All Related Articles

2018 International Tax Competitiveness Index

The structure of a country’s tax code is an important determinant of its economic performance. Our 2018 international tax rankings provide a road map for each of the 35 OECD countries to improve the structure of their tax codes and achieve a more neutral, more competitive tax system.

11 min read

2019 State Business Tax Climate Index

Our 2019 State Business Tax Climate Index compares each state on over 100 variables including corporate, individual, property, and sales taxes. How does your state rank?

17 min read

The Economics of Stock Buybacks

Stock buybacks are readily visible, and unfortunately some have misunderstood stock buybacks to be taking place at the expense of long-term investments.

17 min read

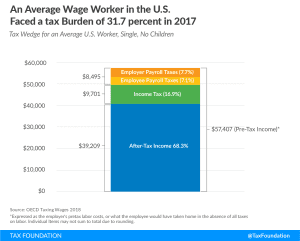

A Comparison of the Tax Burden on Labor in the OECD, 2018

Before accounting for state and local sales taxes, the tax burden that a single average wage earner faces in the U.S. is 31.7 percent of pretax earnings, amounting to $18,198 in taxes in 2017.

18 min read

The TCJA’s Expensing Provision Alleviates the Tax Code’s Bias Against Certain Investments

The Tax Cuts and Jobs Act made significant progress in improving businesses’ ability to recover the cost of making investments in the United States by enacting 100 percent bonus depreciation.

11 min read

Pennsylvania: A 21st Century Tax Code for the Commonwealth

Policymakers from across the spectrum recognize that Pennsylvania’s tax code has not kept up with a 21st century economy. Here are comprehensive solutions for how Pennsylvania can achieve a more competitive tax code.

13 min read

Post-Wayfair Options for States

What is included in the “Wayfair checklist,” what policy choices do legislators have to make their state compliant, and, ultimately, how prepared is each state to start requiring that online retailers collect sales tax?

42 min read

Reviewing Different Methods of Calculating Tax Compliance Costs

Tax compliance creates real costs, which can be calculated. Each method provides unique illustrations of the cost of complying with U.S. tax code.

11 min read

State Tax Implications of Federal Tax Reform in Virginia

Virginia has an opportunity to improve its tax competitiveness following the Tax Cuts and Jobs Act. Inaction will result in higher taxes.

14 min read

The Benefits of Cutting the Corporate Income Tax Rate

The Tax Cuts and Jobs Act reduced the corporate income tax rate from the highest statutory rate in the developed world to a more globally competitive 21 percent.

13 min read

The Tax Cuts and Jobs Act Simplified the Tax Filing Process for Millions of Households

The newly expanded standard deduction will reduce the time taxpayers spend working on Form 1040 by 4 to 7 percent, translating into $3.1 to $5.4 billion saved annually.

15 min read

Online Sales Tax Revenue Presents Opportunity for Permanent, Comprehensive Reform in Wisconsin

Wisconsin’s tax system needs to be more competitive. New revenue from online sales taxes will make it easier to accomplish comprehensive reforms that benefit all Wisconsinites.

13 min read

Enhancing Tax Competitiveness in Connecticut

Connecticut has failed to live up to the expectations of 1991. Changes intended to make tax collections more stable, combined with constraints intended to promote fiscal prudence, have strayed far wide of the mark. To turn things around, Connecticut needs a more competitive tax code.

32 min read