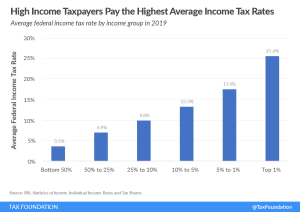

Summary of the Latest Federal Income Tax Data, Tax Year 2020

The latest IRS data shows that the U.S. federal individual income tax continued to be progressive, borne primarily by the highest income earners.

43 min read

The latest IRS data shows that the U.S. federal individual income tax continued to be progressive, borne primarily by the highest income earners.

43 min read

When we discuss tax policy, the conversation inevitably turns to who pays, who should pay, and how much they should pay. Unfortunately, the tax burdens debate is often missing a key point: how income transfer programs—like Social Security or Medicaid—affect households’ tax burdens.

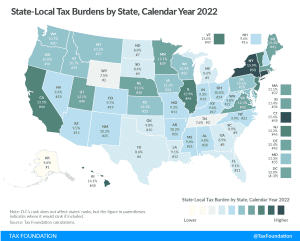

Tax burdens rose across the country as pandemic-era economic changes caused taxable income, activities, and property values to rise faster than net national product. Tax burdens in 2020, 2021, and 2022 are all higher than in any other year since 1978.

24 min read

Senators Chris Van Hollen (D-MD) and Cory Booker (D-NJ) have each introduced proposals aimed at cutting taxes for lower- and middle-income taxpayers and raising them on high-income taxpayers.

9 min read

If you’ve filed your taxes already, you may have noticed a larger refund this year. That’s due to changes Congress made with the One Big Beautiful Bill Act (OBBBA) last year that retroactively cut taxes for 2025.

3 min read

Structural reforms such as broadening tax bases, improving cost recovery, and shifting toward less distortive taxes can improve competitiveness without necessarily reducing revenue.

7 min read

Senator Bernie Sanders introduced a proposed 5 percent annual wealth tax on billionaires to fund direct payments to Americans and expand social welfare programs.

5 min read

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections. How do income taxes compare in your state?

9 min read

State lawmakers around the country have begun their legislative sessions, and many are considering tax reform. This piece highlights some of the areas on which they are likely to focus.

4 min readOur analysis of the major tax provisions included in the OBBBA finds it will increase long-run GDP by 0.7 percent. The major tax provisions will reduce federal tax revenue by nearly $5.2 trillion between 2025 and 2034, on a conventional basis.

12 min read

Denmark (55.9 percent), France (55.4 percent), and Austria (55 percent) levy the highest top personal income tax rates in Europe.

4 min read

Washington lawmakers are holding their first hearing on long-anticipated legislation that would create a new 9.9 percent tax on income over $1 million.

6 min read

Should both HB 979 and HB 378 pass, Virginia would have the nation’s highest top marginal rate on investment income.

8 min read

Michigan’s proposed 5 percent income surtax on high earners, yielding a top marginal rate of 9.25 percent, is also a tax on the small businesses that employ nearly 2 million Michiganders.

25 min read

When taxpayers file their 2025 tax returns in 2026, many will see larger refunds than in recent years. That’s due to the One Big Beautiful Bill Act (OBBBA), which reduced individual income taxes for 2025 by an estimated $129 billion.

4 min read

The 2026 Billionaire Tax Act, a California ballot initiative, would ostensibly impose a one-time tax of 5 percent on the net worth of the state’s billionaires. Due, however, to aggressive design choices and possible drafting errors, the actual rate on taxpayers’ net worth could be dramatically higher.

18 min read

A proposed “millionaire’s tax” in Washington State would yield the highest combined state and local top rate in the country.

6 min read

As policymakers consider reforms to the individual income tax, understanding the types of income that make up the individual income tax base can help them understand the trade-offs of different changes to the tax system.

8 min read

Scandinavian countries are well known for their broad social safety nets and their public funding of services such as universal health care, higher education, parental leave, and child and elderly care. High levels of government spending naturally require high levels of taxation. So, how do these countries raise their tax revenues?

7 min read

Forty-three states will ring in 2026 with notable tax changes. Eight states will see reduced individual income tax rates in the new year while four states will see reduced corporate income tax rates.

30 min read

Instead of implementing new wealth taxes, European policymakers should focus on making the current tax system more efficient and transparent.

Switzerland’s proposed 50 percent billionaire estate tax promises negligible revenue, risks economic harm, and strips cantons of their autonomy and tax competition.

5 min read

Who really pays for European welfare states? Many assume the answer is obvious: high-income earners contribute while low-income earners benefit. However, that assumption is only partly true, and often misleading.

6 min read