Under the federal individual alternative minimum taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. (AMT), many taxpayers are required to calculate their income tax liability under two different systems and pay the higher amount. Established in 1969, the federal AMT was created when Congress discovered that 155 high-income taxpayers were eligible to claim so many deductions that they ended up with no federal income tax liability at all. Under the federal AMT, the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. is disallowed, and certain itemized deductions—including the state and local tax (SALT) deduction—are added back, recapturing income from taxpayers who would otherwise be eligible to claim them.

While the federal AMT was originally intended to be a narrow fix to a narrow problem, it was not indexed for inflation. As a result, it wasn’t long before many middle-income taxpayers found themselves having to calculate and pay an AMT. After the federal AMT was adopted, several states followed suit. This meant that some taxpayers were required to calculate their tax liability four times: twice under the federal code and twice under their state’s code.

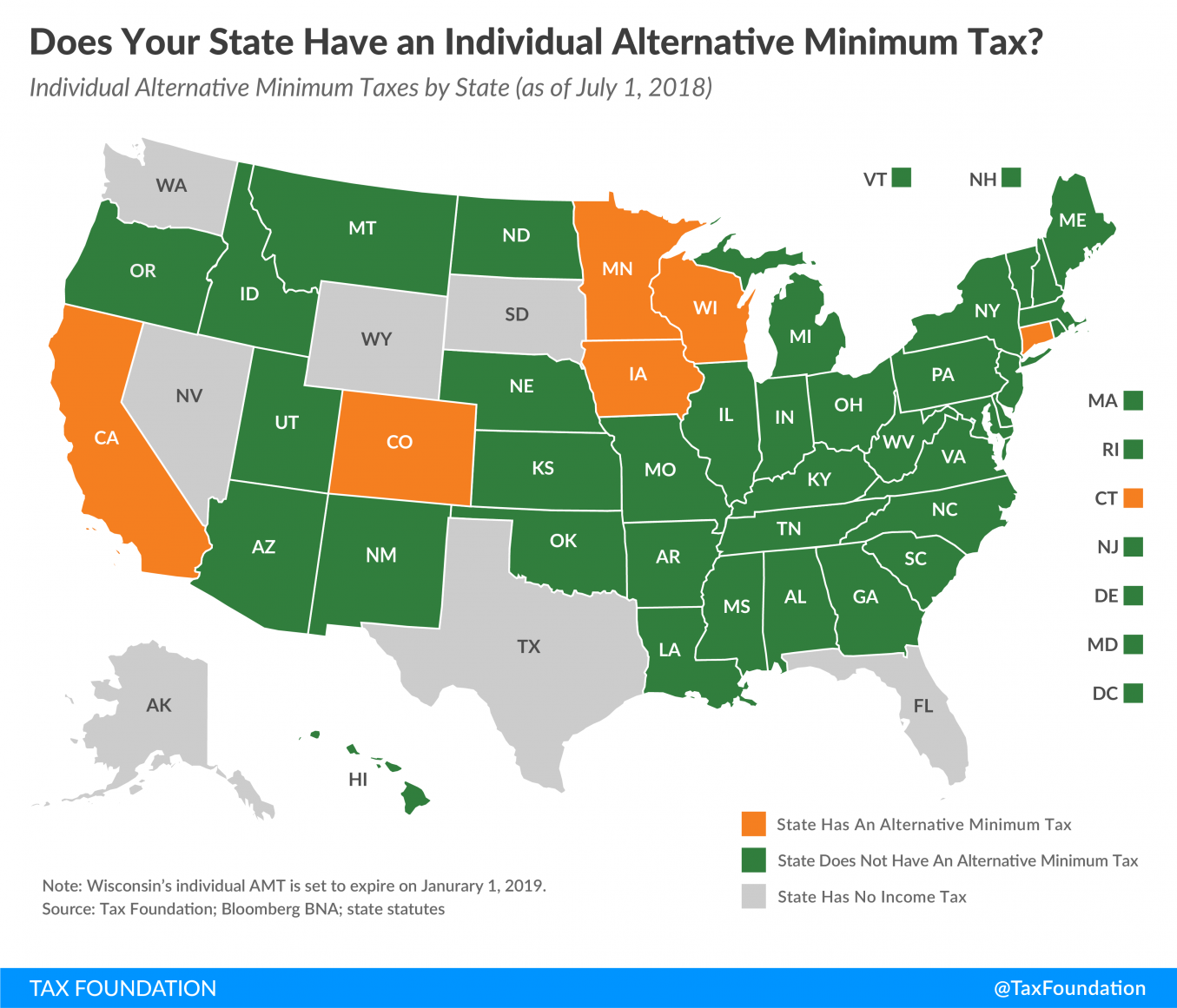

Today, six states have an AMT in their individual income tax code: California, Colorado, Connecticut, Iowa, Minnesota, and Wisconsin. (Wisconsin adopted AMT repeal in 2017, effective starting in tax year 2019.)

Additionally, the Tax Cuts and Jobs Act increased the federal AMT’s exemption amounts and phaseout thresholds through 2025, meaning fewer taxpayers will be required to calculate and pay the federal AMT in forthcoming years. In states that conform to the federal provision or use it as the basis for their own calculation, fewer filers will be subject to the AMT—for now. Unless Congress chooses to extend it, the higher exemption amounts will sunset after 2025, a change that will also impact state tax codes.

The original goal of AMTs—to prevent deductions from eliminating income tax liability altogether—can best be accomplished not through an alternative tax (which adds complexity and lacks transparency and neutrality), but through simplifying the existing tax structure.