Expert

Janelle Fritts

Senior Policy Analyst

Janelle Fritts is a Senior Policy Analyst with the Tax Foundation’s Center for State Tax Policy. She is the lead researcher on the annual State Tax Competitiveness Index and serves as a resource to policymakers in their efforts to modernize and improve the structures of their state tax codes. Her work has been cited in The New York Times, the Associated Press, Bloomberg, and numerous state media outlets across the country.

Janelle has been with the Tax Foundation since 2019, with a brief hiatus to teach high school literature, logic, and rhetoric. Before joining the state team, she interned at the Mackinac Center for Public Policy, the Reason Foundation, and the Illinois Policy Institute. She graduated from Dordt University (Sioux Center, Iowa) with a bachelor’s degree in English with a writing emphasis and a minor in Chemistry.

Born and raised in Midland, Michigan, Janelle now lives in Reston, Virginia. In her free time, she enjoys baking, thrifting, and spending time with her husband and infant daughter.

Latest Work

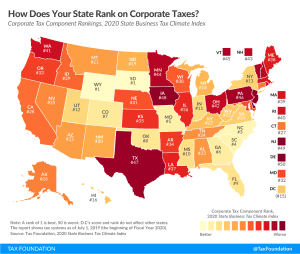

State Corporate Income Tax Rates and Brackets, 2020

Forty-four states currently levy a corporate income tax. Rates range from 2.5 percent in North Carolina to 12 percent in Iowa. Over the past year, several states, including Florida, Georgia, Indiana, Mississippi, Missouri, and New Jersey, implemented notable corporate income tax changes.

7 min read

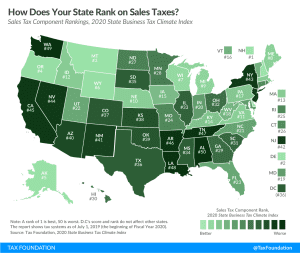

State and Local Sales Tax Rates, 2020

While many factors influence business location and investment decisions, sales taxes are something within lawmakers’ control that can have immediate impacts.

12 min read

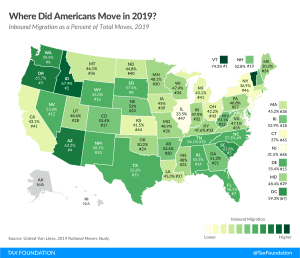

Where Did Americans Move in 2019?

3 min read

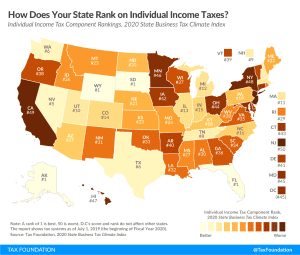

State Sales Taxes in the Post-Wayfair Era

Our new report explores the choices states have made regarding sales taxes following the South Dakota v. Wayfair Supreme Court online sales tax decision heading into calendar year 2020, outlines legal pitfalls states should seek to avoid, and offers up a few best practices for designing reliable, equitable, legally-sound remote sales tax regimes.

58 min read

Kansas Tax Modernization: A Framework for Stable, Fair, Pro-Growth Reform

Our new report outlines various policy recommendations for Kansas to consider in order to begin a robust and bipartisan conversation about modernizing the state’s tax code to suit a 21st century economy.

15 min read