yes | Yes | Yes | Yes | Yes |

| Massachusetts | No | Partial | Yes | Yes | Yes | Yes |

| Michigan | No | Partial | Yes | Yes | Yes | Yes |

| Minnesota | No | N/A | Partial | N/A | No | Yes |

| Mississippi | No | Yes | Yes | Yes | Yes | Yes |

| Missouri | Yes | No | Yes | No | Yes | No |

| Montana | Yes | No | Yes | Yes | No | Yes |

| Nebraska | No | No | Yes | Yes | No | Yes |

| Nevada | No | No | Yes | No | Yes | Yes |

| New Hampshire | – | – | – | – | – | – |

| New Jersey | No | No | Partial | Yes | No | Yes |

| New Mexico | No | No | Yes | No | Yes | Yes |

| New York | – | – | – | – | – | – |

| North Carolina | No | No | Yes | Yes | No | No |

| North Dakota | No | No | Partial | Yes | No | Yes |

| Ohio | – | – | – | – | – | – |

| Oklahoma | Yes | Yes | Yes | Yes | No | Yes |

| Oregon | No | No | Yes | Yes | Yes | Yes |

| Pennsylvania | – | – | – | – | – | – |

| Rhode Island | Yes | No | Yes | No | Yes | Yes |

| South Carolina | Yes | No | Yes | Yes | Yes | Yes |

| South Dakota | No | No | Partial | Yes | No | Yes |

| Tennessee | Yes | No | Yes | No | No | No |

| Texas | No | Yes | Yes | No | No | No |

| Utah | No | No | Yes | No | No | No |

| Vermont | No | Partial | Yes | No | Yes | Yes |

| Virginia | Yes | Partial | Yes | No | Yes | Yes |

| Washington | No | No | Yes | No | No | Yes |

| West Virginia | Yes | Yes | Yes | Yes | No | No |

| Wisconsin | No | No | No | Yes | No | Yes |

| Wyoming | No | No | Yes | Yes | No | Yes |

| District of Columbia | Yes | No | Yes | Yes | N/A | Yes |

| Total “Yes” | 15 | 7 | 36 | 28 | 23 | 34 |

Notes

[1] Janelle Cammenga, “To What Extent Does Your State Rely on Property Taxes?” Tax Foundation, May 1, 2019, https://taxfoundation.org/state-and-local-property-tax-reliance-2019/.

[2] Sourced from Census Bureau data and Tax Foundation calculations. For an overview of state and local tax collections, see Jared Walczak, “Unpacking the State and Local Tax Toolkit: Sources of State and Local Tax Collections,” Tax Foundation, June 20, 2017, 4-5, https://taxfoundation.org/toolkit-sources-state-local-tax-collections/.

[3] Joan Youngman, A Good Tax: Legal and Policy Issues for the Property Tax in the United States (Cambridge, MA: Lincoln Institute of Land Policy, 2016), 5.

[4] Ibid, 5.

[5] Andrey V. Korytin and Tatiana A. Malinina, “Международный опыт налогообложения движимого имущества организаций” [“International Experience in Taxation of Business Personal Property”], inansovyj žhurnal — Financial Journal, No. 2, 2019, 22-36, https://econpapers.repec.org/article/frufinjrn/190202_3ap_3a22-36.htm.

[6] Md. Code, Tax -Prop. §§ 9-205, -230.

[7] Idaho Code Ann. § 63-602NN.

[8] New Mexico Taxation & Revenue Department, “2019 Business Personal Property Valuation Guidelines,” 58, http://www.tax.newmexico.gov/uploads/files/2019%20Buisness%20Personal%20Property%20Manual.pdf.

[9] N.M. Stat. § 7-36-3.1

[10] New Mexico Taxation & Revenue Department, “2019 Business Personal Property Valuation Guidelines,” 23-25.

[11] Ibid, 25.

[12] Ibid, 3; For an overview of the differences among depreciation methods, see Stephen J. Entin, “The Tax Treatment of Capital Assets and Its Effect on Growth,” Tax Foundation, Apr. 24, 2013, https://taxfoundation.org/article-nstax-treatment-capital-assets-and-its-effect-growth-expensing-depreciation-and-concept-cost-recovery/.

[13] States may use federally defined depreciation schedules under the Modified Accelerated Cost Recovery System (MACRS) or states may define their own depreciation schedules for tangible personal property.

[14] N.M. Stat. § 7-37-3.

[15] Joyce Errecart, Ed Gerrish, and Scott Drenkard, “States Moving Away From Taxes on Tangible Personal Property,” Tax Foundation, Oct. 4, 2012, 4, https://taxfoundation.org/states-moving-away-taxes-tangible-personal-property.

[16] MD. Code Ann. Tax-Prop. §§ 9-205, -230.

[17] Nev. Rev. Stat. § 274.310.

[18] See generally, Jared Walczak, “Property Tax Limitation Regimes: A Primer,” Tax Foundation, Apr. 23, 2018, https://taxfoundation.org/property-tax-limitation-regimes-primer/.

[19] Ibid, 1.

[20] This excludes TPP that may appreciate like real property, such as collectables.

[21] Wash. Rev. Code § 84.52.050; see also Washington Department of Revenue Property Tax Division, “Property Tax Levies,” September 2018, 109, https://dor.wa.gov/sites/default/files/legacy/Docs/Pubs/Prop_Tax/LevyManual.pdf.

[22] For a review of the economic impact of property taxes, see Jared Walczak, Scott Drenkard, and Joseph Bishop-Henchman, 2019 State Business Tax Climate Index, Tax Foundation, Sept. 26, 2018, 42-47, https://taxfoundation.org/publications/state-business-tax-climate-index/.

[23] Ibid, 42.

[24] Author calculations using a 7 percent rate of return. Under a full expensing regime, a firm’s marginal effective tax rate (METR) is unaffected by the income tax rate.

[25] See generally, Huaqun Li, “Measuring Marginal Tax RateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. on Capital Assets,” Tax Foundation, Dec. 12, 2017, https://taxfoundation.org/measuring-marginal-tax-rate-capital-assets/.

[26] Nicole Kaeding and Kyle Pomerleau, “Sen. Warren’s Wealth TaxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary. is Problematic,” Tax Foundation, Jan. 24, 2019, https://taxfoundation.org/warren-wealth-tax/.

[27] Garrett Watson and Nicole Kaeding, “Tax Policy and Entrepreneurship: A Framework for Analysis,” Tax Foundation, Apr. 3, 2019, 4-6, https://taxfoundation.org/tax-policy-entrepreneurship/.

[28] Sian Mughan and Geoffrey Propheter, “Estimating the Manufacturing Employment Impact of Eliminating the Tangible Personal Property Tax: Evidence from Ohio,” Economic Development Quarterly 31(4), Sept. 26, 2017, https://journals.sagepub.com/doi/abs/10.1177/0891242417732123.

[29] Errecart, Gerrish, and Drenkard, “States Moving Away From Taxes on Tangible Personal Property,” 8.

[30] Nev. Rev. Stat. § 361.068(2).

[31] Lincoln Institute of Land Policy, “Tax Base by Property Type,” https://www.lincolninst.edu/research-data/data-toolkits/significant-features-property-tax/topics/property-tax-base.

[32] We cannot say that personal property tax collections or burdens are lower in 2017 than in 2012 or 2006, as the property tax base data omits the tax rate that was assessed on personal property. For example, a state may offset a narrower personal property tax base with a higher tax rate on the remaining personal property subject to tax to keep tax collections constant. This data also includes intangible personal property, which could also have changed among 2006, 2012, and 2017 as a proportion of the property tax base.

[33] Katherine Loughead, “Indiana Chips Away at Tangible Personal Property Taxes,” Tax Foundation, Apr. 5, 2019, https://taxfoundation.org/indiana-tangible-personal-property-tax/.

[34] Ibid, and Indiana Legislative Services Agency, “SB 233 Fiscal Impact Statement,” Apr. 2, 2019, http://iga.in.gov/legislative/2019/bills/senate/233#document-0225b146.

[35] Ibid.

[36] Utah Code Ann. § 59-2-1115; see also Utah Tax Commission, “Business Personal Property Taxes,” January 2019, https://tax.utah.gov/forms/pubs/pub-20.pdf.

[37] Colo. Rev. Stat. § 39-22-537.

[38] Loughead, “Indiana Chips Away at Tangible Personal Property Taxes.”

[39] Oregon Department of Revenue, “Personal Property Assessment and Taxation,” https://www.oregon.gov/DOR/programs/property/Pages/personal-property.aspx.

[40] Texas Tax Code Ann. § 11.145.

[41] Fla. Stat. § 196.183.

[42] For de minimis exemptions, taxpayers lose the exemption once they exceed the exemption threshold, generating a higher implied marginal tax rate.

[43] Idaho State Tax Commission, “New Idaho law allows property tax exemption for $100,000 in personal property value for business,” Apr. 17, 2013, https://tax.idaho.gov/n-feed.cfm?idd=401.

[44] Idaho exempts the first $100,000 of a taxpayer’s TPP that is not otherwise exempt, so there is no ambiguity on whether to count a piece of property worth less than $3,000 toward broader $1000,000 exemption. See Idaho State Tax Commission, “Personal Property Valuation,” https://tax.idaho.gov/i-2008.cfm.

[45] Wash. Admin. Code. § 458-16-115(3); Wash. Rev. Code § 84.36.015.

[46] Sarah Curry and Luke Ashton, “This Time, It’s Personal: Nebraska’s Personal Property Tax,” Platte Institute, Sept. 26, 2017, https://www.platteinstitute.org/research/detail/this-time-its-personal-nebraskas-personal-property-tax.

[47] Montana Chamber of Commerce, “Lower the Business Equipment Tax,” https://www.montanachamber.com/wp-content/uploads/2017/05/MCC-Issue-Brief-BET.pdf.

[48] Michigan State Tax Commission, “Assessor Guide to Eligible Manufacturing Personal Property Tax Exemption and ESA,” February 2019, 19-21, https://www.michigan.gov/documents/treasury/Assessor_Guide_to_PPT_Exemptions_101016_538412_7.pdf.

[49] Ga. Code § 48-5-48.2. See also Georgia Department of Revenue, “Freeport Exemption,” https://dor.georgia.gov/freeport-exemption.

[50] Mich. Comp. Laws § 211.9c.

[51] Nicole Kaeding, “Does Your State Tax Business Inventory?” Tax Foundation, Sept. 7, 2016, https://taxfoundation.org/does-your-state-tax-business-inventory/.

[52] Commonwealth of Kentucky Department of Revenue, “Kentucky Technical Advice Memorandum 18-07,” Nov. 26, 2019, https://revenue.ky.gov/TaxProfessionals/PublishingImages/Pages/Guidance/KY-TAM-18-07.pdf.

[53] Mo. Rev. Stat. § 137.115(3).

[54] S.C. Code Ann. § 12-43-220.

[55] Utah Code Ann. § 59-2-1101.

[56] Kan. Stat. Ann. § 79-223.

[57] See generally, Jared Walczak, “Why State-for-Local Tax Swaps Are So Hard to Do,” Tax Foundation, Apr. 18, 2019, https://taxfoundation.org/state-for-local-tax-swaps/.

[58] La. Rev. Stat. Ann. § 47:6006.

[59] Tyler Bridges, “Much-maligned inventory tax faces possible phase-out, but powerful forces oppose proposed alternative,” The (Baton Rouge, La.) Advocate, May 7, 2017, https://www.theadvocate.com/baton_rouge/news/politics/legislature/article_a14e72f8-31cb-11e7-b7fa-dbe0225bed47.html.

[60] VT. Stat. Ann. tit. 32, § § 3848-3849.

[61] Vermont Department of Taxes, Division of Property Valuation and Review, “Annual Report: Based on 2018 Grand List Data,” Jan. 14, 2019, https://tax.vermont.gov/sites/tax/files/documents/PVR-Annual%20Report-2018%20Grand-List-Data.pdf.

[62] William F. Stine, “The Effect of Personal Property Tax Repeal on Pennsylvania’s Real Estate TaxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs. Growth and Stability,” National Tax Journal, 56(1), March 2003, 45-60, https://econpapers.repec.org/article/ntjjournl/v_3a56_3ay_3a2003_3ai_3a1_3ap_3a45-60.htm.

[63]For information on state conformity on federal depreciation rules for income tax purposes, see Jared Walczak, “Toward a State of Conformity: State Tax Codes a Year After Federal Reform,” Tax Foundation, Jan. 28, 2019, 28-29, https://taxfoundation.org/state-conformity-one-year-after-tcja/.

[64]Arizona Commerce Authority, “Additional Depreciation,” https://www.azcommerce.com/incentives/additional-depreciation/.

[65]Walczak, Drenkard, and Bishop-Henchman, 2019 State Business Tax Climate Index, 42.

Note: The author thanks Brittany Moore for contributing to statutory research for this piece.