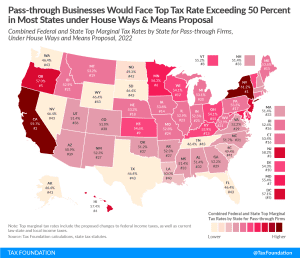

How Would House Dems’ Tax Plan Change Competitiveness of U.S. Tax Code?

The legislation put forward by Democratic members of the House of Representatives would reverse many of the 2017 reforms while increasing burdens on businesses and workers.

2 min read