Key Findings

- Studies indicate that taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. complexity and compliance costs are on the rise, with much of the compliance burden attributable to business income taxes. To better understand business tax compliance costs in light of recent tax and regulatory developments, we surveyed 21 large multinational enterprises (MNEs).

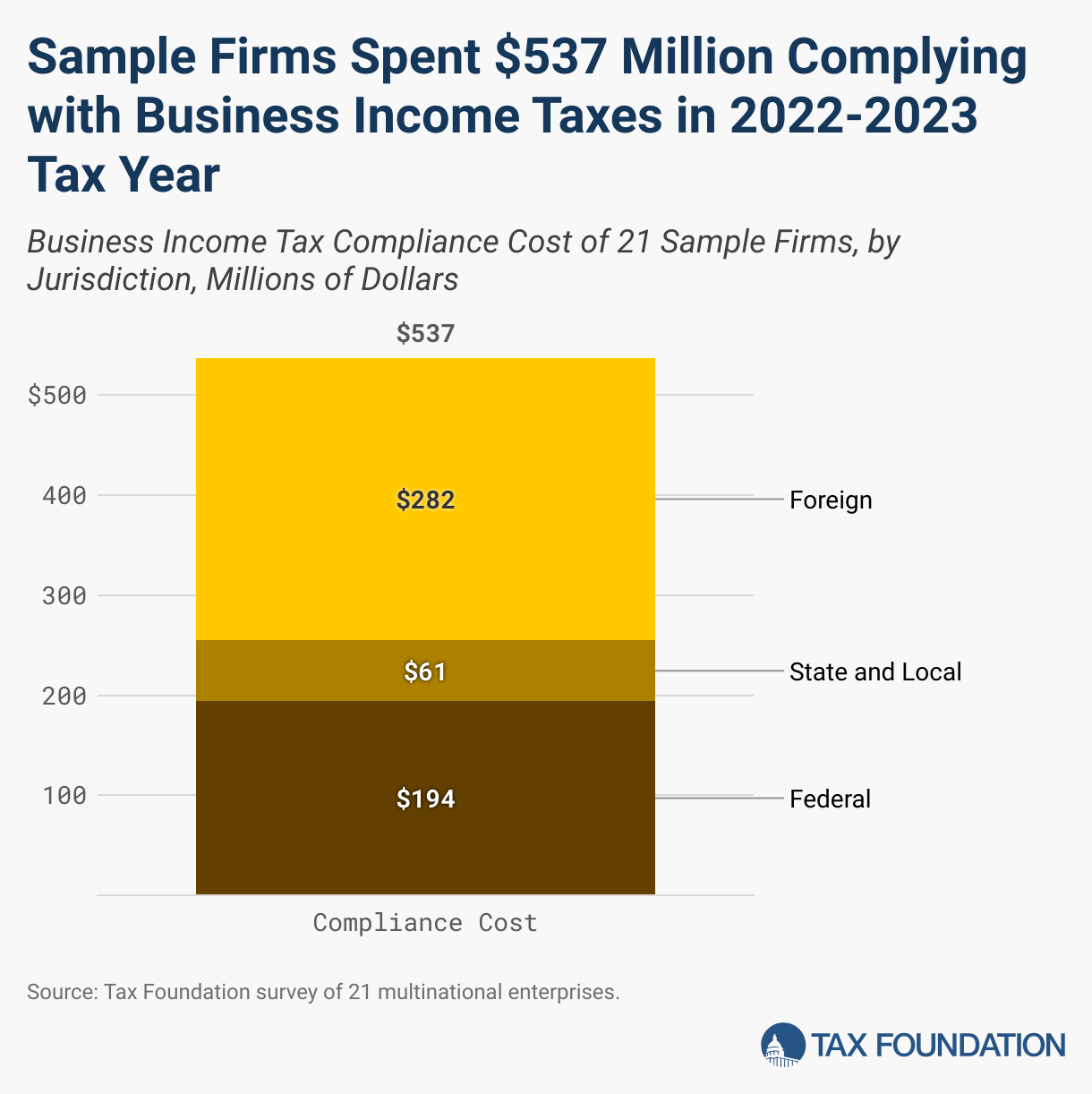

- In total, as of tax year 2022 or 2023, the companies spent $537 million on income tax compliance, an average of $25.6 million per company, including $282 million for foreign income tax compliance, $194 million for federal income tax compliance, and $61 million for state and local income tax compliance.

- While the sample size is small and limited to relatively large companies, evidence points to economies of scale in tax compliance costs, meaning smaller companies are disproportionately burdened and disadvantaged by tax complexity.

- All companies indicated an increase in income tax complexity since 2017, with a weighted average increase in funds dedicated to compliance costs of 32 percent from 2017 to 2023. Most companies attributed compliance cost growth primarily to increasingly complicated international rules, including the Tax Cuts and Jobs Act (TCJA) reforms. Several companies also cited the new corporate alternative minimum tax enacted as part of the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. Reduction Act, as well as the OECD’s Pillar Two rules and the TCJA provision requiring research and development amortization.

- On average, companies estimated that 43 percent of their federal income tax compliance costs were due to rules relating to foreign-source income.

- Lawmakers should consider simplifying reforms, including reducing unnecessary information reporting, especially for foreign operations, and eliminating one or more layers of minimum tax. More fundamental reforms should also be considered, such as Estonia’s much simpler distributed profits taxA distributed profits tax is a business-level tax levied on companies when they distribute profits to shareholders, including through dividends and net share repurchases (stock buybacks). .

Introduction

The US federal income tax code is staggeringly complex, the result of decades of legislative and regulatory additions punctuated only rarely by efforts to streamline and simplify certain rules. However, the net effect has been a trend toward more income tax complexity and with it a growing burden of compliance costs.

As one measure, a recent study finds that the length of the Internal Revenue Code has grown about 40 percent over the last three decades, from 3.1 million words in 1994 to 4.3 million words in 2021 (for context, the King James Bible is about 783,000 words). The study also compares tax codes across six countries, finding the US has by far the longest and most complex tax code.[1]

To meet a requirement of the Paperwork Reduction Act of 1980, the Internal Revenue Service (IRS) and the Office of Information and Regulatory Affairs (OIRA) provide regular estimates of the time it takes taxpayers to complete each tax form.[2] The latest estimates indicate Americans will spend more than 7.9 billion hours complying with the federal tax code in 2024. Multiplying these hours by an average hourly compensation yields an aggregate compliance cost of about $413 billion. The IRS estimates Americans spend an additional $133 billion on out-of-pocket costs to comply with the tax code, resulting in total compliance costs of $546 billion in 2024—almost 2 percent of GDP.[3]

The IRS/OIRA-based estimates indicate much of the compliance burden is due to rules related to taxing business income. The compliance cost associated with corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. returns is nearly $119 billion, and quarterly tax filings and depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. schedules cost businesses an additional $70 billion annually. Pass-through businesses that file under the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. code bear a substantial portion of the $145 billion compliance cost associated with individual income tax returns, as well as the $19 billion compliance cost related to the pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. deduction.

A limited number of other studies gauge US business tax compliance costs in ways that are comparable across countries, generally finding the US has a relatively complicated business tax code leading to relatively high costs for US business taxpayers.[4]

Understanding the drivers of compliance costs for business income taxes, how they affect companies and the broader economy, and how recent legislation and regulatory developments are likely to change compliance costs can shed light on where to concentrate reform efforts.

In some areas, the degree to which the IRS/OIRA-based estimates account for recent developments is not entirely clear. In particular, the new corporate alternative minimum tax (CAMT), enacted as part of the Inflation Reduction Act in 2022, targets US corporations with $1 billion or more of adjusted financial statement income (book incomeBook income is the amount of income corporations publicly report on their financial statements to shareholders. It provides a picture of a firm’s financial performance and follows Generally Accepted Accounting Practices (GAAP). While it is a useful measure for assessing financial performance, it is not useful for assessing tax liability. ) and is likely to significantly increase compliance costs.[5] As well, the Organisation for Economic Co-operation and Development’s (OECD) Pillar Two initiative is leading several countries to implement minimum taxes that could apply to the worldwide book income of US-based multinational enterprises (MNEs), creating an additional complex layer of tax that varies by country.[6]

A recent survey by Deloitte of more than 1,000 tax and finance executives within the Forbes Global 2000 set of MNEs indicates that the biggest challenge faced by these professionals is “increasingly burdensome and complex tax reporting and data collection requirements.”[7] Tax reporting outranks other concerns including the OECD Pillar Two initiative, changing patterns of remote work, and increased environmental taxation, although rising compliance costs are an aspect of these other concerns, especially Pillar Two.

To that point, Deloitte also recently surveyed more than 500 tax leaders and CFOs of MNEs potentially subject to the Pillar Two rules, finding these professionals expect the rules to result in substantial new compliance cost burdens.[8] Among respondents, 70 percent expected to spend $500,000 or more annually on compliance costs related to Pillar Two, and 25 percent expected to spend more than $1 million. Meanwhile, only 53 percent of respondents anticipate their businesses will incur higher taxes as a result of Pillar Two, indicating that a large share of companies expect the compliance costs of Pillar Two to exceed the associated tax liabilities. In addition, 77 percent of respondents indicated it is very likely or moderately likely that Pillar Two will lead to more tax disputes due to the “complexity of the new rules, lack of clarity and certainty, and varying interpretations by countries.”

Contributing to efforts to better understand business tax compliance costs in light of recent developments, we fielded a survey to measure the compliance costs associated with business income taxes at the federal, state and local, and international levels. Many of the questions were based on an earlier survey by Joel Slemrod and Marsha Blumenthal, with updates and expansions to cover current developments and foreign business income taxes, resulting in a detailed and comprehensive questionnaire.[9] We solicited responses from hundreds of businesses with a US presence and received completed responses from a small sample (21) of relatively large MNEs. While the small sample limits the conclusions we can draw, we are still able to identify several key insights because these are companies likely to have direct experience with the new US CAMT, OECD Pillar Two rules, and other taxes and reporting requirements aimed at large MNEs. Our paper provides a summary of the main results and analysis of the survey.

Survey Results and Analysis

In May and June of 2024, we solicited responses to the survey by emailing dozens of large companies and several business associations that agreed to participate by sending the survey to their members (see appendix for a copy of the survey questionnaire and methodology). Over the course of June, July, and early August, 21 companies submitted responses to the survey.

Company Characteristics

All 21 companies that responded to the survey are MNEs, and 20 of the 21 are based in the US. The companies represent a range of industries, including manufacturing, finance and insurance, wholesale and retail, information, transportation and warehousing, mining, and services.

The companies range in size but are relatively large. Among respondents, the average number of worldwide employees is about 148,000; five companies have between 500 and 10,000 employees, eight companies have between 10,000 and 100,000, and the remaining eight companies have more than 100,000 employees. Most respondents indicated that the majority of their worldwide employment is in the US. In total, respondents reported about 2 million US employees, representing about 1.4 percent of US employment (full-time equivalents), and about 3.1 million worldwide employees.[10] The companies reported total worldwide assets of about $4.4 trillion, with an average of $222 billion, and total worldwide receipts or sales of about $1.7 trillion, with an average of $81 billion, as of 2022 or 2023.

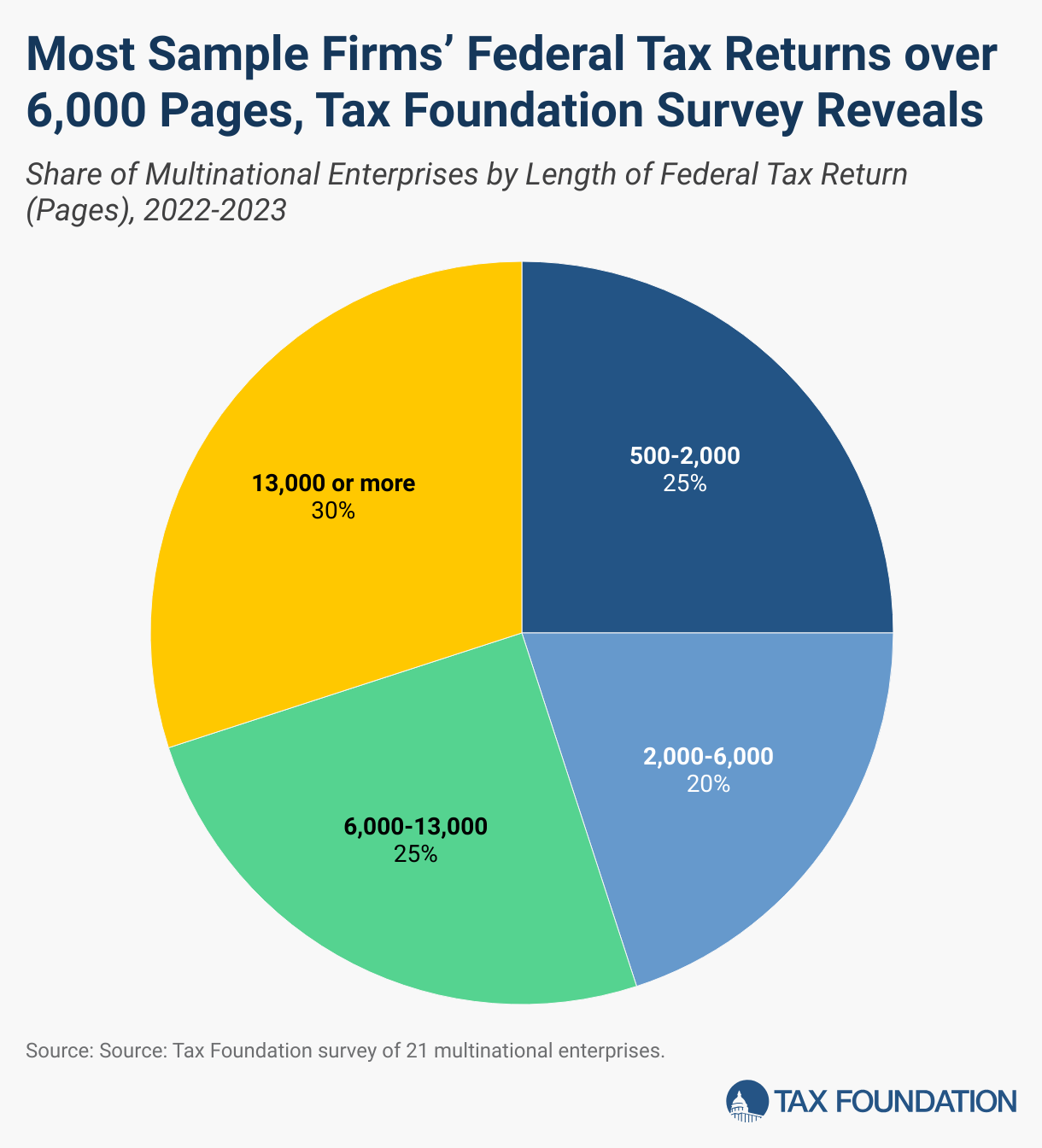

All respondents were C corporations that filed a consolidated federal tax return that included several entities (on average about 212).[11] Most respondents (16) referred to tax year 2022, while four referred to a tax year ending in 2023, and one did not indicate a year. Most respondents reported filing several thousand pages as part of their federal tax return, with an average length of 10,567 pages and a median of 6,050 pages; six reported a length in excess of 13,000 pages, 13 reported a length between 1,000 and 13,000 pages, and one reported a length between 500 and 1,000 pages.

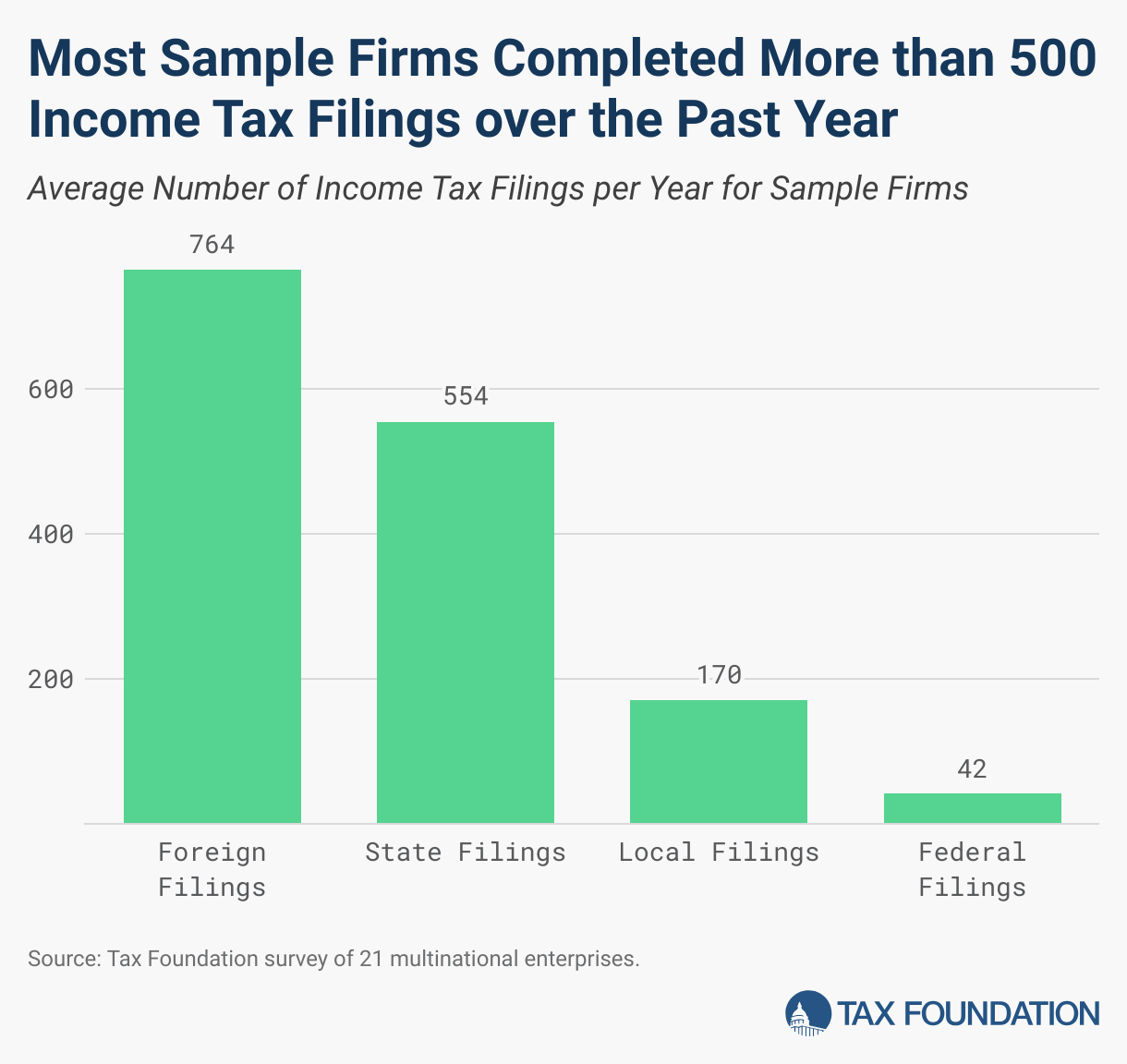

In addition, most respondents indicated they completed several other federal income tax filings over the past year (including for estimated tax, request for extension, and amended or corrected returns), with an average of about 42 total federal income tax filings per company. To comply with income taxes at the state and local levels, respondents made an average of 554 state income tax filings over the past year, plus an average of about 170 local income tax filings. All respondents reported significant foreign activity, with an average of about 764 foreign income tax filings made over the last year. In total, including income tax filings at all levels of government, most respondents indicated they completed several hundred or several thousand income tax filings over the past year, with an average of 1,381 and a median of 567.

Regarding the CAMT—which was enacted in 2022 and went into effect January 1, 2023, but continues to lack final regulations—18 of the 21 surveyed companies indicated they have not been subject to it and only five companies expect to be subject to it within the next two years. Of the six companies with a current or expected CAMT liability, there is no indication they are relatively large compared to other companies in the sample, even though CAMT targets companies with $1 billion or more of income. The group of six includes some of the smallest and largest companies in the sample (measured by employees, assets, or sales), and by some measures, the companies are relatively small compared to the sample average and median. Note, however, that the survey did not ask respondents to report their income, and it is possible that even the smallest companies in the sample have income above $1 billion.

Of the 18 companies indicating they have not been subject to CAMT, all 18 indicated they have gone through the effort of calculating the CAMT liability or otherwise made calculations to determine if they are in scope. Consistent with recent studies, our findings indicate a much larger set of companies are expending resources to comply with the CAMT than are actually paying tax under its rules.[12]

Measures of Compliance Costs

Our survey asked companies to estimate the number of full-time equivalent (FTE) staff devoted to business income tax at the federal, state and local, and foreign levels. Companies provided a range of responses: six companies had a staff size exceeding 100, eight companies had between 20 and 100 staff, and the remaining seven companies had fewer than 20 staff. In total, the companies had 1,405 FTEs devoted to income tax compliance, with about 63 percent devoted to foreign income tax, 27 percent to federal income tax, and 9 percent to state and local income tax. Larger tax departments tended to have a greater share of staff devoted to foreign income tax.

As a share of total company employment, staff devoted to income tax compliance was about 0.05 percent on average, but the ratio varied considerably across companies, with smaller companies having a much larger ratio. Among the five smallest companies by total employment, the average share of staff devoted to income tax compliance was about 0.5 percent, 10 times larger than for the sample as a whole. Across the sample, company size as measured by employment is negatively correlated (-0.22) with the share of company employment devoted to income tax compliance. Our results are consistent with other studies finding economies of scale in tax compliance costs.[13]

Reflecting the variation in staff size, companies varied in how much they spent on salaries and other compensation for all staff devoted to income tax compliance. The six largest tax departments each spent in excess of $10 million, eight companies spent between $5 million and $10 million, and the remaining seven companies spent less than $5 million. In total, the companies spent $251 million on staff devoted to income tax compliance, with about 54 percent devoted to foreign income tax, 35 percent to federal income tax, and 11 percent to state and local income tax. Larger tax departments tended to have a greater share of compensation devoted to foreign income tax.

By task, the largest portion of compliance cost measured by compensation was for filing returns (27 percent), followed by preparing information for financial statements and related reporting (18 percent); planning (11 percent); dealing with other personnel (11 percent); audits, appeals, and litigation (10 percent); keeping records (9 percent); researching tax laws and filing requirements (7 percent); and monitoring and participating in the tax policy process (5 percent).

In addition to compensation, companies in the sample spent a total of $71 million on non-personnel costs for income tax compliance (e.g., for computers, software, record storage and retrieval, office space, general supplies, copying, travel, research subscriptions, and training, etc.)—on average about $3.4 million per company. On average, 51 percent of this cost was for foreign income tax compliance, 36 percent was for federal income tax compliance, and 11 percent was for state and local income tax compliance. Combined, including compensation and non-personnel costs, the companies spent $322 million on in-house costs for income tax compliance, an average of $15.3 million per company.

Companies spent an additional $215 million on outside tax assistance related to income tax compliance, an average of $10.2 million per company. On average, 51 percent of this cost was for foreign income tax compliance, 37 percent was for federal income tax compliance, and 12 percent was for state and local income tax compliance. Accounting firms received the largest portion (69 percent) of this expenditure, followed by law firms (26 percent), and other firms (5 percent). Outside tax assistance was primarily for planning (25 percent), filing (24 percent), and audits, appeals, and litigation (23 percent), and to a lesser degree for researching tax laws (10 percent), monitoring and participating in the tax policy process (8 percent), and other tasks (each less than 5 percent).

In total, combining in-house and external costs, the companies spent $537 million on income tax compliance, an average of $25.6 million per company. Of the total, $282 million (53 percent) was for foreign income tax compliance, $194 million (36 percent) was for federal income tax compliance, and $61 million (11 percent) was for state and local income tax compliance.

As a share of total company revenues, total compliance costs amounted to 0.03 percent on average, but this varied considerably across companies. As with employment, compliance cost as a share of revenue is negatively correlated (-0.24) with revenue, again pointing to economies of scale in compliance costs. These results hold when looking at compliance cost as a share of assets, which is 0.01 percent on average but higher for smaller companies: compliance cost as a share of assets is negatively correlated (-0.31) with assets.[14]

Causes of Compliance Costs and Suggested Reforms

When asked to name aspects of the current tax code that are most responsible for the cost of complying with federal income tax, companies most commonly cited international rules, especially the TCJA reforms (GILTI, BEAT, and FDII), as well as Subpart F, foreign tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. rules, and reporting requirements for controlled foreign corporations (particularly Form 5471). On average, companies estimated that 43 percent of their federal income tax compliance costs were due to rules relating to foreign-source income.[15]

Several companies also mentioned the rules regarding research and development (R&D), including the R&D credit as well as the new requirement to amortize R&D costs over the course of 5 years in the case of domestic R&D or 15 years in the case of foreign R&D. While the R&D credit has been a complicated aspect of the code since 1981, the requirement to amortize R&D is new as of 2022, due to a TCJA provision. Prior to that, companies were simply allowed to fully deduct (expense) R&D costs in the year incurred.

Other provisions mentioned by more than one respondent include the new CAMT, the Pillar Two rules (another minimum tax requiring another set of books), and rules relating to transfer pricing, depreciation, and interest disallowance.

When asked to name aspects of the current tax code that are most responsible for the cost of complying with state income tax, companies most commonly mentioned states decoupling from federal rules and the general lack of conformity and standardization across states. Companies also named many of the same federal issues, including GILTI and foreign income inclusions, depreciation rules, and interest disallowance rules. More than one company also mentioned apportionmentApportionment is the determination of the percentage of a business’s profits subject to a given jurisdiction’s corporate income tax or other business tax. US states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. rules. When asked to name jurisdictions where compliance costs are most attributable, companies most commonly mentioned California, as well as New York (state and city), Massachusetts, Texas, and Illinois.

When asked to name aspects of the current tax code that are most responsible for the cost of complying with foreign income tax, several companies mentioned transfer pricing rules, as well as Pillar Two and the challenge of operating in multiple countries. When asked to name jurisdictions where compliance costs are most attributable, companies most commonly mentioned the UK and India, as well as Australia.

Perhaps not surprisingly, every company in the sample indicated tax complexity has increased since 2017. The average company estimated a 29 percent increase in its funds allocated for income tax compliance between 2017 and 2023, a 32 percent increase for the sample when weighted by compliance cost. When asked to name aspects of the tax system, including federal income tax, state and local income tax, and foreign income tax, that have increased complexity the most since 2017, the largest number of companies (over half the sample) mentioned the international rules, including the TCJA reforms (GILTI, FDII, BEAT). Several other companies mentioned the new CAMT, Pillar Two rules, and the requirement to amortize R&D. When asked to name areas of the tax code that have become simpler, most companies answered with “none” or something similar.

About one-third of companies indicated they were dissatisfied with their interactions with the IRS. In describing reasons for dissatisfaction, companies noted unnecessary delays, errors, and litigation caused by a lack of experience and turnover at the IRS, as well as bureaucratic processes, a lack of transparency, and a lack of communication across teams. In general, companies indicated little has changed over the last two years regarding their level of satisfaction with IRS interactions. Most companies (18 of 21) indicated they were currently under examination by or have tax years before appeals or under litigation with the IRS.[16]

Several companies (10) indicated tax complexity is a major factor in either location, investment, or planning decisions. Only a slightly larger number of companies (12) indicated income tax liability is a major factor in those decisions.

Companies were asked to suggest reforms to reduce compliance costs, and they offered several ideas. More than one company recommended reducing information forms, unnecessary filings, and disclosure reporting when no liability exists (such as for BEAT and CAMT); streamlining Form 5471 reporting for controlled foreign corporations; eliminating tax regimes based on book income; and avoiding retroactivity and temporary changes.

Conclusion

Business income taxes have become extraordinarily complex, particularly for large MNEs operating in multiple jurisdictions across the US and internationally. Multiple layers of minimum taxes, including the new CAMT and the OECD Pillar Two rules, on top of the TCJA’s complex international reforms (including GILTI, another minimum tax), and other changes under the TCJA, such as R&D amortization, have led to a substantial increase in compliance costs since 2017. Large companies may be able to absorb these costs, master the new rules, and handle additional waves of complexity and uncertainty due to economies of scale in compliance costs. However, complex policies may be reducing dynamism and competition more broadly in the economy, to the extent they present barriers to entry for, say, domestic companies seeking to grow internationally, or mid-sized companies seeking to become large companies. In other words, the case for simpler taxes is really made by considering the impacts on the millions of smaller companies and potential companies that would be allowed to flourish absent the complexities of today’s tax system.

The companies that responded to the survey have suggested many sensible reforms to simplify business taxes, including reducing unnecessary information reporting, especially regarding foreign operations. It is also a good idea to eliminate one or more of the minimum taxes, such as CAMT, that require companies to keep multiple sets of books. Streamlining the treatment of R&D would also make sense. More fundamental reforms to business tax should also be considered, such as the much simpler distributed profits tax that Estonia has implemented.[17] In general, lawmakers should consider compliance costs—not just tax liabilities—when evaluating reforms to business income taxation.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeAppendix: Survey Methodology, Initial Request and Questionnaire

We created a survey to measure tax compliance costs associated with business income taxes at the federal, state and local, and international levels. The survey includes a questionnaire with 62 questions grouped into four sections, a copy of which is provided below. The first section asks about company characteristics, the second section about in-house compliance costs, the third section about external compliance costs, and the fourth section about attitudes and suggestions for reform. Many of the questions are based on an earlier survey by Joel Slemrod and Marsha Blumenthal with updates and expansions to cover current developments and foreign business income taxes.[1] We used Survey Monkey to create a web-based survey instrument that includes the questionnaire, an introduction, and instructions.

On May 29, 2024, we sent emails to several dozen companies that have a pre-existing relationship with the Tax Foundation requesting they complete the survey by July 12, 2024, attaching a PDF copy of the questionnaire, introduction, and instructions. We also sent the request to several business associations that agreed to participate by sending the survey to their members (the Business Roundtable, U.S. Chamber of Commerce, Global Business Alliance, and American Petroleum Institute). We sent periodic reminders in June and July, extended the deadline, and closed the survey in mid-August.

A total of 21 companies completed the survey sufficiently to be included, with some companies submitting the survey by filling out the PDF and sending it by email. We then validated and corrected the responses in some cases, e.g., so that all responses were in the requested units and consistent with other available information about the company. In a small number of cases where responses were missing, we imputed responses using other available information about the company and average relationships between variables for the sample as a whole.

The following is the text of the initial request and the survey questionnaire:

Initial Request

Dear [recipient],

The business community is well aware of the increasing complexity of the tax system and the rising cost of complying with it. However, there is little in the way of research to shed light on the degree to which tax compliance cost has increased in recent years, and the factors that are driving it, despite the fact that business taxes in the US have changed dramatically in recent years through major legislation, such as the 2017 Tax Cuts and Jobs Act and the 2022 Inflation Reduction Act, as well as OECD rulemaking impacting international taxes. What we do know, from IRS surveys of US taxpayers, is that federal tax compliance cost is in aggregate on the order of $300 billion annually, and businesses bear the lion’s share of this cost via additional operating expenses.

Tax Foundation is researching tax compliance costs with this survey [HTML link to Survey Monkey interactive survey], and we would welcome your participation in this important work. We are asking several hundred companies with a US presence to participate.

All results will be anonymous and aggregated. Separate company data will not be disclosed. A final published analysis is planned for this September. While not required, please share your contact information in the survey for any follow-up questions.

Please complete the survey by July 12. If you have any questions, please contact Will McBride (wmcbride@taxfoundation.org). Thank you.

Daniel Bunn,

President and CEO

[1] Joel Slemrod and Marsha Blumenthal, “The Income Tax Compliance Cost of Big Business,” Tax Foundation, Nov. 1, 1993, https://taxfoundation.org/research/all/federal/income-tax-compliance-cost-big-business/.

[1] Youssef Benzarti and Luisa Wallossek, “Rising Income Tax Complexity,” NBER Working Paper 31944, December 2023, https://www.nber.org/papers/w31944.

[2] John Guyton, Pat Langetieg, Pete Rose, Brenda Schafer, and Sherri Edelman, “Taxpayer Compliance Burden,” IRS Publication 5743, February 2023, https://www.irs.gov/pub/irs-pdf/p5743.pdf.

[3] Scott Hodge and Claire Rock, “Tax Complexity Now Costs the U.S. Economy Over $546 Billion Annually,” Tax Foundation, Aug. 6, 2024, https://taxfoundation.org/data/all/federal/irs-tax-compliance-costs/. For a review of related studies and a discussion of the larger topic of deadweight loss associated with the tax code, see Jason J. Fichtner and Jacob M. Feldman, “The Hidden Costs of Tax Compliance,” Mercatus Center, May 20, 2013, http://mercatus.org/sites/default/files/Fichtner_TaxCompliance_v3.pdf.

[4] Diego D’Andria and Mareike Heinemann, “Overview on the Tax Compliance Costs Face by European Enterprises – with a Focus on SMEs,” European Parliament, February 2023, https://www.europarl.europa.eu/RegData/etudes/STUD/2023/642353/IPOL_STU(2023)642353_EN.pdf; World Bank Group and PwC, Paying Taxes 2020, Nov. 26, 2019, https://archive.doingbusiness.org/en/reports/thematic-reports/paying-taxes-2020; Alex Mengden, “International Tax Competitiveness Index 2023,” Tax Foundation, Oct. 18, 2023, https://taxfoundation.org/research/all/global/2023-international-tax-competitiveness-index/; William McBride, Huaqun Li, Garrett Watson, Alex Durante, Erica York, Alex Muresianu, “Details and Analysis of a Tax Reform Plan for Growth and Opportunity,” Tax Foundation, Jun. 29, 2023, https://taxfoundation.org/research/all/federal/growth-opportunity-us-tax-reform-plan/; William McBride, Garrett Watson, and Erica York, “Taxing Distributed Profits Makes Business Taxation Simple and Efficient,” Tax Foundation, Mar. 1, 2023, https://taxfoundation.org/blog/distributed-profits-tax-us-businesses/.

[5] William McBride, Alex Muresianu, Erica York, and Michael Hartt, “Inflation Reduction Act One Year After Enactment,” Tax Foundation, Aug. 16, 2023, https://taxfoundation.org/research/all/federal/inflation-reduction-act-taxes/.

[6] Isabella Sara and Sean Bray, “Pillar Two’s Unintended Consequences,” Tax Foundation, Aug. 22, 2024, https://taxfoundation.org/blog/pillar-two-unintended-consequences/; Daniel Bunn, “Weeding the Garden of International Tax,” Tax Foundation, Jul. 19, 2023, https://taxfoundation.org/blog/decluttering-international-tax-rules/.

[7] Deloitte, “2024 Global Tax Policy Survey,” Jul. 29, 2024, https://www.deloitte.com/global/en/about/press-room/deloittes-2024-global-tax-policy-survey-reveals-executives-navigating-priorities.html.

[8] Deloitte, “Committed to Compliance: Preparing for Pillar Two,” Jul. 31, 2024, https://www.deloitte.com/content/dam/assets-shared/docs/services/tax/2024/dttl-pillar-two-research-report.pdf.

[9] Joel Slemrod and Marsha Blumenthal, “The Income Tax Compliance Cost of Big Business,” Tax Foundation, Nov. 1, 1993, https://taxfoundation.org/research/all/federal/income-tax-compliance-cost-big-business/; See also Arthur P. Hall, “The High Cost of Tax Compliance for U.S. Business,” Tax Foundation, Nov. 1, 1993, https://taxfoundation.org/data/all/federal/high-cost-tax-compliance-us-business/; Joel Slemrod and Varsha Venkatesh, “The Income Tax Compliance Cost of Large and Mid-Size Businesses,” Ross School of Business Paper No. 914, September 2002, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=913056; Chris Evans, Philip Lignier, and Binh Tran-Nam, “The Tax Compliance Costs of Large Corporations: An Empirical Inquiry and Comparative Analysis,” Canadian Tax Journal 64:4 (2016), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2909028.

[10] US employment measured in full-time equivalents was 141.7 million as of 2022. See Bureau of Economic Analysis, “Table 6.5D Full-Time Equivalent Employees by Industry,” https://www.bea.gov/itable/national-gdp-and-personal-income.

[11] One respondent indicated they also filed partnership returns, and another indicated they also filed an insurance return. All but five respondents indicated they also filed one or more unconsolidated tax returns.

[12] For example, a recent study finds that about 80 companies are expected to pay incremental tax under the CAMT rules but a total of about 268 are expected to be in scope. See Jennifer Blouin and Nathan Born, “The Corporate Alternative Minimum Tax: A Congressional Folly,” National Tax Journal 77:2 (June 2024), https://www.journals.uchicago.edu/doi/abs/10.1086/730211.

[13] Joel Slemrod and Marsha Blumenthal, “The Income Tax Compliance Cost of Big Business,” Tax Foundation, Nov. 1, 1993, https://taxfoundation.org/research/all/federal/income-tax-compliance-cost-big-business/; Diego D’Andria and Mareike Heinemann, “Overview on the Tax Compliance Costs Face by European Enterprises – with a Focus on SMEs,” European Parliament, February 2023, https://www.europarl.europa.eu/RegData/etudes/STUD/2023/642353/IPOL_STU(2023)642353_EN.pdf

[14] Because of the variation in compliance costs by company size, as well as the small sample size, it would not be appropriate to scale the results of the survey to a larger population of companies.

[15] A similar result came out of the original survey by Slemrod and Blumenthal.

[16] A similar share of companies indicated they were currently under examination by or have tax years before appeals or under litigation with both state and foreign revenue agencies.

[17] William McBride, Huaqun Li, Garrett Watson, Alex Durante, Erica York, and Alex Muresianu, “Details and Analysis of a Tax Reform Plan for Growth and Opportunity,” Tax Foundation, Jun. 29, 2023, https://taxfoundation.org/research/all/federal/growth-opportunity-us-tax-reform-plan/; William McBride, Garrett Watson, and Erica York, “Taxing Distributed Profits Makes Business Taxation Simple and Efficient,” Tax Foundation, Mar. 1, 2023, https://taxfoundation.org/blog/distributed-profits-tax-us-businesses/.

Share this article