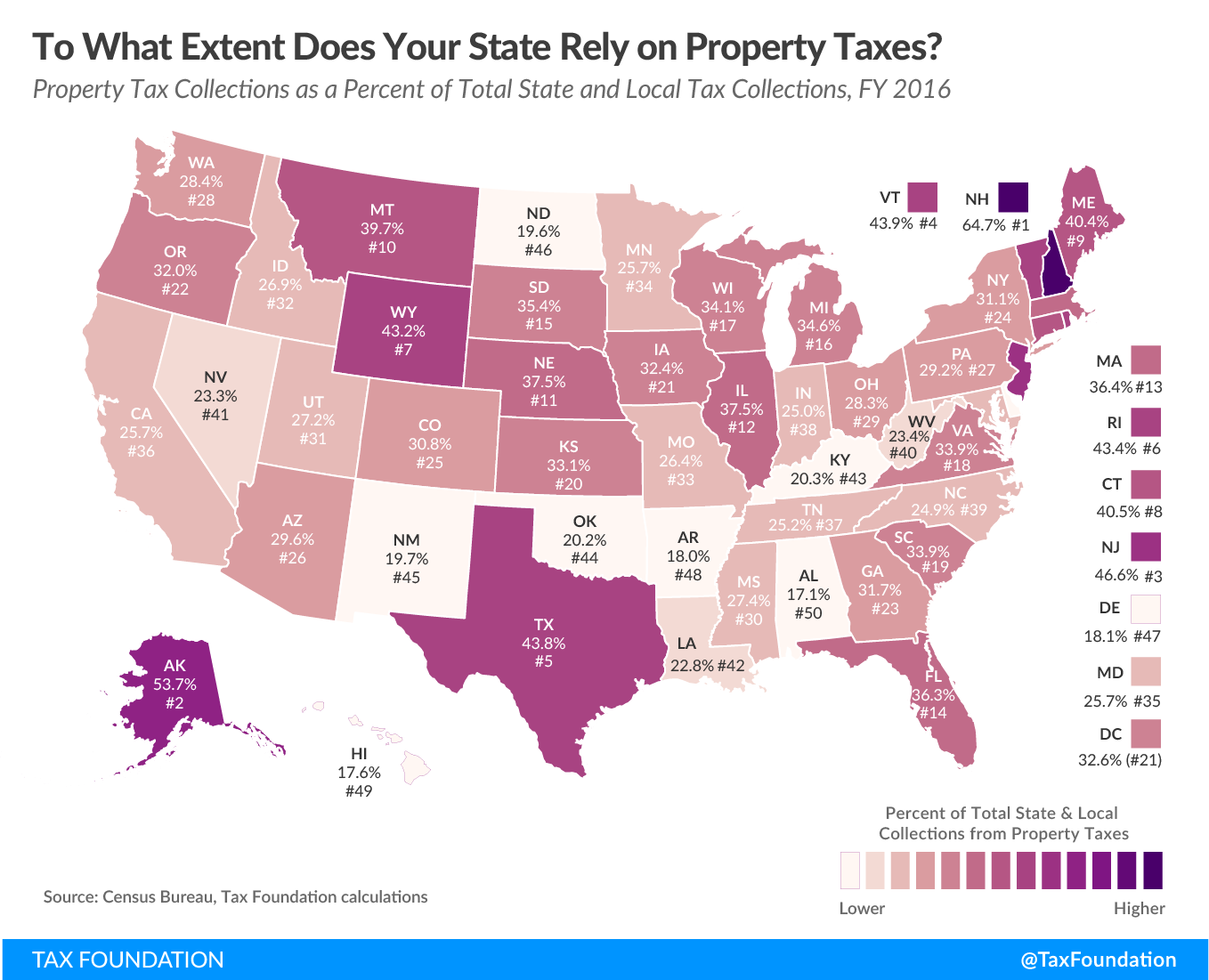

States and localities rely on property taxes as a major source of revenue. In fiscal year 2016, the last year where data is available, property taxes accounted for 31.5 percent of total U.S. state and local taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. collections, more than any other source of tax revenue. In the same year, 26 states and the District of Columbia raised the greatest share of their tax revenue from property taxes (see Table 8 in our Facts & Figures).

A variety of local political subdivisions—counties, cities, school boards, fire departments, and utility commissions, to name a few—have the authority to set property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. rates. While most tax jurisdictions levy property taxes based on the fair market value of a property, some base it on income potential (in the case of commercial properties) or other factors. In addition, some states place limits on how much property tax rates may increase per year or impose rate adjustments to achieve uniformity throughout the state.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeOf the 50 states, New Hampshire and Alaska relied most heavily on property taxes, which respectively accounted for 64.7 percent and 53.7 percent of their tax collections in FY 2016. Alabama and Hawaii landed at the other end of the spectrum, raising the smallest portion of their state and local tax revenue through property taxes: 17.1 percent and 17.6 percent, respectively.

It is important to note that a heavy reliance on property taxes does not necessarily indicate a high overall tax burden in any given state. For example, while Alaska is among the states that rely most heavily on property taxes, it is also among the states with the lowest state and local tax collections per capita (see Facts & Figures Table 6).

At the same time, states and localities that generate less revenue through property taxes tend to depend more on general sales taxes, individual and corporate income taxes, excise taxes, and others. For example, North Dakota derives much of its tax revenue from severance taxes while generating relatively little revenue from property taxes.

Note: This is part of a map series in which we examine the primary sources of state and local tax collections.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe