Two major provisions in the federal taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code have been limited since the Tax Cuts and Jobs Act (TCJA) of 2017: the state and local tax (SALT) deductionThe state and local tax (SALT) deduction permits taxpayers who itemize when filing federal taxes to deduct certain taxes paid to state and local governments. The Tax Cuts and Jobs Act (TCJA) capped it at $10,000 per year, consisting of property taxes plus state income or sales taxes, but not both. and the home mortgage interest deduction (MID). Limiting the two provisions helped broaden the tax base, offsetting tax revenue loss from reduced tax rates. The limitations are slated to expire at the end of 2025, but policymakers should consider extending them along with the lower tax rates.

Taxpayers generally have two options for income tax deductions, which reduce a taxpayer’s taxable income: a standard deduction, which is a fixed deduction amount set by the government ($12,550 for single filers and $25,100 for joint filers in 2021), or itemized deductions, which allow individuals to subtract designated expenses from their taxable income in lieu of the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative..

Among itemized deductions are the MID, which grants homeowners the ability to deduct mortgage interest paid on either their first or second residence. The TCJA limited the interest deduction to the first $750,000 in principal value, down from $1 million. Another itemized deductionItemized deductions allow individuals to subtract designated expenses from their taxable income and can be claimed in lieu of the standard deduction. Itemized deductions include those for state and local taxes, charitable contributions, and mortgage interest. An estimated 13.7 percent of filers itemized in 2019, most being high-income taxpayers. is the SALT deduction, which grants individuals the ability to deduct state and local taxes against their federal taxable income. The TCJA limited the SALT deduction to $10,000.

While the deductibility of mortgage interest moves the tax treatment of residential real estate closer to a consumption tax, there are still critiques of the MID. High-income taxpayers are more likely to itemize their returns and are often the main beneficiaries of this deduction. The real value of the MID also increases with the value of the home, making the benefits even more concentrated among wealthy individuals.

Increased demand spurred by the MID can also lead to increased housing costs, mainly among taxpayers who itemize, making the housing market less accessible more broadly. Critics of the change suggested it could result in less mortgage participation, hurt the middle class, and reduce the homeownership rate. However, we find little evidence supporting these claims. After 2025, MID claims may increase as TCJA’s limitation expires.

The SALT deduction is similar to the MID in that it is another itemized deduction limited by the TCJA. Prior to the TCJA, individuals could deduct an unlimited amount of state and local income or sales taxes, real estate taxes, and personal property taxes against their federal taxable income. Post-TCJA, the SALT deduction is capped at $10,000 for income, sales, and property taxes (unless they were related to business activity). The cap made the tax code more progressive by broadening the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates., and it helped partially fund reductions in statutory tax rates. Repeal of the SALT deduction cap would be more regressive than the entirety of the TCJA and provide a $31,000 tax cut for the top 1 percent of earners.

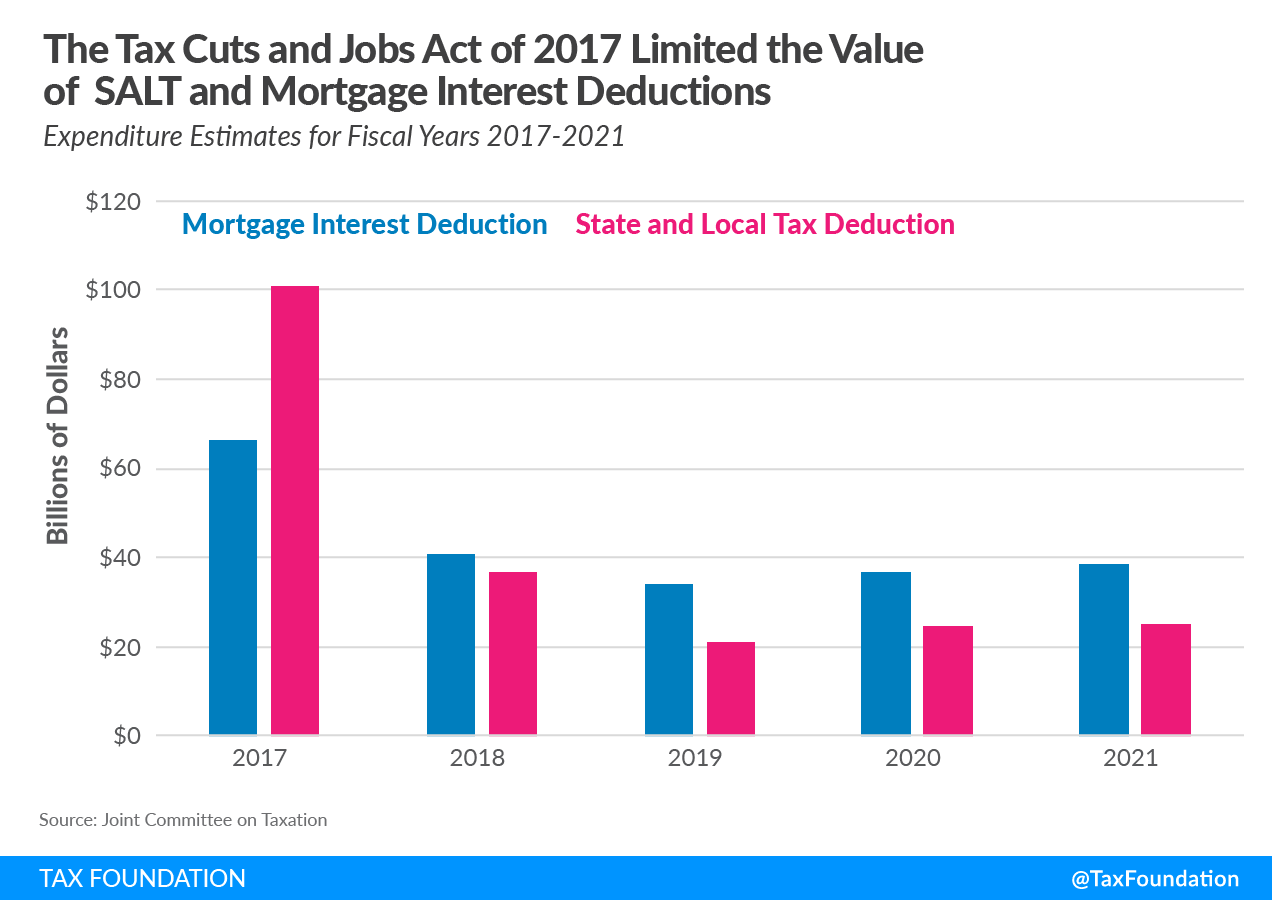

Given the changes to the MID and SALT deductions in the TCJA, one would expect a sizable decrease in those tax expenditures for fiscal years after the passage of the bill. Tax expenditureTax expenditures are departures from a “normal” tax code that lower the tax burden of individuals or businesses through an exemption, deduction, credit, or preferential rate. However, defining which tax expenditures grant special benefits to certain groups of people or types of economic activity is not always straightforward. estimates from the Joint Committee on Taxation (JCT) indeed show that: estimated claims for the MID fell from $66.4 billion in 2017 to $38.7 billion in 2021 and for the SALT deduction, from $100.9 billion in 2017 to $25.2 billion in 2021. Rather than making these limitations more generous or repealing them early, policymakers should consider keeping these limitations in place.

Share this article