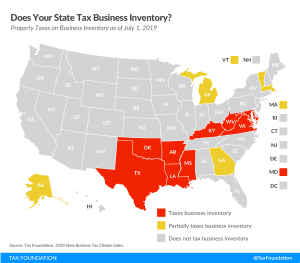

Does Your State Tax Business Inventory?

Inventory taxes are levied regardless of whether a business makes a profit, adding to the burden of businesses already struggling to stay afloat.

2 min read

Inventory taxes are levied regardless of whether a business makes a profit, adding to the burden of businesses already struggling to stay afloat.

2 min read

The OECD recently announced that the negotiation timeline for new digital tax proposals has now been pushed back to October due to the COVID-19 pandemic, although the end-of-year deadline for the overall project is still in place.

5 min read

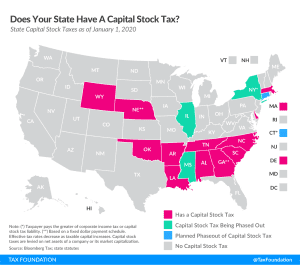

As many businesses may need time to return to profitability after this crisis, states should prioritize reducing reliance on capital stock taxes, and shift toward more neutral forms of business taxation.

4 min read

Permanent full expensing for all types of investment is an effective policy change lawmakers can use to encourage additional investment and economic growth.

9 min read

One of the most cost-effective policy changes would be to make full expensing of machinery and equipment permanent and extend this important tax treatment to structures as well as for firms in a net operating loss position.

7 min read

Virginia enacted a biennial budget, which includes a new excise tax on “skill games.” Meanwhile, Arizona and Connecticut announced plans to convene in special sessions later this year while Oklahoma gets the green light to use rainy day fund money to close budget gaps.

4 min read

Alaska and North Dakota collect revenue primarily from oil-related taxes. These states must start thinking about how to plan for an era of reduced oil revenue.

5 min read

As states look for a path out of these fiscally troubling times, Louisiana has several options for aspects of its tax code to promote economic recovery and growth. The Pelican State’s federal deductibility, Corporation Franchise Tax, and sales tax structure present opportunities for beneficial tax reform in the wake of the coronavirus crisis.

3 min read

What could the next phase of relief look like and what role does tax policy play in ensuring the U.S. and countries around the world make a strong economic recovery?

1 min read

The U.S. Department of the Treasury recently issued new guidance on allowable expenses using the $150 billion in state aid provided under the CARES Act, a point on which there has been considerable confusion.

3 min read

The sooner federal policymakers or regulators clarify tax questions about the Paycheck Protection Program (PPP), the more certainty firms will have when they accept the economic relief to keep their businesses afloat.

3 min read

When businesses and taxpayers look to the government for relief, it is paramount that lawmakers do their best to craft transparent and coherent legislation that is the least confusing for all.

4 min read

While it’s unclear how soon state economies may be able to fully open again, it’s not too early for states to consider how they can remove barriers to businesses & consumers resuming activity.

3 min read

Governments at all levels must work to remove the tax policy barriers that stand in the way of economic recovery and long-term prosperity following the COVID-19 crisis. Our new guide outlines several comprehensive options that policymakers can take at the federal and state levels.

26 min read

On July 1, sales taxes levied on internet access in six states—Hawaii, New Mexico, Ohio, South Dakota, Texas, and Wisconsin—will become illegal under the provisions of the Permanent Internet Tax Freedom Act (PITFA)

4 min read

We examine whether excise taxes are a solution to budget deficits, and while the short answer to that question is no, there are of course nuances. Excise taxes can play a role in state revenues even as policymakers appreciate that excise taxes are not viable long-term revenue tools for general spending priorities.

21 min read