Members of the Revenue, Education, and Retirement Committees,

Thank you for the opportunity to testify today on LB 289 as amended by AM 1381. My name is Joseph Bishop-Henchman, and I am with the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation in Washington, D.C. We are a national think tank that collects data and conducts analysis on tax issues. We do not take a position on legislation, but I would like to make three informational points.

First, sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. broadening is a common trend undertaken in many states now, as a way of modernizing the sales tax to reflect today’s service-based economy. However, you should be aware that including sales tax exemptions only for necessities is a difficult task, as every sale of a good or service is considered a necessity by someone. Additionally, picking only a few goods and services to subject to sales tax, rather than a more comprehensive approach that doesn’t leave many exemptions on the table as you do here, can leave the sectors you are expanding the sales tax to feeling unfairly targeted.

Second, cigarette tax revenue declines year over year, due to falling consumption of that product. This is a nationwide, decades-long trend. Using this revenue dollar-for-dollar for tax cuts elsewhere may balance in year one but will create a widening gap in subsequent years as that revenue source resumes its monotonic decline. Cigarette tax revenue should not be part of a package designed to be revenue-neutral, because it makes it not revenue-neutral.

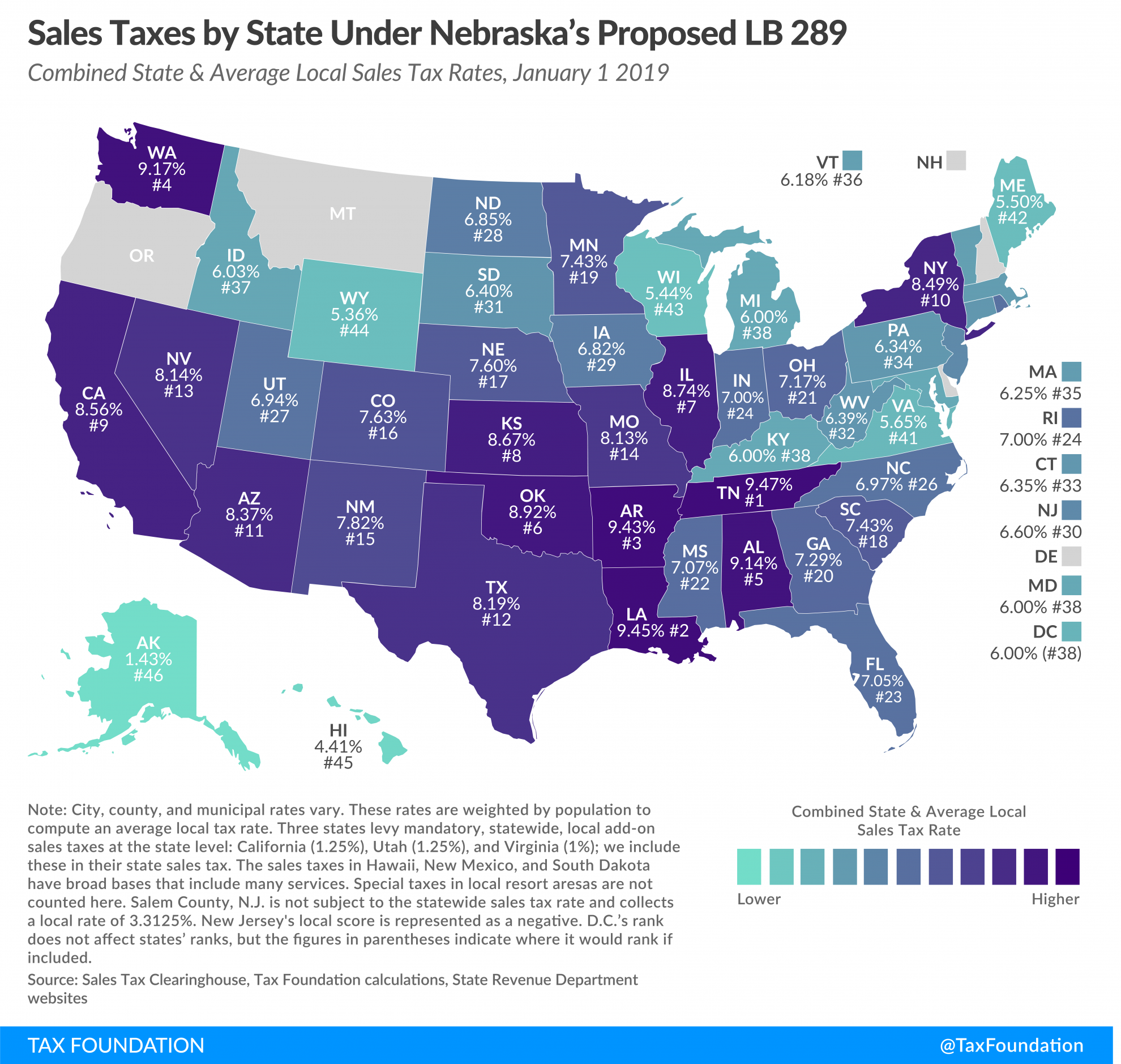

Third, Nebraska currently has the 27th highest sales tax in the United States by rate when you include both state and average local sales taxes. This bill would take it to 17th highest, similar to Colorado’s.

{kind=link}

Nebraska’s property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. is currently 12th highest by collection, and this bill would take it to 13th or 14th highest, still higher than Kansas, Missouri, Colorado, and South Dakota. (See table.)

Nebraska would still have the 19th highest individual income tax, just below Minnesota and higher than Missouri, Kansas, and Colorado, and 16th highest corporate income tax, as this bill misses the opportunity to address those taxes.

Overall, we project that this bill would worsen Nebraska’s ranking on the State Business Tax Climate Index, our comprehensive ranking of state tax structures for business friendliness, from 24th to 26th if the property tax reductions fully materialize, and 29th if they do not, moving below Kansas in terms of our ranking of state tax structure. It would not be unprecedented: my home state of California, for example, has a core tax policy of raising sales and income taxes to pay for lower property taxes, with resultant pros and cons.

Put simply, Nebraska has high income, business, and property taxes. This bill would result in Nebraska having high income, business, property, and sales taxes. Thank you.

| State | Collections per Capita | Rank |

|---|---|---|

| Source: U.S. Census Bureau | ||

| District of Columbia | $3,535 | |

| New Jersey | $3,127 | 1 |

| New Hampshire | $3,115 | 2 |

| Connecticut | $2,927 | 3 |

| New York | $2,782 | 4 |

| Vermont | $2,593 | 5 |

| Rhode Island | $2,415 | 6 |

| Wyoming | $2,393 | 7 |

| Massachusetts | $2,357 | 8 |

| Illinois | $2,120 | 9 |

| Maine | $2,105 | 10 |

| Alaska | $2,047 | 11 |

| Nebraska | $1,909 | 12 |

| Texas | $1,762 | 13 |

| Wisconsin | $1,629 | 14 |

| Iowa | $1,582 | 15 |

| Minnesota | $1,567 | 16 |

| California | $1,559 | 17 |

| Maryland | $1,547 | 18 |

| Virginia | $1,545 | 19 |

| Montana | $1,520 | 20 |

| Kansas | $1,490 | 21 |

| Pennsylvania | $1,478 | 22 |

| Oregon | $1,444 | 23 |

| Washington | $1,436 | 24 |

| Colorado | $1,425 | 25 |

| Michigan | $1,413 | 26 |

| South Dakota | $1,394 | 27 |

| North Dakota | $1,296 | 28 |

| Ohio | $1,264 | 29 |

| Florida | $1,263 | 30 |

| South Carolina | $1,164 | 31 |

| Georgia | $1,159 | 32 |

| Hawaii | $1,140 | 33 |

| Arizona | $1,062 | 34 |

| Utah | $1,019 | 35 |

| Nevada | $994 | 36 |

| Mississippi | $988 | 37 |

| North Carolina | $975 | 38 |

| Missouri | $971 | 39 |

| Indiana | $967 | 40 |

| Idaho | $944 | 41 |

| West Virginia | $915 | 42 |

| Louisiana | $887 | 43 |

| Delaware | $860 | 44 |

| Tennessee | $836 | 45 |

| Kentucky | $775 | 46 |

| New Mexico | $768 | 47 |

| Arkansas | $712 | 48 |

| Oklahoma | $699 | 49 |

| Alabama | $548 | 50 |