The recently passed One Big Beautiful Bill Act (OBBBA) makes permanent the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. cuts from the 2017 Tax Cuts and Jobs Act (TCJA) and makes several other changes to the tax code. While Congress worked on the OBBBA to cut taxes, however, President Trump has imposed significantly higher taxes by placing tariffs on more than 70 percent of US imports. Our analysis finds the current US-imposed and scheduled tariffs threaten to offset much of the economic benefits of the tax cuts, while falling short of paying for them.

As of July 2025, President Trump has imposed tariffs on nearly all US trade partners and additional product-specific tariffs, with few exceptions. The tariffs currently in effect include 20 percent on all imports from China and an additional 10 percent on certain imports from China, 25 percent on non-USMCA goods from Mexico and Canada (10 percent on non-USMCA Canadian energy and potash), 10 percent on most imports from nearly all other trading partners, 50 percent on steel and aluminum, and 25 percent on most autos and auto parts. Starting August 1, a 50 percent Section 232 copper tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. will go into effect, as will the reciprocal tariffs on more than 50 US trading partners.

If the tariffs in effect today are left in place permanently, they would reduce long-run GDP by 0.5 percent before retaliation, while raising about $2.1 trillion in revenue from 2025 through 2034 on a conventional basis. If the reciprocal tariffs and the Section 232 copper tariff take effect August 1 as scheduled, they would reduce GDP by an additional 0.3 percent while raising $401 billion in additional revenue (a relatively small increase as imports would fall substantially under those rates). In total, before accounting for retaliation, the tariffs imposed and threatened would reduce long-run GDP by 0.8 percent, raising about $1.7 trillion in revenue from 2025 through 2034 measured on a dynamic basis, accounting for slower economic growth.

The OBBBA would increase long-run GDP by 1.2 percent, while increasing the deficit on a conventional basis by $4.0 trillion (accounting for spending cuts but excluding interest costs) from 2025 to 2034. Accounting for the effects of economic growth would reduce the deficit impact (excluding interest costs) to $3 trillion over that period. Altogether, the tariffs would offset a little more than half the cost of the OBBBA on a dynamic basis and would reduce the long-run economic growth effects to 0.4 percent.

Table 1. Summary of Tariffs an the One Big Beautiful Bill Act

| One Big Beautiful Bill Act | Total US-Imposed and Scheduled Tariffs Before Retaliation | Tariffs in Effect July 2025, Before Retaliation | Scheduled Reciprocal and Copper Tariffs | |

|---|---|---|---|---|

| GDP | 1.2% | -0.8% | -0.5% | -0.3% |

| Capital Stock | 0.7% | -0.7% | -0.5% | -0.3% |

| Hours Worked in FTEs | 938,000 | -788,000 | -478,000 | -310,000 |

| Conventional Revenue, 2025-2034, Billions | -$3,973.0 | $2,466.4 | $2,065.8 | $400.6 |

| Dynamic Revenue, 2025-2034, Billions | -$3,036.1 | $1,691.9 | $1,679.5 | $12.6 |

Note: Totals may not sum exactly due to rounding.

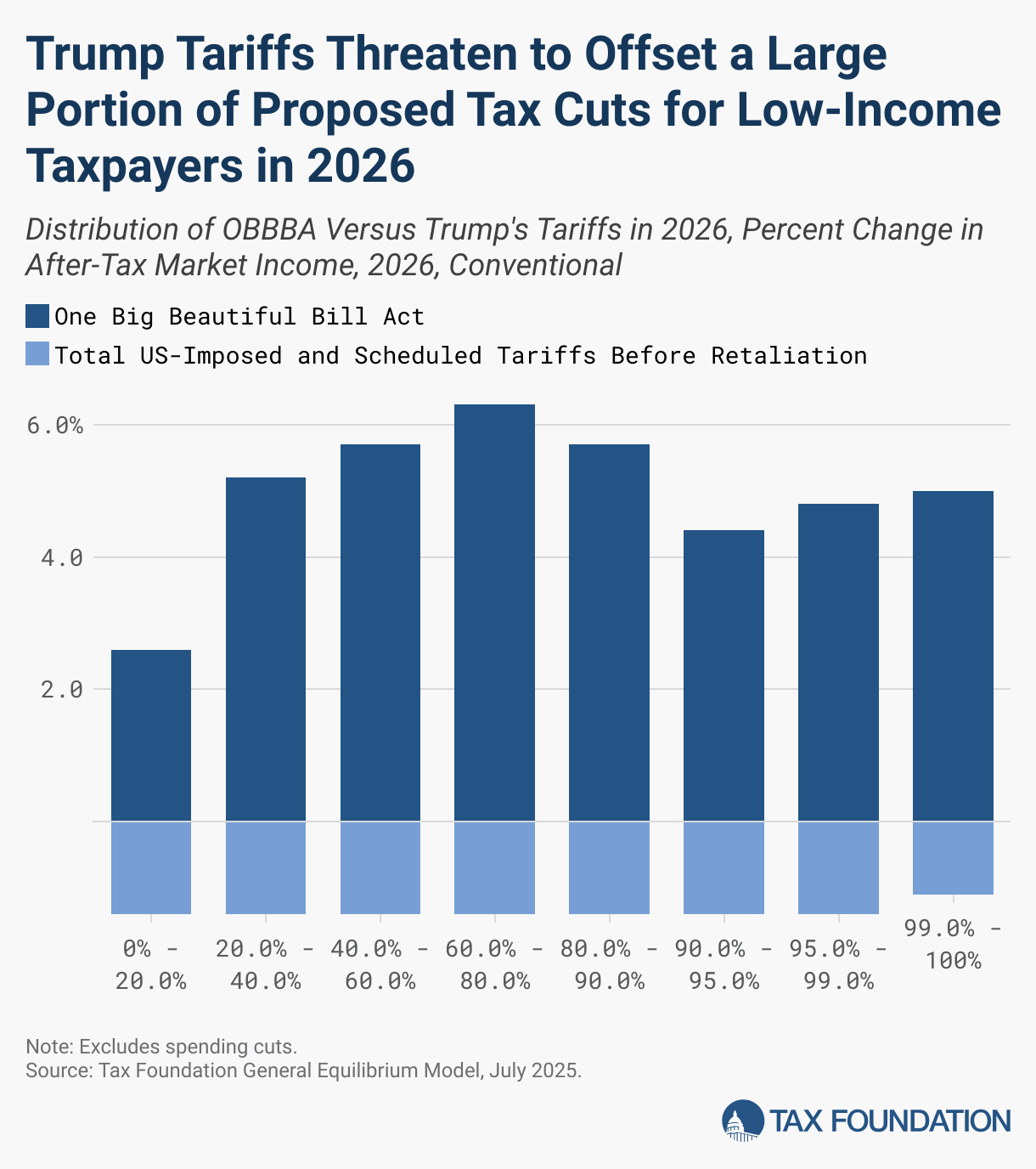

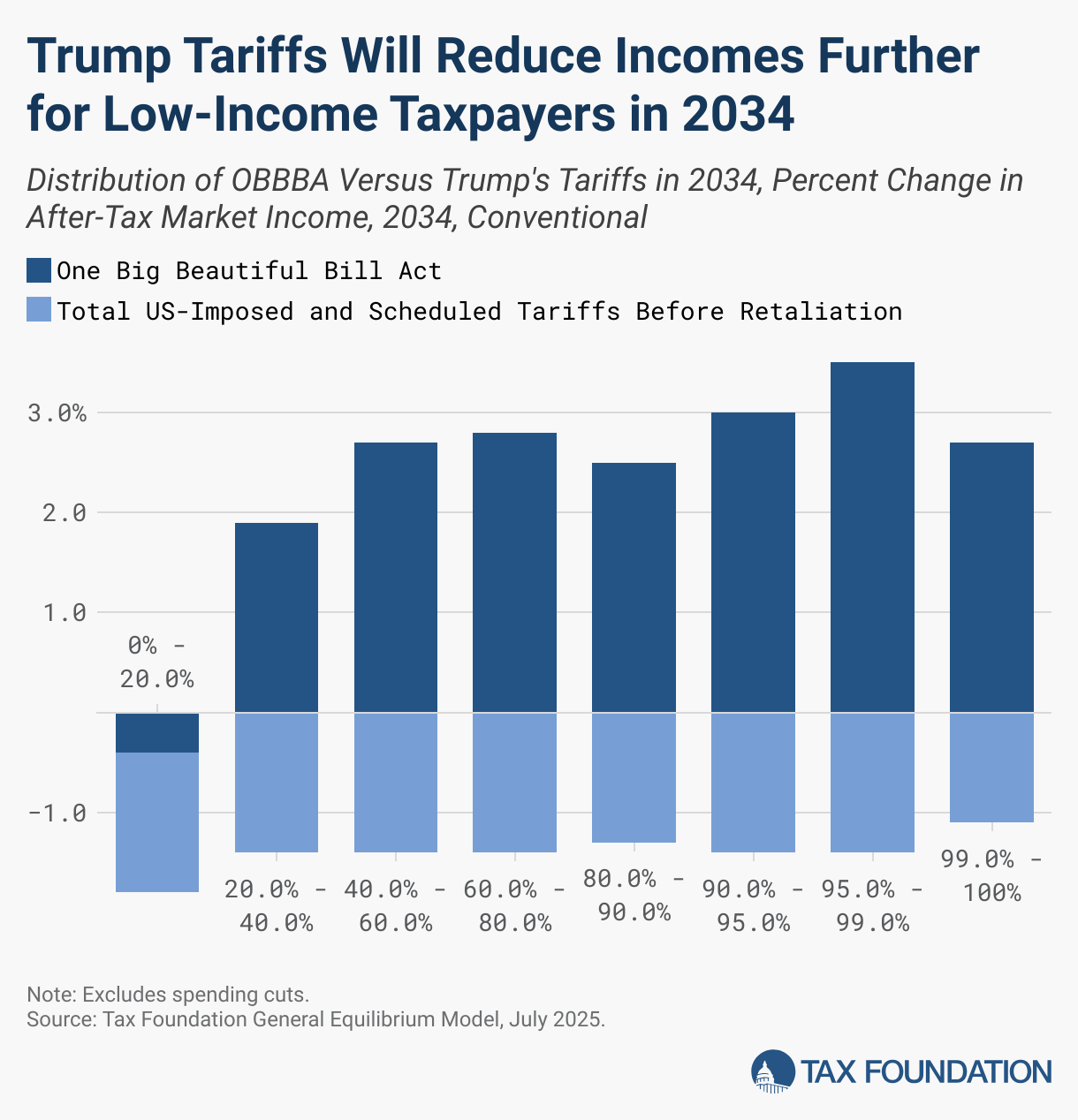

Because the combination of OBBBA’s tax provisions and Trump’s tariffs results in a major reduction in federal tax revenue, it also results in net tax cuts on average. But the effects are not the same across the income spectrum. The tariffs offset a larger portion of the tax cuts for lower- and middle-income taxpayers than for higher-income taxpayers, and by the end of the budget window, many low-income taxpayers would be worse off under the combination. Since there are several tax provisions in the OBBBA that are scheduled to expire at the end of 2028, by 2034, the bottom quintile will actually see a net reduction in after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. of 1.5 percent when accounting for the tariffs, measured on a conventional basis. Note also that these estimates do not include the distribution effects of the spending cuts, which would likely reduce after-tax income for this group even more.

Table 2. Percentage Change in After-Tax Market Income, 2026, Conventional

| Market Income Percentile | One Big Beautiful Bill Act | Total US-Imposed and Scheduled Tariffs, Before Retaliation |

|---|---|---|

| 0% - 20.0% | 2.6% | -1.4% |

| 20.0% - 40.0% | 5.2% | -1.4% |

| 40.0% - 60.0% | 5.7% | -1.4% |

| 60.0% - 80.0% | 6.3% | -1.4% |

| 80.0% - 100% | 5.0% | -1.4% |

| 80.0% - 90.0% | 5.7% | -1.4% |

| 90.0% - 95.0% | 4.4% | -1.4% |

| 95.0% - 99.0% | 4.8% | -1.4% |

| 99.0% - 100% | 5.0% | -1.1% |

| Total | 5.4% | -1.4% |

Source: Tax Foundation General Equilibrium Model, July 2025

Table 3. Percentage Change in After-Tax Market Income, 2034, Conventional

| Market Income Percentile | One Big Beautiful Bill Act | Total US-Imposed and Scheduled Tariffs, Before Retaliation |

|---|---|---|

| 0% - 20.0% | -0.4% | -1.4% |

| 20.0% - 40.0% | 1.9% | -1.4% |

| 40.0% - 60.0% | 2.7% | -1.4% |

| 60.0% - 80.0% | 2.8% | -1.4% |

| 80.0% - 100% | 2.9% | -1.3% |

| 80.0% - 90.0% | 2.5% | -1.4% |

| 90.0% - 95.0% | 3.0% | -1.4% |

| 95.0% - 99.0% | 3.5% | -1.4% |

| 99.0% - 100% | 2.7% | -1.1% |

| Total | 2.8% | -1.4% |

Source: Tax Foundation General Equilibrium Model, July 2025 Share this article