Key Findings

- Policymakers on both the left and right have brought industrial policy back into focus after slow growth over the past few decades and growing concern over the state of America’s manufacturing sector.

- In the context of the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code, industrial policy usually comes in the form of non-neutral subsidies for specific industries or sectors, or taxes on imports (i.e., tariffs) of particular goods to protect a specific domestic industry.

- The existing tax code is biased against capital-intensive manufacturers, as it prevents companies from deducting capital costs the same way they deduct labor costs.

- Fixing the bias against capital investment is preferable to pursuing industrial policy through the tax code, as subsidies tend to be ineffective and tariffs often weaken protected domestic industries and harm downstream industries.

Table of Contents

- Introduction

- — Background on Manufacturing: Has it Declined? Why is it Important?

- The Tax Code’s Existing Bias Against Manufacturing and Capital-Intensive Industries

- Tax Reform as (de)Industrial Policy: The History of the 1980s Tax Reforms

- — Traditional Manufacturing

- — Residential Construction

- — Energy

- The Misuse of Bonus Depreciation as Industrial Policy

- Contemporary Industrial Tax Policy

- Import Taxes as Industrial Policy

- — Steel Tariffs

- — Solar Panel Tariffs

- The Problem with “Made in America”

- Conclusion

Related Content

Introduction

The COVID-19 pandemic drove a major rethinking of economic policymaking, including a renewed focus on policies to bring back manufacturing operations from overseas.[1] Initially, onshoring discussions centered on goods immediately relevant to the crisis, such as personal protective equipment (PPE) or medical supplies. The discussions have since expanded to broader onshoring efforts, with many policymakers proposing ideas that fit under the umbrella of industrial policy.[2] Though evidence indicates entirely domestic supply chains can be as—or even more—vulnerable to disruption as global supply chains, the ensuing chaos of the pandemic made bringing supply chains onshore an attractive idea for some policymakers and analysts.[3]

The renewed interest in industrial policy, however, predates the pandemic and associated supply chain disruptions.[4] Economic growth has been slow since before the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. .[5] As a result, policymakers and scholars on both sides of the aisle have shown interest in rethinking a status quo (usually characterized, fairly or not, as laissez-faire) that is not delivering promised benefits.[6] Enter industrial policy.

Industrial policy can be difficult to define.[7] As policy analyst Caleb Watney wrote in 2020, some definitions of industrial policy are as broad as “an official strategic effort to encourage the development or growth of all or part of the economy, often focused on all or part of the manufacturing sector.” Accordingly, any policy enacted with the intent to increase economic growth could qualify as industrial policy.

A tighter definition of industrial policy is limited to efforts to target support to specific industries, in strictly commercial contexts. Scott Lincicome of the Cato Institute (an industrial policy critic) narrowed the term to four core aspects:[8]

- a focus on manufacturing, to the exclusion of services and agriculture;

- targeted and directed microeconomic (firm or industry‐specific) support (e.g., tariffs or subsidies), as opposed to horizontal, sector‐wide, or economy‐wide policies (e.g., corporate tax rate reductions or patents);

- a government plan to fix market failures, including negative externalities, and thereby achieve in targeted industries/companies clear, specific, and measurable commercial outcomes, such as jobs, investments (research and development, capital expenditures, etc.), output, or products that are better than what the market could provide in the absence of industrial policy; and

- a requirement that these market-beating commercial outcomes be generated within national borders.

For example, Oren Cass of the national conservative think tank American Compass (and an industrial policy advocate) argued for industrial policy with three bullet points:[9]

- First, that market economies do not automatically allocate resources well across sectors.

- Second, that policymakers have tools that can support vital sectors that might otherwise suffer from underinvestment—tools [called] “industrial policy.”

- Third, that while the policies produced by our political system will be far from ideal, efforts at sensible industrial policy can improve upon our status quo, which is itself far from ideal.

Cass lists a series of policies to support manufacturing, broadly defined to include all parts of the economy involved in the production of physical things—from traditional manufacturing to resource extraction, agriculture, energy production, and some construction, among others.[10] His policy solutions range from funding basic scientific research to research in specific areas of importance to local content requirements in major supply chains.

Most relevant to our paper is his proposal to “bias the tax code in favor of profits generated from the productive use of labor.” The idea has two core problems.

First, the U.S. tax code is not currently neutral towards productivity-enhancing investments; instead, the current tax code is biased against them. The existing bias against productivity-enhancing investments produces distortions for firms within and across sectors, ultimately harming the kinds of industries industrial policy proponents want to support. Policymakers do not need to create a bias for manufacturing as Cass suggests—they need to eliminate the bias against it.

Second, the track record of industry-specific tax policy in the U.S. is mixed at best. Discretionary tax policy at a domestic level in the U.S. has mostly been an ineffective substitute for fair general treatment of physical capital. Worse yet, policymakers in some cases have used discretionary policy to favor software and intangible-reliant industries over manufacturing. Meanwhile, protective tariffs designed to make certain domestic production stronger have instead weakened it by insulating our companies from competition and driven job losses in related industries.

Background on Manufacturing: Has it Declined? Why is it Important?

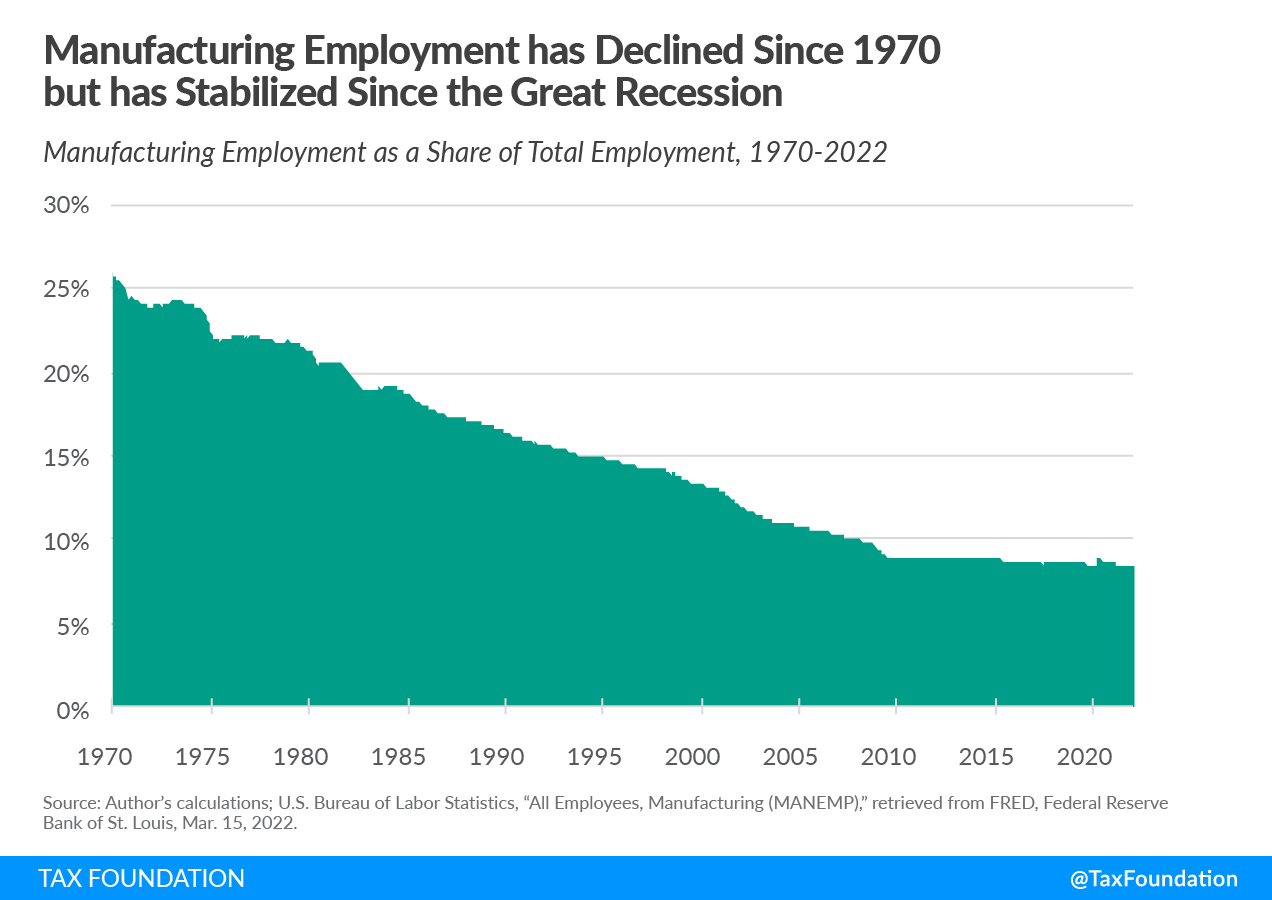

Developed economies across the world have seen both manufacturing employment as a share of total employment and manufacturing output as a share of total output decline over recent decades.[11] A few factors contribute to the decline, the first being that production of durable goods has gotten much more efficient, and therefore durable goods have gotten much cheaper, relatively speaking. Relatedly, as productivity growth makes the production of goods less expensive, labor-intensive services that are harder to automate grow, both as a share of labor and eventually of output.[12] Conversely, manufacturing’s employment share and output share decline.

The explanation for the broader trend of manufacturing’s employment since the 1970s also helps account for a recent bounce-back in manufacturing employment since 2010. Manufacturing employment as a share of total U.S. employment has been near flat since the end of the Great Recession, after declining steadily since 1970.[13]

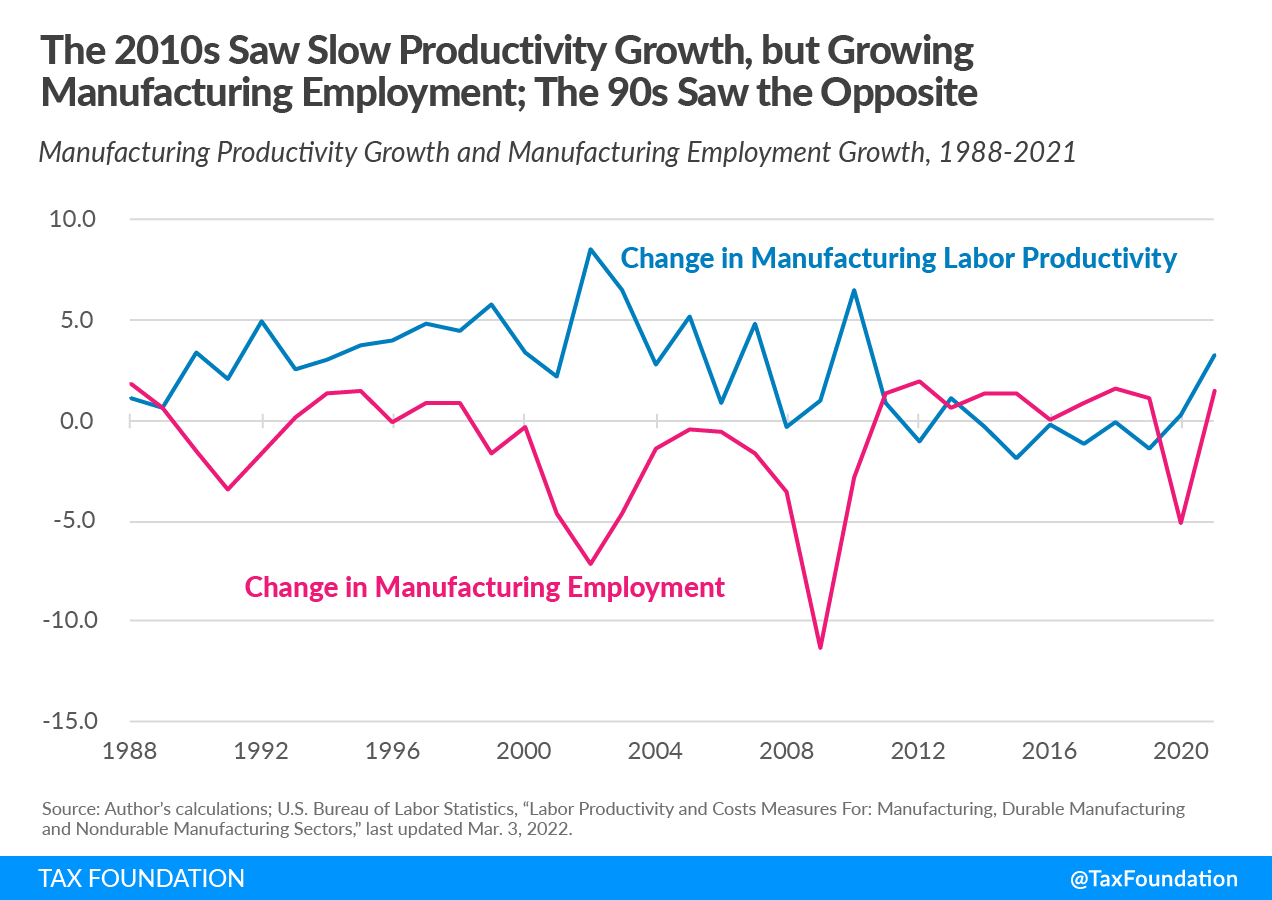

Meanwhile, the opposite is true of labor productivity. Through the 1990s and early 2000s, labor productivity in manufacturing was strong, even as employment (measured both in absolute terms and as a share of the total labor force) declined. Then, in the past decade, when employment has stabilized (and even grown in absolute terms), productivity in the industry has been stagnant or even negative.[14]

Increased trade and global competition is the other oft-cited reason behind manufacturing’s decline.

Some studies argue (contrary to the above theory) the productivity growth in manufacturing did lead to higher manufacturing employment, but faster growth and lower costs in foreign producers swamped the positive effects, leading to lower manufacturing employment on net.[15] The “China Shock,” which accelerated when the People’s Republic of China entered the World Trade Organization in 2001, is a salient example of exposure to cheap imports, with estimates that increased competition from cheap Chinese imports alone is responsible for 25 percent of the decline in U.S. manufacturing employment from 1990 to 2007.[16] Some critics of the theory, however, have noted Chinese imports were often concentrated in industries already declining domestically, making it difficult to isolate trade’s impact.[17]

Regardless of the exact breakdown of how much of manufacturing’s decline was driven by trade and how much was driven by technological change and automation, manufacturing declining as a share of GDP and of employment is a trend shared across the developed world across the past 50 years.[18] Given the change, it’s unreasonable to target, say, 1970 levels of manufacturing employment as a policy goal.

At the same time, manufacturing is still important. Manufacturing tends to be more research-intensive than service industries, and research and development (R&D) drives long-run innovation and productivity growth.[19] Manufacturing also tends to be more capital-intensive, and capital per worker is another important piece of long-run productivity and wage growth.[20] And lastly, having cutting-edge technology manufactured in the United States provides additional advantages and spillover benefits.[21]

Even in a globalized economy, the U.S. still needs conventional industry too. Generally, diversified supply chains, featuring some domestic production as well as imports from several different sources, hold up best in case of disruption.[22] Additionally, goods that are high in physical volume relative to their cost are often economically impractical to import across the world.

Ensuring the tax system treats manufacturers fairly is necessary to allow the economy to evolve to the most efficient mix of producing goods and services. Unfortunately, the existing tax code has a structural bias against manufacturing and capital-intensive businesses broadly. By forcing companies to spread deductions for capital investments out over long periods of time, the code creates a tax bias in favor of services firms with high labor costs and low capital costs, and against firms with high capital costs and low labor costs.

Policymakers have adopted a series of targeted measures—from tariffs to industry- or product-specific tax breaks to government procurement—in response to specific crises or industry pressures to mitigate the tax bias. Their efforts have been a poor substitute for fixing the underlying structural problem. Ideally, policymakers should eliminate the tax bias against large-scale physical capital investment and eliminate narrow stopgap solutions.

The Tax Code’s Existing Bias Against Manufacturing and Capital-Intensive Industries

Rather than begin with subsidies, the first thing policymakers should consider when looking for ways to support domestic heavy industry is whether current law penalizes it, and if so, how to eliminate the penalties.

To understand how the tax system disadvantages investment in physical capital, one must understand depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. . Economically, depreciation is the way an asset declines in value over time as it wears out or becomes obsolete—but in the tax system, depreciation describes how a taxpayer can deduct investment costs over time. While most business costs, such as utility bills or wages and salaries, are immediately deducted when they are incurred, business costs associated with physical capital are not immediately deducted. Instead, businesses must follow recovery periods set by lawmakers, indicating how many years over which deductions must be spread.[23]

Just as justice delayed is justice denied, a deduction delayed is a deduction denied, or at least, devalued. We can see why because a dollar of deductions 10 years from now is not as valuable as a dollar of deductions today. Over time, inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. and the time value of money reduce the real value of deferred deductions. When inflation is zero, the real time value of money (a normal real return on capital of about 3 percent) is the only source of erosion. When inflation is present, the erosion is more severe. The recent increase in inflation makes the bias worse, and the need to resolve it even more urgent.[24]

The ideal tax treatment of physical capital costs is full expensing, when they are deducted the year the investments are made. Immediately deducting costs ensures the value of the deductions are not eroded. The longer deductions are spread (and the higher the inflation rate), the worse for industry. The following is a calculation of the present value of deductions with different asset lives and different levels of inflation.

| 5-Year Asset | 10-Year Asset | 15-Year Asset | 20-Year Asset | 39-Year Asset | |

|---|---|---|---|---|---|

| Full Expensing | $100.00 | $100.00 | $100.00 | $100.00 | $100.00 |

| MACRS with 1.5 percent inflation | $89.68 | $80.75 | $73.00 | $66.26 | $47.50 |

| MACRS with 2 percent inflation | $88.63 | $78.94 | $70.66 | $63.56 | $44.38 |

| MACRS with 2.6 percent inflation | $87.40 | $76.86 | $68.01 | $60.55 | $41.05 |

| MACRS with 5 percent inflation | $82.78 | $69.37 | $58.85 | $50.53 | $31.20 |

| MACRS with 7 percent inflation | $79.26 | $64.00 | $52.66 | $44.11 | $25.80 |

| Note: Assumes straight-line depreciation and a real discount rate of 3 percent. | |||||

| Sources: Author’s calculations, Alex Muresianu and Jason Harrison, “How the Tax Code Handles Inflation (and How it Doesn’t),” Tax Foundation, Jun. 28, 2021, https://taxfoundation.org/taxes-inflation/. | |||||

Recovery periods vary significantly across asset classes. Structures, or buildings, must be spread out over the longest amount of time: residential structures over 27.5 years, and commercial structures over 39 years. Companies must also spread their deductions for long-lived structures in equal increments, but for short-lived assets, such as various types of equipment, they can deduct a larger part of the costs in earlier years.

Profit is correctly defined as revenue minus the cost of earning the revenue. If some costs are not fully allowed as deductions, as is the case with purchases of physical capital, profit is overstated. Even though the business will eventually take the deductions in the future in nominal terms, denying a full deduction for investment upfront increases the overall cost of making investments because inflation and the time value of money reduce the real value of deductions.[25]

Thus, businesses do not ever get to fully recover the real amounts they spend on investments before being subject to tax. The effect is a higher cost of acquiring physical capital.

Any policy stopping short of full, immediate expensing for capital investment places heavy industry at a disadvantage. Tangible, physical assets like machinery and structures make up a larger share of the expenses of a steel producer than of a professional services firm, which is likely more reliant on labor. Labor costs are fully deductible, but capital costs are not, so less capital-intensive firms can immediately deduct a larger share of their costs, meaning manufacturers and other industries more reliant on physical capital are at a relative disadvantage.

In recent years, Congress has offset some of the bias against manufacturing by authorizing the option to immediately expense short-lived assets (such as equipment) on a temporary basis through bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. . The Tax Cuts and Jobs Act of 2017 provided 100 percent bonus depreciation through 2022, but scheduled it to phase out by the end of 2026.[26] Failure to make 100 percent bonus depreciation permanent, especially as inflation is on the rise, would be a serious blow to domestic capital formation and production.

Tax Reform as (de)Industrial Policy: The History of the 1980s Tax Reforms

Tax changes made in the 1980s show it is a mistake to entrust policymakers to allocate capital across sectors.

The Economic Recovery Tax Act of 1981 introduced the Accelerated Cost RecoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages. System, or ACRS.[27] ACRS reduced the tax bias against capital-intensive firms by reducing the number of years over which they had to spread deductions and allowing larger deductions in earlier years.

The Economic Recovery Tax Act of 1981 also changed the Investment Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. (ITC). Previously, companies could claim a 7 percent credit on all physical capital investment. The 1981 Act made some long-lived capital assets ineligible for the credit, while raising the credit percentage for eligible assets to 10 percent. The ITC was effectively a subsidy, but ACRS stopped short of fully neutral tax treatment of capital investment as it still required depreciation deductions be taken over time. As a result, the combination of ACRS and the ITC loosely approached neutral tax treatment of investment—although a few assets fared even better as they faced negative effective marginal tax rates due to the ITC.[28]

Just a few years later, however, the Tax Reform Act of 1986 (TRA86) upended many of the new policies. TRA86 reduced the corporate tax rate from 46 percent to 34 percent, while lengthening cost recovery schedules, limiting accelerated depreciation, and eliminating the investment tax credit.[29] The changes disadvantaged firms more reliant on physical capital, like manufacturers, relative to firms reliant on intangibles.[30]

The choice of a lower rate and longer cost recovery schedules was the cardinal sin of the Tax Reform Act of 1986: on a dollar-for-dollar basis, better cost recovery for investment is a more effective way to boost growth than a lower corporate tax rate, as the former is only a tax cut for new investment, while reducing the corporate tax rate is a tax cut on both new and old investment.[31] As a result, the corporate tax changes in the Tax Reform Act of 1986 had a negative impact on economic growth, but the negative effect was partially offset by pro-growth changes to individual taxes.[32]

Two factors contributed to the decisions made in TRA86. The first was political: as documented in Showdown at Gucci Gulch: Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform, journalists Jeffrey Birnbaum and Alan Murray note how capital-intensive manufacturers pushed Congress to keep the accelerated depreciation provisions, while capital-light companies, such as retailers, preferred a lower corporate tax rate.[33]

On another level, an aspect of industrial (or deindustrial) planning was at play. As the information technology boom was beginning, policymakers saw traditional manufacturing as an industry of the past. So they thought taking away provisions benefiting old industries would help reallocate capital from the perceived dinosaurs and towards the more sophisticated industries of the future, such as software.[34]

Ironically, though the previous 1981 Economic Recovery Tax Act moved the tax code closer to neutral treatment of manufacturing, opponents of ACRS enacted in 1981 described it as “industrial policy,” based on it benefiting manufacturers more than other industries.

For example, in 1984, during the Reagan administration, Treasury Department Secretary Donald Regan told a group of reporters, “We have to decide whether we want our corporate tax policy to be an industrial policy. Accelerated depreciation and the investment tax credit have definitely favored manufacturing over services.”[35] Other internal administration officials, such as Ronald Pearlman, a lawyer who served as Assistant Secretary for Tax Policy, and his deputy, Charles McLure, argued the deductions for manufacturing broke from a neutral tax system.

Their position makes little sense, except in the narrow cases where the combination of the ITC and ACRS produced a negative effective marginal tax rate for certain assets. If allowing companies to deduct capital investments is industrial policy for capital-intensive firms, then allowing companies to deduct labor costs—a feature of the tax code almost no one disputes—is industrial policy for labor-intensive firms. Worsening tax treatment for investment broadly puts capital-intensive firms at a disadvantage, but TRA86 also made the tax treatment for machinery used by manufacturing firms worse relative to machinery used by services firms.

| Asset Type | Asset Life under 1985 Law | Asset Life Post-1986 |

|---|---|---|

| General Industrial Machinery | 5 | 7 |

| Special Industrial Machinery | 5 | 7 |

| Office and Computer Machinery | 5 | 5 |

| Service Industry Machinery | 5 | 5 |

| Source: Adapted from Dale Jorgenson and Kun-Young Yun, “Tax Reform and U.S. Economic Growth,” Journal of Political Economy 98:5 (1990), https://dash.harvard.edu/bitstream/handle/1/3403059/jorgenson_taxreform.pdf?sequence=2. | ||

Volumes have been written about the decline in manufacturing, and the relative rise of more service-oriented industries over the past almost 50 years. The decline in manufacturing as a share of national economies is a trend roughly shared across the developed world, and tax policy is only one slice of the debate.[36] But the Tax Reform Act of 1986 ended up favoring firms more reliant on intangible, rather than physical, capital, and at least somewhat shifted capital away from more physical capital-intensive areas.[37]

Some policymakers now worry the shift away from manufacturing, caused in part by past policymakers’ attempts to reallocate capital across sectors by changing tax policy, has been harmful. Such past decisions should make us wary that today’s politicians know any better how to allocate capital across sectors.

Traditional Manufacturing

Lengthy cost recovery schedules are particularly harmful for conventional manufacturing. TRA86’s elimination of the Investment Tax Credit and modifications to cost recovery schedules reduced investment in equipment relative to existing trends.[38]

The United Kingdom-based Adam Smith Institute notes stopping short of full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for physical capital investment amounts to a “factory tax.”[39] The United Kingdom’s experience of deindustrialization reflects the consequences of such a factory tax, as the country enacted similar reforms to the U.S.’s Tax Reform Act of 1986 during the 1980s, getting a lower corporate tax rate in exchange for unfavorable tax treatment of physical capital investment.[40] The United Kingdom has among the least-generous deductions for physical capital investment in the OECD, and has simultaneously seen higher rates of deindustrialization and low worker productivity growth relative to the rest of the OECD.[41]

Meanwhile, strong evidence shows bonus depreciation (allowing companies to deduct a larger portion of investment when it is made, sometimes up to 100 percent) encourages investment and growth. In particular, when the U.S. introduced 30 percent bonus depreciation in 2001, investment in eligible assets grew by 10.4 percent relative to investment ineligible ones, and when it was reintroduced in 2008 at 50 percent, investment increased by 16.9 percent in eligible assets relative to ineligible ones.[42] Fixed capital investment is responsive to tax policy changes.[43]

| Act | Depreciation Percentage* | Effective Dates |

|---|---|---|

| Job Creation and Worker Assistance Act of 2002 | 30% | Sept 12, 2001 – Dec 31, 2004 |

| Jobs and Growth Tax Relief Reconciliation Act | 50% | May 5, 2003 – Jan 1, 2006 |

| Economic Stimulus Act of 2008 | 50% | 2008 |

| American Recovery and Reinvestment Act of 2009 | 50% | 2009 |

| Small Business Jobs Act of 2010 | 50% | 2010 |

| Tax Relief, Unemployment Compensation Reauthorization, and Job Creation Act of 2010 | 100% | Sept 9, 2010 – Dec 31, 2011 |

| Tax Relief, Unemployment Compensation Reauthorization, and Job Creation Act of 2010 | 50% | 2012 |

| American Taxpayer Relief Act of 2012 | 50% | 2013 |

| Tax Increase Prevention Act of 2014 | 50% | 2014 |

| Protecting Americans from Tax Hikes Act of 2015 | 50% | 2015 – 2017 |

| Protecting Americans from Tax Hikes Act of 2015 | 40% | 2018 |

| Protecting Americans from Tax Hikes Act of 2015 | 30% | 2019 |

| Tax Cuts and Jobs Act | 100% | 2018 – 2022 |

| Tax Cuts and Jobs Act | 80% | 2023 |

| Tax Cuts and Jobs Act | 60% | 2024 |

| Tax Cuts and Jobs Act | 40% | 2025 |

| Tax Cuts and Jobs Act | 20% | 2026 |

| *This percentage reflects the share of the eligible investment that companies are able to deduct in the first year. | ||

| Source: Congressional Research Service, “The Section 179 and Section 168(k) Expensing Allowances: Current Law and Economic Effects,” May 1, 2018, https://crsreports.congress.gov/product/pdf/RL/RL31852. | ||

Growth in the capital stock means growth in long-run productivity and worker wages too. History demonstrates improvements to cost recovery have helped manufacturing investment and employees. The state-level adoption of bonus depreciation and expansion of Section 179 expensing (passed at a federal level in 2001) raised employee compensation and investment in manufacturing.[44] Additionally, evidence from variation in the tax treatment of investment from both 1979 to 1988 and 2001 to 2011 shows reduced costs for capital goods drives increases in wages for employees.[45]

Residential Construction

Housing, like manufacturing, has experienced non-neutral tax policy. The effects of the Tax Reform Act of 1986 on housing showcase the downsides of focusing tax policy on a very specific policy objective at the expense of more neutral treatment of investment more broadly.[46]

As it relates to housing, TRA86 made companies deduct the cost of investment in residential structures over 27.5 years instead of 19 years and prevented companies from taking larger deductions in earlier years.

Multifamily housing construction, generally built as investment projects, predictably collapsed: from 1986 to 1990, multifamily housing starts dropped 71 percent.[47] At the time, policymakers anticipated worsening the tax treatment of apartment construction would hurt investment in housing. Their answer was to create the Low-Income Housing Tax Credit (LIHTC), which provides a tax break to developers for constructing affordable housing.[48] Unfortunately, the LIHTC has been plagued with inefficiency and cost bloat. The allocation of LIHTC credits involves countless federal and state bureaucracies, and research shows the construction costs of LIHTC projects are almost 20 percent higher than equivalent private sector projects.[49]

Overall, the targeted tax subsidy provided through the LIHTC was not enough to offset broadly worse tax treatment—the following collapse reduced the supply of housing and contributed to rising rents in the long term.[50] The share of the U.S. population living in multifamily housing collapsed after 1986, pushing the U.S. towards the path of sprawl development.[51]

Energy

The energy sector—specifically clean energy—has perhaps been the biggest area in which the tax code has served as industrial policy.[52]

Tax credits have been a staple of the U.S.’s approach to incentivizing clean energy development since the Energy Tax Act of 1978, which established the Section 48 investment tax credit.[53] Under current law, a laundry list of provisions supports energy investments, including for renewable energy production, energy conservation and efficiency, lower-emission vehicles and vehicle fuels, as well as carbon capture.[54]

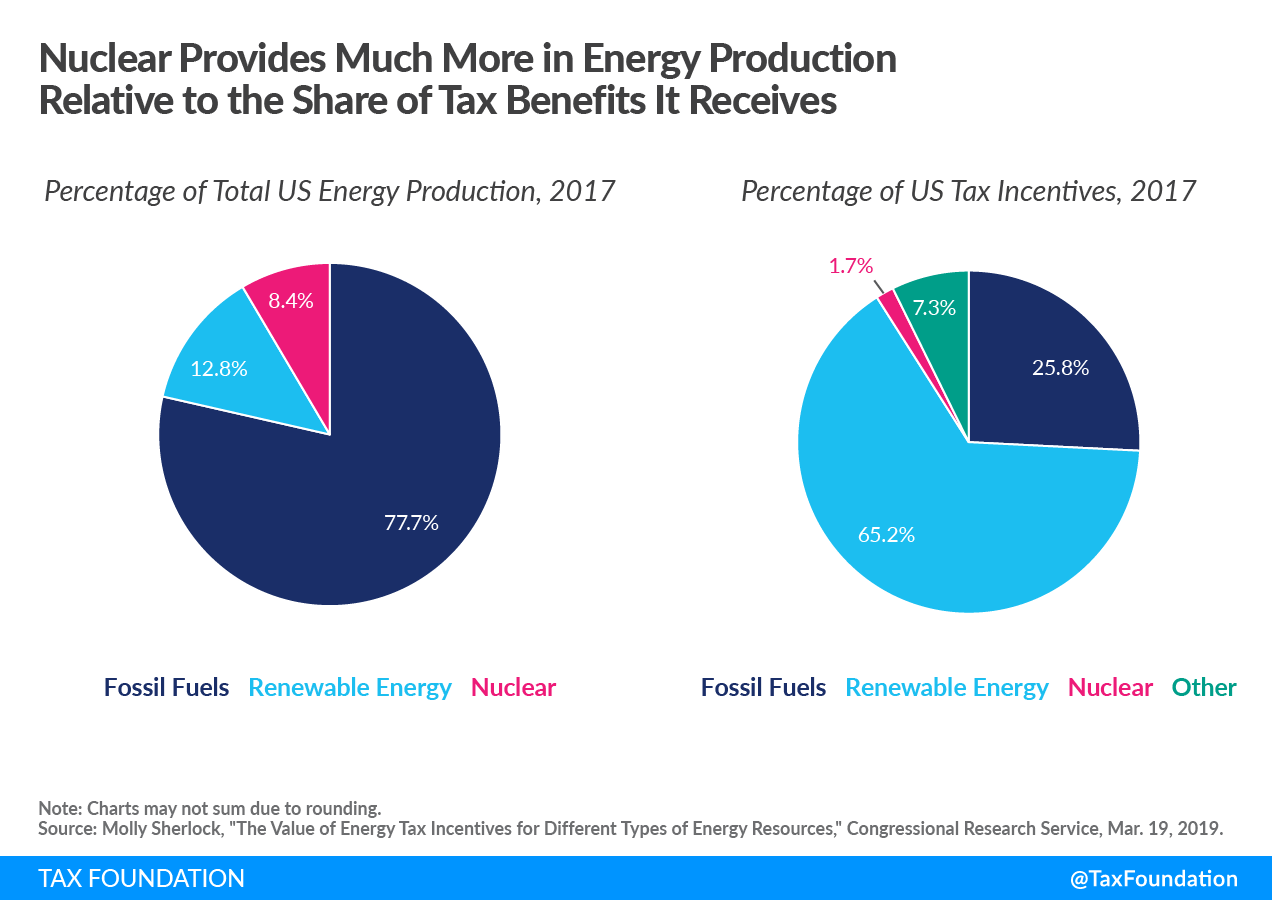

The system of targeted tax credits has numerous flaws. The mishmash of credits provide different levels of support for different power sources, but the differing levels of support are not dependent on the relative benefits provided by the different power sources[55] For instance, solar and wind energy receive disproportionate support relative to nuclear energy, even though nuclear energy produces minimal carbon emissions.[56] Lawmakers’ chosen method of incentivizing low-carbon technologies creates the problem of non-neutral subsidies: it is very difficult to equally subsidize different technologies.[57]

The policies have also had mixed results in generating investment. For example, credits for residential energy conservation spending have increased investment in such projects.[58] But generally, the set of tax policies intended to reduce carbon emissions has proven ineffective, or at the very least inefficient. The cost of carbon emissions to society is often estimated to be roughly $50 per ton.[59] But the tax credit for ethanol in motor fuel, as one example, effectively spent $1,000 to reduce carbon emissions by one ton, magnitudes more than the societal cost of one ton of emissions.[60]

In the automobile space, policymakers have used the gas guzzler tax (applied to vehicles that do not meet fuel efficiency standards) and tax credits for hybrid and electric vehicles to advance environmental technology. Both policies are poorly designed: the gas guzzler tax only applies to passenger cars, and excludes light trucks and SUVs.[61] This dynamic, coupled with the underlying fuel efficiency standards placing much stricter rules on passenger cars than light trucks, helped shift consumers away from passenger cars and towards “crossovers” and other light trucks, which have higher carbon emissions.[62]

One reason carbon emissions decline is capital turnover: the replacement of old, dirty technology with new, less carbon-intensive technology. Turnover matters for general types of capital, such as steel furnaces or automobile plants, and specific investments in energy efficiency improvements.[63] As Marilyn Brown and Sharon Chandler argued in the Stanford Law and Policy Review, investments in energy efficiency improvements involve an upfront capital cost for a business, in exchange for lower energy costs in the future. But this investment is disadvantaged under a system where annual energy costs can be deducted when they are incurred, yet capital costs cannot be immediately deducted.[64]

Similarly, faster capital turnover matters in the power generation sector.[65] Policy that, on the margin, makes companies more likely to invest and replace old capital with new capital would accelerate the transition to growing renewable energy sources. A system that stops short of full expensing is biased towards less capital-intensive operations and against new capital. At an economy-wide level, producers are, on the margin, less incentivized to replace a plant using an older energy source like coal with an up-and-coming source such as solar or wind generation.

The Misuse of Bonus Depreciation as Industrial Policy

Unfortunately, one of the reasons the disparity in tax treatment between labor and physical capital has continued is because policymakers see variations in depreciation schedules as a way to reallocate capital across sectors or industries. For example, policymakers have provided shortened depreciation schedules to specific kinds of energy investment.

In the past two years, several bills have been introduced to provide full expensing for narrow categories of assets, attempts to address some industry-specific problems. Last year, the production of medical supplies and personal protective equipment (PPE) was a particularly salient issue. Rep. Chip Roy (R-TX) introduced the BEAT China Act, which would allow firms to deduct the costs of investment in new medical manufacturing facilities.[66]

Such a narrow, short-term view of cost recovery ignores how physical capital investment actually takes place. Companies make major physical capital investments over the long term, so fiddling with investment incentives to respond to an immediate problem is not particularly effective.

Further, the cost of selectively using accelerated depreciation as an industrial policy is disadvantageous to other capital-intensive industries—industries that may suddenly become crucial. For example, in 2019, few policymakers thought of our ability to manufacture ventilators domestically as a particularly pressing issue. We do not know which industries could suddenly become important, which is why it is best to treat every industry evenly, rather than leave a bias against manufacturing in the tax code and selectively and belatedly reduce it when an industry-specific emergency arises.

It is better to have built-up capacity in the long term with fair treatment of physical investment than to have a delayed reaction to a crisis caused by said lack of capacity. Now, the importance of semiconductors as a component in so much of the economy might justify some kind of policy action, but targeted tax subsidies are not ideal.[67]

Lastly, one other domestic tax policy enacted with the goal of boosting domestic manufacturing was the domestic production activities deduction, or DPAD. Passed in the Jobs Creation Act of 2004, Section 199 initially allowed companies to deduct 3 percent of their income derived from domestic manufacturing, which was later raised to 6 and then 9 percent by 2010. The provision was then repealed in the Tax Cuts and Jobs Act of 2017. Evidence indicates the DPAD increased investment.[68] But it was an awkward policy, providing a tax cut for both existing manufacturing activities and new manufacturing activities, as well as creating classification issues surrounding which income counts as domestic manufacturing income. Full expensing for capital investment would instead provide a tax cut for new projects alone, and create fewer classification distortions.

Contemporary Industrial Tax Policy

Tax policy towards semiconductors provides another illustration of policymakers having to fight the last battle to compensate for generally disadvantageous treatment of capital investment. Shortages of semiconductors led to production stoppages in numerous industries in 2021, especially in the auto manufacturing industry. The stoppages pushed prices of autos higher (along with inflation driven by expansionary fiscal and monetary policy).[69]

Bills in the House and Senate are focused on competing with China, particularly as it related to the semiconductor industry. The bipartisan, Senate-passed U.S. Innovation and Competition Act (USICA, and originally the Endless Frontier Act)[70] would authorize $200 billion of government spending on R&D and an additional $52 billion of spending specifically for semiconductors.[71] The House America Creating Opportunities for Manufacturing, Pre-Eminence in Technology, and Economic Strength (America COMPETES) Act differs in some ways but features many of the same components, including the CHIPS Act, the package of subsidies and R&D spending for the semiconductor industry.[72] Lawmakers from both parties have also proposed the FABS Act, which would provide a 25 percent investment tax credit for investment in semiconductor manufacturing.

In his State of the Union Address, President Biden urged lawmakers to come to an agreement on USICA in order to compete for the jobs of the future and “level the playing field with China and other competitors.”

Such policies would be less necessary if the tax code had treated investment neutrally in the first place—particularly because semiconductor manufacturing is especially capital-intensive.[74]

While USICA and COMPETES would boost spending by government agencies for R&D, they notably lack tax changes to end the tax bias against private R&D investment, which must be amortized over five years rather than immediately deducted. Requiring R&D expenses to be amortized has made the U.S. less competitive. No other developed country forces companies to spread R&D deductions over multiple years—instead, companies usually receive immediate deductions as well as generous subsidies.[75] For example, China allows R&D expenses to be immediately deducted and provides additional “super deductions” to encourage R&D investment.[76]

Rather than offer wasteful, poorly-timed subsidies to an industry already making investments in the United States,[77] lawmakers could stimulate investment by ending the tax penalties against it. Permanently restoring immediate expensing of R&D investment would make the U.S. more competitive while avoiding the pitfalls that would come with narrowly-targeted subsidies.

Import Taxes as Industrial Policy

Taxes on imports, commonly known as tariffs, have also been used to protect favored industries. Such efforts have repeatedly failed to boost domestic manufacturing and have resulted in net harm due to negative effects on downstream industries. Clear evidence shows protectionist policies like tariffs produce far greater economic costs for consumers than benefits for workers or protected industries. Nonetheless, policymakers continue to impose new iterations of tariffs in attempts to protect favored industries.

Governments use tariffs to shield domestic industry from foreign competition. TariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. proponents argue tariffs provide time for domestic companies to regain their footing and competitiveness, but protection often backfires. Industries become stagnant without foreign companies competing with them for the domestic market. Further, tariffs on one good raise costs for other domestic manufacturers (as well as consumers), and trigger retaliatory tariffs from other countries that also hurt domestic production.

The U.S. experience with steel tariffs and solar panel tariffs illustrates how protectionist measures like tariffs backfire.

Steel Tariffs

Tariffs to protect metal producers date to the 1790s.[78] Though tariffs have often been credited with the phenomenal industrial growth of early America, most research indicates other factors, such as capital accumulation, technological improvements, rapid population growth, and natural resource endowments, better explain the industrial expansion.[79] More recently, in the 1970s and 1980s, steel protection made a comeback that continued with major increases in the early 2000s and in 2018.

Research by economists Stefanie Lenway, Randall Morck, and Bernard Yeung on the tariff and quota episodes in the 1980s indicates that steel protection boosted the lobbying efforts of less innovative firms and discouraged productive firms from engaging in research & development (R&D).[80] The authors note their results “raise the possibility that trade barriers reduce the value of innovation in the protected industry.” In other words, it is more likely that tariffs encourage rent-seeking behavior rather than innovation and competition:

Overall, our results are consistent with the following conclusions: Lobbying for trade protection is undertaken by less competitive firms whose workers and top managers have established comfortable positions. Protection is a form of rent-seeking. It confers private benefits upon lobbyers’ shareholders, senior workers, and top managers…appears to reduce returns to true innovation and encourage innovative firms to exit. These dynamic costs of protection…are potentially much more serious than the distortions shown in standard trade theory diagrams.”

In 2002, succumbing to political pressures, the George W. Bush administration placed tariffs ranging from 8 percent to 30 percent on imports of certain steel products in an attempt to protect the domestic U.S. steel industry from foreign dumping, to be in place for 36 months.[81] The tariffs were promptly removed after being in place for 20 months, due to a variety of factors including harms to downstream steel users and the threat of retaliatory tariffs from the European Union.[82]

While the tariffs afforded temporary reprieve from foreign competition for steel producers, they increased prices for steel users, including, but certainly not limited to, producers of fabricated metal, machinery, equipment, transportation equipment, and parts; chemical manufacturers; petroleum refiners and contractors; tire manufacturers; and nonresidential construction companies. For a sense of scale, recent estimates indicate the steel-producing industry in the United States employs 140,000 workers and is declining due to new technology and higher productivity, while steel-consuming industries employ 6.5 million workers and are poised to grow.[83]

As a result of higher steel prices from those Bush steel tariffs, researchers Joseph Francois and Laura M. Baughman estimate a loss of nearly 200,000 jobs in the steel-consuming sector, a loss larger than the total employment of 187,500 in the steel-producing sector at the time. The tariffs led to supply shortages and higher prices. U.S. steel market prices were generally higher than prices in global markets, giving foreign producers of steel-containing products a cost advantage over U.S. producers of steel-containing products. In response, end customers began shifting orders from U.S. manufacturers to foreign manufacturers.

Even though the tariffs were promptly removed, new research from Harvard economist Lydia Cox demonstrates how the temporary tariffs led to long-term damage. Cox found “even temporary tariffs can have cascading effects through production networks when placed on upstream products…upstream steel tariffs have highly persistent negative impacts on the competitiveness of U.S. downstream industry exports.”[84]

In other words, imposing tariffs disrupts established trade flows, but when tariffs are lifted, trade patterns do not automatically snap back in place: “declines in the competitiveness of U.S. exports due to the tariffs are highly persistent—global market share remains depressed relative to pre-tariff levels for at least 8 years after the tariffs are lifted. Likely a result of this loss in market share…steel-intensive industries suffered persistent declines in employment in response to relatively high steel tariff rates.”[85]

In March 2018, the Trump administration placed tariffs of 25 percent on imports of certain steel products (and 10 percent tariffs on imports of certain aluminum products), this time under the guise of protecting national security. Certain countries, including South Korea and Brazil, accepted annual quotas as an alternative.

The steel (and aluminum) tariffs were further expanded in 2020, when the Trump administration extended the import tax to derivative products—U.S. businesses had increased purchases of steel-containing products not subject to the original tariffs from foreign suppliers, and the Trump administration wanted to prevent such circumvention.[86] Unlike the George W. Bush administration steel tariffs, the Trump administration tariffs and quotas have no expiration date.

Gary Hufbauer and Euijin Jung of the Peterson Institute for International Economics estimated the Trump administration’s steel tariffs would expand steel employment by about 8,700 jobs, but at an average cost of about $650,000 per job.[87] Their analysis did not attempt to measure employment loss in downstream industries but they note “job losses probably exceed jobs created by a large magnitude.” Even without accounting for job losses elsewhere in the economy, their estimates indicate a high level of inefficiency and economic loss as the trade-off for small increases in steel production employment—the cost of saving a steel job amounts to about 11 times greater than the average wage earned by a steelworker.[88]

Scott Lincicome of the Cato Institute has illustrated how U.S. manufacturers face a competitive disadvantage due to the steel tariffs—the prices U.S. manufacturers pay for steel are significantly higher than what competitors in China, Europe, and elsewhere pay.[89] Additional research from economists at Harvard University and the University of California, Davis, indicates downstream job losses “created by putting these steel-using industries at risk appear to be substantial, and well in excess of any jobs that may have emerged in the steel-production industry as a result of the tariffs.”[90]

In total, the limited benefit of using protectionist policies to save very few steel-making jobs in the short run is unequivocally outweighed by the unintended consequences of higher prices, competitive disadvantages, and job losses across other U.S. industries, especially manufacturing companies that rely on steel as an input.

Solar Panel Tariffs

Anti-dumping and countervailing duties have also been used to shield the domestic solar panel manufacturing industry from foreign competition. The tariffs have failed to boost domestic manufacturing, reduced demand for and adoption of solar as an alternative source of energy, and cost downstream jobs in installation and sales.

Tariffs on solar panels date to 2012, when applied to imports from China, and 2015, when increased and expanded to imports from Taiwan to prevent circumvention of the original tariffs.[91],[92] At the time of the 2012 tariffs, Gary Clyde Hufbauer and Martin Vieiro of the Peterson Institute for International Economics warned, “…environmental policies designed to encourage renewable energy and limit the emission of greenhouse gasses are hurt when alternatives to fossil fuels are made more expensive. The solar cell case also underlies the lopsided…process, which gives no legal standing to downstream industries—in this case installers of solar cells—that will lose jobs when they have to pay penalty duties on imported components.”[93]

A 2018 Brookings policy report by Minji Jeong and Nathan Hultman sums up the outcome of the 2012 and 2015 tariffs:[94]

…the [2012 and 2015] tariffs imposed did not really save U.S. solar cell and module manufacturing from international market pressures. At this point, there are only 14 solar cell/module manufacturers in the U.S. A majority of solar cell and modules are now produced in Asia, with China as the leading (and most cost competitive) producer worldwide. The impact of American tariffs was insignificant partially because Chinese manufacturers could simply move their production to other Asian countries to avoid the tariffs. The tariffs on Taiwanese cells attempted to close this loophole, but the manufacturers still had many other options (such as Vietnam).

In 2018, President Trump approved tariffs on all solar panel imports to last for four years, saying, “We’re going to benefit our consumers, and we’re going to create a lot of jobs.”[95] The tariffs began at a 30 percent rate, declining by 5 percentage points per year until they expire, though the tariffs can be renewed for another four years at the discretion of the sitting president. Jeong and Hultman offered a prediction of the likely outcome:

The new Trump solar tariff closes this potential loophole by covering all imports. However, it will not likely lead to a dramatic boost to domestic cell and module manufacturing, for several reasons. …the competitiveness gap between the most well-positioned players—Chinese manufacturers—and U.S. manufacturers seems too significant to be closed via the new tariff. According to the International Renewable Energy Agency, the average solar module price in China was 0.43 cents per watt in 2016, while it was 0.61 cents per watt in California, which was one of the highest averages among major markets…

As with the steel tariffs, researchers caution that rather than boosting the innovative capacity of protected industries, protectionist policies like tariffs work against innovation. Center for Strategic and International Studies Director and Senior Fellow Sarah Ladislaw explains both steel and solar panel tariffs:[96]

It is not clear that either tariff remedy will do very much to make even the targeted portion of the industry more competitive over the long run. In both the steel and solar industry, long-term competitiveness is about innovation, the costs of capital, and labor. Tariffs may provide a near-term boost for manufacturers, but if they do not take the steps to address the long-term competitive pressures facing their industry, then the tariffs are simply temporary reprieves from the relentless pace of industrial progress in an increasingly digitalized and automated world.

In 2020, the U.S. solar industry employed 231,474 workers, and just 13 percent of the workers are in manufacturing, with the majority in installations and development, sales and distribution, or operations and maintenance.[97]

The Solar Energy Industries Association, a trade group representing producers, installers, and others in the industry, estimates the impact of the Trump administration tariffs resulted in 62,000 fewer industry jobs from 2017 through 2021, 10.5 gigawatts of lost solar deployment, and $19 billion of lost investment.[98] According to its report, while solar price declines continued in the rest of the world, price declines in the United States were undercut by the tariffs, leaving U.S. prices among the highest—43 percent to 57 percent higher than the global average.

Research by Wenjun Wang of the Agricultural Bank of China found imposing $1 of tariffs on solar panels increases the final price of an installed system by $1.34: “U.S. manufacturers gained little from the anti-dumping policies whereas U.S. installers were largely negatively affected, as well as Chinese manufacturers. Overall, our results suggest that the solar trade war led to large welfare losses in both countries and substantially slowed the adoption of solar PV” [cells].[99]

The various iterations of solar panel tariffs have failed to make domestic production competitive, reduced investment, caused steep job losses in downstream industries, and reduced demand for solar panels by artificially increasing the price of an installed system. They also work in opposition to energy tax credits that promote investments in and adoption of solar, undermining goals of clean energy adoption.

Unfortunately, the evidence against their effectiveness did not deter the Biden administration from extending the solar panel tariffs another four years in February 2022.[100] Though the administration doubled the quota level, the tariffs will continue to apply to marginal solar panel imports, leading to similar cost pressures and inefficiencies as past instances.

The Problem with “Made in America”

The U.S. imposes restrictions on government procurement to funnel business toward domestic producers, severely driving up the cost of public infrastructure. Since 1933, the Buy American Act (BAA) has forced the U.S. to give preference to domestic producers over foreign producers when purchasing supplies or materials for government projects and initiatives. Although the U.S. has opened its procurement to foreigners to some extent through free trade agreements and as a signatory to the World Trade Organization’s (WTO) Government Procurement Agreement, the agreements cover just 48 percent of all U.S. procurement.[101] As a result, most U.S. procurement is subject to Buy American provisions, which in effect act as a tax on foreign procurement, restricting competition and increasing costs.

When the U.S. government invests in a project, both domestic and foreign producers will bid for a contract to provide their construction materials and end products to the government, and the U.S. will accept the one that offers the “best value.” The BAA defines a domestic end product as a product in which “the cost of the components mined, produced, or manufactured in the United States exceeds 50 percent of the cost of all components.”[102] The U.S. must purchase the domestic end product unless the lowest domestic offer is deemed “unreasonable.”

To determine whether the domestic offer is “unreasonable,” the BAA requires that when the lowest offer is from a foreign business, the price of the contract must be increased by a certain percentage.74 Prior to 2021, the competing foreign offer may be increased by either 6 percent or 12 percent, depending on whether the lowest domestic offer is from a large or small business. If the contract is for Department of Defense procurement, it must be increased by 50 percent. In this sense, the BAA functions as a tax on foreign procurement. After applying the tax, the contract is then awarded to the domestic firm as long as the domestic offer is below the lowest foreign offer.

The Trump administration sought to strengthen the BAA through a series of executive orders (EO). The latest took effect in January 2021 and increased the required U.S. components for domestic end products consisting of iron or steel from 50 percent to 55 percent.[103] The EO also increased the penalties for foreign end products: Foreign offers from large businesses must be increased by 20 percent, whereas offers from small businesses must be increased by 30 percent. Upon entering office, President Biden issued an EO affirming the rule change and establishing a new “Made in America” office to review any proposed waivers to the BAA. In summer 2021, President Biden proposed increasing the domestic content requirements to 60 percent immediately, eventually increasing to 75 percent over an unspecified time period.[104]

Although the BAA was enacted to protect American industries and workers, the law has imposed real costs on American taxpayers and industry. Recent estimates find the BAA provisions are equivalent to a tariff of 25 percent on federal government purchases, which adds to the several other reasons why American infrastructure is so expensive.[105] This harm comes on top of the economic harms tariffs impose to begin with.[106] Even when jobs are “saved,” the costs to taxpayers are often much larger than the incomes earned at saved jobs. The Peterson Institute of International Economics estimated every job “saved” by the BAA cost American taxpayers roughly $250,000.[107]

A trio of Australian economists studied the impact of the BAA on the U.S. economy and found eliminating it would increase jobs by about 300,000 and raise GDP by 0.12 percent.[108] The BAA reduces employment because job increases in the protected industries are offset by job losses elsewhere in the economy. Suppliers to the government must alter the components of their end products to ensure they are BAA-compliant, increasing costs and complexity in the production process.

It’s worth noting that most domestic procurement requirements are not focused on critical national security issues, nor on ensuring some level of redundancy in supply chains. In his recent State of the Union address, President Biden touted providing subsidies for domestic production as a means to reduce inflation.[109] But insisting on domestic-manufactured material for, say, infrastructure projects, would make the inflation problem worse by raising costs and slowing the very investments in supply chain integrity needed now.

And while having some domestic production could improve resiliency, exclusively domestic supply chains are more vulnerable to shocks, as was found during the pandemic.[110] Such issues with domestic disruption was one of the reasons President Trump exempted many kinds of personal protective equipment from the China tariffs to address shortages.[111]

In some specific, security-related cases, simply fixing the tax code’s bias against physical capital investment, as we outline above, may not suffice. In such cases, it would be prudent for policymakers to consider expanding the Strategic National Stockpile (SNS) rather than protecting specific industries through tariffs, procurement restrictions, or other industry-specific tax policy.[112] The SNS, first established by the Department of Health and Human Services (HHS) in 1999, stockpiles medicinal goods in the event of a public health crisis. HHS is responsible for procurement while the distribution of supplies is typically managed by state and local governments. Prior to the COVID-19 pandemic, the SNS held an estimated $8 billion in medical assets, but HHS officials noted that they were ill-equipped to meet the surge in demand for supplies as the pandemic unfolded in March 2020.[113]

Depending on the context and the specific design of SNS procurement policy, however, it can end up emboldening protectionism. Some policymakers may give preference to certain domestic producers over foreign ones when procuring supplies, although for the purposes of addressing a supply shortage, it should not matter where the goods are produced. For example, one investigation found that nearly half of the stockpile’s annual budget for the past decade went to a single U.S. company that manufactured anthrax vaccines.[114] Policymakers should not discriminate against foreign producers when replenishing the stockpile, as doing so imposes additional costs on U.S. taxpayers and leads to inefficient spending.

Alternatively, rather than permanently altering the tax code to incentivize domestic production, the U.S. government could also offer purchase agreements to U.S. firms to boost needed production during a public emergency. In response to concerns about the swine flu in 2009, many manufacturers made large capital investments to ramp up production of personal protective equipment.[115] But once they finished, concerns about the swine flu had already waned, and the firms suffered significant losses from their investments. As a consequence, firms may actually underinvest in production of critical goods because they are uncertain about how long a crisis will last due to past experiences. A federal government purchase agreement, agreeing to buy certain quantities of a good for a specified time period, would reduce risk and help firms recover their fixed costs from making such large investments.

Conclusion

Over the past several decades, tax policy towards manufacturing has been defined by two things: the first, a broad penalty for capital-intensive industries, and second, a grab bag of special provisions designed to mitigate problems caused by the first. Tariffs have not helped American heavy industry, especially when tariffs to prop up one industry end up raising costs for an entire sector.

Policymakers actively marginalized the manufacturing sector by saddling them with cost recovery rules that prevent them from deducting the full cost of investment in physical plant and equipment. Going forward, policymakers should avoid haphazard fixes, targeted measures, and protectionism. Instead, moving to full expensing for all capital investment, in research and development, equipment, and structures, would finally put manufacturing back on an even footing with the service sector.

[1] Sabri Ben-Achour, “Reshoring Gets New Attention During COVID-19,” Marketplace.org, May 19, 2020, https://www.marketplace.org/2020/05/19/reshoring-gets-new-attention-during-covid-19/.

[2] American Compass, “Moving the Chains: 9 Strategies for Retaking Global Leadership and Innovation,” May 2020, https://americancompass.org/wp-content/uploads/2020/06/American-Compass-Moving-the-Chains-FINAL-with-Comments.pdf.

[3] Barthélémy Bonadio, Zhen Hou, Andrei A. Levchenko, and Nitya Pandalai-Nayar, “Global Supply Chains in the Pandemic,” National Bureau of Economic Research Working Paper No. 27224, May 2020, https://www.nber.org/papers/w27224.

[4] Alex Muresianu, “What the Conservative Civil War Means for Republican Policy,” Arc Digital, Feb. 20, 2020, https://medium.com/arc-digital/what-the-conservative-civil-war-means-for-republican-policy-a60c0e248d18.

[5] John Fernald and Huiyu Li, “Is Slow Still the New Normal for GDP Growth,” Federal Reserve Bank of San Francisco Economic Letter 2019-17, June 24, 2019, https://www.frbsf.org/economic-research/files/el2019-17.pdf.

[6] Julius Krein, “What Alexandria Ocasio-Cortez and Marco Rubio Agree On,” The New York Times, Aug. 20, 2019, https://www.nytimes.com/2019/08/20/opinion/america-industrial-policy.html.

[7] Caleb Watney, “Untangling Innovation Policy from Industrial Policy,” Agglomerations, Sept. 2, 2020, https://www.agglomerations.tech/untangling-innovation-from-industrial-policy/.

[8] Scott Lincicome and Huan Zhu, “Questioning Industrial Policy: Why Government Manufacturing Plans are Unnecessary and Ineffective,” Cato Institute, Sept. 28, 2021, https://www.cato.org/white-paper/questioning-industrial-policy.

[9] Oren Cass, “America Should Adopt an Industrial Policy,” Law & Liberty, July 23, 2019, https://www.manhattan-institute.org/resolved-that-america-should-adopt-an-industrial-policy.

[10] Ibid.

[11] Scott Lincicome, “Manufactured Crisis: ‘Deindustrialization,’ Free Markets, and National Security,” Cato Institute, Jan. 27, 2021, https://www.cato.org/publications/policy-analysis/manufactured-crisis-deindustrialization-free-markets-national-security.

[12] Timothy B. Lee, “Why Agatha Christie Could Afford a Maid and a Nanny but not a Car,” Full Stack Economics, Jan. 25, 2022, https://fullstackeconomics.com/why-agatha-christie-could-afford-a-maid-and-a-nanny-but-not-a-car/; see also William D. Nordhaus, “Baumol’s Diseases: A Macroeconomic Perspective,” The B.E. Journal of Macroeconomics 8:1 (2008), http://pinguet.free.fr/nordhaus2008.pdf.

[13] U.S. Bureau of Labor Statistics, “All Employees, Manufacturing / All Employees, Total Nonfarm,” retrieved from Federal Reserve Bank of St. Louis, Feb 23, 2022, https://fred.stlouisfed.org/graph/?g=cAYh.

[14] Michael Brill, Brian Chansky, and Jennifer Kim, “Multifactor Productivity Slowdown in U.S. Manufacturing,” Monthly Labor Review, Bureau of Labor Statistics, July 2018, https://www.bls.gov/opub/mlr/2018/article/multifactor-productivity-slowdown-in-us-manufacturing.htm.

[15] William Nordhaus, “The Sources of the Productivity Rebound and the Manufacturing Employment Puzzle,” National Bureau of Economic Research Working Paper No. 11354, May 2005, https://www.nber.org/system/files/working_papers/w11354/w11354.pdf.

[16] David H. Autor, David Dorn, and Gordon H. Hanson, “The China Syndrome: Local Labor Market Effects of Import Competition in the United States,” American Economic Review 103:6 (2013), https://pubs.aeaweb.org/doi/pdfplus/10.1257/aer.103.6.2121; see also David H. Autor, David Dorn, and Gordon H. Hanson, “The China Shock: Learning from Labor Market Adjustment to Large Changes in Trade,” Annual Review of Economics 8 (2016), https://www.annualreviews.org/doi/pdf/10.1146/annurev-economics-080315-015041.

[17] Katherine Eriksson, Katheryn N. Russ, Jay C. Shambaugh, and Minfei Xu, “Trade Shocks and the Shifting Landscape of U.S. Manufacturing,” Journal of International Money and Finance 111 (March 2021), https://www.sciencedirect.com/science/article/abs/pii/S0261560620302102; see also Scott Lincicome, “Testing the China Shock: Was Normalizing Trade with China a Mistake?” Cato Institute, July 8, 2020, https://www.cato.org/policy-analysis/testing-china-shock-was-normalizing-trade-china-mistake.

[18] Scott Lincicome, “Manufactured Crisis: ‘Deindustrialization,’ Free Markets, and National Security.”

[19] National Center for Science and Engineering Statistics, “Business Research and Development Survey: 2018,” Dec. 16, 2020, https://ncses.nsf.gov/pubs/nsf21312#general-notes&data-tables.

[20] Richard Peach and Charles Steindel, “Low Productivity Growth: the Capital Formation Link,” Liberty Street Economics, Federal Reserve Bank of New York, June 26, 2017, https://libertystreeteconomics.newyorkfed.org/2017/06/low-productivity-growth-the-capital-formation-link/.

[21] Gary P. Pisano and Willy C. Shih, “Restoring American Competitiveness,” Harvard Business Review (July-August 2009), https://hbr.org/2009/07/restoring-american-competitiveness.

[22] Barthélémy Bonadio, Zhen Hou, Andrei Levchenko, and Nitya Pandalai-Nayar, “Global Supply Chains in the Pandemic.”

[23] Department of the Treasury, “How to Depreciate Property,” Internal Revenue Service, Publication 946, updated Oct. 29, 2021, https://www.irs.gov/pub/irs-pdf/p946.pdf.

[24] Alex Muresianu and Jason Harrison, “How the Tax Code Handles Inflation (and How it Doesn’t),” Tax Foundation, June 28, 2021, https://www.taxfoundation.org/taxes-inflation/.

[25] Stephen J. Entin, “The Tax Treatment of Assets and Its Effect on Growth: Expensing, Depreciation, and the Concept of Cost Recovery in the Tax System,” Tax Foundation, Apr. 24, 2013, https://www.taxfoundation.org/tax-treatment-capital-assets-and-its-effect-growth-expensing-depreciation-and-concept-cost-recovery/.

[26] Erica York and Alex Muresianu, “The TCJA’s Expensing Provision Alleviates the Tax Code’s Bias Against Certain Investments,” Tax Foundation, Sept. 5, 2018, https://www.taxfoundation.org/tcja-expensing-provision-benefits/.

[27] David W. Brazell, Lowell Dworkin, and Michael Walsh, “A History of Federal Depreciation Policy,” Office of Tax Analysis, U.S. Department of the Treasury, OTA Paper 64 (May 1989), https://home.treasury.gov/system/files/131/WP-64.pdf.

[28] Barry P. Bosworth, “Taxes and the Investment Recovery,” Brookings Institution, Brookings Papers on Economic Activity No. 1 (1985), https://www.brookings.edu/wp-content/uploads/1985/01/1985a_bpea_bosworth_shoven_summers.pdf.

[29] Dale W. Jorgensen and Kun-Young Yun, “Tax Reform and U.S. Economic Growth,” Journal of Political Economy 98:5 (1990), https://dash.harvard.edu/bitstream/handle/1/3403059/jorgenson_taxreform.pdf?sequence=2.

[30] George E. Moody and Don P. Holdren, “The Effect of the Tax Reform Act of 1985 on Manufacturing Corporations,” Journal of Applied Business Research (Fall 1986), https://clutejournals.com/index.php/JABR/article/view/6560/6637; see also Joseph J. Cordes, Harry S. Watson, and J. Scott Hauger, “Effects of Tax Reform on High Technology Firms,” National Tax Journal 40:3 (September 1987), https://www.jstor.org/stable/41788676.

[31] Kyle Pomerleau, “Why Full Expensing Encourages More Investment Than a Corporate Rate Cut,” Tax Foundation, May 3, 2017, https://www.taxfoundation.org/full-expensing-corporate-rate-investment/.

[32] Scott Greenberg, John Olson, and Stephen J. Entin, “Modeling the Effects of Past Tax Bills,” Tax Foundation, Sept. 14, 2016, https://www.taxfoundation.org/modeling-economic-effects-past-tax-bills/; see also Alan J. Auerbach and Joel Slemrod, “The Economic Effects of the Tax Reform Act of 1986,” Journal of Economic Literature 35:2 (June 1997), https://www.jstor.org/stable/2729788.

[33] Jeffrey Birnbaum and Alan Murray, Showdown at Gucci Gulch: Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform (New York: Random House, 1988).

[34] Ibid.; see also Timur Ergen and Inga Rademacher, “The Silicon Valley Imaginary: US Corporate Tax Reform in the 1980s,” Socio-Economic Review 19:4 (Oct. 14, 2021), https://academic.oup.com/ser/advance-article/doi/10.1093/ser/mwab051/6397034.

[35] Jeffrey Birnbaum and Alan Murray, Showdown at Gucci Gulch: Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform, 61.

[36] Scott Lincicome and Huan Zhu, “Questioning Industrial Policy: Why Government Manufacturing Plans are Unnecessary and Ineffective.”

[37] Don Fullerton and Andrew B. Lyon, “Tax Neutrality and Intangible Capital,” Tax Policy and the Economy 2 (1988), https://www.jstor.org/stable/20061773; see also Yolanda K. Kodrzyzcki, “The Composition of Business Investment: Has Tax Policy Mattered?” National Tax Association 85 (1992), https://www.jstor.org/stable/42910757.

[38] Alan J. Auerbach and Kevin Hassett, “Recent U.S. Investment Behavior and the Tax Reform Act of 1986: A Disaggregate View,” National Bureau of Economic Research, Working Paper No. 3626 (February 1991), https://www.nber.org/system/files/working_papers/w3626/w3626.pdf.

[39] Sam Dumitru and Pedro Serodio, “Abolishing the Factory Tax: How to Boost Investment and Level Up Britain,” Adam Smith Institute, Feb. 19, 2020, https://static1.squarespace.com/static/56eddde762cd9413e151ac92/t/5e4c2406d37804306a23664c/1582048264192/Abolishing+the+Factory+Tax+-+Sam+Dumitriu+%26+Dr+Pedro+Serodio+-+Final.pdf.

[40] Stephen Bond, Kevin Denny, and Michael Devereux, “Capital Allowances and the Impact of Corporation Tax on Investment in the U.K.,” Fiscal Studies 14:2 (May 1993), https://www.jstor.org/stable/24437251.

[41] Elke Asen, “Capital Cost Allowances Across the OECD,” Tax Foundation, Mar. 31, 2021, https://www.taxfoundation.org/publications/capital-cost-recovery-across-the-oecd/; see also Sam Dumitru and Pedro Serodio, “Abolishing the Factory Tax: How to Boost Investment and Level Up Britain.”

[42] Eric Zwick and James Mahon, “Tax Policy and Heterogenous Investment Behavior,” American Economic Review 107:1 (2017), https://www.jstor.org/stable/24911327.

[43] Christopher L. House and Matthew D. Shapiro, “Temporary Investment Tax Incentives: Theory with Evidence from Bonus Depreciation,” American Economic Review 98:3 (2008), https://www.jstor.org/stable/29730094.

[44] Eric Ohrn, “The Effects of Tax Incentives on U.S. Manufacturing: Evidence from State Accelerated Depreciation Policies,” Journal of Public Economics 180 (December 2019), https://ericohrn.sites.grinnell.edu/files/State_Bonus/Ohrn_JPubE_Manuscript.pdf.

[45] Austan Goolsbee, “Investment Subsidies and Wages in Capital Goods Industries: To the Workers Go the Spoils?” National Tax Journal 56:1 (March 2003), https://www.jstor.org/stable/41789662; see also E. Mark Curtis, Daniel G. Garrett, Eric C. Ohrn, Kevin A. Roberts, and Juan Carlos Suárez Serrato, “Capital Investment and Labor Demand,” National Bureau of Economic Research Working Paper No. 29485, February 2022, https://www.nber.org/papers/w29485.

[46] Alex Muresianu, “1980s Tax Reform, Cost Recovery, and the Real Estate Industry: Lessons For Today,” Tax Foundation, July 23, 2020, https://www.taxfoundation.org/1980s-tax-reform-cost-recovery-and-the-real-estate-industry-lessons-for-today/.

[47] Roy E. Cordato, “Destroying Real Estate Through the Tax Code,” Institute for Research on the Economics of Taxation, Feb. 12, 1991, http://iret.org/pub/BLTN-48.PDF; see also Ronald C. Clute, Don P. Holdren, and George E. Moody, “The Impact of the Tax Reform Act of 1986 on the Housing Industry,” Journal of Applied Business Research 4:1 (Fall 1988), https://clutejournals.com/index.php/JABR/article/view/6446/6524.

[48] Taylor LaJoie and Everett Stamm, “An Overview of the Low-Income Housing Tax Credit,” Tax Foundation, Aug. 11, 2020, https://www.taxfoundation.org/low-income-housing-tax-credit-lihtc/.

[49] Michael D. Eriksen, “The Market Price of Low-Income Housing Credits,” Journal of Urban Economics 66:2 (September 2009), https://isiarticles.com/bundles/Article/pre/pdf/49904.pdf.

[50] James M. Poterba, “Taxation and Housing: Old Questions, New Answers,” The American Economic Review 82:2 (May 1992), https://www.jstor.org/stable/2117407.

[51] Thomas Davidoff, “Tax Reform and Sprawl,” Joint Center for Housing Studies at Harvard University, September 2013, https://www.jchs.harvard.edu/sites/default/files/hbtl-05.pdf.

[52] Gilbert E. Metcalf, “Federal Tax Policy Towards Energy,” Tax Policy and the Economy 21 (2007), https://www.journals.uchicago.edu/doi/pdf/10.1086/tpe.21.20061917.

[53] Gilbert E. Metcalf, “Supporting Low-Carbon Energy Through a New Generation of Tax Credits,” The Center for International Environment and Resource Policy, September 2021, https://sites.tufts.edu/cierp/files/2021/09/CPL_Policy_Brief_US_Tax-Credits.pdf.

[54] Molly F. Sherlock, “Energy Tax Provisions: Overview and Budgetary Cost,” Congressional Research Service, Aug. 3, 2021, https://sgp.fas.org/crs/misc/R46865.pdf.

[55] Gilbert Metcalf, “Supporting Low-Carbon Energy Through a New Generation of Tax Credits.”

[56] Clifton Painter and Alex Muresianu, “Tax Treatment of Nuclear Energy Should Be Simplified, Neutral, with Renewable Energy Sources,” Tax Foundation, Aug. 12, 2021, https://www.taxfoundation.org/nuclear-energy-tax-treatment/.

[57] Gilbert E. Metcalf, “Tax Policies for Low-Carbon Technologies,” National Tax Journal 62:3 (September 2009), https://www.journals.uchicago.edu/doi/abs/10.17310/ntj.2009.3.10.

[58] Gilbert Metcalf and Kevin Hassett, “Energy Tax Credits and Residential Conservation Investment: Evidence from Panel Data,” Journal of Public Economics 57:2 (June 1995), http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.996.5080&rep=rep1&type=pdf.

[59] Alex Muresianu, “Carbon TaxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them. : Weighing the Options for Reconciliation,” Tax Foundation, Sept. 29, 2021, https://www.taxfoundation.org/carbon-tax-reconciliation/.

[60] Gilbert Metcalf, “Using Tax Expenditures to Achieve Energy Policy Goals,” American Economic Review 98:2 (May 2008), https://www.aeaweb.org/articles?id=10.1257/aer.98.2.90.

[61] James Sallee, “The Taxation of Fuel Economy,” Tax Policy and the Economy 25:1 (September 2011), https://www.journals.uchicago.edu/doi/full/10.1086/658379.

[62] Kate S. Whitefoot and Steven J. Skerlos, “Design Incentives to Increase Vehicle Size Created from the U.S. Footprint-Based Fuel Economy Standards,” Energy Policy 41 (February 2012), https://www.meche.engineering.cmu.edu/_files/images/research-groups/whitefoot-group/WS-FootprintFuelEconomy-EP.pdf.

[63] Ernst Worrell and Gijs Biermans, “Move Over! Stock Turnover, Retrofit, and Industrial Energy Efficiency,” Energy Policy 33:7 (May 2005), https://www.sciencedirect.com/science/article/pii/S0301421503003203; see also John A. Laitner, Steven Nadel, R. Neal Elliott, Harvey Sachs, and A. Siddiq Khan, “The Long-Term Energy Efficiency Potential: What the Evidence Suggests,” American Council for an Energy-Efficient Economy, January 2012, https://www.aceee.org/sites/default/files/publications/researchreports/e121.pdf.

[64] Marylin A. Brown and Sharon (Jess) Chandler, “Governing Confusion: How Statutes, Fiscal Policy, and Regulations Impede Green Energy Technologies,” Stanford Law and Policy Review 19:3 (Summer 2008), https://smartech.gatech.edu/bitstream/handle/1853/23053/wp28.pdf.

[65] Alex Muresianu, “How Expensing for Capital Investment Can Help Accelerate the Transition to a Cleaner Economy,” Tax Foundation, Jan. 12, 2021, https://www.taxfoundation.org/energy-efficiency-climate-change-tax-policy/.

[66] Rep. Chip Roy, “HR.6690 – Bring Entrepreneurial Advancements To Consumers Here In North America,” May 1, 2020, https://www.congress.gov/bill/116th-congress/house-bill/6690?s=1&r=2.

[67] See later discussion of procurement policy.

[68] Eric Ohrn, “The Effect of Corporate Taxation on Investment and Financial Policy: Evidence from the DPAD,” American Economic Journal: Economic Policy 10:2 (2018), https://ericohrn.sites.grinnell.edu/files/DPAD/DPAD_AEJ_Pol.pdf.

[69] Fernando Leibovichi and Jason Dunn, “Supply Chain Bottlenecks and Inflation: the Role of Semiconductors,” Federal Reserve Bank of St. Louis, Dec. 16, 2021, https://research.stlouisfed.org/publications/economic-synopses/2021/12/16/supply-chain-bottlenecks-and-inflation-the-role-of-semiconductors.

[70] S.1260 – United States Innovation and Competition Act of 2021.

[71] Dean DeChiaro, “House, Senate will go to conference on R&D proposals,” Roll Call, Nov. 18, 2021, https://rollcall.com/2021/11/18/house-senate-will-go-to-conference-on-rd-proposals/.

[72] H.R.4521 – America COMPETES Act of 2022.

[73] President Joseph R. Biden, “State of the Union Address,” Mar. 1, 2021, https://www.whitehouse.gov/state-of-the-union-2022/.

[74] Erica York, “Boost Semiconductor Manufacturing by Removing Tax Barriers, not Creating Tax Subsidies,” Tax Foundation, June 18, 2021, https://www.taxfoundation.org/semiconductor-manufacturing-tax-credit/.

[75] Daniel Bunn, “Tax Subsidies for R&D Spending and Patent Boxes in OECD Countries,” Tax Foundation, Mar. 17, 2021, https://www.taxfoundation.org/rd-tax-credit-rd-tax-subsidies-oecd/.

[76] Ibid.